When a chargeback notification hits your inbox, it's easy to feel like you're on the defensive. A customer has gone to their bank, reported an issue, and just like that, the money is yanked from your account. But this isn't the end of the story. You have a chance to fight back, and your single most powerful weapon is the letter of rebuttal.

This letter is your official, fact-based response to the dispute. It’s the heart of the entire chargeback representment process and your one shot at presenting your side with evidence to reclaim that revenue. Getting this document right is a huge deal for protecting your bottom line.

Why Your Letter of Rebuttal Is Your Most Important Tool

Think of your rebuttal letter as the opening argument in your case. It’s the very first thing the bank’s dispute analyst will read, and it sets the stage for all the evidence you’re about to provide. A sharp, well-written letter makes their job simple by clearly and quickly explaining why the chargeback is invalid.

This formal process, known as chargeback representment, is your right as a merchant. Without a compelling letter to lead the charge, your chances of winning are practically zero.

The Stakes Are Getting Higher

Just ignoring disputes and hoping they go away isn't a good strategy anymore. The e-commerce world is seeing chargebacks skyrocket, which makes a strong defense more important than ever.

According to industry projections, global chargeback volumes are expected to leap from 261 million in 2025 to a massive 324 million by 2028. That’s a 24% jump in just three years. Every single one of those chargebacks represents a potential loss for a business like yours. Each one you don't fight—or fight poorly—is money walking right out the door.

A letter of rebuttal isn't just about recovering one sale. It's about protecting your merchant account, pushing back against friendly fraud, and staying in control of your hard-earned revenue.

It's More Than Just a Letter

Don't mistake this for a simple denial. Your rebuttal is a strategic document designed to persuade a neutral third party with facts. It has to accomplish several things at once.

A truly effective letter will:

- Tackle the reason code head-on. Every chargeback comes with a specific code, like "Product Not Received" or "Transaction Not Recognized." Your letter must directly refute that specific claim.

- Be a roadmap for your evidence. It guides the reviewer, telling them what documents you’ve attached (like shipping confirmations, AVS checks, or customer emails) and what each one proves.

- Establish your professionalism. A clean, organized letter shows the bank you're a serious business, which immediately adds credibility to your entire case.

Let's say a customer files a chargeback claiming a purchase was unauthorized. Your rebuttal letter wouldn't just say, "No, it was." It would lead by stating the claim is incorrect and then point the reviewer to the proof: the IP address matching the customer's location, the AVS confirmation, and the delivery receipt showing the package arrived at the cardholder's verified address.

By presenting a clear, evidence-backed narrative, you shift the dynamic. It's no longer just the customer's word against yours—it's a decision based on cold, hard proof. This one document truly can be the difference between losing money and protecting your business.

The Anatomy of a Persuasive Rebuttal Letter

A winning letter of rebuttal isn't just a simple note; it's a structured, logical argument. Think of it less like a letter and more like a persuasive cover sheet for all your evidence. Its job is to make the bank reviewer’s decision as easy as possible by presenting a clear, fact-based story they can quickly understand and verify.

Every single element has a purpose. Without a solid structure, even the most compelling evidence can get lost in the shuffle. Your goal is to connect the dots for the reviewer, leaving no room for doubt about the transaction's legitimacy.

Start With a Clear and Concise Summary

Your very first paragraph needs to get straight to the point. This isn't the place for a long, winding story. Instead, you need to state the essential transaction details and immediately address the chargeback reason code. The person reading this is reviewing dozens, maybe hundreds, of cases a day. Grab their attention by showing you understand the dispute and are ready to counter it.

For instance, if the reason code is "Product Not Received," your opening should sound something like this:

"This letter is in response to chargeback #12345 for the amount of $79.99. The customer has claimed the merchandise was not received; however, our evidence confirms successful delivery to the cardholder's verified address on January 15, 2024."

That one sentence does three critical things: it identifies the dispute, acknowledges the claim, and immediately states your counter-argument. It's direct and powerful.

Tailor Everything to the Reason Code

One of the biggest mistakes I see merchants make is sending a generic, one-size-fits-all response. Your rebuttal must be a direct answer to the specific reason code provided. A response to a "Transaction Not Recognized" claim looks completely different from one for a "Not as Described" dispute.

- For Fraud Claims: Your letter should highlight evidence like AVS/CVV matches, IP address logs, and any previous order history to prove the legitimate cardholder made the purchase.

- For 'Not as Described' Claims: Here, you need to focus on proving the product perfectly matched its description. Your letter should point to evidence like product page screenshots, clear photos, and links to your public policies. Believe it or not, the principles behind writing product descriptions that sell can be a huge help in crafting these arguments.

- For Subscription Disputes: The key is proving the customer agreed to recurring billing. Your letter should reference screenshots of the checkout page where they accepted your terms and include a copy of your cancellation policy.

This tailored approach shows the bank you've done your homework. You're addressing the specific complaint, not just firing off a template and hoping for the best.

To make sure you're hitting all the right notes, here’s a quick-reference table that breaks down the must-have elements for any effective rebuttal letter.

Essential Components of a Rebuttal Letter

Think of this table as your pre-flight checklist before submitting. If you're missing any of these pieces, your argument might not get off the ground.

Maintain a Professional, Fact-First Tone

It’s so easy to get frustrated, especially when you suspect a case of friendly fraud. But letting that emotion seep into your letter will only hurt your case. The bank reviewer is a neutral party looking for cold, hard facts—not feelings. An angry or accusatory tone can make you seem unprofessional and less credible.

Stick to the evidence. Instead of saying, "The customer is lying about not receiving the package," you should say, "Attached is the delivery confirmation from FedEx, which includes a GPS location stamp and signature from the cardholder." Let the proof do all the talking for you.

To ensure you're including all these essential components in a logical flow, it helps to follow a proven structure. For a deeper dive, our guide on the ideal rebuttal letter format provides a detailed framework that makes your argument persuasive and incredibly easy for the reviewer to follow.

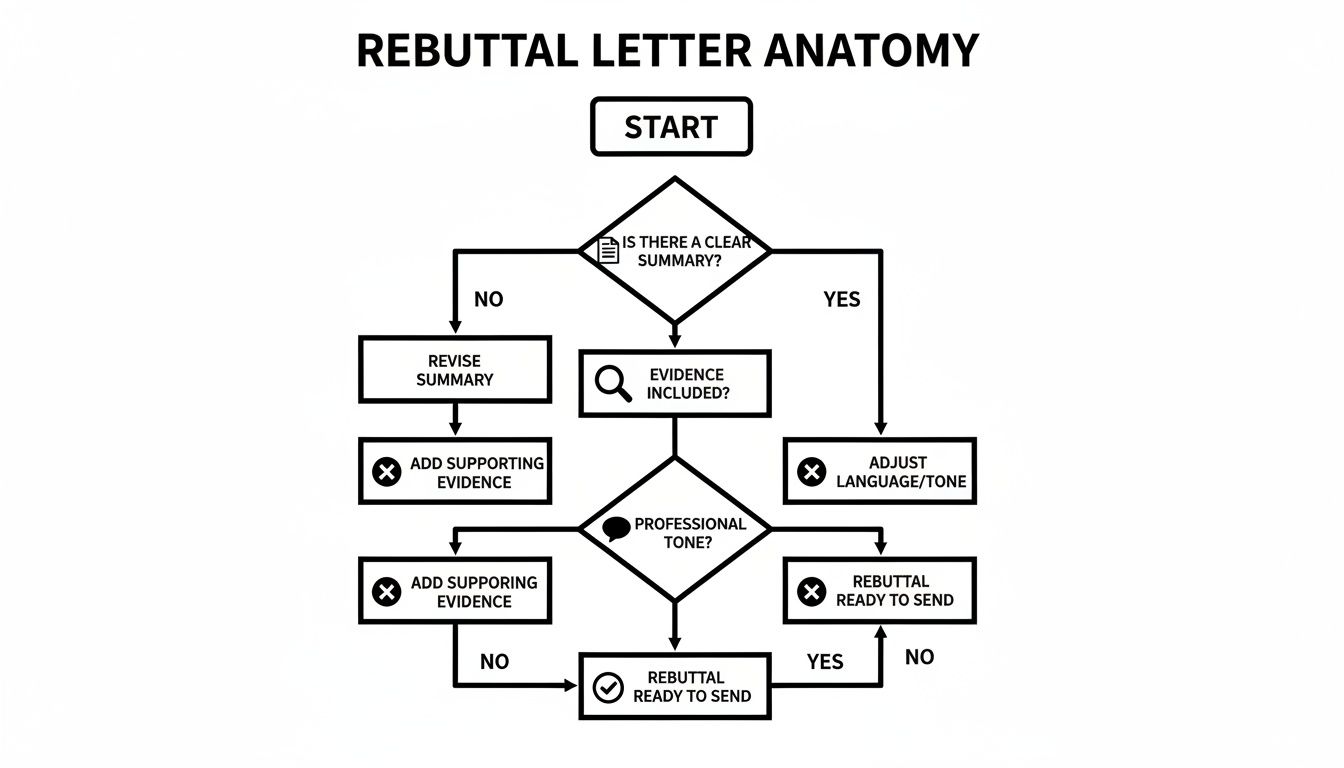

Gathering Evidence That Actually Wins Disputes

Think of your rebuttal letter as the story you're telling the bank, but your evidence? That's the cold, hard proof. Without solid, compelling evidence, your letter is just a bunch of words. Honestly, gathering the right proof is the most critical part of the entire card dispute process. It's the only thing that can definitively prove your side of the story.

The key is to think like a detective. You're not just throwing random documents at the wall and hoping something sticks. You need to pull together specific, relevant proof that directly torpedoes the customer’s claim and leaves zero room for doubt.

This flowchart breaks down the essential flow of a strong rebuttal, showing just how foundational your evidence really is.

As you can see, evidence is the central pillar. It supports everything else. A fact-based approach is always your best bet.

Matching Evidence to the Chargeback Reason

The kind of evidence you need completely depends on the chargeback reason code. What you’d submit for a "friendly fraud" claim looks totally different from what you'd need for a dispute over a subscription cancellation.

Let’s break down the must-have evidence for the most common scenarios you'll run into.

For 'Product Not Received' Claims

Your goal here is simple: prove the item made it to the customer's doorstep.

- Shipping Confirmation: This is your primary weapon. It absolutely must show the delivery address matches the one the customer gave you.

- Signature Confirmation: If you have it, this is golden. A signature from someone at that address is incredibly difficult for a cardholder to argue against.

- GPS or Photo Confirmation: Many carriers now provide GPS data or a photo of the package right at the delivery location. This is powerful, modern proof.

- Customer Communication: Don't forget to include any emails or chat logs. If the customer acknowledged the order or asked about shipping, it proves they were fully aware of the transaction.

For 'Transaction Not Recognized' or Friendly Fraud Claims

Here, you have to prove the legitimate cardholder authorized the purchase.

- AVS and CVV Results: Show the bank that the Address Verification System (AVS) and Card Verification Value (CVV) checks passed.

- IP Address Logs: Provide the IP address used for the purchase and, if possible, show that it matches the customer’s billing location.

- Customer Order History: Has this person ordered from you before? If they've used the same card and shipped to the same address previously, that’s a huge red flag for friendly fraud.

- Login or Account Activity: This is crucial for digital goods. Show that the customer logged into their account to download the file, stream the video, or use the service they bought.

Pro Tip: When you put your evidence together, organize it logically. Start with your knockout punch—like a signature confirmation—and then add the supporting documents. Use clear labels like "Attachment A: Delivery Confirmation" to make the reviewer's job as easy as possible. They’ll thank you for it.

Evidence for Digital and Subscription-Based Businesses

Disputes for non-physical goods can feel a bit trickier, but they are just as winnable with the right proof. It all comes down to documenting the customer's actions and agreements.

For Subscription Cancellation Disputes

These disputes often hinge on two things: Did the customer know they were signing up for a recurring charge, and did they follow your cancellation policy?

- Proof of Agreement: A screenshot of the checkout page is essential. It needs to show where the customer ticked a box agreeing to your terms of service and recurring billing policy.

- Your Cancellation Policy: Provide a clear, timestamped copy of your policy and show that the customer had access to it before or during their purchase.

- Service Usage Logs: This is a big one. Can you show that the customer logged in and used the service after the billing date in question? This proves they were aware of and benefiting from the subscription.

- Communication Records: Any welcome emails, billing reminders, or cancellation confirmation emails are crucial pieces of the puzzle.

Manually gathering and bundling all this information is a massive time-sink. It's also where many businesses slip up, leading to lost disputes. Research from Juniper highlights how AI-driven systems are changing the game. While manual rebuttals typically win only 20-30% of the time, automated systems that compile perfect evidence bundles can boost win rates to 65% or even higher.

This is where a solution like ChargePay can make a huge difference. It automates this entire process, generating winning responses and operating on a pay-per-success model, which means there's no upfront risk for you.

Rebuttal Letter Templates You Can Use Today

Knowing the theory behind a good letter of rebuttal is one thing. Having a battle-tested template ready to go when a dispute notice lands in your inbox is a whole lot better.

Generic examples often miss the mark because every chargeback tells a different story. The real key is knowing how to adapt your response to the specific situation you're facing.

To get you started, we’ve put together a few fill-in-the-blank templates for the most common—and frustrating—scenarios we see merchants deal with every single day. These aren't just scripts; they're structured to be clear, persuasive, and easy for a busy bank reviewer to understand. We’ll even kick each one off with a quick, relatable story to show you exactly when and how to deploy it.

Template for Friendly Fraud Claims

Picture this: a customer buys a high-end coffee machine from your store. They get it, sign for it, and you even have an email from them a week later asking for brewing tips. A month later, bam—a chargeback hits with the reason code "Transaction Not Recognized."

This is a textbook case of friendly fraud. Your rebuttal letter needs to be sharp, factual, and leave no room for doubt.

Here’s how to structure your response:

Subject: Rebuttal for Chargeback Case #[Chargeback Case Number]

Dear Dispute Analyst,

This letter is in response to the chargeback for $[Amount] on transaction #[Transaction ID], dated [Date of Transaction]. The cardholder’s claim is that they did not recognize the transaction. Our records and compelling evidence show this purchase was fully authorized by and delivered to the cardholder.

We have attached the following evidence to validate this transaction:

- Attachment A: Transaction Details & AVS/CVV Confirmation. The AVS matched the billing address on file, and the CVV code was entered correctly.

- Attachment B: IP Address Log. The purchase was made from an IP address ([IP Address]) located in [City, State], which matches the cardholder’s billing information.

- Attachment C: Signed Delivery Confirmation. The order was delivered on [Date of Delivery] and signed for at the cardholder's verified address.

- Attachment D: Customer Communication. An email from the cardholder ([Customer's Email]) on [Date of Email] confirms receipt and use of the product.

This evidence confirms the legitimate cardholder made and received this purchase. We respectfully request that this chargeback be reversed.

Sincerely,

[Your Name][Your Company Name]

Template for 'Product Not Received' Disputes

Here's another one we see all the time. You ship an order for a set of custom-printed t-shirts. The tracking information clearly shows it was delivered to the customer’s apartment complex mailroom two weeks ago. Then, out of nowhere, you get a "Product Not Received" chargeback.

Your job is to prove delivery with undeniable facts.

Use this template to build your case:

Subject: Rebuttal for Chargeback Case #[Chargeback Case Number]

Dear Dispute Analyst,

We are writing to dispute the chargeback for $[Amount] for transaction #[Transaction ID]. The customer claims the merchandise was not received (Reason Code 13.1). However, our shipping documentation confirms a successful delivery to the cardholder's address.

The attached evidence proves this claim is invalid:

- Attachment A: Order Invoice. This shows the purchased items and the shipping address provided by the customer: [Customer's Full Shipping Address].

- Attachment B: Shipping Confirmation from [Carrier Name]. The tracking number is [Tracking Number].

- Attachment C: Proof of Delivery. This document from [Carrier Name] confirms the package was delivered on [Date of Delivery] at [Time of Delivery] to the address listed above. It includes GPS location data confirming the correct delivery location.

The evidence clearly demonstrates that we fulfilled our obligation and the product was successfully delivered. We request that the chargeback be reversed. For more detailed guides and additional rebuttal letter examples, check out our comprehensive article on the topic.

Thank you,

[Your Name][Your Company Name]

Remember, the person reviewing your case is human. Making their job easier with a clear, well-organized letter and labeled attachments significantly increases your chances of winning. Don't make them hunt for the information they need.

Template for Subscription Cancellation Issues

Subscription models are great—until a customer disputes a recurring charge they forgot about or didn't cancel correctly.

Let's say a customer signed up for your monthly subscription box. They loved it for three months, then filed a chargeback for the fourth payment, claiming they canceled. But when you check your records, there’s no cancellation request to be found.

This template helps you point back to the terms they agreed to from the start:

Subject: Rebuttal for Chargeback Case #[Chargeback Case Number]

Dear Dispute Analyst,

This letter addresses the chargeback for $[Amount] on transaction #[Transaction ID], related to our recurring subscription service. The customer claims the charge was unauthorized, but our records show this was a valid recurring charge based on terms the customer accepted at signup.

Please review the following supporting evidence:

- Attachment A: Initial Order and Terms of Service Agreement. This is a screenshot from [Date of Initial Order] showing the customer checked a box to agree to our recurring billing policy and terms of service.

- Attachment B: Our Cancellation Policy. A copy of our clear and accessible cancellation policy, which requires customers to cancel via their account dashboard or by contacting support.

- Attachment C: Customer Account Logs. These logs show the customer accessed and used our service on [Dates of Use] after the billing date in question.

- Attachment D: Communication Records. We have no record of a cancellation request from the customer's registered email ([Customer's Email]) prior to this dispute.

The customer agreed to the recurring charges and did not follow the agreed-upon procedure to cancel their subscription. Therefore, this charge is valid. We kindly ask for this chargeback to be reversed.

Sincerely,

[Your Name][Your Company Name]

Common Mistakes That Will Cost You Money

Winning a chargeback is often less about having a silver bullet and more about not shooting yourself in the foot. I’ve seen countless merchants lose disputes they absolutely should have won, simply because they fell into a few common, costly traps. A strong letter of rebuttal can be completely torpedoed by one simple mistake.

These errors aren't complex, but they can instantly sink your case before a bank reviewer even gets to your evidence. Knowing what these pitfalls are is the first step to sidestepping them and keeping your revenue where it belongs.

Letting Your Emotions Take the Wheel

It's completely normal to feel angry when you get a chargeback you know is bogus. This is especially true with blatant friendly fraud. The urge to write an emotional, accusatory letter is strong, but you have to fight it.

Remember, the person reading your rebuttal is a neutral analyst looking for cold, hard facts—not your feelings. An unprofessional tone immediately makes you seem less credible and can bias the reviewer against you from the start.

Instead of this:

- "This customer is clearly a liar and is trying to steal from us!"

Try this:

- "The evidence confirms the cardholder authorized and received this purchase."

Let your proof do the talking for you. A calm, professional, and fact-based approach is always going to be more persuasive.

Missing the Incredibly Strict Deadlines

Every single chargeback comes with a ticking clock. Your payment processor will give you a firm deadline to submit your rebuttal and all your evidence, and that date is non-negotiable. It doesn't matter if you have a mountain of perfect proof—if you submit it one day late, you lose. Period.

I once saw a merchant lose a $500 dispute they had slam-dunk evidence for. They were just a few hours late submitting their rebuttal. The bank didn't care; the case was closed, and the money was gone for good.

Set up alerts, check your dashboard daily, and treat these deadlines like your revenue depends on them—because it does. Procrastination is one of the most expensive mistakes you can possibly make in the chargeback world.

The 'More Is Better' Evidence Trap

When you know you’re in the right, it’s tempting to bury the bank in every piece of data you can find. You might think a ten-page rebuttal with 20 attachments shows how thorough you are, but it usually just creates confusion.

Bank reviewers are strapped for time. A messy, disorganized pile of irrelevant information is more likely to get your case denied than carefully reviewed.

Your rebuttal should be a concise, one-page summary that guides the reviewer directly to your most compelling proof. Focus on quality over quantity. A single, clear delivery confirmation with a signature is worth more than ten pages of your internal notes.

The need for a sharp, effective rebuttal is only growing. The number of chargebacks is projected to jump from 238 million in 2023 to 337 million by 2026—a 41% rise. As global merchant losses climb towards $41.69 billion by 2028, your ability to avoid these simple mistakes becomes a critical survival skill.

Got Questions About Rebuttal Letters? We Have Answers.

When you're staring down a chargeback, even with the best templates in hand, questions are bound to pop up. The whole process can feel like navigating a maze, and it's easy to get tangled up in the details.

To cut through the confusion, we've rounded up some of the most common—and critical—questions merchants ask about rebuttal letters and the representment process. Here are the straightforward answers you need.

How Long Do I Have to Submit My Rebuttal?

This is where it gets a little tricky. Officially, the card networks like Visa or Mastercard might give you anywhere from 7 to 45 days. But that's not the deadline you really need to worry about.

The date that truly matters is the one set by your payment processor, whether that’s Stripe, PayPal, or another gateway. They’ll give you their own, much shorter window to get your evidence in. It is absolutely critical to check this deadline in your merchant portal the second a dispute notice hits. Miss it, even by an hour, and you automatically lose, no matter how solid your case is.

Should I Bother Fighting a Chargeback I Know Is My Fault?

In a word: no. If you know a chargeback is legit—maybe you shipped the wrong size, a product was defective, or a cancellation request genuinely slipped through the cracks—just accept it and move on.

Trying to fight a losing battle is a waste of your time. More importantly, it can hurt your reputation with your payment processor. A high chargeback ratio, which includes disputes you lose, can trigger higher fees, frozen funds, or even account termination. The smart play is to focus your energy on the illegitimate disputes you can actually win.

What's the Real Difference Between a Chargeback and a Refund?

This is a crucial distinction every merchant needs to understand. A refund is a conversation between you and your customer. They reach out, you agree to return their money, and you part on good terms. It's cooperative.

A chargeback, however, is a forced reversal of funds kicked off by the customer's bank. The customer goes completely around you and straight to their financial institution. This makes the whole process adversarial from the very start.

Sure, the customer gets their money back either way, but a chargeback is far more damaging for you. It comes with non-refundable dispute fees (even if you win the case!) and dings your merchant account health.

Is It Really Worth Fighting Those Small, Low-Value Chargebacks?

Absolutely, and here's why. It’s incredibly tempting to look at a $15 or $20 chargeback and just write it off. It feels like it’s not worth the hassle, right? Wrong. Ignoring these small disputes is a dangerous habit.

For one, it basically hangs a sign on your door that tells fraudsters you're an easy target, which can invite even more fraudulent orders.

Even more importantly, your chargeback ratio is almost always calculated based on the number of disputes you get, not their dollar value. A flood of tiny, uncontested chargebacks can inflate your ratio just as fast as a few big ones, putting your entire merchant account in jeopardy. Fighting every illegitimate dispute, no matter the size, is essential for the long-term health of your business.

Feeling buried under the constant threat of chargebacks? ChargePay uses advanced AI to handle the entire rebuttal process for you—from gathering the right evidence to writing the perfect response. You can recover lost revenue without lifting a finger. See how much you can get back by visiting ChargePay's website today.

.svg)

.svg)

.svg)

.svg)