.webp)

Are chargebacks and credit memos causing you headaches in your business operations? Understanding the Differences between Chargeback and Credit Memo will help you navigate these terms more precisely.

Running a business can be tough, and dealing with chargebacks and credit memos can make it even tougher. These financial transactions can be confusing, and if not handled correctly, they can hurt your bottom line.

But don't worry, we've got your back. In this article, we're going to break down the differences between chargebacks and credit memos in simple terms that you can easily grasp. No more scratching your head when these terms come up. We're here to make it crystal clear for you.

Whether you're a small business owner or a finance professional, understanding these concepts is crucial. Chargebacks and credit memos can impact your revenue, customer relationships, and overall financial health.

So, let's get going to understand these financial processes, so you can get back to doing what you do best—running your business smoothly and efficiently.

What is a Chargeback (A Debit Memo)?

A chargeback, sometimes also called a debit memo, is a transaction reversal process in which a customer asks their bank to reverse a charge on their credit or debit card.

It means the money that was initially paid to a merchant gets taken back from them. It's important for you, as a merchant, to understand how chargebacks work.

1. How Chargebacks Happen

Chargebacks usually happen when a customer is not satisfied with a purchase. Instead of contacting the merchant directly, they go to their bank and request a chargeback.

Common reasons for chargebacks include receiving a damaged or incorrect product, not getting what was promised, or unauthorized transactions.

2. Why Chargebacks Matter for Merchants

Chargebacks can be a headache for merchants. When a chargeback occurs, the disputed amount is temporarily taken out of your account, and you may also face additional fees.

Too many chargebacks can hurt your business's reputation and even lead to your account being terminated by payment processors.

What is a Credit Memo?

A credit memo is like a helpful note in the world of business. It's something you send to a customer when you owe them money or need to give them credit for something they bought from you.

1. What's Inside a Credit Memo?

Inside a credit memo, there's some basic info you need to include. First, there's the date when you're sending it out as it helps everyone keep track of things. Then, you put in your business name and contact info.

Next up, you list the customer's info - their name and how to reach them. You want to make sure they know where this credit memo is coming from.

Now, the most important part: what's the credit memo for? You write down the details of why you're giving them money back or what they're getting credit for.

And of course, you have to include the numbers. That means how much they're getting back and why. You want it to be clear as day.

2. Why Use Credit Memos?

Credit memos are pretty handy for businesses. They keep things organized and show that you're on top of your game. Plus, it's like a little thank-you note to your customer. It shows you care about them and their business.

3. When to Use Credit Memos

You use a credit memo when you need to:

- Refund Money: Maybe the customer paid too much or wants to return something. A credit memo lets you give their money back.

- Fix Mistakes: If you made an error on their bill, a credit memo sets things straight.

- Give Credits: Sometimes, customers buy more than they use. You can give them credit for their next purchase.

4. How to Send a Credit Memo

Now, sending a credit memo isn't rocket science. You can send it through email or good old snail mail. Just make sure it gets to your customer.

7 Key Differences Between Chargebacks and Credit Memos

Being a merchant, it's crucial to understand the key differences between chargebacks and credit memos. These two financial transactions may seem similar at first glance, but they serve distinct purposes and have significant implications for your business.

Let's break down the important contrasts:

1. Definition

- Chargeback: A chargeback is a forced transaction reversal initiated by the customer's bank or credit card company due to a dispute. It's essentially a refund that bypasses you, the merchant.

- Credit Memo: A credit memo is a voluntary refund or credit issued by you, the merchant, directly to the customer. It's a goodwill gesture or a resolution for an issue.

2. Initiation

- Chargeback: Customers initiate chargebacks by disputing a transaction with their bank. Common reasons include unauthorized transactions, fraud, or dissatisfaction with the product or service.

- Credit Memo: Merchants initiate credit memos as a proactive step to address customer concerns or issues, such as defective products or billing errors.

3. Decision-Maker

- Chargeback: The decision to grant or deny a chargeback is made by the customer's bank or credit card company after reviewing evidence from both parties.

- Credit Memo: You, as the merchant, have full control over issuing credit memos to customers.

4. Dispute Resolution

- Chargeback: Chargebacks are often more adversarial, involving a dispute process where you can submit evidence to defend the transaction.

- Credit Memo: Credit memos are a means of resolving issues amicably, promoting customer satisfaction, and maintaining goodwill.

5. Financial Responsibility

- Chargeback: In the case of a chargeback, the financial responsibility falls on the merchant. You may lose the sale, incur chargeback fees, and risk damage to your reputation.

- Credit Memo: With credit memos, you voluntarily refund a portion or the full amount to the customer, taking responsibility for any errors or issues.

6. Impact on Chargeback Ratio

- Chargeback: Excessive chargebacks can harm your business by increasing your chargeback ratio, potentially leading to higher processing fees and the loss of your merchant account.

- Credit Memo: Credit memos generally do not impact your chargeback ratio, as they are seen as a positive resolution.

7. Customer Communication

- Chargeback: The customer may not always communicate with you directly when initiating a chargeback, leading to missed opportunities for resolution.

- Credit Memo: Credit memos encourage direct communication with customers, allowing you to address concerns and build trust.

%252520(2).webp)

In short, while chargebacks and credit memos both involve refunds, they differ significantly in terms of initiation, control, and purpose. Understanding these distinctions is essential for effective financial management and customer relations in your business.

Understanding the Chargeback Process

For merchants, understanding the chargeback process is crucial in managing disputes with customers and protecting their businesses.

Here, we'll go through the step-by-step guide to the chargeback process, helping you navigate this often complex aspect of business operations.

1. Customer Disputes a Transaction

The chargeback process typically begins when a customer disputes a transaction with their bank or credit card company.

This dispute can arise due to various reasons, such as unauthorized charges, defective products, or billing errors. When a customer initiates a dispute, it triggers the chargeback process.

2. The Bank Reviews the Dispute

Once the customer files a dispute, their bank reviews the case. They'll assess the validity of the customer's claim and gather relevant information, including transaction records, receipts, and communication between the customer and the merchant.

3. The Bank Notifies the Merchant

If the customer's claim is deemed valid, the bank notifies the merchant about the dispute. At this stage, you'll receive a chargeback notification, which includes details of the disputed transaction, the reason for the dispute, and the customer's supporting documentation.

4. Merchant's Response

As a merchant, you have the opportunity to respond to the chargeback. You'll need to provide compelling evidence to support your case.

This evidence may include order confirmations, shipping receipts, and any correspondence with the customer. It's crucial to respond promptly and with all necessary documentation.

5. Bank Reviews Merchant's Response

Once the merchant submits their response, the bank reviews the provided evidence and assesses the legitimacy of the merchant's claims. They will consider both the customer's and the merchant's arguments before making a decision.

6. Resolution

After a thorough review, the bank will make a final decision. There are three possible outcomes:

I. Chargeback Accepted

If the bank determines that the customer's claim is valid, the transaction amount is refunded to the customer, and the merchant bears the cost.

II. Chargeback Rejected

If the bank finds in favor of the merchant, the customer is not refunded, and the merchant retains the funds.

III. Arbitration

In some cases, disputes may require further investigation or arbitration by the credit card company or an external party.

7. Communication with the Customer

Throughout the process, it's important to maintain open and respectful communication with the customer.

Clear and timely responses can sometimes prevent disputes from escalating to chargebacks. Keep records of all communications for reference.

8. Preventing Future Chargebacks

To reduce the likelihood of chargebacks, consider implementing preventive measures. These may include improving customer service, providing detailed product descriptions, offering a clear return policy, and using secure payment processing systems.

Understanding the Credit Memo Process

you need to know how the credit memo process works because it can greatly benefit your business.

A credit memo is like a promise you make to your customer, saying you'll give them credit for a certain amount. This can happen for various reasons, like returns, damaged goods, or overcharges.

Here's how the credit memo process typically works:

1. Initiating the Credit Memo

When an issue arises, like a customer returning a product, you start the credit memo process. You gather all the necessary information, such as the customer's name, the product details, and the reason for the credit.

2. Documentation is Key

Proper documentation is crucial. You create a credit memo document that includes all the details about the transaction. This document should be clear and easy to understand, with no room for confusion.

3. Approval Process

Depending on your business's size and structure, the credit memo might need approval. Usually, it goes through relevant departments like sales, finance, and management to ensure accuracy and legitimacy.

4. Adjusting Your Books

Once approved, you make the necessary adjustments in your accounting books. This typically involves reducing the revenue and recording the credit amount as a liability.

5. Issuing the Credit

After all the approvals and accounting entries are done, you issue the credit memo to your customer. This can be in the form of a physical document or an electronic one, depending on your business processes.

6. Communication

It's essential to communicate with your customer throughout this process. Let them know that you've acknowledged their concern and the credit is on its way. This builds trust and shows your commitment to customer satisfaction.

7. Application of Credit

When the customer makes their next purchase, they can apply the credit to reduce their bill. It's crucial to track and manage these credits to ensure they're used correctly.

8. Monitoring and Reporting

Keep an eye on your credit memos and analyze them regularly. This helps you identify trends or recurring issues that might need attention, such as a particular product with frequent returns.

9. Legal Compliance

Make sure your credit memo process complies with relevant laws and regulations. This is especially important when dealing with sensitive customer data or offering refunds.

10. Continuous Improvement

Lastly, always strive to improve your credit memo process. Look for ways to streamline it, reduce errors, and enhance customer satisfaction. This will benefit both you and your customers in the long run.

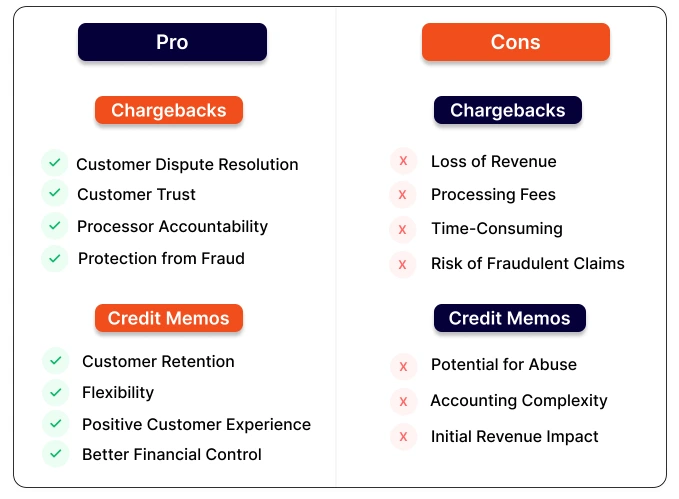

Chargebacks vs. Credit Memos: Pros and Cons

Merchants, let's get into the pros and cons of chargebacks and credit memos, so you can better understand which option works best for your business.

4 Pros of Chargebacks

1. Customer Dispute Resolution

Chargebacks help resolve disputes between you and your customers. If they claim an unauthorized transaction, chargebacks can investigate and provide a resolution.

2. Customer Trust

Offering chargebacks can build trust with customers. Knowing they have recourse if something goes wrong can make them more comfortable making purchases from your business.

3. Payment Processor Responsibility

In many cases, the responsibility for handling chargebacks falls on the payment processor, freeing you from the administrative burden.

4. Protection from Fraud

Chargebacks offer protection against fraudulent transactions. If you spot a suspicious transaction, you can initiate a chargeback to investigate and potentially recover the funds.

4 Cons of Chargebacks:

1. Loss of Revenue

The most significant downside of chargebacks is the potential loss of revenue. When a chargeback is approved, you lose both the sale and the merchandise.

2. Processing Fees

Chargebacks can come with processing fees. These fees can add up, especially if your business faces frequent disputes.

3. Time-Consuming

The chargeback process can be time-consuming, requiring you to gather evidence and respond to inquiries. This can divert your resources from other business operations.

4. Risk of Fraudulent Claims

Some customers may abuse chargebacks for personal gain, making false claims and potentially harming your business's reputation.

4 Pros of Credit Memos:

1. Customer Retention

Credit memos offer a way to address customer complaints while retaining their loyalty. Instead of losing a sale, you can issue a credit that encourages future purchases.

2. Flexibility

Credit memos are flexible. You can offer partial or full credits, allowing you to tailor solutions to individual customer issues.

3. Positive Customer Experience

Offering a credit memo shows that you value your customers and are willing to make amends when necessary, contributing to a positive customer experience.

4. Better Financial Control

With credit memos, you have more control over your finances. You decide when and how to issue credits, helping you manage your cash flow.

3 Cons of Credit Memos:

1. Potential for Abuse

While credit memos can improve customer relations, there's a risk of customers abusing the system to get free credits for unwarranted complaints.

2. Accounting Complexity

Handling credit memos can add complexity to your accounting processes. You need to ensure accurate documentation and tracking of credits.

3. Initial Revenue Impact

Issuing a credit memo means not receiving immediate revenue for the sale, which can impact short-term cash flow.

15 Best Practices for Managing Chargebacks and Credit Memos

Managing chargebacks and credit memos effectively is crucial for merchants like you. These best practices can help you navigate these financial transactions smoothly:

1. Understand the Reasons

To manage chargebacks and credit memos well, it's vital to grasp why they happen. Familiarize yourself with the common reasons customers initiate chargebacks and businesses issue credit memos.

2. Maintain Detailed Records

Keep meticulous records of all transactions, including invoices, receipts, and communication with customers. This documentation will be invaluable when dealing with chargebacks and credit memos.

3. Deliver Outstanding Customer Service

Offering excellent customer service can prevent disputes. Be responsive to customer inquiries and complaints. Resolve issues promptly to reduce the likelihood of chargebacks.

4. Set Clear Policies

Clearly define your refund and return policies on your website and in your terms of service. Make sure customers are aware of these policies at the time of purchase.

5. Monitor Transactions

Regularly monitor your transactions for any suspicious or unusual activity. This can help you detect and prevent fraudulent chargebacks.

6. Use Advanced Payment Verification Tools

Implement advanced verification tools to confirm the legitimacy of transactions. These tools can help reduce fraudulent chargebacks.

7. Train Your Staff

Train your staff to handle chargebacks and credit memos professionally. They should be well-informed about your company's policies and procedures.

8. Respond Promptly

When you receive a chargeback or need to issue a credit memo, respond promptly. Meeting deadlines and adhering to procedures are essential to a successful resolution.

9. Be Transparent

Maintain transparency throughout the process. Provide all necessary information and evidence to support your case when responding to chargebacks.

10. Automate Where Possible

Consider automating parts of your chargeback and credit memo management process. Automation can help streamline tasks and reduce human error.

11. Regularly Review and Update Policies

Stay up-to-date with industry regulations and customer expectations. Regularly review and update your policies to ensure they remain effective.

12. Seek Professional

Help If you're facing complex chargeback issues, consider consulting with experts or legal professionals specializing in dispute resolution. They can provide valuable guidance.

13. Monitor Chargeback Ratios

Keep an eye on your chargeback ratios. High chargeback ratios can lead to penalties from payment processors. Take corrective action if necessary.

14. Implement Fraud Prevention

Measures Utilize fraud prevention measures like address verification and card security codes. These measures can deter fraudulent transactions.

15. Educate Your Customers

Educate your customers about the chargeback process and when it's appropriate to contact your support team. Clear communication can prevent misunderstandings.

By following these best practices, you can effectively manage chargebacks and credit memos, ultimately safeguarding your business's financial health and reputation. Remember that proactive management is key to minimizing the impact of these financial transactions on your bottom line.

Win Hassle Free Chargeback With ChargePay

Winning chargebacks has never been easier than with ChargePay. Our hassle-free chargeback solution leverages the power of AI to contest and win disputes effortlessly. Say goodbye to the time-consuming manual efforts and let ChargePay handle it all for you.

.webp)

With real-time responses and AI-generated representments, we consistently achieve remarkable win rates, recovering up to 80% of your previously lost revenue. Don't let chargebacks burden your business any longer – choose ChargePay for a stress-free, hands-free approach to reclaiming what's rightfully yours.

.svg)

.svg)

.svg)

.svg)