So, you've made a sale through Stripe. Great! But then, you get a notification that feels like a punch to the gut: a chargeback. What does that even mean?

A Stripe chargeback is basically a forced refund. It happens when a customer disputes a charge with their bank instead of coming to you first. The bank then yanks the money right out of your account, often without your say-so, and slaps you with fees that you won't get back. It’s not just a return; it’s a formal, and often painful, dispute process that can really sting your business.

What a Stripe Chargeback Really Costs Your Business

Think about it this way: a customer wants their money back. But instead of shooting you an email or calling your support line, they go straight to their bank and say, "I don't approve this charge." The bank then reverses the transaction, pulling the funds directly from your Stripe account and returning them to the cardholder.

This whole system was originally set up as a safety net for consumers, protecting them from fraudulent charges and merchants who don't deliver on their promises. While the intention is good, it often leaves honest business owners in a really tough spot, costing far more than just the price of the item sold. Every single chargeback you receive piles on both direct and hidden costs that can quickly spiral out of control.

The Hidden Financial Drain

Losing the money from the original sale is just the tip of the iceberg. On top of that, Stripe hits you with a $15 non-refundable dispute fee for every single chargeback. Yes, you read that right—even if you fight the dispute and win, that $15 is gone forever. If you lose, you're out the sale amount, the product or service you already provided, and that pesky fee.

These individual costs are part of a massive global problem. Experts predict that by 2025, chargebacks will drain a staggering $33.79 billion from the e-commerce world. For every dollar lost to fraud, merchants actually lose an average of $4.61 when you factor in all the associated costs. And if you're dealing with international customers on Stripe? Currency conversion rates and cross-border fees can easily push the total cost of one chargeback to over 5% of the transaction's value.

The numbers don't lie. The actual cost of a single chargeback is often much higher than merchants realize. Let's break it down.

The True Cost of a Single Stripe Chargeback

As you can see, a simple $100 transaction can end up costing you nearly double that amount. This doesn't even account for the long-term damage.

More Than Just Money

Beyond the immediate financial hit, chargebacks cause other kinds of damage. A high number of disputes can seriously tarnish your reputation with Stripe and its banking partners. Once your chargeback rate crosses certain thresholds, you're flagged as a high-risk business, and the consequences can be severe.

A high chargeback rate signals risk to payment processors. This can lead to your account being placed in a monitoring program, facing higher fees, or even being terminated, effectively shutting down your ability to accept card payments.

This is exactly why getting a handle on the full cost of a Stripe chargeback is so important. It’s a toxic mix of lost revenue, unavoidable fees, and the potential for long-term damage to your business's financial health. For a deeper dive into the fundamentals, you might be interested in our guide on what a Stripe chargeback is and how it works.

Understanding Why Customers File Chargebacks

To effectively fight a Stripe chargeback, you first have to get to the bottom of why it happened in the first place. Not all disputes are created equal, and figuring out the root cause is your first step toward building a solid defense and prevention plan. Think of yourself as a detective; you need to understand the motive before you can crack the case.

Most chargebacks fall into one of three main buckets. Each one requires a completely different mindset and strategy to handle correctly.

Simple Merchant Errors

This is the most straightforward category and, luckily, the easiest one to fix. These chargebacks pop up when a simple mistake is made on your end. Maybe you shipped the wrong size T-shirt, a product showed up damaged, or a recurring subscription was billed incorrectly.

The customer is genuinely owed a refund, but instead of reaching out to your support team, they went straight to their bank. While it's frustrating, this is often a huge red flag that your customer service or return process isn't as clear or accessible as it needs to be.

Criminal Fraud

This is the classic, clear-cut case of theft. A fraudster gets their hands on stolen credit card details and uses them to buy something from your store. When the real cardholder sees the bogus charge on their statement, they rightfully dispute it.

There's not much to argue in these situations. The transaction was fraudulent, plain and simple, so the chargeback is valid. Your focus here isn't on trying to win the dispute but on beefing up your fraud detection systems to stop these purchases from ever happening again.

Globally, e-commerce has seen a 222% increase in chargebacks, driven by a perfect storm of rising online sales, delivery delays, and a surge in the most challenging type of dispute: friendly fraud. As merchants expand their reach, they face varying regional challenges; for instance, countries like Brazil and Mexico see chargeback rates as high as 3.48% and 2.81% respectively. You can explore more about these trends in chargeback statistics from Chargeback.io.

The Challenge of Friendly Fraud

This is where things get really murky. Friendly fraud is when a customer disputes a purchase they—or someone in their household—actually made and received. It's not malicious in the same way criminal fraud is, but it costs you just as much money.

The reasons for it are all over the map, creating a massive gray area that’s tough to navigate. Getting a handle on these nuances is crucial, because this is often the most preventable and winnable type of dispute. Check out our detailed guide to learn more about the different forms of chargeback fraud and how to identify them.

Here are a few common friendly fraud scenarios:

- Buyer's Remorse: The customer simply regrets their purchase and sees a chargeback as an easy way out, bypassing your official return policy entirely.

- Family Fraud: A child or another family member uses the card without getting permission. The cardholder doesn’t recognize the charge on their statement and disputes it.

- Forgotten Purchase: The customer flat-out forgot they bought something. This is especially common with recurring subscriptions or when your billing descriptor on their statement is unclear.

How to Respond and Win a Stripe Dispute

Getting that dreaded “Dispute notification” email from Stripe can make your stomach drop. It’s a mix of frustration and maybe a little bit of panic. But now is not the time to hesitate.

The clock starts ticking the moment that notification hits your inbox. You have to act fast and, more importantly, act smart to have any shot at winning.

Responding to a dispute is a flat-out race against time. The card networks give you a pretty tight window—usually just 7 to 21 days—to get your evidence together and submit it. If you miss that deadline, it's an automatic loss. No appeals, no second chances.

Think of yourself as building a case. You need to gather your proof, organize it into a clear story, and present it before time runs out.

Your Step-by-Step Response Plan

Fighting a Stripe dispute happens right inside your Stripe Dashboard. While the platform makes the process itself feel simple, winning or losing comes down to one thing: the quality of your evidence.

You’re not just submitting documents; you’re telling a story that proves the transaction was legit and that you delivered on your promise to the customer.

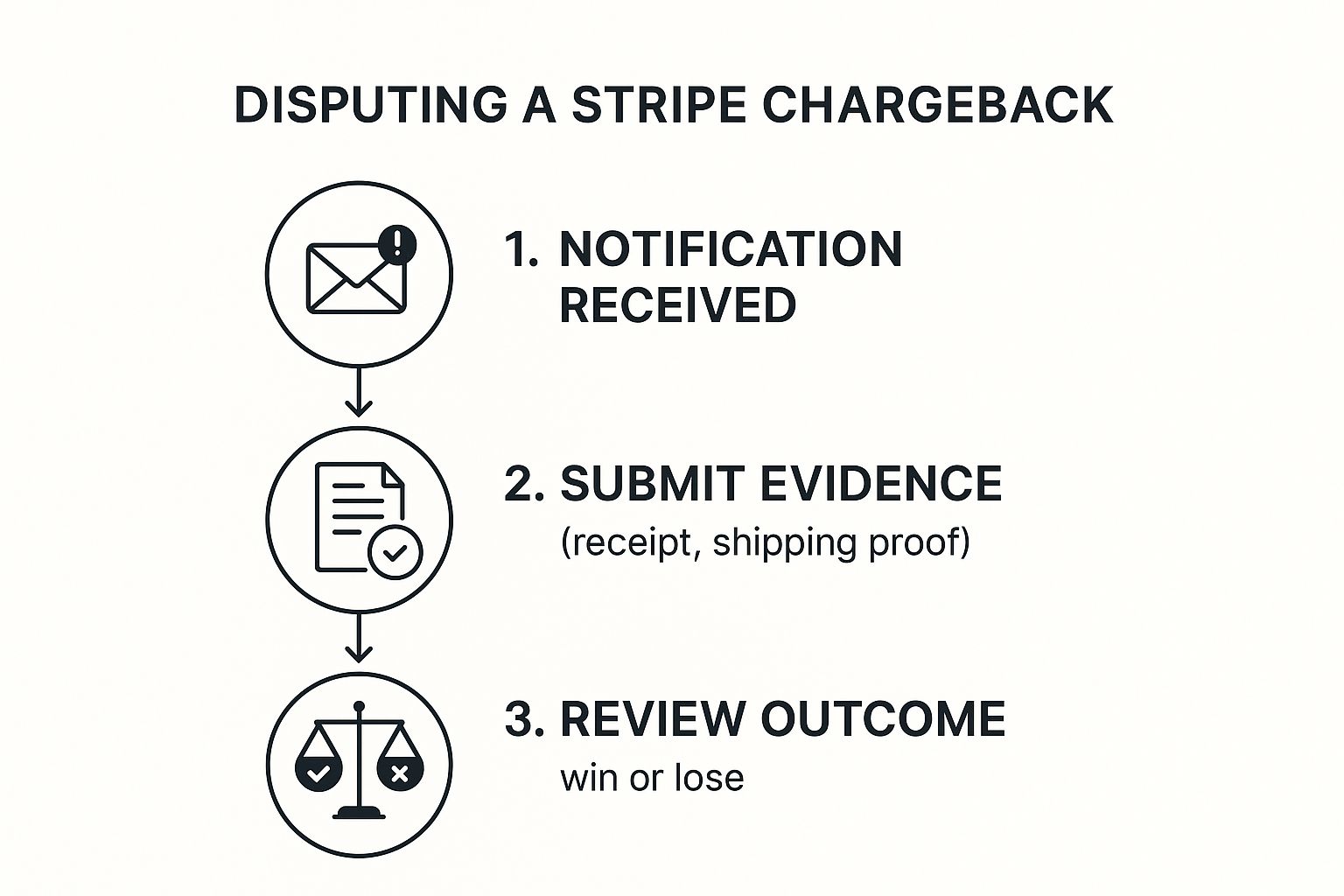

This is the basic flow you'll follow from your end:

It’s a simple three-step process: you get the notification, you submit your evidence, and then you wait for the cardholder's bank to make a decision.

Gathering Compelling Evidence

The evidence you need really depends on what you sell. The goal here is to provide undeniable proof that directly counters the customer’s specific reason for the dispute. A generic, copy-paste response just won't work.

Here’s a quick checklist of what you should be scrambling to find, based on what you sold:

- Proof of Delivery: This is your silver bullet. You need a tracking number and a screenshot from the carrier’s website showing the package was delivered to the customer’s address.

- Order Confirmation: Pull up any emails or receipts that show the customer's name, their billing and shipping details, and exactly what they bought.

- Usage Logs: This is crucial. Show that the customer logged in, downloaded the file, or used your software. IP addresses and timestamps are your best friends here.

- Customer Communications: Did they email you for support? Did they acknowledge receiving the product in a chat? Any communication like this is gold.

- Signed Contracts or Agreements: This is the strongest evidence you can have. It needs to clearly outline the scope of work and payment terms.

- Proof of Service Rendered: Think project completion reports, client sign-off emails, or detailed messages proving you did the work you were paid for.

When you're ready, Stripe gives you a straightforward interface to upload all your documents and write a brief summary of your case.

This is what you'll be looking at in your dashboard. It’s clean, organized, and makes managing everything much less of a headache.

Having all your evidence in one place like this helps you build a much stronger case and easily keep track of how each dispute is progressing.

Key Takeaway: The bank employee reviewing your case has zero context. They don't know your business, and they don't know the customer. Your evidence needs to paint a complete picture, from the moment the order was placed to the moment it was fulfilled, leaving no room for doubt. Be concise, stick to the facts, and always stay professional.

Ultimately, winning a Stripe chargeback comes down to being prepared and hitting them with overwhelming proof. For a deeper dive into more advanced tactics, check out our complete guide on how to fight a chargeback and win.

Once you’ve submitted everything, the final call is made by the customer’s bank. Be prepared to wait, as this process can take anywhere from 60-75 days.

Strategies for Preventing Chargebacks

While knowing how to fight a Stripe chargeback is a valuable skill, let’s be honest: the best way to win a dispute is to stop it from ever happening in the first place. Shifting your mindset from reactive defense to proactive prevention will save you a ton of time, money, and stress.

A preventative approach is all about building trust and clarity into every single step of your customer's journey. When customers feel like they're in the loop and treated fairly, they're far more likely to shoot you an email for help instead of going straight to their bank. Most of these strategies are surprisingly simple, and they all boil down to clear communication and great service.

Nail the Basics with Crystal-Clear Communication

The root of so many chargebacks isn't a malicious customer; it's just plain old confusion. A customer who feels misled, or simply can't recognize a charge on their statement, is a prime candidate for filing a dispute. You can get way ahead of this by making every detail of the transaction totally transparent.

Put yourself in your customer’s shoes and look at every touchpoint. Is everything perfectly clear?

- Detailed Product Pages: Don’t just list a few features. Use high-quality photos from multiple angles, list accurate dimensions, and write honest descriptions. If a shirt runs small, say so! This sets the right expectations from the start and heads off those frustrating "not as described" disputes.

- Upfront Policies: Your shipping, return, and refund policies should be impossible to miss. Make sure they're linked clearly from your product pages and right there during checkout, so there are no nasty surprises down the road.

- Recognizable Billing Descriptor: This one is huge. Customize your billing descriptor in Stripe to be your brand name or website URL. A vague, cryptic charge like "SP *WEBSERVICES" is way more likely to be disputed than a clear one like "SP *YOURBRANDNAME".

Make Top-Notch Customer Service Your First Line of Defense

When something goes wrong—and it will—you want customers coming to you, not their bank. The only way that happens is by making your support team accessible, friendly, and genuinely helpful. Remember, a quick and easy refund is always, always cheaper than a long, drawn-out chargeback battle.

A customer service interaction costs a business an average of $1 to $15, depending on the channel. In contrast, a single chargeback can easily cost hundreds of dollars in lost revenue, fees, and operational time. Making support easy isn't just nice; it's a smart financial decision.

Make it dead simple for customers to find your contact info. A prominent "Contact Us" page with an email, a phone number, and maybe even a live chat option can deflect a massive number of potential disputes before they even start.

Use Stripe's Built-In Prevention Tools

Beyond just great service, Stripe itself gives you some powerful tools designed to sniff out fraudulent transactions and lower your Stripe chargeback risk before a payment is even processed.

Here are a few essential tools you should absolutely be using:

- Stripe Radar: Think of this as your fraud-fighting powerhouse. Radar uses machine learning to look at every single transaction and give it a risk score. You can set up rules to automatically block high-risk payments or just flag them for a quick manual review.

- 3D Secure (SCA): For an extra layer of security, require 3D Secure authentication. This is what prompts the customer to verify their identity with their bank, usually with a code sent to their phone. The best part? It shifts the liability for fraudulent chargebacks from you over to the card issuer.

- Address and CVC Checks: Always, always make sure you have Address Verification System (AVS) and Card Verification Code (CVC) checks turned on. These simple checks make it much harder for someone with stolen card details to make a purchase.

By combining clear communication with Stripe’s powerful security features, you create a seriously robust defense system. For a more exhaustive list of tactics, check out our complete guide on effective chargeback prevention.

Using Automation to Defend Your Revenue

Fighting every single Stripe chargeback that comes your way feels like a losing battle. It’s a massive drain on your time, energy, and resources—like trying to bail water out of a sinking boat with a teaspoon. You’re working hard, but you’re not really getting anywhere. This is exactly where modern tools can step in and put your entire defense process on autopilot.

Think of it like having a dedicated chargeback expert on your team, working 24/7 to protect your sales. That's what AI-powered automation really does. These services plug directly into your Stripe account, becoming your first line of defense the moment a new dispute lands.

How Automation Works for You

Instead of you scrambling to find evidence for a transaction from weeks ago, the system does all the heavy lifting. It instantly gathers all the crucial data points for that specific order—we’re talking delivery confirmations, customer emails, IP logs, and AVS checks.

From there, it uses that evidence to write a compelling, perfectly formatted dispute response that speaks the language banks understand. The finished response is submitted on your behalf, often without you ever lifting a finger. What was once a tedious manual chore becomes a seamless, hands-off operation.

The true magic of automation is its ability to analyze massive amounts of data to build the strongest possible case. A person might overlook a key piece of evidence, but an AI system sifts through everything to construct a data-backed argument, seriously boosting your chances of winning.

The Benefits of Putting Your Defense on Autopilot

Adopting an automated approach isn't just about saving time; it's about fundamentally changing how you handle disputes to protect your bottom line. You can dive deeper into this in our complete guide to automated chargeback management.

Here’s what you really stand to gain:

- Reclaim Your Time: Stop losing countless hours every week digging through records and writing responses. Automation frees you and your team to focus on what actually grows your business—like marketing, developing new products, and talking to your customers.

- Boost Your Win Rate: These systems are built on data from thousands and thousands of disputes. They know exactly what evidence works for specific reason codes and craft arguments designed to win, often leading to a much higher revenue recovery rate than manual efforts ever could.

- Protect Your Revenue: By winning more disputes, you’re preventing revenue from walking out the door. Automation turns a costly problem into a managed process with a clear, positive return on your investment.

Your Stripe Chargeback Action Plan

Let's be real: navigating the world of Stripe chargebacks can feel like a maze. But when you cut through the noise, a solid strategy really just boils down to a few core principles. This is your game plan, a simple checklist to protect your revenue and keep your business on solid ground.

Think of it as a four-step cycle. First, you have to truly understand the financial hit. A chargeback is never just the lost sale. It’s a painful package deal: the original revenue, the cost of your product, the time your team spent, and that non-refundable $15 Stripe dispute fee all rolled into one. Acknowledging this full impact is the first step toward taking every single dispute seriously.

Next up, you need to play detective and pinpoint the real reasons for your disputes. Are they simple merchant errors that a bit of clearer communication could fix? Or are you dealing with friendly fraud, which calls for much stronger evidence? Getting to the root cause is everything—it dictates how you'll respond and how you'll prevent it from happening again.

Your Core Strategy Checklist

From there, it's all about how you respond with compelling evidence. You have to act fast, meet every deadline, and give them undeniable proof that you held up your end of the bargain. This isn't the time for weak arguments; your evidence, whether it's a delivery confirmation or user logs, needs to tell a complete, fact-based story.

Finally, and this is the most important part, you have to make prevention your top priority. As of 2025, Stripe is handling a mind-boggling $1.3 trillion in payments every year. That scale makes chargeback management a massive risk for any merchant on the platform. Proactive measures are your best defense, from something as simple as clear billing descriptors to using powerful tools like Stripe Radar. To get a sense of just how big Stripe is, you can read more about Stripe's incredible scale and what it means for merchants.

Common Questions About Stripe Chargebacks

Even with a solid game plan, you're bound to run into specific questions about handling a Stripe chargeback dispute. When you're in the thick of it, the finer points can get a little confusing, so let's clear up a few of the most common concerns we see merchants wrestling with.

Think of this as your quick-reference guide for those tricky situations that need a bit more clarity.

How Long Does the Stripe Dispute Process Take?

This is the part that requires some patience. After you've sent in all your evidence, the final call is made by the customer's bank, not Stripe. This stage of the process can drag on for a surprisingly long time—we're typically talking between 60 and 75 days.

During this waiting period, those disputed funds are held back from your account. The best thing you can do is make sure your initial evidence submission was as rock-solid as possible and hang tight for the final verdict.

Can I Block a Customer Who Files a Chargeback?

Yes, you absolutely can. Your Stripe Dashboard gives you the power to block future payments from specific email addresses and card numbers. If you're dealing with a chargeback that you're certain is fraudulent, blocking them is a good way to prevent the same person from causing more trouble down the road.

Just be sure to use this feature wisely. Blocking a customer over a simple misunderstanding can create a really negative experience and might even earn you some bad reviews. It’s best to save this for clear-cut cases of fraud or abuse.

Keep in mind, blocking a customer stops future payments, but it does not make the current chargeback go away. You still need to fight the existing dispute with compelling evidence if you want a shot at getting your money back.

What Happens If My Dispute Rate Gets Too High?

This is something you really want to avoid. Card networks like Visa and Mastercard keep a very close eye on merchant dispute rates. If your rate starts creeping over their thresholds (usually around 0.75% to 1.0% of your transactions), you risk being placed in a monitoring program.

Getting flagged like this can lead to painful consequences, like higher processing fees, intense scrutiny of your account, and in the worst-case scenarios, losing your ability to process card payments altogether. It's a perfect example of why having a proactive prevention strategy isn't just a nice-to-have—it's essential for the long-term health of your business.

Manually managing every single detail of the chargeback process is a constant drain on your time and energy. ChargePay uses AI to put your entire dispute defense on autopilot, handling everything from gathering evidence to submitting the case. This helps you win more disputes and get your revenue back, all without you lifting a finger. Learn how ChargePay can protect your business.

.svg)

.svg)

.svg)

.svg)