When you're running an e-commerce store, keeping customer payment data safe isn't just a nice-to-have—it's your core responsibility. The two heavy hitters in data security are encryption and tokenization. While they both aim to protect sensitive info, they go about it in completely different ways. Getting this distinction right is crucial for your store's security and compliance.

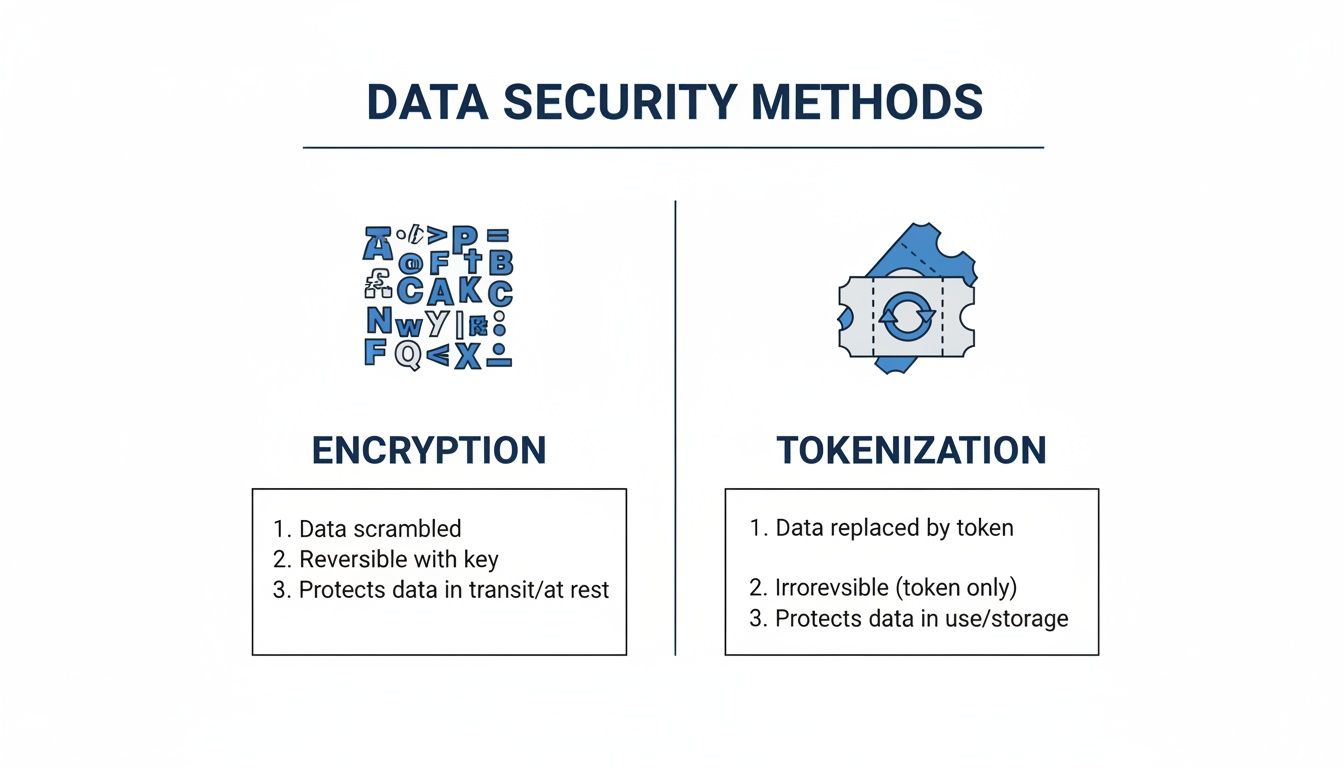

The simplest way to think about it is this: encryption mathematically scrambles sensitive data, while tokenization replaces it with a completely random, non-sensitive placeholder. Think of encryption as writing a secret message in a code that can be deciphered with the right key. Tokenization, on the other hand, is like swapping that secret message for a generic claim ticket.

Encryption vs. Tokenization: What Is The Core Difference?

Encryption is a reversible process. It takes readable data (like a credit card number) and uses a complex algorithm and a secret "key" to transform it into unreadable gibberish called ciphertext. If you have the correct decryption key, you can reverse the process and get the original data back. This makes it perfect for protecting data while it's in motion—for example, as it travels from a customer’s browser to your payment processor.

Tokenization is fundamentally different because it's not mathematically reversible. It completely swaps sensitive data for a unique, randomly generated value called a token. The original data is then locked away in a separate, highly secure server known as a "vault." The token itself has no mathematical relationship to the original data, making it worthless to a thief if intercepted.

This visual breaks down that core concept of scrambling data versus replacing it entirely.

The key takeaway is that an encrypted value can be unlocked with its key, but a token is just a useless stand-in without access to its secure vault.

Encryption vs. Tokenization At A Glance

To help you see the differences more clearly, let’s put them side-by-side. Each method has its own strengths depending on the situation, whether you're processing a simple one-time transaction or managing recurring subscriptions for loyal customers.

This table provides a quick summary of their fundamental differences.

Ultimately, the choice isn't about which one is "better" overall, but which one is right for a specific job. Encryption protects data as it moves, while tokenization removes it from your environment entirely, dramatically simplifying your compliance burden.

How Each Technology Secures Your Payment Data

To really get the difference between encryption and tokenization, we need to pop the hood and see how each one actually works to protect your customers' payment info. While they both have the same goal—securing data—their methods are completely different, and that leads to very different use cases for your e-commerce store.

Encryption is all about math. It takes a sophisticated algorithm, like the Advanced Encryption Standard (AES), and a secret cryptographic key to scramble readable data (plaintext) into a completely unreadable format (ciphertext). Think of it like a digital lockbox where the original data is inside, but it's been jumbled up according to a complex formula.

The most critical thing to remember about encryption is that it’s reversible. Anyone who gets their hands on the correct decryption key can unlock the ciphertext and see the original, sensitive information. This makes encryption perfect for protecting data while it's in motion—like when a customer’s credit card number travels from their browser to your payment gateway.

Tokenization: A Vault-Based Approach

Tokenization isn't about scrambling data at all—it’s about replacing it entirely. When your customer’s payment information enters a secure system, tokenization swaps the sensitive Primary Account Number (PAN) for a unique, randomly generated string of characters. We call this a token.

This token has zero mathematical relationship to the original card number. The actual, sensitive data is stripped from your systems and locked away in a highly secure, offsite server known as a token vault.

The whole security principle behind tokenization is that the token itself is useless if stolen. Since there's no mathematical key to reverse-engineer it, a hacker would have to breach the heavily fortified token vault to get the original data—a much, much harder job.

This process lets you do things like process recurring billing or offer one-click checkouts using just the token, all without ever storing or even touching the actual credit card details.

Comparing How They Work in Practice

While both methods secure data, the way they operate has huge implications for how you manage your payment infrastructure and data, especially as you grow.

- Encryption's Reversibility: This means you have to be extremely careful with your cryptographic keys. If a key is ever compromised, every piece of data encrypted with that key is suddenly vulnerable.

- Tokenization's Substitution: This approach offloads most of the security burden. The risk is effectively transferred to the token vault provider, who specializes in protecting this kind of sensitive data.

- Data Format Preservation: Here's a neat trick with tokens. They can be designed to match the format of the original data (like a 16-digit number), which makes them incredibly easy to integrate into existing systems without a major overhaul. Encrypted data, on the other hand, often changes in length and format, which can force you to make system adjustments.

Furthermore, scalability really separates the two when you're dealing with massive data volumes—a key consideration for global e-commerce platforms. Encryption scales pretty efficiently and can handle petabyte-scale databases, making it a good fit for big data environments. Tokenization can sometimes run into performance issues because of the need for vault lookups, and it often only protects the primary field (like the card number), potentially leaving other personal data like names and addresses exposed.

For those interested in the absolute frontier of data protection, advanced techniques like Zero-Knowledge Proofs are pushing the boundaries of privacy and security, particularly in blockchain environments.

Which Offers Better Protection In A Data Breach?

This is the question that keeps merchants up at night. When your systems get hit, which method actually keeps your customers' data safer? While both encryption and tokenization are solid security tools, they perform very differently when a breach actually happens.

Let’s cut to the chase: for protecting stored payment information, tokenization is the clear winner. The reason is simple and all comes down to what a thief gets their hands on if they break into your network. With tokenization, the data they steal is just a pile of useless, random tokens.

On the other hand, if you’re storing encrypted data, a breach turns into a high-stakes race against time. If the attackers manage to find and steal your decryption key, they suddenly have the power to unlock every single piece of customer data you have stored.

The Critical Role Of The Encryption Key

The security of your entire encrypted dataset hangs on a single point of failure: the encryption key. Honestly, managing these keys is a huge operational headache. You’re responsible for generating them, storing them securely, rotating them regularly, and making absolutely sure they are never exposed.

If an attacker breaches your system and also compromises your key management, they can reverse the encryption and access the original, sensitive data. It’s like a thief not only breaking into your house but also finding the master key to every safe inside. This is why key management is such a critical—and often complex—part of using encryption for stored data. You can learn more about comprehensive strategies, including how to handle outdated hardware, by exploring secure data destruction practices for physical assets.

The core difference in a breach scenario is this: a stolen token is just a random reference number with no value, while a stolen encryption key can unlock your entire dataset.

Tokenization effectively outsources this risk. By using a payment provider's token vault, you transfer the responsibility of protecting the actual cardholder data to a specialized third party whose entire business is built around securing that vault. That’s one less critical vulnerability you have to worry about.

Tokenization's Advantage In A Breach

By its very design, tokenization is the superior choice for breach protection. It renders stolen data completely useless without access to the highly secured vault—a massive advantage when cyber threats are constantly targeting payment systems.

Think about it: encrypted data is reversible. If keys are mismanaged, that ciphertext is entirely crackable, as we saw in the infamous 2014 breach affecting 500 million Yahoo accounts. In contrast, tokenization's random, non-mathematical tokens hold zero value on their own. This design alone can slash the potential impact of a data breach by an estimated 80-90%.

Here’s why tokenization holds up so much better:

- No Intrinsic Value: Stolen tokens can't be reverse-engineered to reveal the original card number. There is no mathematical formula to crack.

- Reduced Scope: Since the valuable data isn't even on your servers, the potential damage of a breach to your systems is massively contained.

- Contained Risk: The attacker would need to pull off a second, far more difficult breach against the secure token vault, which is typically protected by layers of security far beyond what most merchants can implement on their own.

This isn't to say encryption isn't valuable; it's absolutely essential for protecting data in transit. However, when it comes to storing data for future use, tokenization offers a fundamentally safer architecture. This approach is a cornerstone of effective e-commerce fraud prevention because it drastically reduces your attack surface and minimizes the potential fallout from a security incident.

How Tokenization Makes PCI DSS Compliance Easier

For any online merchant, the Payment Card Industry Data Security Standard (PCI DSS) can feel like a mountain to climb. These rules dictate how every business that accepts credit cards must protect customer data, and the process is often complex and expensive. The good news? Your choice between encryption and tokenization has a huge effect here, and tokenization provides a much simpler path forward.

Using a payment gateway’s tokenization service is a genuine game-changer. It means sensitive cardholder data never even touches your servers. When a customer pays, their details go straight to the payment processor, which sends a secure, non-sensitive token back to you. This single strategic move can pull most of your systems out of scope for PCI DSS requirements.

Reducing Your PCI Scope

The concept of "PCI scope" covers all the people, processes, and technology in your business that store, process, or transmit cardholder data. The larger your scope, the more complicated and costly compliance gets.

When you use tokenization, you stop handling raw card data altogether. You’re only managing the meaningless token. This dramatically shrinks your compliance footprint.

The core benefit is simple: if the sensitive data isn't in your environment, your environment doesn't need to meet the strictest PCI DSS rules. This directly translates to lower audit costs, less administrative work, and a much lower risk of facing steep non-compliance fines.

This is a world away from using encryption for stored data. If you encrypt and store card information yourself, you also hold the keys to decrypt it. Because you have the power to reverse the process and view the original data, your systems remain fully in scope for tough, expensive PCI audits.

The Real-World Impact on Your Business

A smaller compliance footprint isn't just a technicality; it delivers tangible benefits that hit your bottom line and boost your efficiency. It's a major reason why so many businesses are making the switch.

By 2026, the volume of tokenized payment transactions is projected to top one trillion globally, a shift driven by e-commerce leaders like Shopify and PayPal. This highlights a key advantage: unlike encryption, which depends on keys that can be stolen, tokenization swaps sensitive data for useless tokens kept in a secure vault. This risk reduction is why some payment processors report that merchants can slash their PCI audit costs by up to 50%. You can dive deeper into how this works in our guide on what tokenization in payments means for merchants.

Here’s how that simplification looks in practice for an e-commerce store:

- Simplified Audits: Instead of a complex, multi-day audit, you might only need to fill out a much shorter Self-Assessment Questionnaire (SAQ).

- Lower Costs: Fewer systems in scope mean less money spent on auditors, specialized security software, and endless employee training.

- Reduced Risk: By passing off sensitive data storage to a specialized provider, you transfer a massive amount of risk away from your business.

Ultimately, by using tokenization through your payment gateway, you effectively outsource the hardest parts of PCI compliance. This frees you up to focus on what really matters—growing your business.

Practical Scenarios For Your E-Commerce Store

Knowing the theory behind encryption and tokenization is one thing. Seeing how they actually work in your day-to-day operations is where it really clicks. Let’s move past the definitions and look at real situations every online merchant faces, highlighting where each technology truly shines.

These aren't just abstract technical examples; they're core functions of a modern e-commerce business. Nailing the security approach for each one is essential for protecting your customers, simplifying your PCI scope, and building the trust you need to grow.

Scenario 1: Setting Up Recurring Billing

For any subscription business—whether you're selling monthly coffee boxes, software, or access to a service—recurring billing is your lifeblood. To charge a customer automatically every month, you have to store their payment information securely.

This is a perfect job for tokenization.

When a customer signs up, your payment gateway handles the initial transaction and sends you a token in return. You store this token, not the actual card number. Each month, you simply tell the gateway to charge that token again.

By using a token, you completely sidestep the need to store sensitive cardholder data on your own servers. This not only makes you a much less attractive target for hackers but also dramatically simplifies your PCI DSS compliance. It's the industry standard for a reason.

If you tried to do this with encryption, you’d be holding onto the encrypted card number and the decryption key. That would put your systems squarely in scope for the most complex PCI audits, making you fully responsible for protecting that data.

Scenario 2: Enabling One-Click Checkouts

Customers love convenience, and nothing says "easy" like a one-click checkout. It slashes friction and can give your conversion rates a serious boost, especially for returning shoppers. Much like recurring billing, this feature requires you to "remember" a customer's payment details.

Once again, tokenization is the clear winner here.

The process is almost identical to subscriptions. After a customer’s first purchase, their payment details are vaulted by your payment provider, and you get a token linked to their account. The next time they visit, they can finalize their purchase instantly by authorizing a charge against that stored token.

This delivers a seamless customer experience without introducing unnecessary security risks to your business. To learn more about how this fits into a broader payment strategy, check out our guide on building a payment orchestration platform.

Scenario 3: Securing Data In Transit

Every single time a customer hits that "Pay Now" button, their payment info—card number, expiration date, CVV—has to travel from their web browser to your payment gateway. That journey across the open internet is where data is most vulnerable to being intercepted by bad actors.

This is the ideal use case for encryption.

Specifically, this is handled by Transport Layer Security (TLS), which you probably know as SSL. It encrypts the data packet before it leaves the shopper's device and only decrypts it once it reaches the secure payment gateway. This ensures that even if a cybercriminal manages to snatch the data along the way, all they'll get is unreadable gibberish.

Scenario 4: Managing Chargeback Evidence

Finally, let's talk about a less pleasant but critical part of e-commerce: handling chargebacks. When you need to provide evidence to dispute a claim, you have to reference the original transaction. But sharing full credit card numbers in dispute documents is a massive security risk and a PCI compliance nightmare.

Tokenization provides a secure and elegant solution.

Instead of referencing the raw Primary Account Number (PAN), you can use the transaction's unique token as the identifier. This allows you to submit all the necessary evidence to the banks without ever exposing sensitive cardholder data in your communications. It helps you maintain a secure, professional, and compliant dispute resolution process from start to finish.

Choosing The Right Data Security Strategy

So, after digging into encryption vs. tokenization, you're probably wondering which one makes sense for your business. The truth is, it’s not really an either/or situation. The smartest data security strategy for almost any e-commerce merchant is a combination of both, letting each technology do what it does best.

Think of it this way: encryption is your go-to for protecting data in transit, while tokenization is the undisputed champ for securing data at rest. Modern payment solutions are built to manage this handshake for you, blending both methods to create a secure ecosystem without you ever needing to get tangled up in the technical weeds.

Making a Confident Decision

When you're looking at payment processors, you’re not just picking a way to get paid—you’re choosing a partner to handle your data security. To make the right call, you need to ask questions that cut through the jargon and connect technical features to what actually matters: reducing your risk, lowering costs, and building customer trust.

Use this quick checklist to guide those conversations and make sure any potential partner has your back.

Questions to Ask Your Payment Processor:

- How does your solution shrink my PCI compliance scope? Their answer should be all about tokenization and how they keep raw cardholder data off your servers.

- Do you provide both gateway tokenization and a secure vault? This confirms they can manage the full token lifecycle, from the moment it's created to when it's safely stored.

- What encryption standards, like TLS, do you use for data in transit? This is a simple but critical question to ensure they’re following modern best practices for securing data on the move.

- Can I use your tokens with other payment processors if I decide to switch? This is a huge one. It's all about avoiding vendor lock-in and giving your business the flexibility to grow and adapt.

The real goal isn’t just to find a provider that offers these technologies, but one that implements them in a way that makes your life easier. A great partner absorbs the security complexity so you can focus on what you do best—selling.

Bringing It All Together

At the end of the day, a solid payment security setup should just work, protecting you and your shoppers without adding any friction. A modern payment solution will automatically encrypt transaction data the second a customer clicks "buy." Once that data hits the payment gateway, it’s instantly tokenized, and that secure token is sent back to your system for things like one-click checkouts or recurring billing.

This hybrid approach truly gives you the best of both worlds. Encryption is the armored truck for your data, and tokenization is the impenetrable vault where it’s stored. You get all the operational benefits of using tokens without ever compromising on end-to-end transaction security. As you weigh your options, it's also a good idea to see how providers handle customer information in their policies. For an example, you can learn more about how we handle user data in our privacy policy.

By asking the right questions and understanding how these two technologies team up, you can choose a solution that doesn't just secure your payments but actually helps your business grow.

Frequently Asked Questions

When you get down to the brass tacks of encryption versus tokenization, a few common questions always pop up. We’ve heard these from countless merchants, so we’ve put together some straightforward answers to help you connect these concepts to your own business.

Getting this right is a big deal for building a secure and smooth-running payment system.

Can I Use Both Encryption And Tokenization Together?

Yes, and honestly, you really should. A hybrid approach isn't just possible; it's the gold standard for e-commerce security today.

Think of it like this: encryption is the armored car that protects cardholder data while it's in transit—that critical journey from your customer's browser to the payment gateway. Once that encrypted data arrives safely, the gateway processes it and sends you back a token. You then keep that token—not the card data—for future use like subscriptions or one-click checkouts. This way, you're using each technology for what it's best at, creating powerful, layered protection.

Does Tokenization Completely Eliminate My PCI Compliance?

It won't make PCI compliance vanish into thin air, but it does make it significantly easier and cheaper to handle. By using tokenization, you ensure sensitive card data never even touches your systems, which dramatically shrinks your PCI scope. That means fewer of your systems fall under the strictest PCI DSS regulations.

This reduction in scope is the single biggest compliance benefit of tokenization. It often allows you to use a much shorter and simpler Self-Assessment Questionnaire (SAQ), saving you a tremendous amount of time, money, and stress during audits.

You’ll still have responsibilities, of course, like making sure your checkout page is secure. But the overall burden is massively reduced.

Is One Better Than The Other For Managing Chargebacks?

While neither encryption nor tokenization directly stops a chargeback from happening, tokenization is a huge help when you're managing the dispute process. It gives you a secure way to reference transactions without ever exposing sensitive card information.

When it's time to submit evidence for a dispute, you can use the transaction's unique token as the identifier instead of the customer's full credit card number. This is crucial for a couple of reasons:

- It prevents accidental data exposure. You avoid sending sensitive cardholder data in emails or documents to banks and card networks.

- It keeps things professional. Using tokens shows you have a secure, compliant process for handling financial information.

- It simplifies evidence collection. Your team can pull up transaction records using the token without ever needing access to the raw credit card details.

This approach helps you maintain a secure and efficient workflow throughout the entire dispute lifecycle, protecting your business and your customers.

At ChargePay, we help merchants automate the entire chargeback dispute process, from generating winning evidence to recovering lost revenue—all without manual work. Learn how ChargePay can boost your win rate and protect your bottom line.

.svg)

.svg)

.svg)

.svg)