Ever wonder how money magically travels from a customer's credit card to your bank account? It’s not magic—it's a payment processor.

Think of a payment processor as the essential plumbing that connects your business to the entire financial world. It’s the invisible engine working behind the scenes, making sure every credit card transaction is handled securely and efficiently from the moment a customer pays until the funds are safely in your account.

In simple terms, a payment processor is the ultimate financial translator. It allows all the different banks and card networks to speak the same language, ensuring every transaction is understood and processed correctly.

What a Payment Processor Really Does

A payment processor is the workhorse of modern commerce. Whether a customer swipes a physical card in your store or types their details into your website's checkout page, the processor is the one orchestrating the entire journey of that payment from start to finish.

This "translator" grabs the sensitive payment information from your customer and securely routes it through the correct card networks, like Visa or Mastercard. From there, it communicates directly with the customer's bank to ask a simple question: "Are there enough funds for this purchase?"

Based on the bank's "yes" or "no" response, the transaction is either approved or declined in a matter of seconds. Without this critical go-between, your business simply wouldn't be able to accept credit or debit card payments.

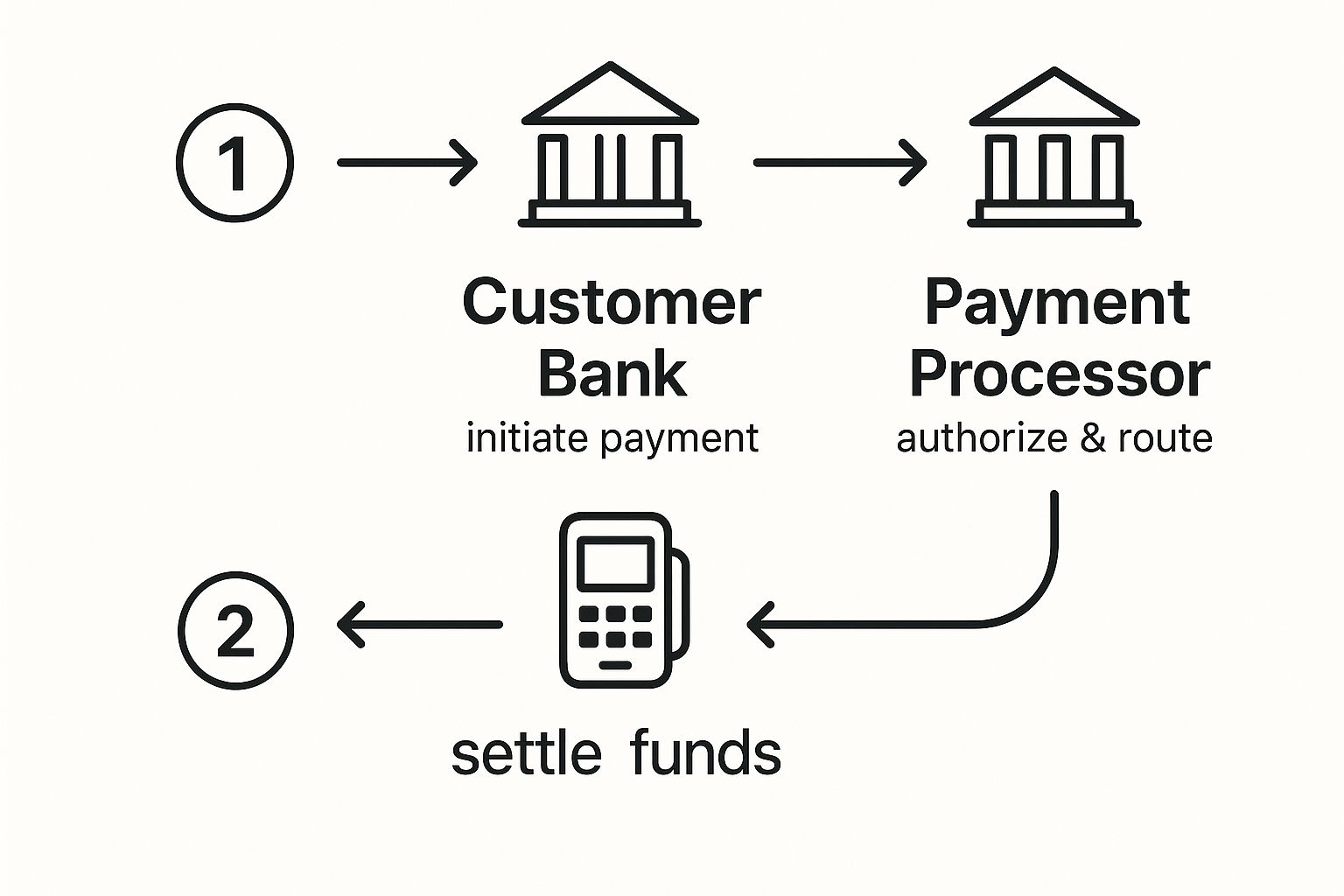

The Key Players in Every Card Transaction

Every time a customer uses their card, a few key players jump into action. The payment processor is the central coordinator, making sure everyone communicates properly so that information—and money—flows smoothly.

To make this crystal clear, let's break down who's who in the world of card transactions.

The processor sits right in the middle, connecting all these players to get the job done.

This quick overview shows how the processor acts as the central hub, sending the transaction request out for authorization and then ensuring the funds are properly settled into your business account.

This entire system is what makes those near-instant approvals we all expect at the checkout counter possible. It’s a complex dance, but it happens in the blink of an eye.

Considering that a whopping 86% of global consumers now prefer digital payments over cash, having a solid processor isn't just a nice-to-have anymore. It's an absolute necessity for survival and growth. The digital economy would grind to a halt without them. You can discover more consumer payment trends in the full report.

How a Card Transaction Actually Works

Ever wonder what really happens in those few seconds after a customer swipes their card or clicks ‘Buy Now’? It feels like magic, but behind the scenes, a complex, high-speed journey is unfolding. The payment processor is the director of this entire performance, making sure every actor hits their mark perfectly.

Think of it like a lightning-fast relay race. The baton—your customer's payment data—is passed from one player to the next at incredible speed. The whole point is to get a simple "yes" or "no" and start the process of moving money from their account to yours.

This entire sequence breaks down into three main stages: authorization, clearing, and settlement. Let's pull back the curtain and see what's happening in plain English.

Stage 1: Authorization – The Initial Handshake

This is the very first step, where your system basically asks for permission to charge the card. It all kicks off the moment your customer is ready to pay.

- The Request Begins: Your point-of-sale (POS) terminal or website’s payment gateway grabs the customer's card details. This sensitive info is then securely zapped over to your payment processor.

- The Information Relay: The processor instantly forwards that request to the correct card network, like Visa or Mastercard. The card network acts as a traffic controller, routing the request to the customer's bank—also known as the issuing bank.

- The Big Question: The customer's bank does a quick check. Do they have enough funds? Does anything look fishy? It then sends an approval or decline code back through the exact same chain—from the card network to the processor, and finally, right back to your terminal or checkout page.

This entire round trip is mind-bogglingly fast, often taking less than two seconds. It’s the reason you see "Approved" pop up almost instantly.

Stage 2: Clearing – The Transaction Log

Once the day's sales are done, all those authorization codes are just promises of payment. The clearing stage is where you bundle up all those promises and send them off to be officially processed.

At the end of your business day, you'll "batch out" your transactions. This is essentially sending a single digital file containing all of that day's approved sales to your payment processor. The processor then sorts these transactions and shoots them off to the right card networks.

The card networks act as a central clearinghouse, exchanging all the transaction data between your bank (the acquiring bank) and the dozens, hundreds, or even thousands of different customer banks (the issuing banks). This ensures every single transaction is officially logged and accounted for.

Stage 3: Settlement – The Money Arrives

Settlement is the final and, let's be honest, most important step: getting paid. This is when the actual cash moves from the customer's bank account into yours.

After the clearing process finishes its job, the issuing banks transfer the funds for all the approved transactions over to your acquiring bank, minus any interchange fees. From there, your acquiring bank deposits the money into your merchant account. This process typically takes about 24-48 hours.

Payment processors are the true backbone of this entire system. To give you some perspective, global card payment processing generated approximately $8.47 trillion USD in 2021 alone, and the use of non-cash payments just keeps climbing. These processors make modern commerce possible, ensuring every step of the payment journey is both secure and efficient. Discover more insights about the growth of electronic payments from The Nilson Report.

For an even deeper dive into the mechanics of it all, you can also explore our guide on how credit card transactions work.

Payment Processor vs Payment Gateway

In the world of online payments, it’s easy to get payment processor and payment gateway mixed up. They work so closely together that they can seem like the same thing, but they actually have two very different jobs.

Getting the distinction right is key to understanding how money actually moves from your customer’s wallet to your bank account.

Let's break it down with an analogy. Think of your e-commerce store as a busy restaurant.

The payment gateway is like the waiter who takes your customer’s credit card from the table. The waiter’s job is to securely collect the card details, keep them safe, and deliver them to the back office for processing. It’s the first point of contact for the payment information.

The payment processor, on the other hand, is the person running that back office. It takes the card details from the waiter (the gateway) and does all the heavy lifting—connecting with card networks and banks to get the transaction authorized and actually move the funds.

So, the gateway is the secure messenger, and the processor is the financial engine making it all happen.

How They Work Together as a Team

For any online sale to go through, you need both players on the field. The gateway is the secure front door on your website, while the processor handles all the complicated financial chatter in the background.

- Payment Gateway: This is the tech your customers interact with. It plugs into your website’s shopping cart, encrypts the sensitive card data, and securely passes it along to the processor. It’s basically the digital version of a physical credit card reader.

- Payment Processor: This is the financial muscle working behind the scenes. It manages the authorization and settlement, making sure the money gets from the customer’s bank to your business account.

In the early days of e-commerce, businesses had to sign up for these two services separately. You’d get a gateway from one company and a processor from another, which was often a huge headache to set up and manage.

The Rise of All-in-One Solutions

Thankfully, things are much simpler now. Modern payment companies have bundled these services into a single, seamless package.

Companies like Stripe and PayPal act as both a payment gateway and a payment processor. This creates what we call a Payment Service Provider (PSP). This all-in-one approach has made it incredibly easy for businesses to start accepting online payments without needing a ton of technical know-how.

Our guide on the PayPal checkout process digs deeper into how these integrated systems make life easier for e-commerce stores.

Understanding Payment Processing Fees

So, why does it cost money just to accept a payment? It’s a fair question. When you see a small percentage disappear from every sale, it’s only natural to wonder where that money is going.

The short answer is that every single transaction involves multiple players who all need a tiny slice of the pie for their part in making the payment happen securely.

Think of it like shipping a package. You aren't just paying the delivery driver; you're also covering the costs for the warehouse staff, the logistics software, and the fuel for the truck. Payment processing fees work the same way—they’re a bundle of small costs from different companies all working in tandem.

While the fee structures can seem complex at first glance, they mostly boil down to three core components.

The Three Main Transaction Costs

Every time a customer swipes, taps, or clicks to pay with a card, three distinct fees are charged behind the scenes. Your payment processor bundles these together, but knowing what they are helps you see exactly what you’re paying for.

- Interchange Fee: This is the big one, typically making up 70-80% of the total cost. This fee goes straight to the customer's bank (the issuing bank) to cover the risks and operational costs of approving the transaction.

- Assessment Fee: This is a much smaller fee paid directly to the card networks themselves, like Visa, Mastercard, or American Express. You can think of it as a licensing or network access fee for using their rails to route the payment.

- Processor Markup: This is the slice your payment processor keeps for their services. It’s what covers their technology, customer support, operational overhead, and, of course, their profit.

These combined costs are why you see fees on every transaction. Processors are not just middlemen; they are managing a complex financial service that involves risk, security, and multiple institutional partners.

Common Payment Processor Pricing Models

How those fees are packaged and presented to you all comes down to your processor's pricing model. You’ll usually run into one of three main structures, each with its own set of pros and cons depending on your business. Getting familiar with them is the first step toward finding a fair deal.

Here’s a look at the three main pricing models to help you understand how they stack up.

Common Payment Processor Pricing Models Compared

Most processors charge fees somewhere in the range of 1.9% to 3.5% per transaction, often plus a small fixed fee. These charges are the lifeblood of their businesses, fueling a massive global payment industry. To put its scale into perspective, the industry's revenue is projected to hit a staggering $2.7 trillion by 2025. You can discover more insights about the global payments market with McKinsey.

Understanding these models is absolutely crucial. For a practical example of how these fees can be structured, you can explore ChargePay's clear pricing model to see how a modern provider presents its costs.

How to Choose the Right Payment Processor

Picking a payment processor isn't just about finding the lowest transaction fee. It’s about finding a reliable partner that actually fits the way you do business. The right choice makes your operations feel effortless, but the wrong one can bury you in headaches and hidden costs.

To make the right call, you have to look past the advertised rates. A great processor should feel like a natural part of your business, armed with the tools you need to grow without a hitch. Start by making a checklist of what truly matters for your specific setup.

Security and Compliance Are Non-Negotiable

First things first: your customers' data has to be locked down. Any processor you even think about using must be PCI DSS compliant. This is the gold standard for security in the payments world, and it's your main shield against data breaches and fraud.

When you partner with a compliant processor, they do the heavy lifting to secure every transaction. That takes a massive amount of risk and responsibility off your shoulders, letting you focus on your business instead of getting tangled in complex security rules. This is one area where you absolutely cannot compromise.

Integration and Compatibility

How well will a new processor fit with the tools you already use? This is a huge deal. A processor that can’t connect smoothly with your e-commerce platform, accounting software, or CRM is just creating more manual work for you.

The best payment processor for your business is one that feels invisible. It should integrate so smoothly into your existing workflow that you barely notice it's there—it just works.

Look for providers that offer ready-made integrations or have clear, well-documented APIs. This is your ticket to a seamless connection between your sales channels and your financial backend, saving you a ton of time and preventing costly errors.

Payment Methods and Customer Support

These days, customers expect to pay however they want. Your processor needs to support not just the usual credit and debit cards but also popular digital wallets like Apple Pay and Google Pay. The growth of mobile wallets has been massive; by 2023, more than 4.4 billion people around the world were using digital payment methods. Offering these options is a must if you want to keep your conversion rates high. Discover more insights about digital wallet adoption from Juniper Research.

Finally, don't sleep on customer support. When something goes wrong with your payments—and eventually, it will—you need help, and you need it fast. Scour the reviews and see what other merchants are saying about their support experience. Responsive and knowledgeable support can be an absolute lifesaver when you're in a tight spot.

Popular Payment Processors for Different Businesses

Picking a payment processor isn’t a one-size-fits-all game. What works for a massive enterprise would be total overkill for a local coffee shop, and the reverse is just as true. Let’s break down some of the most popular players and figure out who they’re really built for.

For most businesses just trying to get off the ground, especially online, all-in-one platforms are a lifesaver. These guys bundle everything you need—the payment gateway, the processing, and the merchant account—into a single, straightforward package.

All-in-One Platforms for Online Businesses

If you’re running an e-commerce store or a startup, you need something that just works. Easy setup and smooth integration with your website are non-negotiable, and that’s where modern processors really shine.

- Stripe: This is the darling of tech-savvy online businesses and software platforms for a reason. Stripe is famous for its powerful APIs and developer-friendly tools that let you customize just about everything.

- PayPal: As one of the most recognized names on the planet, PayPal gives customers that warm, fuzzy feeling of a trusted checkout. It's also incredibly simple to plug into almost any website.

Processors have come a long way since the early days. Back in 1971, one of the pioneers, First Data Corporation, was founded and eventually grew to handle trillions in transactions. Today, all-in-one providers like Stripe and PayPal have become household names, each processing hundreds of billions of dollars every single year.

Solutions for Brick-and-Mortar and Large Enterprises

Businesses with a physical storefront have a different set of challenges, often needing hardware that syncs up perfectly with their software. Big corporations, on the other hand, are focused on shaving every fraction of a percent off their processing costs.

Square is an absolute powerhouse in the world of physical retail and restaurants. Their whole ecosystem of point-of-sale (POS) hardware—from simple card readers to full-blown registers—works seamlessly with their processing software. This makes them the go-to choice for countless in-person businesses.

For large-scale enterprises moving massive sales volumes, traditional merchant account providers often make more financial sense. Big players like Fiserv offer more complex pricing structures that can lead to significantly lower overall fees for high-volume merchants. For any business serious about building successful e-commerce websites, knowing which path to take is a fundamental first step.

If you’re running your store on Shopify, it's worth taking a deep dive into the specific Shopify payment processors available to find an option perfectly tailored to that platform.

Got Questions? Let's Clear a Few Things Up

Even after you get the hang of the basics, a few questions always seem to pop up when you're wading into the world of payment processors. Let's tackle some of the most common ones you might be thinking about.

Do I Need a Merchant Account?

Sometimes, but not always. Back in the day, you absolutely needed a dedicated merchant account—basically a special bank account just for holding funds from your transactions.

But things have changed. Modern, all-in-one providers like Stripe or PayPal now operate as Payment Service Providers (PSPs). They use a shared merchant account for all their users, which makes getting set up incredibly fast and simple. It's a game-changer, especially for small businesses just getting started.

What Is PCI Compliance?

Think of PCI DSS (Payment Card Industry Data Security Standard) as the rulebook for keeping card information safe. It’s a set of security standards that any business handling card data has to follow.

Getting this right is crucial for preventing fraud and data breaches. Using a PCI-compliant processor isn't just a good idea—it's non-negotiable. They handle all the complex security heavy lifting for you, which massively reduces your risk and lets you sleep better at night.

Can I switch payment processors? Absolutely. Just make sure to read your contract first and check for any early termination fees (ETFs). The good news is that many modern processors now offer simple month-to-month contracts, giving you the freedom to move if a better deal comes along.

Beyond taking payments directly, some businesses look into other ways to get funding based on their sales volume. If you're curious, you can get a great overview by reading about The Merchant Cash Advance Explained.

Ready to stop losing money to chargebacks? ChargePay uses AI to fight and win disputes for you, recovering up to 80% of your lost revenue automatically. See how much you can recover with ChargePay.

.svg)

.svg)

.svg)

.svg)