Ecommerce fraud prevention is all about the strategies and tools you use to stop bogus transactions and shield your business from taking a financial hit. It’s your front-line defense against everything from stolen credit cards to chargeback abuse, making sure your revenue—and customer trust—stay right where they should be.

Understanding the Real Cost of Ecommerce Fraud

When you hear "ecommerce fraud," your mind probably jumps straight to the cost of a lost product and the sting of a chargeback. That's definitely a big piece of the puzzle, but it's really just the tip of the iceberg. The true cost of fraud runs much deeper, impacting your operations and leaving a mark long after the transaction is over.

Think about the operational drain for a minute. Every single suspicious order that gets flagged needs a manual review. That means someone on your team has to drop what they're doing to dig into transaction details, check IP addresses, and try to verify customer info. Those hours are spent on damage control, not on growing the business, and they add up fast.

The Hidden Financial Drains

Beyond that initial loss, a whole host of hidden expenses can quietly chip away at your bottom line. These are the costs that are easy to overlook but can be just as damaging.

- Chargeback Fees: Payment processors don't just take the money back. They also slap you with a separate fee for every single dispute, usually somewhere between $15 to $100 a pop.

- Increased Processing Fees: If your chargeback rate climbs too high, you risk being labeled a "high-risk" merchant. That can lead to significantly higher transaction fees on every sale you make.

- Loss of Payment Processing: In a worst-case scenario, if fraud levels stay out of control, you could lose your merchant account entirely. That makes it nearly impossible to accept credit card payments, which is a death sentence for an online store.

The scale of this problem is staggering. Globally, ecommerce fraud losses are projected to hit a massive $343 billion between 2023 and 2027. We're already seeing annual losses hover around $48 billion. Sift.com has some more eye-opening stats on this if you want to dig deeper.

Common Threats Every Online Store Faces

To build a solid defense, you first have to know your enemy. Fraudsters are always cooking up new schemes, but most of their attacks fall into a few familiar categories. Spotting these is key to stopping them in their tracks.

One of the most common issues by far is chargeback fraud, which makes up about 34% of all ecommerce fraud. This often includes what’s known as "friendly fraud," where a real customer disputes a legitimate charge. Sometimes it’s an honest mistake, but plenty of times, it's a deliberate attempt to get something for free. You can learn more about the complexities of friendly fraud in our detailed guide.

Another huge threat is account takeover (ATO), accounting for roughly 29% of cases. This is where a fraudster gets into a real customer's account, usually with stolen login details, to make purchases or swipe personal data. This doesn't just cost you money—it shatters the trust your legitimate customers have in you. Protecting your store isn't just about saving a few bucks; it's about safeguarding your reputation for the long haul.

Building Your Foundational Fraud Defenses

Let's get practical. You don't always need a massive budget or a team of security experts to start preventing ecommerce fraud. In fact, some of the most powerful defenses are the simple, foundational tools that every online store—big or small—should have switched on from day one.

These are your non-negotiables for transaction security.

Think of these tools as the locks on your digital front door. You wouldn't leave your physical shop unlocked overnight, right? The same logic applies here. Processing online payments without these basic checks is like putting out a welcome mat for fraudsters.

Your First Line of Defense: AVS and CVV

The two most essential tools in your starter kit are the Address Verification System (AVS) and the Card Verification Value (CVV). Nearly every payment processor offers these checks. Your job is to make sure they're not just enabled, but also configured to flag or outright block suspicious transactions.

AVS is pretty straightforward: it checks the numbers in the billing address a customer enters against the address the card-issuing bank has on file. If a fraudster has a stolen card number but doesn't know the cardholder's real address, AVS will catch that mismatch instantly.

Similarly, the CVV is that three- or four-digit code on the back of a credit card. Requiring it proves the customer either has the physical card or at least has access to its full details. Since this number is never stored in merchant databases after a transaction, it's a potent defense against data breaches where only card numbers were stolen.

Key Takeaway: Setting strict rules for AVS and CVV mismatches is crucial. A partial match might just be a typo, but a complete mismatch should immediately raise a red flag. That transaction should either be blocked automatically or funneled into a manual review queue.

Shifting Liability with 3D Secure

Another powerful layer you can add is 3D Secure. You’ve probably seen it in action yourself—it’s often branded as 'Verified by Visa' or 'Mastercard SecureCode'. This tech adds an extra authentication step at checkout, usually asking the customer to enter a one-time password sent to their phone or approve the purchase through their banking app.

I know what you might be thinking: "Won't that add friction?" While it does add a step, the security payoff is enormous. When a transaction is authenticated with 3D Secure, the liability for any resulting fraudulent chargeback often shifts from you, the merchant, to the card-issuing bank.

This "liability shift" is a total game-changer, especially if you sell high-value items.

- How it helps you: It drastically cuts down your financial risk from certain types of fraud.

- What it does for customers: It gives them an extra layer of security, making them feel safer and more confident buying from you.

Establishing a Secure Foundation

Putting these foundational defenses in place is just the beginning. The best approach to security is always a holistic one. To build a strong defense against all sorts of threats right from the start, check out this ultimate website security checklist for more comprehensive steps. It gives you a clear roadmap for protecting your entire site, not just your checkout.

Don't forget, a secure checkout process does more than just stop fraud—it builds customer trust. When shoppers see you're serious about security, they're more likely to finish their purchase and come back again. This positive experience is a core part of great customer relations, and you can explore more best practices in customer service to build that loyalty even further.

Ultimately, these initial security measures create a solid baseline, making it much harder for casual fraudsters to succeed and freeing you up to focus on what really matters: growing your business.

Tailoring Fraud Rules for Your Business

A one-size-fits-all approach to ecommerce fraud prevention is a recipe for trouble. The simple truth is that the fraud risks you face are deeply tied to what you sell and how you sell it. A generic set of rules might catch the most obvious stuff, but it's going to leave gaping holes that are specific to your business model.

Think about it this way: the dangers for a store selling instantly delivered digital gift cards are worlds away from those of a retailer shipping high-end luxury handbags. Each has unique vulnerabilities that fraudsters can't wait to exploit. Your job is to understand your specific weak spots and build a defense that directly counters them.

Different Products, Different Problems

First things first, you need to analyze your own product catalog and customer behavior. Are you selling physical goods, digital products, or a subscription service? The answer dramatically changes your fraud prevention priorities.

A store selling expensive electronics needs to be on high alert for chargebacks and items being stolen in transit. In contrast, a SaaS company offering a monthly subscription is probably more worried about trial abuse and people using stolen credit cards to get a few months of free service.

Key Takeaway: Effective ecommerce fraud prevention isn't about flipping every possible security switch to "on." It's about a careful, deliberate process of identifying your unique risks and applying the right tools to mitigate them without frustrating legitimate customers.

This is where custom rules really show their power. For instance, ecommerce fraud prevention strategies have to be designed for different sectors. Digital goods and services tend to see higher fraud rates, so those businesses should zero in on tools like device fingerprinting and monitoring email age. Subscription services, on the other hand, constantly battle trial abuse, making IP address tracking a much more effective tool. Meanwhile, sellers of luxury goods attract more calculated fraudsters, making manual order reviews and signature verification for shipping absolutely essential.

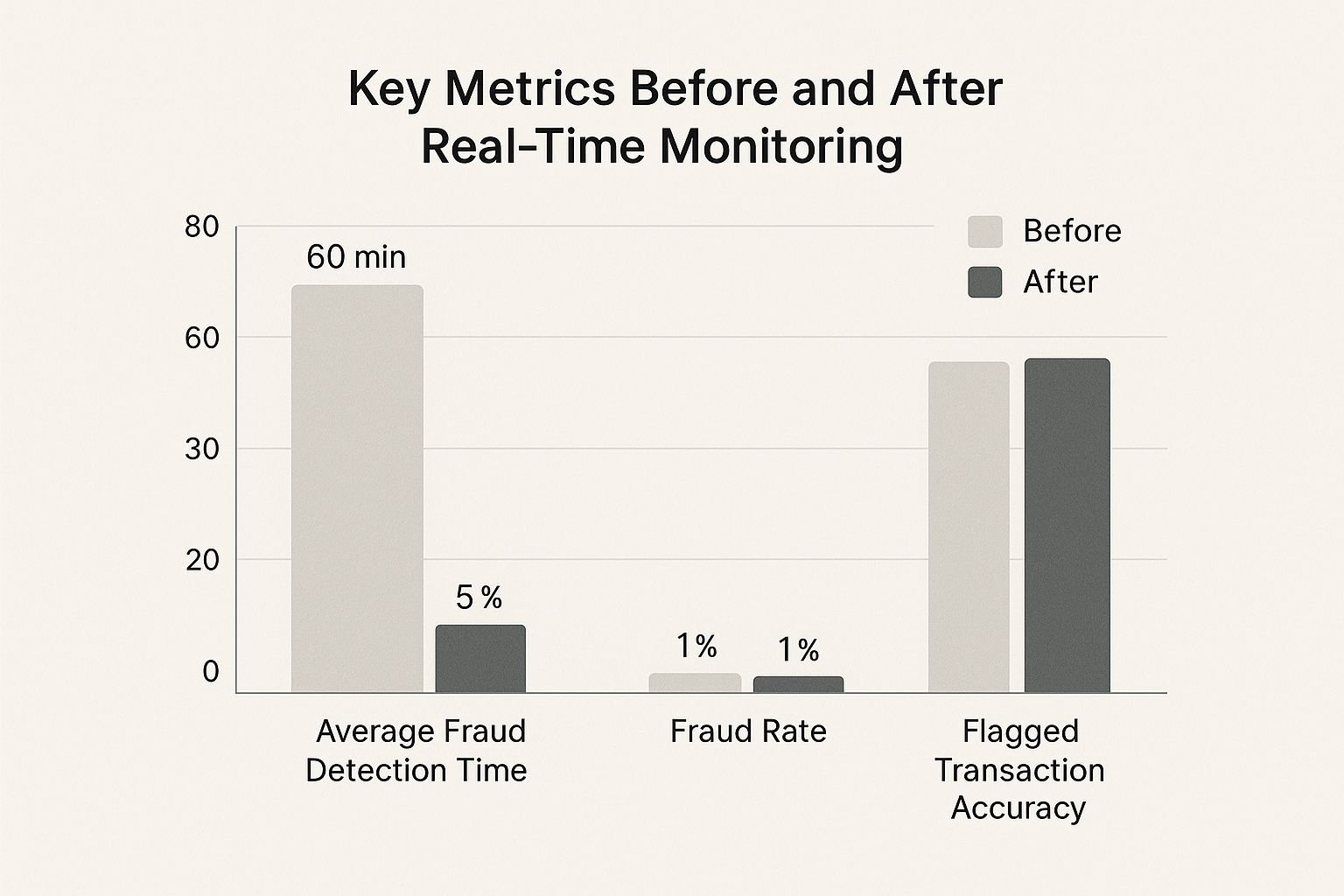

This chart drives the point home, showing how tailored, real-time monitoring can dramatically improve fraud detection.

The data doesn't lie. A smarter, real-time approach slashes detection time from an hour to mere minutes, nearly eliminates fraud, and boosts accuracy through the roof.

Practical Rules for Different Business Models

Let's get into some practical examples of how you can tailor your fraud rules based on what you sell. These aren't just theories; they are actionable steps you can take to build a smarter defense right now.

For Digital Goods (Gift Cards, Software, E-books):

- Check Email Age: A brand-new email address being used to buy five $100 gift cards is a massive red flag. Set a rule to flag or block purchases from email accounts created within the last 30-60 days.

- Implement Device Fingerprinting: This tech helps you see if the same device is being used with multiple credit cards or accounts. It’s a powerful way to spot organized fraud rings.

- Limit Purchase Velocity: Restrict how many high-value items a new customer can buy in a short time. No legitimate customer needs ten software licenses five minutes after creating an account.

For High-Value Physical Products (Luxury Goods, Electronics):

- Require Signature Confirmation: This is non-negotiable. It provides concrete proof of delivery that is invaluable for fighting "item not received" chargebacks.

- Manually Review Large Orders: Set a dollar threshold—say, $500 or $1,000—that automatically sends an order for a human to review. A five-minute check can save you thousands.

- Cross-Reference Billing and Shipping Addresses: While not always fraud, a mismatch on a high-ticket order warrants a closer look, especially if other red flags are present.

For Subscription Services (SaaS, Membership Sites):

- Monitor IP Addresses: Seeing multiple free trials being started from the same IP address? That's a classic sign of trial abuse. You can flag or block these attempts automatically. For repeat offenders, you might need to take stronger action. For more on this, check out our guide on how to blacklist and block fraudulent customers on Shopify.

- Track Payment Method Usage: Be wary if the same credit card is used to sign up for multiple different trial accounts. This could easily be a fraudster testing a list of stolen card numbers.

To give you a clearer picture, let's break down how these risks and solutions line up across different industries.

Industry-Specific Fraud Risks and Solutions

By moving beyond generic settings and creating rules that reflect your specific business, you build a much stronger, more intelligent defense system. It's not about blocking every potential threat; it's about smartly targeting the ones that pose the biggest danger to your bottom line.

How AI and Automation Help You Scale Securely

When your business is small, you can get away with a hands-on, manual approach to checking orders. But that simply doesn’t work once you start to grow. You can’t personally review hundreds or thousands of transactions a day.

This is the exact point where technology becomes your most valuable player in the fight against fraud. It’s not about replacing human oversight entirely, but about giving your team superpowers.

AI and automation are the keys to scaling your ecommerce fraud prevention securely. These systems do what humans can’t: analyze thousands of data points in the blink of an eye. They look at everything from a customer's location and device to their clicking patterns and purchase history, all to answer one simple question: is this transaction legit?

The Power of Real-Time Risk Scoring

The heart of an AI-driven fraud system is its ability to generate a real-time risk score for every single transaction. Think of it like a credit score, but for fraud. The system crunches all the available data and assigns a score that instantly tells you how likely it is that an order is bogus.

A low score means everything looks good, and the order gets approved automatically. A high score, however, triggers an alert. This lets you instantly greenlight the vast majority of good orders—keeping your checkout smooth and customers happy—while flagging the few sketchy ones for a closer look.

This isn't just theory; it's a proven method. Merchants are increasingly relying on digital screening, with some seeing overall declined transaction rates around 20% when they let smart systems do the heavy lifting. The goal isn't just to decline more transactions, but the right ones.

This automated triage is a lifesaver. It frees your team from the tedious work of checking every single order, letting them focus their expertise on the truly suspicious cases that need a human touch.

Identifying Patterns a Human Would Miss

Cybercriminals are incredibly sophisticated. They use bots and advanced techniques to mimic legitimate customer behavior, making them tough to spot with old-school, rule-based systems. AI, on the other hand, is built to identify these subtle, complex patterns.

Here's how these systems outsmart fraudsters:

- Behavioral Biometrics: AI can analyze how a user interacts with your site—things like typing speed, mouse movements, and navigation paths. A bot filling out a form behaves very differently from a human, and AI can spot that instantly.

- Device Fingerprinting: This tech creates a unique ID for a user's device. If the system sees dozens of orders coming from the same device but with different credit cards and shipping addresses, that’s a massive red flag for a fraud ring.

- Velocity Checks: AI is brilliant at monitoring the speed and frequency of transactions. For instance, it can flag a new account that suddenly tries to make ten high-value purchases in five minutes—behavior no real customer would exhibit.

By connecting these dots in real-time, AI spots coordinated attacks that would be completely invisible to the human eye.

Choosing and Integrating the Right Tools

Getting started with AI-powered fraud prevention doesn't have to be a headache. The key is finding a solution that fits your business and plugs smoothly into your existing workflow. You want a tool that not only detects fraud but also helps you manage the aftermath, like disputes and chargebacks.

When a chargeback does happen, for example, AI can be a massive help. Handling these disputes manually is a huge time sink, but automated systems can streamline the entire process. If you want to dive deeper, you can explore our complete guide to automated chargeback and dispute management using AI. It breaks down exactly how this technology can save you time and recover revenue.

Ultimately, integrating AI and automation isn't just about stopping fraud. It's about building a smarter, more resilient business that can accept more good orders, reduce manual work, and protect its bottom line—all while giving your real customers a safer, smoother experience.

Creating a Smart Chargeback Response Plan

No matter how solid your defenses are, chargebacks are an unavoidable part of running an online store. They are going to happen. But how you react can make a massive difference to your bottom line, turning potential losses into recovered revenue.

Winning a chargeback dispute isn’t about just firing off a few documents and hoping for the best. It takes a smart, organized plan. A well-thought-out process for handling disputes from start to finish will not only save you money but also a ton of time and stress.

Understand the Chargeback Reason Codes

The very first step when a dispute lands in your inbox is to look at the chargeback reason code. Every chargeback comes with one, and it's the bank's way of telling you why the customer is disputing the charge. These codes are your roadmap for how to respond.

For example, a code for a "Fraudulent Transaction" requires a completely different set of evidence than one for "Product Not Received." Trying to fight them with the same generic response is a guaranteed way to lose.

- Fraud-Related Codes: These mean the cardholder claims they didn't authorize the purchase. Your goal here is to prove the legitimate cardholder made the purchase.

- Service-Related Codes: These are claims like "Item Not Received" or "Not as Described." For these, you need to prove you delivered the correct product to the right address.

Knowing these codes helps you immediately focus on gathering the specific evidence that will actually win the case.

Gather the Right Evidence Quickly

Once you know why the chargeback was filed, it's time to build your case. The quality and relevance of your evidence are everything. You need to present a clear, compelling story that proves the transaction was legitimate and you fulfilled your end of the deal.

Your evidence file needs to be airtight. Think of it like a detective building a case—every piece of information strengthens your argument and leaves no room for doubt.

Key Takeaway: The goal is to provide so much compelling evidence that the bank has no choice but to rule in your favor. Don't just send a screenshot of the order; build a comprehensive file that tells the full story of the transaction.

Here’s a checklist of what you should start gathering immediately:

- Customer Communications: Pull any emails, live chat transcripts, or social media messages you've had with the customer.

- Order and Shipping Details: This includes the order confirmation, invoice, and, most importantly, proof of delivery with a tracking number and signature confirmation if you have it.

- AVS and CVV Match Results: Show the bank that these security checks passed. This is a strong indicator that the actual cardholder made the purchase.

- IP Address and Geolocation Data: Proving the order was placed from an IP address that matches the customer's billing location is powerful evidence against fraud claims.

This collection of documents is your key to an effective ecommerce fraud prevention strategy after the fact, minimizing the financial sting of disputes.

Write a Persuasive Representment Letter

Your representment letter is your chance to tie all your evidence together into a clear, concise argument. This isn't the place for an emotional rant; it needs to be professional, factual, and easy for the bank's reviewer to digest.

Start by clearly stating the chargeback reason code and explaining why it’s incorrect. Then, walk them through your evidence piece by piece, explaining what each document proves. Using bullet points and bold text to highlight the most critical information is a great way to make your case scannable and impactful.

A well-written letter can be the difference between a win and a loss. It guides the reviewer through your logic and makes it easy for them to see why you're right.

Know When to Fight and When to Fold

Here's a hard truth: not every chargeback is worth fighting. Sometimes, the time and effort it would take to dispute a small-dollar chargeback just aren't worth the potential return. You need a clear internal policy that helps you decide which battles to pick.

Consider the order value versus the time it will take your team to assemble the evidence. For a $10 order with weak evidence, it probably makes more sense to accept the loss and move on. For a $1,000 order where you have solid proof of delivery, you should absolutely fight it.

Creating this cost-benefit analysis saves you from wasting resources on lost causes and allows you to focus your energy on the disputes you can actually win. This strategic approach is just as important as having strong upfront fraud defenses.

Keeping Your Store Protected Long Term

When it comes to ecommerce fraud, there’s no “set it and forget it” solution. Think of it less like installing a security system and more like having a security guard on patrol. It’s an ongoing commitment to learning, adapting, and staying one step ahead of fraudsters who are constantly changing their tactics.

The real trick is finding the right balance. You need robust security, of course, but filters that are too aggressive can create a frustrating checkout experience and turn away perfectly good customers. The goal is to build a smart system that can tell the difference between a legitimate shopper and a potential threat, keeping things smooth for the vast majority of your buyers.

Finding the Sweet Spot Between Security and Sales

So, how do you find that balance? Start by regularly reviewing your flagged transactions. Are your rules catching actual fraud, or are you seeing a high number of false positives? If you’re blocking legitimate sales, it’s time to dial things back.

Tweaking your settings based on real data is a critical part of sustainable chargeback risk management that keeps your business healthy and growing.

The core idea is simple: make it easy for good customers to buy and hard for fraudsters to succeed. This means continuously optimizing your foundational defenses, tailoring your fraud rules, and using technology wisely.

And if your store is hosted in the cloud, don't overlook the importance of implementing essential cloud computing security best practices. By staying proactive and vigilant, you can build a resilient defense that supports safe, sustainable growth for the long haul.

Have Questions? We Have Answers.

Running an ecommerce business means you're bound to have questions about fraud prevention. It’s a complex topic, but we're here to cut through the noise with straightforward answers to the questions we hear most often.

What Should I Do Right After a Fraud Attack?

The second you spot a fraudulent transaction, you need to act fast. Time is absolutely critical.

Your first move? Freeze the transaction immediately. If there's a user account tied to it, lock that down too. This is like stopping the leak before it floods the whole house—it contains the damage and prevents any more fraudulent activity from that source.

Once that's done, it's all about gathering evidence. Pull every piece of data you can find on the order: the IP address, device info, shipping address, and any customer communication. This information is your best friend when it comes to fighting the inevitable chargeback dispute. You'll also want to give your payment processor a heads-up and, if any real customers were impacted, let them know what's going on and how you're securing their accounts.

Will Strong Fraud Prevention Annoy My Good Customers?

This is a big one. It's a question on every merchant's mind, and for good reason. Nobody wants to drive away a legitimate customer by making them jump through a dozen security hoops. Overly aggressive filters often lead to false declines—rejecting a perfectly good order—which is one of the fastest ways to lose a sale and a customer.

The trick is to be smart, not just strict. Modern ecommerce fraud prevention tools don't treat every transaction the same. They work in the background, analyzing hundreds of data points in real time to assign a risk score, all without the shopper even noticing.

This means your loyal, low-risk customers sail through checkout without a hitch. The extra security measures, like two-factor authentication, only pop up for transactions that are genuinely suspicious. It's all about striking that perfect balance between iron-clad security and a seamless customer experience.

Key Insight: The best fraud prevention works silently. It should make it incredibly easy for good customers to buy from you and nearly impossible for fraudsters to get away with anything.

Are There Affordable Options for Small Businesses?

Absolutely. You don’t need an enterprise-level budget to start protecting your store from fraud. In fact, some of the most effective tools are already built into your payment processor and are either free or very cheap to turn on.

You should start with these foundational checks:

- AVS (Address Verification System): This confirms that the billing address entered matches the one the card-issuing bank has on file.

- CVV (Card Verification Value): Requiring this 3- or 4-digit code proves the customer has the physical card in their possession.

- 3D Secure: This adds another layer of authentication, often requiring a password or a one-time code sent to the cardholder's phone.

As you grow, plenty of dedicated fraud prevention apps offer tiered pricing plans made for small businesses. You can get advanced protection that scales with your sales volume, ensuring you only ever pay for what you actually need.

Ready to stop losing revenue to chargebacks? ChargePay uses AI to automate the entire dispute process, recovering up to 80% of your lost funds without you lifting a finger. See how it works at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)