To really get a handle on preventing ecommerce fraud, you have to first appreciate what it truly costs you. It's so much more than just the price tag on a stolen item. A single fraudulent order kicks off a domino effect of hidden fees, wasted time, and lost opportunities. This is why getting proactive about fraud prevention isn't just a security task—it's a core business strategy.

The True Cost of a Fraudulent Order

When a bad order slips through, it’s natural to focus on the lost merchandise. A scammer snags a $100 pair of sneakers, you're out $100. Simple, right?

Not even close. That's just the tip of the iceberg.

The real financial damage runs much deeper, and it often stays hidden until you start digging into the numbers. This is what we in the industry call the "fraud multiplier," and it's a silent killer for your profit margins. For every dollar you lose to the initial transaction, a whole cascade of other expenses follows.

How a Single Fraudulent Order Adds Up

The initial product loss is just where the bleeding starts. Here’s a look at the "fraud multiplier" in action, showing just how quickly the costs stack up from one bogus order.

This table shows how a single $100 fraudulent purchase can actually cost your business $180 or more. That's nearly double the product's value walking out the door. When this happens repeatedly, the impact on your bottom line is massive.

Beyond the numbers in the table, you're also losing out on things that are harder to quantify but just as damaging:

- Chargeback Fees: Banks hit you with a non-refundable fee—usually $15 to $25—for every single chargeback. You pay this whether you win the dispute or not.

- Shipping and Fulfillment Costs: All the money you spent on postage, boxes, tape, and the labor to pack the order? Gone for good.

- Customer Acquisition Costs: Think about the ad spend, marketing efforts, and time it took to attract that "customer." That's all completely wasted.

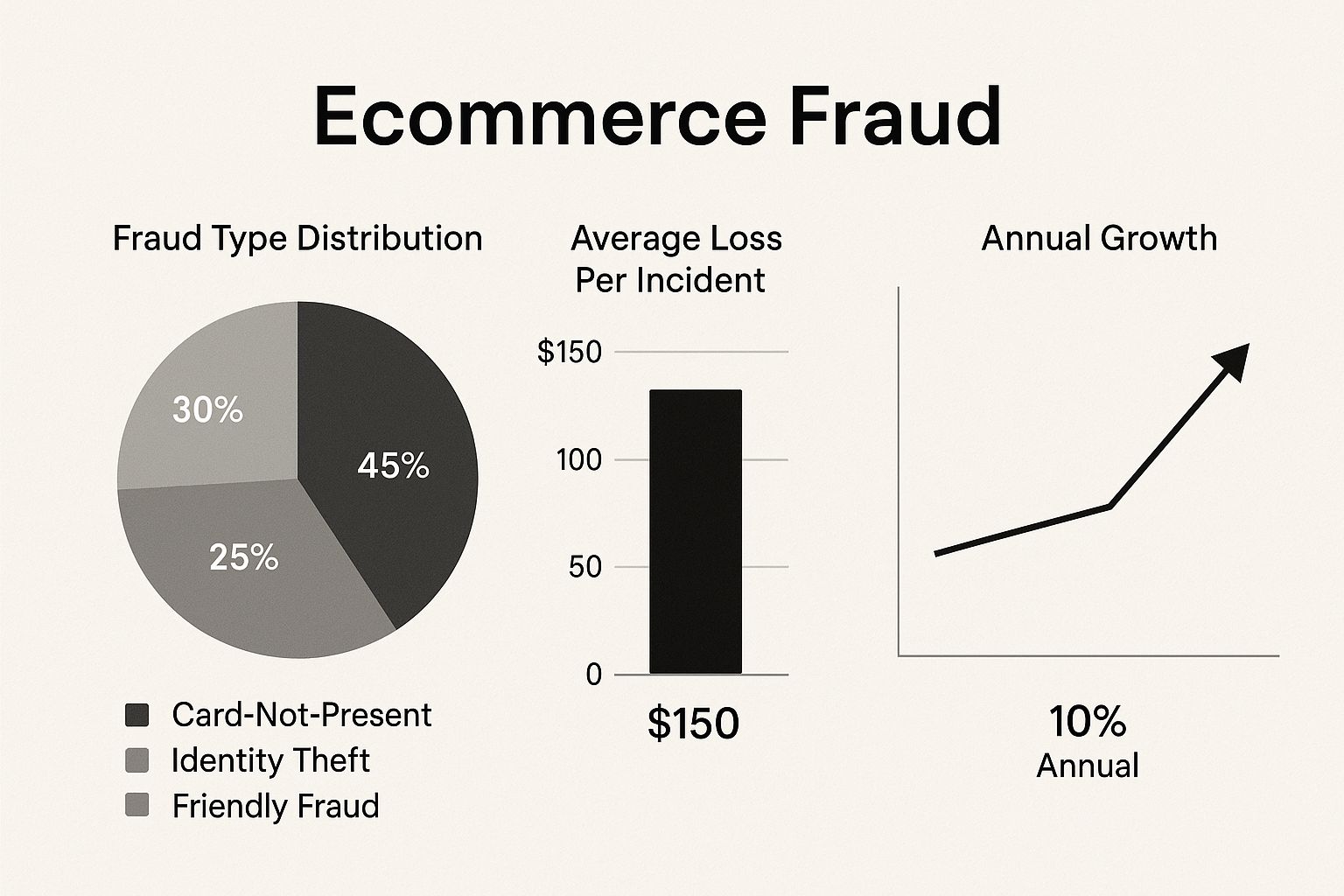

This infographic breaks down some of the most common types of fraud and just how fast they're growing.

As you can see, card-not-present (CNP) fraud is still the biggest headache for online stores, which makes sense—it’s where we're most vulnerable.

The harsh reality is that the final bill for a single fraudulent order can easily be more than double the original product's value. This multiplier effect is why a seemingly small fraud problem can quietly drain your resources and stop your business from growing.

The industry projections are pretty staggering. Ecommerce companies are on track to lose around $48 billion a year to fraud by 2025. That number covers everything from straight-up payment fraud to people abusing your return policies.

When you factor in all those hidden costs, the real damage gets amplified to about $207 for every $100 of fraudulent orders. If you want to dive deeper into the numbers, check out the latest ecommerce fraud statistics from ClickPost.ai. It's crystal clear that just sitting back and reacting isn't an option anymore for any business that wants to stick around.

Recognizing Red Flags in Customer Orders

Fraudsters aren't ghosts; they leave footprints all over their orders if you know what you're looking for. Learning to spot these clues is your first, and often best, line of defense to stop ecommerce fraud before it ever impacts your bottom line.

The real key is moving beyond the obvious and training your eye to catch the subtle patterns. It’s rarely about one single suspicious detail. Instead, it’s about how several small red flags can come together to paint a much clearer picture of a risky transaction.

Mismatched Shipping and Billing Details

One of the most classic signs of a fraudulent order is a mismatch between the billing and shipping addresses. Of course, there are plenty of legitimate reasons for this—someone could be sending a gift, for example. Still, it's a detail that should always make you pause and take a closer look.

The warning sign gets much bigger when the addresses are not just different but are in completely separate countries. Picture this: a billing address in Florida and a shipping address in Eastern Europe. This kind of discrepancy is a huge indicator that a criminal is using stolen card details from one region to ship goods to another.

Never automatically cancel an order just because the addresses don't match. Use it as a trigger for a quick manual review. A simple cross-check of other details can often tell you everything you need to know.

Unusual Order and Customer Behavior

Next up, you have to pay close attention to the order itself. Fraudsters behave differently than your typical customers because their goals are different. They want to get their hands on high-value goods as quickly as possible before the real cardholder realizes their information has been stolen and shuts the card down.

Keep an eye out for these tell-tale signs:

- Unusually Large First-Time Orders: A brand new customer dropping thousands of dollars on your most expensive products should raise an eyebrow. Real customers almost always test the waters with a smaller purchase first.

- Multiple Orders in Quick Succession: Did someone just place five separate orders to the same address using five different credit cards? This is a massive red flag for card testing, where criminals check if stolen card numbers are active.

- Requests for Expedited Shipping: Scammers always opt for the fastest shipping method available. They need the goods delivered before the legitimate cardholder notices the charge and reports it as fraud.

This behavior often boils down to personal data theft. Criminals use stolen information to make these purchases, which is exactly why you see these odd patterns.

On top of that, look at the customer's contact info. Disposable-looking email addresses (like kjshdflk234@yahoo.com) or names filled with random characters are often signs of a fake account created for a one-time fraudulent purchase. These small details, when combined, create a powerful filter. As your business grows, you'll also want to learn how to handle the inevitable disputes that come from these situations, which we cover in our guide to ecommerce chargeback fraud.

Building Your Fraud Prevention Toolkit

Trying to stop e-commerce fraud with a single tool is like trying to guard a castle with just one watchtower. It's a recipe for disaster. Today's criminals are just too sophisticated, and their tactics are always changing. The only real way to protect your store is to build a layered defense system—a stack of tools working together to create a solid safety net.

This multi-layered approach means that if one tool happens to miss a red flag, another one is right there to catch it. The goal is simple: create a process that slams the door on criminals without ever getting in the way of your legitimate customers. You want a smooth, frictionless checkout for them and a dead end for fraudsters.

The Foundational Layers of Defense

Every online store, no matter its size, has to start with the fundamentals. These are the non-negotiable tools that form the bedrock of your fraud prevention strategy. Think of them as the basic locks on your front door—they won’t stop a determined thief, but they’ll definitely keep the opportunistic ones out.

Address Verification Service (AVS): This should be your first line of defense, hands down. AVS checks if the billing address the customer enters matches the one their credit card company has on file. Any mismatch, whether partial or complete, is an immediate signal to take a closer look.

Card Verification Value (CVV): That little three- or four-digit code on the back of a credit card is a powerful gatekeeper. Requiring a CVV helps confirm that the person making the purchase actually has the physical card. This makes life much harder for criminals who've only scraped card numbers from a stolen database.

But let's be real—these tools aren't foolproof. Sophisticated fraudsters often get their hands on full sets of stolen data, including CVV codes and billing addresses. That’s why you absolutely have to add more advanced layers on top.

Adding Advanced Detection Tools

Once you have the basics covered, it's time to bring in the heavy hitters. These advanced tools analyze data points that are much, much harder for a fraudster to fake, giving you a far more accurate picture of who is really behind each transaction.

Take IP geolocation, for instance. This tool instantly shows you where an order is physically originating from. If a customer's IP address is in Nigeria but the billing and shipping addresses are in Ohio, that’s a massive red flag that demands an immediate manual review.

Another incredibly powerful tool is device fingerprinting. This technology creates a unique ID for every device—laptop, smartphone, tablet—used to place an order. If a fraudster tries to hit you again with a different name, email, or credit card, you can still block them instantly because you recognize their device.

A layered approach is all about creating a web of security checkpoints. Each tool verifies a different piece of the puzzle. When you combine their signals, you get a much clearer, more reliable risk assessment for every single order.

When assembling your fraud prevention toolkit, it's also smart to think through the security features of various secure payment methods. Layering these technologies is especially crucial for merchants on high-volume platforms; you can dive deeper into platform-specific tactics in our guide to Shopify fraud prevention. By combining these tools, you're not just blocking fraud—you're building an intelligent system that can expertly separate your best customers from the bad actors.

Using AI to Outsmart Modern Fraud

As your business scales, trying to manually review every single order just isn't going to cut it. It’s a recipe for burnout and missed fraud. This is where modern tech—specifically artificial intelligence (AI)—steps in to do the heavy lifting. Forget the sci-fi stuff; in our world, AI is all about using smart systems to crunch data at a scale no human team could ever dream of.

Think about it. A manual review might catch five or six obvious red flags, like a mismatched shipping address or a weird-looking email. An AI-powered system, on the other hand, can analyze thousands of data points in less than a second. It’s looking at everything from the customer's device and IP address to their browsing behavior and purchase history.

Based on that massive analysis, the system spits out a simple risk score for each transaction. This instantly separates the good from the bad. Obviously safe orders fly right through, and clearly fraudulent ones get blocked on the spot. This frees up your team to focus their expertise on that small handful of "gray area" orders that actually need a human touch.

How AI Learns and Adapts

The real magic of AI isn't just its speed; it's the ability to learn. Old-school fraud rules are static. You set them, and they stay that way until you change them again. For example, you might create a rule to "block all orders over $1,000 from a new customer." The problem? That can easily block legitimate customers while missing clever fraudsters who know how to stay just under the limit.

AI doesn't bother with these rigid, one-size-fits-all rules. Instead, it uses machine learning to spot complex, ever-changing patterns of bad behavior.

- It learns what a "normal" transaction looks like for your specific store.

- It finds subtle connections between seemingly unrelated orders that a person would never catch.

- Most importantly, it adapts in real time as fraudsters shift their tactics.

When a new fraud pattern pops up, the AI system learns from it and automatically updates its logic to block similar attempts in the future. This means your defenses get stronger and smarter with every single transaction.

Making Automation Work for You

Putting this kind of technology to work has a massive impact on your ability to stop ecommerce fraud in its tracks. AI-powered fraud detection systems have shown an impressive average accuracy of 92%. That high level of precision means you can confidently automate the vast majority of your order reviews. You can find more details on how these advanced countermeasures are working in global markets.

This level of automation is the cornerstone of effective credit card chargeback protection, as it stops fraudulent transactions long before they can become expensive disputes. By letting AI handle the bulk of the work, you not only beef up your security but also create a much smoother checkout experience for your real customers. It's all about working smarter, not harder, to keep your business safe.

Creating Strong Internal Policies and Training

Even the most sophisticated fraud detection software is only one part of the equation. Without a well-trained team and clear internal rules, you’re leaving massive gaps in your defense. Building a security-first culture isn't just a buzzword; it's essential for stopping ecommerce fraud in its tracks.

Think of your team, especially your customer service reps, as your human firewall. They're on the front lines every day, talking to customers and processing orders. When everyone on your team knows the game plan, they can spot subtle threats that automated systems might overlook.

This all comes down to creating simple, easy-to-follow guidelines. When your team feels confident and prepared, they transform from a potential vulnerability into one of your strongest assets.

Developing Clear Fraud Prevention Policies

You absolutely need to establish straightforward procedures for handling risky situations. Good policies take the guesswork out of the equation and ensure everyone responds consistently, every single time.

A useful policy document isn't a 50-page legal manuscript gathering dust on a shelf. It should be a practical, living checklist that gives your team immediate answers to the questions they face daily.

Here's what your internal policies should nail down:

- Manual Review Triggers: Define the exact red flags that automatically send an order to a human for a second look. This could be anything from a high-value, first-time purchase to a shipping address in a high-risk country.

- Customer Verification Steps: Outline the specific process for verifying a suspicious order. Maybe it’s a quick phone call to the number on file or a polite email asking for confirmation of the purchase details.

- Refund and Return Rules: Set crystal-clear conditions for issuing refunds to prevent friendly fraud and policy abuse. For example, you might require photo evidence for any "item damaged in transit" claim.

- Data Protection: Specify exactly how customer data should be handled, who can access it, and how it must be stored to keep everything secure and compliant.

The goal isn't to create more red tape; it's to build a clear roadmap. When an employee faces a tricky situation, they should know precisely who to ask and what to do, without a moment's hesitation.

Training Your Team to Be Fraud Detectives

Policies are just words on a page until your team understands them inside and out. Regular, hands-on training is what turns those guidelines into real-world action. Your people play a vital role in protecting customer data, especially from account takeover attempts.

The key is to focus your training on the actual scenarios your team will likely encounter.

Key Training Areas for Your Staff

- Spotting Phishing Scams: Teach them how to recognize suspicious emails or messages designed to steal login credentials. Show them what to look for—weird sender addresses, grammatical mistakes, and an urgent, demanding tone.

- Handling Social Engineering: Fraudsters are slick. They might call customer service, pretending to be a legitimate customer, and try to change a shipping address or gain account access. Train your team to verify identity with specific, pre-determined security questions before making any changes.

- Chargeback Procedures: While software can automate a lot of the chargeback process, your team still needs to grasp the fundamentals. Knowing how to properly document evidence, for example, can be the difference between winning and losing a dispute. We dive deep into this in our guide on how to prevent PayPal chargebacks.

By investing in your team’s knowledge, you empower every single employee to be a proactive part of your fraud prevention strategy. This human layer of security is truly invaluable.

Common Questions About Ecommerce Fraud

Even with the best tools and policies locked in, you'll probably still have questions bubble up about stopping ecommerce fraud. Getting clear, straightforward answers is the only way to build a strategy you can feel confident about. Here are a few of the most common questions we hear from store owners just like you.

Will a Tough Fraud Prevention System Scare Away Good Customers?

That's a valid worry, and one we hear a lot. But a smart system knows how to find the right balance. Modern tools are designed to do their best work behind the scenes, using things like behavioral analytics that are completely invisible to your shoppers. They don't just throw up annoying roadblocks for everyone.

An extra verification step, like a quick text message code, only gets triggered when a transaction flags several high-risk signs at once. The real goal is to avoid "false positives"—that’s the industry term for mistakenly blocking legitimate customers. By using AI that actually learns from your store's unique data, you can block fraudsters with pinpoint accuracy while keeping the checkout process silky smooth for your real customers.

I Am Just a Small Business—Do I Really Need to Worry About This?

Yes, absolutely. In fact, you might be a bigger target than you think. Fraudsters often specifically go after smaller businesses because they assume security is weaker. This makes you an easy, low-risk target for them to test batches of stolen credit cards.

For a small business, the financial sting of fraud hits much harder.

Even just a handful of chargebacks can seriously disrupt your cash flow and put your payment processing accounts in jeopardy. Implementing the basics, like AVS and CVV checks, and simply knowing the red flags is a crucial first step for any online store, no matter its size. Building good security habits from day one will save you a fortune in lost money and headaches down the road.

Fraud isn't just a big-brand problem. In many ways, small businesses are more vulnerable because every single dollar of lost revenue and every chargeback fee has a much bigger impact on the bottom line.

What Is the Difference Between Friendly Fraud and Chargeback Fraud?

They might sound similar, but the core difference really comes down to intent.

Chargeback fraud is what most people picture when they hear the word "fraud"—a criminal uses a stolen credit card to buy something. The real cardholder eventually sees the unfamiliar charge on their statement and, quite rightly, reports it to their bank to get their money back.

Friendly fraud, on the other hand, is when a legitimate customer makes a purchase and then disputes the charge with their bank. This can happen for a few reasons:

- They have a case of buyer's remorse and see it as an easy way out of a return policy.

- They simply don’t recognize your store's billing descriptor on their bank statement.

- A family member used their card without them knowing.

While it's not always intentionally malicious like traditional fraud, friendly fraud is still a massive, and growing, problem for merchants. It takes clear communication, detailed record-keeping, and excellent customer service to sort out. For more answers to your pressing questions, check out our extensive guide covering more FAQs on chargebacks and fraud.

Ready to stop losing revenue to chargebacks? ChargePay uses AI to automate the entire dispute process, recovering up to 80% of your lost funds without any manual work. Protect your business and boost your win rate today.

.svg)

.svg)

.svg)

.svg)