Yes, you can absolutely file a chargeback for a debit card, and it's one of the most important tools you have as a consumer. Think of it as calling in a referee—your bank—to step in and reverse a transaction when a purchase goes sideways. It’s how you get your money back for things like fraudulent charges or goods that never showed up.

What Is a Debit Card Chargeback, Really?

Ever checked your bank statement and felt that gut-sinking feeling when you spot a charge you know you didn't make? It happens to the best of us, but you're not helpless. A debit card chargeback is your formal right to dispute that transaction, empowering your bank to forcibly take the money back from the merchant’s account and put it right back into yours.

This isn't the same as asking a merchant for a refund. A refund is a request the business can approve or deny. A chargeback, on the other hand, is a formal process kicked off through your bank.

The crucial difference from a credit card dispute is that a debit card transaction uses your actual cash, pulled directly from your checking account. This makes understanding the process—and acting quickly—that much more important.

Who Is Involved in the Process?

When you file a chargeback for a debit card, a few key players get involved. It's no longer just a two-way street between you and the business.

Here's the lineup:

- You (The Cardholder): Your job is to spot the problem, gather your proof, and report it to your bank.

- Your Bank (The Issuing Bank): They review your claim. If it looks legitimate, they'll start the formal chargeback process on your behalf.

- The Merchant: The business that charged you gets a chance to respond and prove the transaction was valid.

- The Merchant's Bank (The Acquiring Bank): This bank defends the merchant and works to challenge your dispute.

Key Takeaway: A debit card chargeback elevates a dispute from a simple customer service issue to a formal, bank-mediated process. It's a safety net designed to protect you when a merchant can't or won't help.

Why It Matters

The whole chargeback system was built to create trust in electronic payments. Without it, you'd be taking a massive risk every time you swiped your debit card. Knowing you can dispute an unauthorized charge or a transaction for an item you never received gives you the confidence to shop online and in stores.

But this process has a huge impact on businesses, too. They face fees and penalties for every dispute filed against them. Because of this, merchants take these claims very seriously, and a well-managed dispute process is critical for them. You can learn more about how businesses handle this from their side by exploring the details of chargeback management.

In the next sections, we'll dive into exactly when you can file a dispute and the steps you need to follow.

Valid Reasons to File a Debit Card Chargeback

When most people hear "debit card chargeback," they immediately think of clear-cut fraud—like a thief swiping their card details online. And while that’s a huge reason the system exists, the actual grounds for a valid dispute are much broader than you might think. You have the right to challenge a transaction anytime a business fails to hold up its end of the deal.

Think of it like a handshake agreement. When you pay for something, you and the merchant have a mutual understanding. If they break their promise, a chargeback is your tool to enforce that agreement and ensure you don’t get left holding the bag for someone else's mistake.

Common Legitimate Dispute Scenarios

Let's get out of the abstract and into the real world. You might be surprised by how many frustrating but common situations fully justify filing a debit card chargeback.

Here are some of the most frequent valid reasons you might encounter:

- Goods or Services Not Received: You ordered that new standing desk for your home office, but weeks have passed, and it's a no-show. The company has gone silent. Time to file a chargeback.

- Item Significantly Not as Described: The "genuine leather" bag you bought online arrives, and it's obviously cheap plastic. It’s not what you paid for, and the seller is refusing a return.

- Defective or Damaged Product: You finally get that new blender, but it arrives with a cracked base or just won't turn on. If the merchant won't help with a replacement or refund, a chargeback is your next logical step.

- Incorrect Transaction Amount: Your dinner bill was $50, but when you check your statement, you see a charge for $500. This is a classic processing error your bank can help fix.

- Duplicate Billing: You were accidentally charged twice for the same pair of concert tickets. You're entitled to get that second charge reversed.

- Recurring Subscription Issues: You followed all the steps to cancel your gym membership, but they just keep billing your debit card every month. Each one of those unauthorized charges is a valid reason for a dispute.

The Problem of "Friendly Fraud"

While the chargeback system is an incredible tool for consumer protection, it's vital to use it ethically. A major headache for businesses is a problem called "friendly fraud," which is when a customer disputes a completely legitimate charge.

This isn't always malicious—sometimes a customer simply forgets about a purchase or doesn't recognize the business name on their bank statement. Other times, though, it’s an intentional attempt to get a product or service for free.

Friendly fraud is a massive issue, accounting for a staggering 80% of all chargebacks. It creates huge financial losses and operational nightmares for merchants.

It’s not a victimless action. Abusing the system can have real consequences. A business you file an improper chargeback against has every right to refuse to sell to you in the future. They might even report your information to databases that flag high-risk customers for other merchants.

Before you jump to filing a dispute, always try to resolve the issue with the merchant first. A chargeback for a debit card should be your final move after you’ve given the business a fair shot to make it right.

Your Step-by-Step Guide to Filing a Dispute

Feeling overwhelmed and ready to get your money back? Knowing the right way to file a chargeback for a debit card can turn a genuinely stressful situation into a manageable one. Think of it less like a confrontation and more like a clear, methodical process to make things right.

Your first move, surprisingly, might not be to ring up your bank. Most banks and financial institutions actually want to see that you've made a good-faith effort to solve the problem directly with the merchant first. A quick phone call or a clear, polite email can often sort things out without ever needing a formal dispute.

But what if the merchant is unresponsive, flat-out refuses to help, or you’re certain you're dealing with fraud? That’s when it’s time to start the official chargeback process. And when you do, you need to act fast.

Gathering Your Evidence

Before you even think about contacting your bank, you need to build your case. Picture yourself as a detective putting together a file for court. The more organized and convincing your evidence is, the better your shot at winning the dispute. Your one and only goal here is to prove the charge was not legitimate.

Here’s the essential proof you’ll want to collect:

- Receipts and Invoices: The basic proof of purchase, showing the date, amount, and exactly what you bought.

- Email or Chat Transcripts: Any and all communication with the merchant, especially where you tried to resolve the issue directly.

- Photos or Videos: If you got a damaged or totally wrong item, nothing beats visual proof. It's incredibly powerful.

- Shipping and Tracking Information: For items that never showed up, this proves the package never made it to your doorstep.

This stack of evidence is the foundation of your entire claim. Having it all ready to go before you call the bank makes everything smoother and shows them you've done your homework.

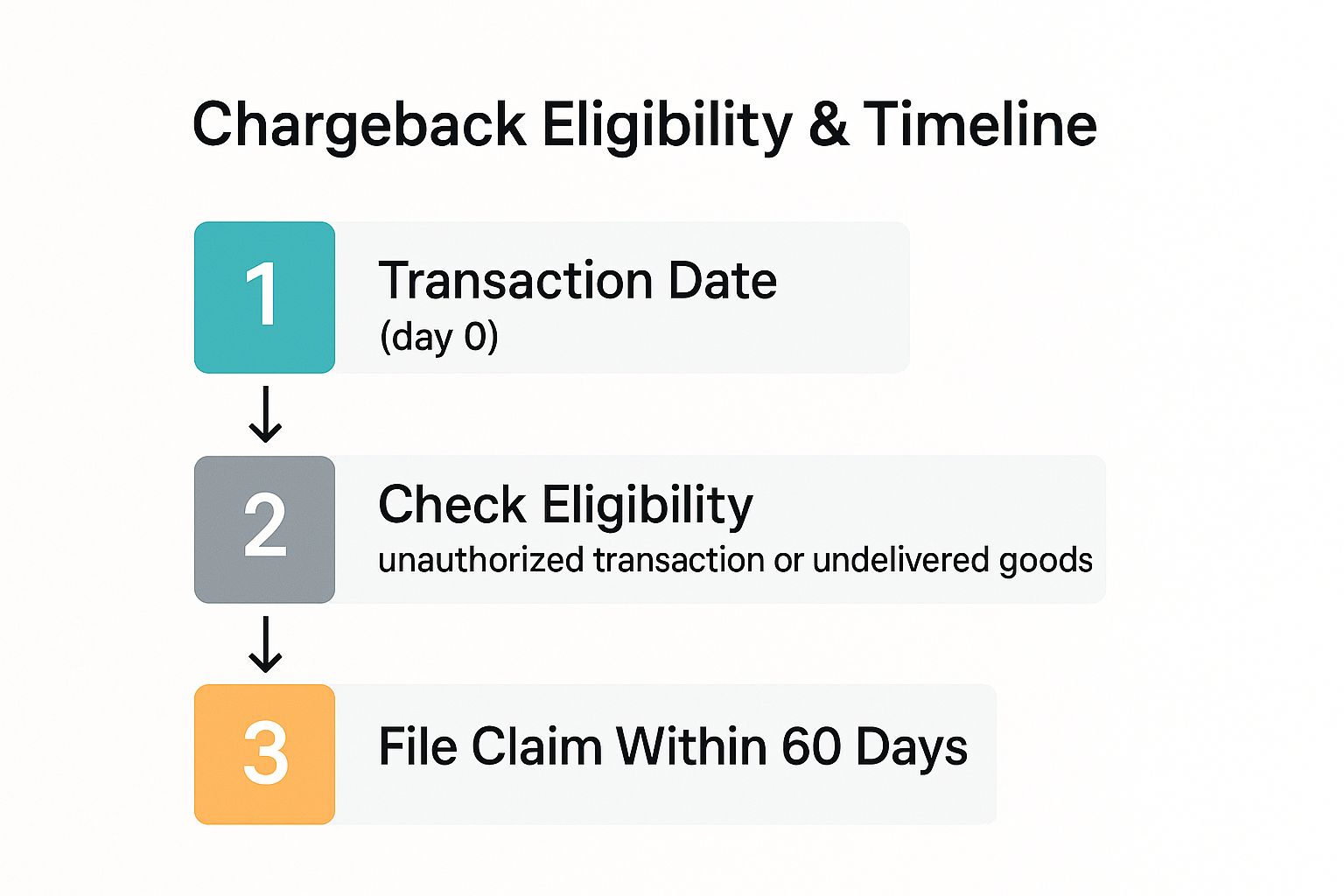

This infographic lays out the crucial first steps and the deadlines you absolutely need to know.

As you can see, the clock starts ticking the moment the transaction happens. You typically have about 60 days to formally file your claim, so don't wait around.

Submitting Your Formal Dispute

With your evidence file organized, it’s time to officially kick off the chargeback for a debit card. You can usually do this by calling the customer service number on the back of your card, popping into a local branch, or using your bank’s online portal or mobile app.

Be ready to explain what happened clearly and to the point. Refer back to the evidence you've gathered. The bank will probably give you a dispute form to fill out, which is where you'll lay out the details of the transaction and the specific reason for your chargeback.

Key Insight: When you talk to your bank, just stick to the facts. State what happened, explain why the charge is wrong, and mention the steps you took to fix it with the business. Ditch the emotional language and focus on providing clear, factual information.

The bank will then slap a "reason code" on your case and kick off its investigation. While this whole system is designed to protect you, remember that the merchant has a right to challenge your claim. If you’re curious about what happens on their end, checking out how to fight a chargeback from a business’s point of view can give you some valuable perspective. Understanding their playbook can actually help you build a stronger case.

Once you’ve submitted your dispute, the bank takes the reins. But make no mistake—your role in providing rock-solid proof is the single most important part of the journey.

Know Your Rights and Critical Timelines

When you're staring down a frustrating debit card chargeback, knowing your rights isn't just a nice-to-have—it’s your most powerful tool. The good news is that you don't have to navigate this alone. Federal law actually provides a pretty solid safety net for consumers.

Your main line of defense is a law called the Electronic Fund Transfer Act (EFTA). You don't need a law degree to get the gist of it. Put simply, the EFTA lays down clear rules for how banks must handle errors and shady transactions on your debit card, giving you a defined path to get your money back.

This act means your bank can't just brush off your claim. It legally forces them to investigate your dispute, look at the evidence from both you and the merchant, and make a fair call. It’s what levels the playing field and makes sure your side of the story gets heard.

The Clock Is Ticking: Your 60-Day Deadline

In a debit card dispute, time is your biggest enemy. The EFTA gives you a very strict window to report a problem, and if you miss it, you could lose your right to get your money back altogether. This is one part of the process you absolutely have to get right.

You generally have 60 days to report an unauthorized transaction or an error. That 60-day clock starts ticking from the date your bank sends you the statement showing the problem charge—not from the date the transaction happened.

Key Takeaway: Missing this 60-day reporting deadline could mean you're stuck with the full liability for a fraudulent charge. Banks are sticklers for this timeline, so moving fast is the best way to protect your money.

If you don't report it in time, the bank can argue that you didn't act responsibly, potentially leaving you to eat the loss. The strictness of the chargeback for a debit card time limit is a huge deal, and you can get more details on how these deadlines work in our complete guide on the chargeback time limit.

What Your Bank Is Required to Do

Once you file your dispute within that 60-day window, the EFTA puts the ball squarely in your bank's court. They can't just leave you high and dry while your money is missing.

Here’s what you can, and should, expect your bank to do:

- Prompt Investigation: Your bank has to kick off a "prompt" investigation into your claim, which usually has to start within 10 business days.

- Provisional Credit: This is a game-changer. If the investigation looks like it will take longer than 10 days, the bank has to give you a provisional credit for the disputed amount. This means they temporarily put the money back in your account, so you aren't out of cash while they sort things out.

- Written Explanation: When their investigation is over, your bank must give you a written explanation of what they found and the final decision they made.

Knowing these rules empowers you. If your bank is dragging its feet or skipping these steps, you can confidently call them out and make sure they handle your claim the right way. This framework turns what feels like a messy, unfair situation into a regulated process with clear protections in your corner.

What Happens After You Submit a Chargeback?

So, you’ve gathered your evidence, filed the chargeback for a debit card, and hit "submit." Now what? It might feel like you've sent your claim into a black hole, but there's actually a well-defined process kicking off behind the scenes, with your bank stepping in to act as your advocate.

The first thing your bank does is give your claim a quick once-over to make sure it's legitimate. If it passes this initial smell test, they'll slap a "reason code" on it. This code is just shorthand for why you're disputing the charge—think "goods not received" or "unauthorized transaction." That code officially gets the ball rolling on the formal investigation.

The Investigation Kicks Off

Your bank doesn't just take your word for it and call it a day. They reach out to the merchant's bank (known as the acquiring bank) and present your claim along with all the proof you provided. It's kind of like your lawyer sending a formal notice to the other side's legal team.

This triggers a structured back-and-forth between the banks:

- The Merchant Gets Notified: The merchant’s bank passes the dispute along to the business that charged you. That business is now on the clock and typically has only 10-20 days to respond.

- The Merchant Mounts a Defense: This is the merchant's opportunity to push back. They can either agree to the chargeback or decide to fight it. If they fight, they'll submit their own evidence in a process called representment.

- Evidence Under Review: Your bank essentially acts as the referee. They take a hard look at the evidence from both sides, comparing the proof you sent in with whatever the merchant submitted to defend the charge.

While all this is happening—a process that can take anywhere from a few weeks to several months—that provisional credit you received usually stays put in your account. The whole system is designed to give both you and the merchant a fair shot to make your case.

The Final Decision Arrives

After carefully weighing all the facts, your bank will make its final call on your debit card chargeback. You'll be notified of the outcome in writing, as required by law. There are really only two ways this can go.

Key Insight: The final decision almost always comes down to who has the stronger, clearer evidence. A well-documented claim will beat an emotional one with missing proof every single time.

Here are the possible outcomes:

- You Win the Dispute: If the bank sides with you, that provisional credit becomes permanent. The money is officially yours to keep, and the case is closed. This often happens when the merchant doesn't bother to respond or when their evidence is just too weak.

- Your Claim is Denied: On the other hand, if the merchant comes back with compelling proof—like a receipt you signed or a delivery confirmation with your signature on it—the bank may rule in their favor. If that happens, the bank will reverse the provisional credit, and the money will be taken back out of your account.

But even if your claim is denied, don't throw in the towel just yet. You still have the right to appeal the decision. And if you feel the bank didn't handle your case fairly, you can always file a complaint with the Consumer Financial Protection Bureau (CFPB).

Why Businesses Are Concerned About Chargebacks

To really get the full picture of the debit card chargeback process, it helps to step into the merchant's shoes for a moment. For any business, but especially for smaller ones, chargebacks are much more than an occasional headache. They're a genuine financial and operational threat.

Every time a customer files a dispute, the business is hit with more than just the loss of the original sale. They also get slapped with a non-refundable chargeback fee from their payment processor, which can range from $20 to $100 per incident. And here's the kicker: they pay that fee whether they win the dispute or not.

This isn't a small problem, either. It's growing fast. Global chargeback volumes are projected to hit a staggering 337 million cases by the end of 2025. That’s a sharp 27% jump from 2022, fueled largely by the boom in e-commerce and card-not-present transactions.

The Real Cost Beyond the Transaction

When a business faces a chargeback, the financial damage goes way beyond a single lost sale and a fee. A high volume of disputes can seriously damage a merchant’s reputation with their bank and payment processor.

If a business's chargeback ratio—the number of chargebacks they get compared to their total transactions—creeps too high, their payment processor might label them as "high-risk." This can trigger higher processing fees or, in worst-case scenarios, the complete termination of their merchant account.

This risk is why merchants are forced to be so diligent in fighting disputes. It’s why they sometimes push back hard, even on what seems like a clear-cut case from the customer's side. They aren’t just trying to be difficult; they’re fighting to protect their business from some very real financial penalties.

To get ahead of this, businesses often implement effective strategies for preventing chargebacks. Understanding this perspective doesn't mean you shouldn't file a legitimate claim. It just makes you a more informed consumer, one who sees how the system impacts everyone involved. It might even encourage you to try resolving the issue directly with the business first, whenever that's an option.

Common Questions About Debit Card Chargebacks

Even after you get the hang of the basics, a few specific questions about a chargeback for a debit card always seem to pop up. Let's tackle some of the most common points of confusion so you feel ready for anything.

Is a Debit Card Chargeback Harder to Win?

It can definitely feel that way, and a big reason is that it's your money—not the bank's—that’s gone from your account while everyone investigates. Credit card disputes are covered by the Fair Credit Billing Act (FCBA), which many people find more consumer-friendly.

Debit card chargebacks, on the other hand, fall under the Electronic Fund Transfer Act (EFTA). The EFTA has much tighter reporting deadlines—often just 60 days—so you have to act fast.

What if My Chargeback Is Denied?

First off, don't just give up. Your first move should be to ask the bank for a written explanation detailing why they denied your claim. If you think they overlooked key evidence you provided, you can appeal their decision.

Still not getting anywhere? You can take it a step further and file a formal complaint with the Consumer Financial Protection Bureau (CFPB). They will follow up with the bank on your behalf to get things sorted out.

Key Takeaway: A merchant can refuse to do business with you after you file a chargeback against them. This is why it's always smart to try resolving the issue with them directly before escalating the dispute.

Tired of manually fighting disputes? ChargePay uses AI to automate the entire chargeback process, boosting your win rates and recovering lost revenue without you lifting a finger. See how it works at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)