A credit card transaction isn't just a simple tap or click; it's a complex, high-speed process that moves money from your customer's bank to yours. From the customer's point of view, it’s over in seconds. But behind the scenes, a lot is happening to make that seemingly instant payment possible.

What Happens When a Customer Pays with a Card

Ever wondered what's really going on in the few seconds after a customer taps their card or hits "buy now"? It feels like magic, but it’s actually a super-fast, highly coordinated relay race. Think of it like a secure message—the transaction request—getting passed between several key players who all need to give it a thumbs-up.

This quick journey ensures every payment is verified, secure, and sent to the right place. Whether it's happening at a coffee shop or on your e-commerce store, the fundamental steps are exactly the same.

Before we dive into the stages, it's helpful to know who the main participants are in this relay race. Each one has a specific job to do to make the whole thing work.

The Four Key Players in Every Transaction

Now that we know the runners in the race, let's look at the track they run on.

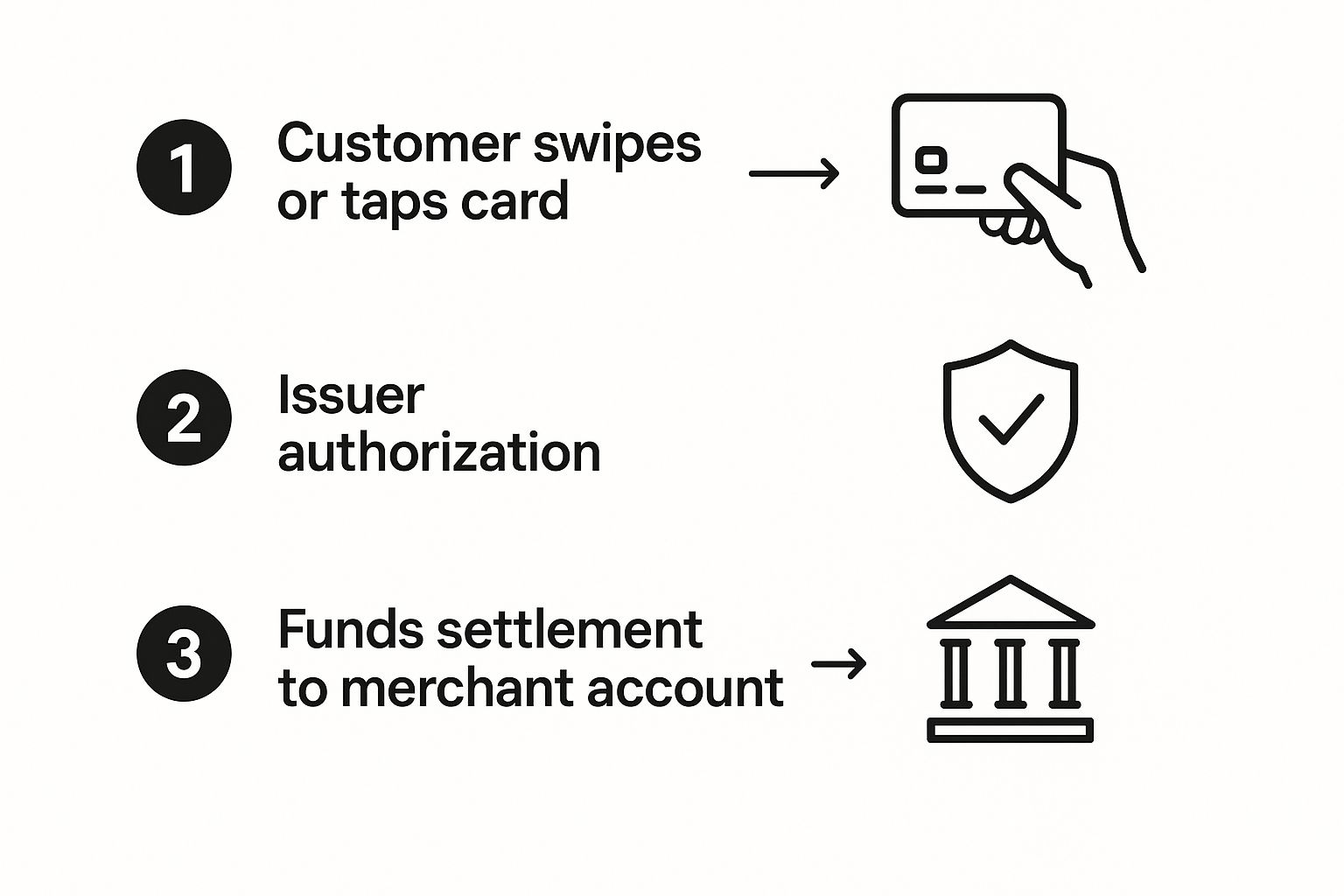

The Three Core Stages of a Transaction

Every single credit card payment unfolds in three distinct stages: Authorization, Clearing, and Settlement. Each one is critical for moving money from your customer's account to your business account safely and efficiently. Getting a handle on this flow is the first step toward mastering your payments.

This visual gives you a simple overview of how it all fits together.

As you can see, the process kicks off with the customer, zips over to the bank for a quick check, and finally wraps up when the funds land in your account.

Let's break down each phase of this incredible journey.

Authorization: This is the initial "permission slip" stage. When a customer pays, your terminal or payment gateway shoots a request through the card network (like Visa) to the customer’s bank. The bank instantly checks if the customer has enough funds and looks for any red flags, like potential fraud. If it’s all good, it sends back an approval code. That's the "Approved" message you see, and it all happens in about two seconds.

Clearing: Think of this as the nightly bookkeeping. At the end of the day, you send a batch of all your approved authorizations to your payment processor. The processor then sorts these transactions and sends them through the card networks to the correct customer banks. In this phase, the banks swap the final transaction details, confirming the exact amounts that need to be moved around.

Settlement: This is the final step—payday! The customer's bank sends the funds to your bank (the acquiring bank), which then deposits the money into your business account. This part of the process isn’t instant; it usually takes 1-3 business days for the cash to actually show up.

Key Takeaway: While authorization feels instantaneous, the actual money transfer is not. The clearing and settlement phases are what ensure you get paid accurately after the initial sale gets the green light.

This complex but lightning-fast system is the backbone of modern commerce. To give you an idea of the scale, the global credit card payments market was valued at USD 622.76 billion in 2024 and is expected to hit nearly USD 1.43 trillion by 2034. You can explore more data on credit card payment growth to see just how massive these operations are. This huge volume shows just how reliable and vital this process has become for businesses everywhere.

The Role of Visa Mastercard and Other Card Networks

If you've ever wondered how a credit card payment magically travels from your customer's wallet to your bank account, you have card networks like Visa, Mastercard, American Express, and Discover to thank. Trying to connect your business directly to thousands of different banks worldwide would be pure chaos. It's simply not possible.

This is where the card networks step in. Think of them as the architects and traffic cops of the entire payment world. They build the digital highways, set the rules of the road, and make sure every transaction gets where it needs to go safely and instantly.

They don't issue the cards or hold your money. Instead, they provide the secure infrastructure that allows your bank (the acquirer) to talk to your customer's bank (the issuer) in a split second.

Open Loop vs. Closed Loop Networks

Not all networks are built the same way. The biggest difference boils down to whether they are an "open-loop" or "closed-loop" system. Understanding this helps explain why some cards come with different fees or operational quirks.

An open-loop system is what you get with Visa and Mastercard. They act as the middlemen connecting thousands of different banks and financial institutions.

- Visa and Mastercard don’t issue cards directly. They partner with countless banks that handle the customer relationships and the money.

- This creates a massive, accessible network where a merchant can accept cards from just about any bank through a single connection.

A closed-loop system, on the other hand, is when one company does it all. American Express and Discover are the classic examples here.

- American Express is the issuer (giving the card to the customer), the acquirer (handling the payment for you), and the network, all rolled into one.

- This structure gives them total control over the whole process, from setting the merchant fees to managing disputes directly.

Why This Matters for Your Business: The closed-loop model is often why Amex fees can be a bit higher—they curate the entire experience and often cater to a higher-spending customer. Open-loop networks, however, dominate in sheer volume, which is why nearly every business on the planet accepts Visa and Mastercard.

The Rulebook for Every Transaction

Beyond just connecting banks, card networks write and enforce the rulebook for every single transaction. This covers everything from complex security protocols to the nitty-gritty of dispute resolution.

For instance, the detailed procedures for handling a payment dispute are dictated by the network. To see just how specific these rules are, you can dig into the Visa chargeback process and see the strict guidelines merchants are required to follow.

These universal standards create consistency and trust. When a customer taps their Visa card in your store or on your website, you both know the transaction will be handled securely and predictably. It’s this reliability that has made card payments the powerhouse they are today.

In fact, our reliance on these networks has exploded. In the U.S., credit cards now make up 35% of all payment transactions as of 2024, making them the most popular payment method by a wide margin. That’s a huge leap from just 18% in 2016.

This massive shift shows just how critical these networks are to modern commerce. Without them, the simple act of paying with a card would be anything but simple.

A Simple Breakdown of Processing Fees

Accepting credit cards is non-negotiable for pretty much any business these days, but that convenience isn’t free. If you’ve ever stared at a monthly processing statement and felt completely lost in a sea of percentages and jargon, you're definitely not alone.

The good news is that all those complicated fees boil down to just three core components. Think of the total fee for one transaction as a small pie cut into three slices. Each slice goes to a different player who made the sale possible. Once you understand who gets which piece, your processing costs will finally start to make sense.

Let's break down exactly where your money is going.

The Three Layers of Credit Card Fees

Every single time a customer pays with a credit card, the fee you're charged is a bundle of three separate costs. Your payment processor rolls them into one, but knowing what they are individually gives you the full picture.

Here are the three pieces of the pie:

Interchange Fees: This is the biggest slice by far, usually accounting for 70-90% of your total cost. This fee goes directly to the customer’s bank (the issuing bank) to cover the risk and operational costs of approving the payment. The rates aren't random; they're set by the card networks like Visa and Mastercard and change based on things like the card type, whether the purchase was online or in-person, and the overall risk level. For example, a premium rewards card used online will carry a higher interchange fee than a basic debit card swiped at a terminal.

Assessment Fees: This is the smallest slice of the pie. It's paid directly to the card network (Visa, Mastercard, etc.) for the privilege of using their payment rails. These fees are non-negotiable and help them maintain, secure, and improve their global networks. We're talking a tiny fraction of the sale, typically around 0.13% to 0.15%.

Processor Markup: This is the final piece and the only one you actually have some control over. It's what your payment processor—like Stripe, Square, or a traditional merchant bank—charges for their services. This is how they make their money for giving you the software, hardware, and support needed to accept cards in the first place.

Key Takeaway: Most of what you pay in processing fees are non-negotiable costs passed through to the customer's bank and the card network. The processor's markup is where you have the real opportunity to find savings.

These costs are also tied to the risk of disputes. If your business sees a lot of disagreements over payments, it can drive your fees up. Getting a handle on professional what is chargeback management is a smart way to protect your revenue and keep those costs in check.

How Processors Package These Fees

Payment processors don’t just send you three separate bills. They bundle these costs into different pricing models, and the one you choose has a huge impact on your monthly bill and how transparent your fees are.

Let’s take a look at the most common structures.

Comparing Common Pricing Models

Picking the right pricing model is a crucial decision for any merchant. Each one has its own way of packaging the interchange, assessment, and markup fees, which can make a big difference to your bottom line.

Ultimately, the best model depends on your sales volume, average ticket size, and how much complexity you're willing to handle. For many growing businesses, the crystal-clear nature of Interchange-Plus pricing offers the best insight into what they're really paying for every credit card transaction, leading to smarter financial planning.

Managing Online Fraud and Chargebacks

While opening your doors to the world of online payments is exciting, it also means dealing with a couple of major headaches: fraud and chargebacks. For any e-commerce merchant, these two are tangled together, and figuring out how to handle them is key to protecting your revenue and keeping your business healthy.

And this isn't a small problem. The numbers are staggering—financial losses from worldwide credit card transaction fraud are on track to blow past $403 billion over the next decade. That alone shows why you absolutely need a solid defense in place.

The Most Common Threats for Merchants

When you think of fraud, you might picture a hacker in a dark room. But honestly, the biggest threats often come from less obvious places. As an online business owner, you have to know what you're up against.

One of the most maddening types is what's known as friendly fraud. This is when a real customer buys something from you but then calls their bank to dispute the charge, claiming they never made the purchase or received the goods. It doesn’t matter if they did it on purpose or by mistake; the end result is a chargeback you now have to fight.

The best way to tackle these threats is with a security strategy that has multiple layers.

- Address Verification Service (AVS): This is a simple but effective tool that cross-references the billing address the customer enters with the one their bank has on file.

- Card Verification Value (CVV): You know that three- or four-digit code on the back of the card? Requiring it proves the customer physically has the card in their hand.

- AI-Powered Fraud Detection: Modern systems use smart algorithms to analyze transaction patterns on the fly, catching weird behavior that older, rule-based systems would totally miss.

Building a Secure Checkout Experience

Keeping your customers' data safe isn't just a nice thing to do—it's a must. Two core concepts, PCI DSS compliance and tokenization, are the bedrock of any secure payment setup. Getting a handle on them helps you build trust and lock down every single credit card transaction.

PCI DSS (Payment Card Industry Data Security Standard) is basically a security rulebook that any business accepting card payments has to live by. Think of it as a mandatory checklist for handling sensitive info, making sure your network is secure and you're protecting cardholder data.

Tokenization is a slick security trick that works like a secret decoder ring. When a customer types in their card details, tokenization swaps the real card number for a unique, meaningless string of characters called a "token." This token is safe to use for future payments because, even if stolen, it's completely useless to a fraudster without the original data.

Why This Matters: Put them together, and PCI compliance and tokenization create a powerful shield. They seriously cut down the risk of a data breach and give customers the peace of mind that their information is safe with you—which is everything when it comes to building loyalty.

Understanding the Chargeback Process

Even with ironclad security, chargebacks are just part of the game when you sell online. A chargeback is simply a forced reversal of a payment, started by the customer's bank. It was created to protect shoppers from shady charges, but it can be a huge drain on your time and money.

Here’s how it usually goes down:

- The Dispute: A customer spots a charge they don't recognize and calls their bank to question it.

- The Provisional Credit: The bank usually gives the customer their money back right away, at least temporarily.

- The Merchant Notification: You get a notice about the chargeback and are given a tight deadline to respond.

- Representment: It's your turn to fight back. You gather evidence—like shipping confirmations or emails—to prove the transaction was legit and submit your case.

- The Final Decision: The card network reviews everything and makes the final call.

Trying to navigate this can feel like a nightmare, but having a proactive plan makes all the difference. For a deeper dive into defending your business, our guide on credit card chargeback protection is packed with valuable insights. A solid strategy can help you win back revenue you might otherwise lose for good.

Smarter Payment Processing for Your Business

Knowing how a credit card transaction works is one thing. Making the process work for your business is a whole different ballgame—and it’s where you can really stand out. Instead of looking at payment processing as just another line item on your expense sheet, you can turn it into a powerful tool for growth by focusing on a few key areas.

This isn’t about flipping your whole operation upside down overnight. It’s about making small, smart tweaks that lead to lower fees, happier customers, and way fewer headaches from disputes.

Lowering Your Processing Costs

While you can't negotiate every processing fee, you absolutely have some control. There are specific strategies you can use to qualify for lower rates, especially if you handle business-to-business (B2B) sales. One of the most effective ways to do this is by providing what’s known as Level 2 and Level 3 data.

Think of a standard transaction as giving the bank just the basics—the "who" and "how much." Level 2 and Level 3 data paints a much fuller picture.

- Level 2 Data: This adds details like the sales tax amount and a customer code.

- Level 3 Data: This gets even more granular, including line-item details like item descriptions, quantities, and shipping info.

When you pass along this extra information, you dramatically lower the perceived risk for the issuing bank. In return, they give you a better deal on interchange rates for those corporate or government card transactions. The savings can be huge, often cutting your costs by up to 1% per transaction.

Key Insight: You can directly lower the cost of accepting B2B payments by simply passing along more data—information you probably already have. Check with your payment processor to see if they support Level 2/3 data so you can start banking those savings.

Refining the Checkout Flow

Your checkout page is make-or-break. A clunky, confusing, or sketchy-looking process is one of the top reasons people abandon their carts. The goal is simple: make paying as easy and secure as possible.

This is all about finding the right balance between security and convenience. Tools like Address Verification Service (AVS) and CVV checks are must-haves for stopping fraud. AVS makes sure the billing address matches what the card issuer has on file, and a CVV check proves the customer actually has the card in their hand.

But if you get too strict, it can backfire. If your system declines a good customer just because they typed "St." instead of "Street," you're not just losing a sale—you're creating a frustrated ex-customer. Fine-tuning these settings is critical to approve more legitimate orders without giving fraudsters an open invitation. For more tips on this, check out our guide to help you prevent ecommerce fraud.

Improving Customer Communication to Minimize Chargebacks

Clear, proactive communication is your best weapon against chargebacks, especially the "friendly fraud" kind where a customer disputes a charge simply because they're confused. A few simple steps can make all the difference.

First, make sure your billing descriptor is instantly recognizable. That's the little line of text that shows up on their credit card statement. It needs to clearly state your business name, not some random corporate entity, to stop those "I don't remember buying this" disputes in their tracks.

Next, make your customer service easy to find and easy to reach. If a customer runs into a problem, you want their first instinct to be contacting you, not their bank. Provide clear contact info on your site, send order and shipping confirmation emails right away, and be quick to respond to questions. It’s all about building trust and solving problems before they blow up into a formal dispute.

As the market keeps growing, getting these things right becomes even more important. In 2025, the United States is still the biggest credit card market on the planet, with over 631 million active accounts. This massive user base is a huge opportunity for merchants who know how to manage their payments effectively. By focusing on these strategies, you can turn payment processing from a necessary evil into a strategic asset that fuels your success.

Frequently Asked Questions About Credit Card Transactions

Even after you've got the basics down, the world of credit card transactions is full of little details that can trip you up. Here are some of the most common questions we hear from business owners, answered in plain English to help you handle payment processing like a pro.

How Long Until I Get My Money?

This is the big one, right? A customer pays, the transaction is approved... so where's the cash?

Typically, the money from a credit card sale will land in your business bank account within 1-3 business days. This waiting period is called settlement. Behind the scenes, your bank (the acquirer) and the customer's bank (the issuer) are squaring up the numbers before the final transfer happens.

The exact timing isn't set in stone. It can be influenced by your payment processor, your bank's specific policies, and even the time of day the sale was made. Sales made over a weekend or on a holiday, for example, usually take an extra day or so to show up.

Payment Processor vs. Payment Gateway

These two terms get thrown around and used interchangeably all the time, but they're not the same thing. Knowing the difference helps you understand what's happening with your tech.

Here's a simple way to think about it: The payment gateway is like a secure, armored truck that picks up the customer's sensitive card information from your website. The payment processor is the central sorting facility where that information is routed to all the right banks to get the payment approved and moved.

Analogy in Action: A payment gateway (like Authorize.net) securely grabs the encrypted payment details from your checkout page. It then hands that info off to the payment processor (like Stripe or Square), which does the heavy lifting of communicating with the card networks and banks to actually move the money.

These days, many modern providers bundle both services into one seamless package. This makes life much easier for you, as you only need one partner to handle both the secure data transmission and the financial plumbing.

Why Do American Express Transactions Cost More?

If you've ever looked closely at your processing statements, you've probably noticed that American Express fees can be a bit higher than Visa or Mastercard. It’s not arbitrary—it’s built into how Amex works.

Amex operates on a "closed-loop" network. This just means that Amex is the issuer (giving cards to customers), the acquirer (working with you, the merchant), and the network. They control the whole process from start to finish.

This setup often leads to higher fees for a few reasons:

- Premium Customers: Amex has always courted a higher-spending customer base, offering them killer rewards and benefits. Those higher merchant fees are what fund those perks.

- Perceived Value: Amex makes the case that its cardholders are more valuable to your business because they tend to spend more per purchase.

- Direct Control: Because they don't have to negotiate with thousands of banks, Amex sets its own rates, and they've historically been higher than the competition.

While the gap isn't as wide as it used to be, accepting Amex can still cost a little more. For most businesses, though, getting access to their loyal, high-spending customers is easily worth the slightly higher fee.

Can My Business Refuse Credit Cards?

In the United States, yes, a private business can generally choose which payment methods to accept. That means you can decide to be cash-only, or you can choose to accept Visa and Mastercard but not American Express.

But before you ditch plastic entirely, there are a couple of big things to consider.

First, your merchant agreement with your payment processor has rules. Many of these agreements forbid you from setting a minimum purchase amount for credit card use or tacking on an extra fee for card payments. While surcharging is legal in most states now, you have to follow very specific rules to do it correctly.

More importantly, not accepting credit cards can seriously shrink your pool of potential customers. People love the convenience, security, and rewards that come with using their cards. Going cash-only could mean turning away a huge chunk of your market.

What Is a Chargeback and Can I Fight It?

A chargeback is basically a forced refund initiated by a customer's bank. It was created to protect consumers from fraud, but it's become a massive headache for merchants, especially with the rise of "friendly fraud"—when a customer disputes a purchase they actually made.

When a chargeback is filed, the money is instantly pulled from your account while the banks investigate. You're then given a short window to fight back by providing evidence that the transaction was legitimate. This formal response process is known as representment.

And yes, you absolutely can—and should—fight back against bogus chargebacks. To win, you need solid proof, like:

- Shipping confirmations with tracking numbers showing delivery.

- Emails or support chats with the customer.

- Records showing the customer has made other, undisputed purchases from you before.

The whole process can be a real time-sink. For a deeper dive into building a winning case, our guide explains how to win a credit card dispute and keep the revenue you earned.

Trying to manage chargebacks on your own is a recipe for lost time and money. ChargePay uses AI to automate the entire dispute process. It builds winning evidence packets in real-time to get your money back without you having to do a thing. Find out how you can boost your win rates at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)