When a customer disputes a charge, it can be tempting to just write it off. Treat it like a small cost of doing business, not worth the hassle.

But that kind of thinking is a trap. Ignoring that "small leak" will eventually sink your ship. Every chargeback you let go unchallenged hits you with a lot more than just the original sale amount. It's a quiet, multi-layered financial drain on your profits.

Let’s break it down. First, you lose the revenue from the sale. Obvious, right? But you also lose the product itself, which you can’t get back and resell. Then, your bank adds insult to injury by hitting you with a non-refundable chargeback fee. This penalty, typically between $20 and $100, comes right out of your pocket, whether you win or lose the dispute.

More Than Just a Lost Sale

The financial bleeding doesn't stop with fees and lost goods. Think about the operational costs. Your team has to spend valuable time digging into the claim, pulling documents, and dealing with the administrative headache. That's time they could have spent on sales, marketing, or anything else that actually grows your business.

Each ignored dispute also chips away at your relationship with your payment processor. They keep a close eye on your chargeback ratio—the number of chargebacks you get compared to your total sales. If this number creeps up, you're looking at serious trouble.

Think of your chargeback ratio as a health score for your merchant account. A high ratio screams "risk" to payment processors, and they'll react by hitting you with higher processing fees, forcing you to keep a cash reserve, or even shutting down your account entirely.

The Real Financial Impact

When you add it all up, the costs are staggering. It’s not just about losing a $50 sale. The whole ordeal snowballs. In fact, each dispute costs merchants an average of $190 when you factor in the lost transaction value, shipping, bank penalties, and the labor to deal with it all.

And while merchants win about 45% of the chargebacks they fight, the actual net recovery rate—after accounting for all those associated costs—is a bleak 18%. If you want to see a deeper breakdown of the numbers, check out these chargeback statistics.

This is exactly why fighting chargebacks is non-negotiable for a healthy business. It's not about being stubborn or winning every single time. It's about protecting your bottom line and showing the banks you're a serious, diligent merchant who stands behind their sales.

Your First Move When a Chargeback Notice Hits

The notification hits your inbox: "Chargeback Filed." It’s easy to feel a surge of frustration or even panic, but your actions in the first 24-48 hours are absolutely critical. A calm, methodical approach right now sets the stage for successfully disputing the chargeback.

The very first thing you need to do is find the chargeback reason code. This is usually a two-digit number provided by the customer's bank, and it tells you exactly why they're disputing the transaction. It could be anything from "unauthorized transaction" to "product not as described," and this code dictates the specific evidence you'll need to gather.

Once you have the code, it’s time for a quick gut check. Not every chargeback is worth fighting. You have to weigh the order value against the time and resources it will take to build your case. A $5 dispute? Probably not worth the effort. But a $500 one? Absolutely. This quick cost-benefit analysis helps you focus your energy where it matters most.

Gather Your Initial Evidence Immediately

Your next move is to start pulling together all the documents related to the transaction. Think of yourself as a detective building a case file. The more detailed and organized your evidence is, the better your chances are of winning.

Here’s a checklist of what you should start collecting right away:

- Original Order Details: This includes the customer's name, the items purchased, the total amount, and the date of the transaction.

- Customer Communications: Pull any emails, chat logs, or support tickets related to the customer or their order. These can prove you acted in good faith to resolve any issues.

- Shipping and Delivery Confirmations: This is non-negotiable, especially for "product not received" claims. Get tracking numbers and, if possible, proof of delivery with a signature.

- Technical Data: Don't forget digital proof like the IP address used for the purchase, AVS/CVV match results, and any device fingerprinting data you collected.

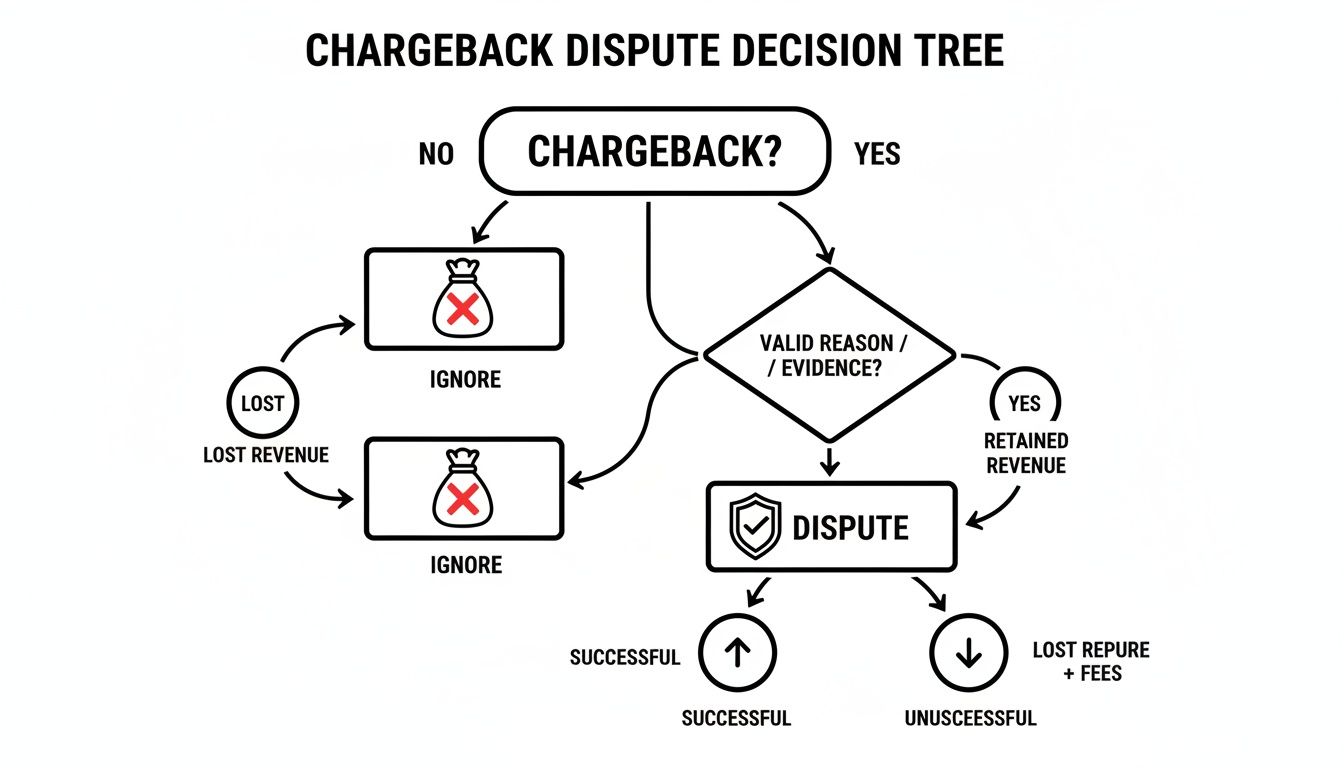

When that notification arrives, you're faced with a simple but crucial choice, as this flowchart shows.

Ultimately, while ignoring a chargeback is an option, actively choosing to dispute it is the only way to protect your revenue.

To make sure you don't miss a beat in those first critical hours, we've put together a checklist. This table breaks down exactly what to do the moment you're notified of a chargeback.

Immediate Action Checklist for Chargebacks

Following this checklist ensures you have a rock-solid foundation for your rebuttal before the deadline clock starts ticking.

Understanding the Broader Picture

Gathering this evidence isn't just about winning a single dispute; it's about understanding the entire lifecycle of a claim. Each piece of information helps you paint a clear picture for the issuing bank, showing them you're a diligent merchant with strong business practices.

Pro Tip: Create a dedicated folder for each chargeback case immediately. Name it with the order number and date, and save all your evidence there. Staying organized from the start prevents a frantic scramble for documents later.

By acting quickly and strategically, you turn a stressful situation into a manageable process. This initial data collection forms the backbone of your rebuttal. For a more detailed look into how banks and card networks handle these claims, you can learn more about the complete card dispute process and see what happens behind the scenes after you submit your evidence.

Building an Unbeatable Case with Compelling Evidence

Winning a chargeback dispute isn’t about who tells the better story. It’s about who has the better proof. Think of banks and card networks as impartial referees; they only care about cold, hard facts. This is where you shift from defense to offense, building an airtight case that leaves zero room for doubt.

Your first move is to match your evidence directly to the chargeback reason code. A "product not received" claim needs a completely different set of documents than a "not as described" dispute. Don't just dump a folder of files on the reviewer. Instead, you need to present a logical, easy-to-follow narrative that proves you held up your end of the bargain.

This meticulous approach is a must. The data shows that success requires vigilance. Merchants who use automated response systems can see 33% fewer chargebacks, and those who properly use card network rules—like Visa's compelling evidence standards—can reverse up to 77% of friendly fraud cases.

But the overall battle is tough. Mastercard data reveals merchants only win about 20% of the disputes they fight. It’s a sobering statistic that highlights just how critical your evidence is.

Matching Evidence to the Claim

Let's break down exactly what you need for the most common dispute types. Think of each document as a puzzle piece that, when put together, creates an undeniable picture of a legitimate transaction.

For "Product/Service Not Received" Claims: This is all about proving delivery. Your knockout punch is the shipping confirmation with a tracking number showing the item was successfully delivered to the customer's address. A signature confirmation is the gold standard here. For digital goods, you'll need server logs showing the download, the customer's IP address, and any records of them accessing the content.

For "Transaction Not Recognized" Claims: Here, your job is to prove the real cardholder made the purchase. Gather the AVS (Address Verification System) and CVV match data from your payment gateway. You should also include the customer's IP address, which you can geolocate to show it lines up with their billing or shipping city.

For "Not as Described" Claims: This one requires you to prove the product you sent was exactly what you advertised. Provide screenshots of the product page from the time of purchase, clear photos of the item you shipped, and any customer service chats where you offered support or a refund that the customer turned down.

Presenting Your Evidence Professionally

How you present your evidence is just as important as what you present. Bank reviewers look at hundreds of cases a day. Your job is to make their job easy.

Start with a well-structured rebuttal letter. This isn't the place for emotion; it's your cover sheet, briefly summarizing the dispute and outlining the evidence you've attached. For a deep dive into crafting the perfect response, check out our guide on how to write a compelling rebuttal letter.

Your goal is to create an undeniable trail of proof. Imagine a reviewer has 60 seconds to look at your case. Can they immediately see that you delivered the right product to the right person at the right address?

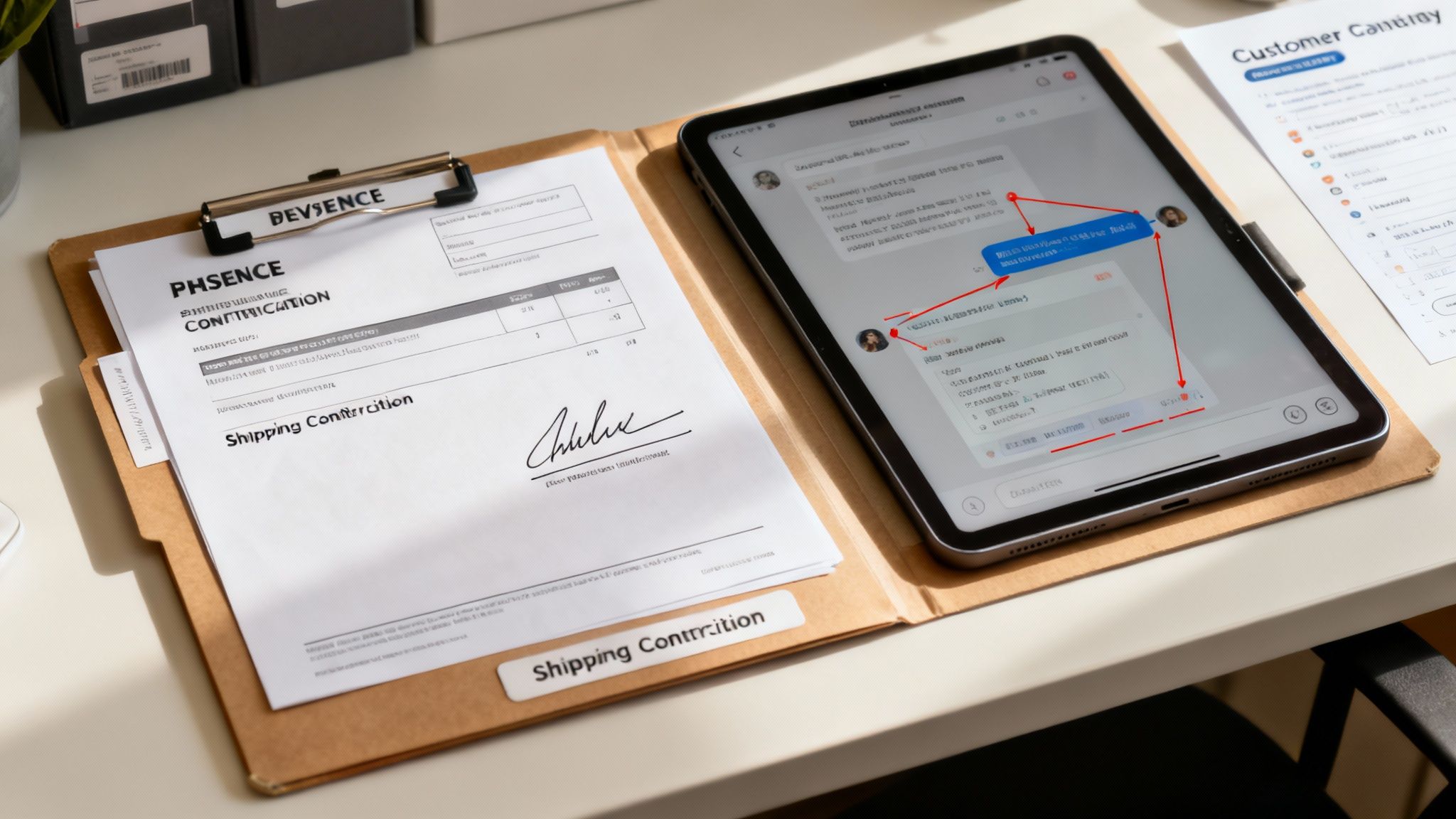

Finally, annotate everything. Don't just attach a raw screenshot of a delivery confirmation. Use arrows, highlights, or circles to point out the customer's name, the delivery address, and the "Delivered" status. Clearly label each document (e.g., "Exhibit A: Proof of Delivery," "Exhibit B: Customer Email Confirmation"). This tiny bit of effort turns a simple claim into a rock-solid, professional defense that dramatically increases your chances of winning.

Navigating the Murky Waters of Friendly Fraud

Let's get real about the biggest headache for most merchants today: friendly fraud.

It’s that infuriating scenario where a real customer buys from you, gets their product, and then calls their bank to dispute the charge. You did everything by the book, but now you’re stuck fighting for the revenue you rightfully earned.

And this isn’t some minor issue. Friendly fraud is now behind a staggering 75% of all chargeback cases.

In 2023 alone, the average cardholder filed 5.7 chargebacks. That added up to more than $65.2 billion in global disputes. The hardest-hit categories were clothing and accessories (20%), digital subscriptions (18%), and home goods (16%). If you want to dig deeper, this in-depth analysis of chargeback stats breaks it all down.

So, why are customers doing this? Their motives can range from an honest mistake to straight-up deception. Sometimes, a customer genuinely forgets they made the purchase or doesn't recognize your business name on their credit card statement. Other times, it's a simple case of buyer's remorse, and they see a chargeback as an easy way out of your standard return process.

Your Toolkit for Fighting Back

When you're up against friendly fraud, the evidence you need is different. The customer isn't claiming their card was stolen; they're claiming something else is wrong. Your job is to prove they not only authorized the purchase but also received exactly what they paid for.

This is where your digital paper trail becomes your most powerful weapon. You need to build a case so airtight that it leaves no room for doubt about the cardholder's involvement.

Here’s the essential evidence you should be gathering:

- AVS and CVV Confirmations: Proof that the Address Verification System (AVS) and Card Verification Value (CVV) match the bank's records. This is your first and best indicator that the legitimate cardholder made the purchase.

- IP Address Logs: The IP address where the order was placed can often be matched to the customer's billing or shipping city. It’s another key piece of evidence connecting them to the transaction.

- Customer Communications: Pull up any emails or support chats. Did the customer ask a question before buying? Did they confirm their order details? Every little bit helps.

- Account and Download History: For digital products, this is gold. Show logs of the customer creating an account, logging in multiple times, and downloading the file.

Think of yourself as a detective laying out the facts for the bank. Each piece of evidence helps you connect the dots, painting a clear picture: the cardholder visited your site, placed an order with their own card, and received the goods at their address.

Going the Extra Mile with Evidence

Sometimes, the standard evidence isn't enough, and you have to think outside the box.

For instance, has the customer posted a photo of themselves with your product on social media? A professional, non-confrontational screenshot of that post can be incredibly compelling.

Another powerful tool is looking at their purchase history with your store. If the same customer has successfully bought from you before—using the same card and shipping to the same address—it seriously undermines their claim that this one specific transaction is fraudulent. Presenting that history shows a pattern of legitimate behavior.

Successfully disputing a chargeback in these situations is about more than just getting your money back. It sends a clear message that you're a diligent merchant who keeps meticulous records. To learn more about tackling this tricky issue, check out our in-depth guide on friendly fraud, where we cover even more strategies for fighting and preventing these disputes.

Beyond a Single Dispute: Proactive Prevention Strategies

Winning a chargeback is a relief, but what if you never had to fight it in the first place? That’s the real victory. Shifting your focus from reactive damage control to proactive prevention is one of the most powerful moves you can make for your business's financial health. It’s all about creating a customer experience so clear and trustworthy that a chargeback never even crosses their mind.

This process starts the moment a customer clicks "buy." One of the most common, and frankly, easiest-to-fix reasons for a dispute is a confusing billing descriptor. You know the one. A customer checks their credit card statement, sees a charge from "XYZ LLC" instead of "Brenda's Boutique," and immediately assumes it's fraud. Make sure your descriptor is instantly recognizable and perfectly matches your store name. It’s a small detail that makes a huge difference.

Strengthen Your Communication and Policies

Honest, clear communication is your best defense against easily avoidable disputes. When a customer feels informed and respected, they're far more likely to shoot you an email with a problem instead of going straight to their bank. It's that simple.

You can implement these key communication practices right now:

- Instant Confirmations: The second a purchase is made, an order confirmation email should hit their inbox. Follow that up with another email containing tracking information as soon as the item ships. No exceptions.

- Clear Refund Policy: Don't bury your refund policy in fine print. Make it easy to find on your website and even easier to understand. A straightforward return process is much less of a headache for a customer than a complicated chargeback.

These small steps build immense trust and can eliminate a massive chunk of "friendly fraud" cases that stem from simple confusion or buyer's remorse. For a deeper dive, check out our comprehensive guide on chargeback prevention.

Use Technology as Your First Line of Defense

While great policies and crystal-clear communication are crucial, modern e-commerce demands a solid layer of technological protection. This is where fraud detection tools become absolutely essential.

Proactive prevention isn’t just good customer service—it’s a robust security strategy. By identifying red flags before a transaction is even completed, you stop potential fraudsters dead in their tracks and protect your bottom line.

Fraud detection systems analyze transactions in real time, hunting for warning signs. Understanding how banks identify suspicious transaction patterns is key here, as these tools are designed to catch the same red flags. They can flag mismatches in billing and shipping addresses, high-risk IP locations, or unusually large orders, giving you a chance to review them before they become a problem.

By combining top-notch customer service with smart fraud detection, you create a powerful defense that not only helps you when disputing a chargeback but actively works to ensure you have fewer to fight in the first place.

Common Questions About Disputing a Chargeback

Even with a solid game plan, you're bound to have questions when you're in the thick of a dispute. Let's tackle a few of the most common ones we hear from merchants.

How Long Does This All Take?

This is probably the biggest question on every merchant's mind. The short answer? It's not fast.

From the moment you submit your initial response to the final decision from the card network, you can expect the entire process to take anywhere from 45 to 90 days. It’s rarely a quick fix, which is why having your evidence organized and ready from day one is so critical.

Should I Handle This In-House or Use a Service?

Another common dilemma. For businesses that only see a handful of chargebacks, managing them internally can definitely be the most cost-effective route.

But as your business grows, so does the volume and complexity. The time spent fighting disputes can quickly become overwhelming. This is where professional services come in. A team that specializes in disputing chargebacks often secures higher win rates simply because it’s all they do, day in and day out.

What If I Lose the Dispute?

Losing a dispute is frustrating, but it's not always the end of the road. Depending on the card network (like Visa or Mastercard), you might have an opportunity to escalate the case to pre-arbitration or arbitration. Think of it as an appeal.

Be warned, though: arbitration is a serious step. It comes with additional, non-refundable fees. If you lose this round, you're out that money. You should only even consider it if you have truly compelling, new evidence that wasn't included in your initial response.

Ultimately, winning requires a deep understanding of the rules of the game. For a complete playbook on building your case from the ground up, our guide on how to win a credit card dispute digs into more advanced tactics and strategies to improve your odds.

Feeling overwhelmed by chargeback management? ChargePay uses AI to automate the entire dispute process, from generating evidence-packed responses to recovering your lost revenue. Stop wasting time and start winning more disputes by visiting https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)