Alternative forms of payment are, simply put, any way a customer can check out that isn't a traditional credit card from a major player like Visa or Mastercard. Today's shoppers fully expect to pay with digital wallets, direct bank transfers, or even installment plans, making these options absolutely essential for any online store.

Why Alternative Payments Are No Longer Optional

The whole checkout game has changed. Not too long ago, just accepting major credit cards was good enough. Now, relying only on cards is like having a single, narrow entrance to a bustling shop—you're going to miss out on a ton of business.

Think of it this way: every payment method you offer is another open door. When a shopper sees their favorite, most trusted way to pay, the friction to hit that "buy" button just melts away. This isn't just a minor perk; it's a powerful way to build trust and, frankly, make more sales.

Meeting Modern Customer Expectations

Today’s shoppers are all about choice and security. They want to use the methods they’re most comfortable with, whether that's the one-tap simplicity of Apple Pay or the structured payments of a Buy Now, Pay Later service. If you don't offer those choices, you’re practically inviting them to abandon their cart.

The global shift to digital wallets has been nothing short of explosive. By 2030, experts project they'll handle a staggering 65% of all eCommerce payments worldwide. While this opens up huge opportunities for merchants, it also brings new headaches, like managing a higher volume of disputes from wallet transactions.

The big idea is simple: meet your customers where they are. Giving them familiar and convenient ways to pay shows you get their needs, which is a massive step in turning a one-time buyer into a loyal fan.

Unlocking Growth and Reducing Friction

Offering a variety of alternative forms of payment has a direct impact on your bottom line. It's not just about catering to preferences; it's a smart, strategic move.

Here's why:

- Improve Conversion Rates: More options mean fewer reasons for a shopper to bail on your site.

- Unlock New Customer Segments: Certain payment methods are wildly popular with specific demographics and in different parts of the world.

- Build Lasting Trust: Just displaying familiar logos like PayPal or Klarna can instantly boost a customer's confidence in your brand.

By expanding your payment options, you’re not just tacking on features—you’re building a more inclusive and effective sales funnel. To see how different processors stack up, check out our guide on Shopify Payments vs Stripe and learn how they handle these options.

Getting to Know Your Payment Options

To really get a handle on alternative payments, let's break down the most popular choices for your business. We'll go beyond the basic definitions and look at how each one actually works, both for your customer and for you on the other side of the counter. Think of this as your menu of modern payment methods, each with its own unique flavor.

The goal isn't just to list them out. When you truly understand their mechanics, it becomes much easier to see which ones make sense for your store and your shoppers.

Digital Wallets: The One-Tap Checkout

Digital wallets are pretty much what they sound like: secure, virtual versions of a physical wallet. Services like Apple Pay, Google Pay, and PayPal store a customer's payment info—credit card numbers, bank details—so they don't have to punch it in every single time they buy something.

For the customer, the appeal is obvious. It’s fast, simple, and secure. A single tap or click is all it takes. For you, that speed is gold. It drastically cuts down on checkout friction, which can directly boost your conversion rates.

Account-to-Account (A2A): Direct Bank Transfers

Account-to-Account (A2A) payments, or direct bank transfers, are another great option. They let customers pay you straight from their bank account, completely sidestepping the traditional card networks. For merchants, this often translates to lower processing fees.

This payment method is picking up serious steam, especially in international markets. In fact, alternative payment methods, with A2A leading the charge, are expected to make up a massive 58% of all ecommerce transactions by 2028. This boom is fueled by real-time systems like India's UPI and Brazil's Pix. You can see more insights from Visa about this shift away from cards.

Think of A2A as the digital version of a wire transfer, but way faster and built for a modern checkout. It’s a secure, cost-effective way to get paid directly.

The technology behind these systems is fascinating, and a deep dive into fintech software development can show you the tools powering modern finance. If you're curious about how these transactions get managed behind the scenes, you can learn more about what a payment processor does in our detailed guide.

Buy Now, Pay Later (BNPL): The Modern Layaway

You’ve probably seen them everywhere. Buy Now, Pay Later (BNPL) services from companies like Klarna, Afterpay, and Affirm have exploded in popularity, especially with younger shoppers. These services let customers grab an item right away and pay for it over time in a series of interest-free installments.

It’s like an automated, instant version of the old-school layaway plan, but with one huge difference: the customer gets their product immediately. You, the merchant, get paid the full amount upfront by the BNPL provider (minus their fee, of course). They’re the ones who take on the risk of collecting the payments. Offering BNPL can give your average order value a serious lift by making bigger purchases feel much more affordable for your customers.

Choosing the Right Payment Mix for Your Store

With so many alternative forms of payment out there, picking the right ones can feel overwhelming. The secret isn’t to offer every single option under the sun. Instead, you want to build a smart, strategic mix that actually makes sense for your customers and your business.

Think of it like stocking the shelves in a physical shop. You wouldn't just throw random products everywhere; you’d curate items you know your shoppers are looking for. The same logic applies to your checkout page. Every payment method you add should have a clear purpose—whether it's cutting your costs, getting cash in the bank faster, or just making it dead simple for people to buy from you.

To get this right, you really need to look at three things from a merchant's point of view: the costs, the risks, and how quickly you get your money. These are the factors that directly hit your bottom line and shape your daily operations.

Balancing Cost and Convenience

Every payment method comes with its own fee structure, and those little differences can add up in a big way. Traditional credit cards usually hit you with a percentage-based fee plus a flat rate for each transaction. On the other hand, direct bank transfers (A2A payments) can be significantly cheaper because they bypass the expensive card networks entirely.

But while lower fees are always tempting, you have to weigh them against what your customers want. Digital wallets might have fees similar to credit cards, but their one-click convenience can give you a serious lift in conversions. The trick is to strike a balance where your processing costs don’t eat up your margins, but you’re not losing sales just to save a few pennies per transaction.

Don't get tunnel vision on the lowest transaction fee. A slightly more expensive payment method that slashes your cart abandonment rate by 20% is a much better deal for your business.

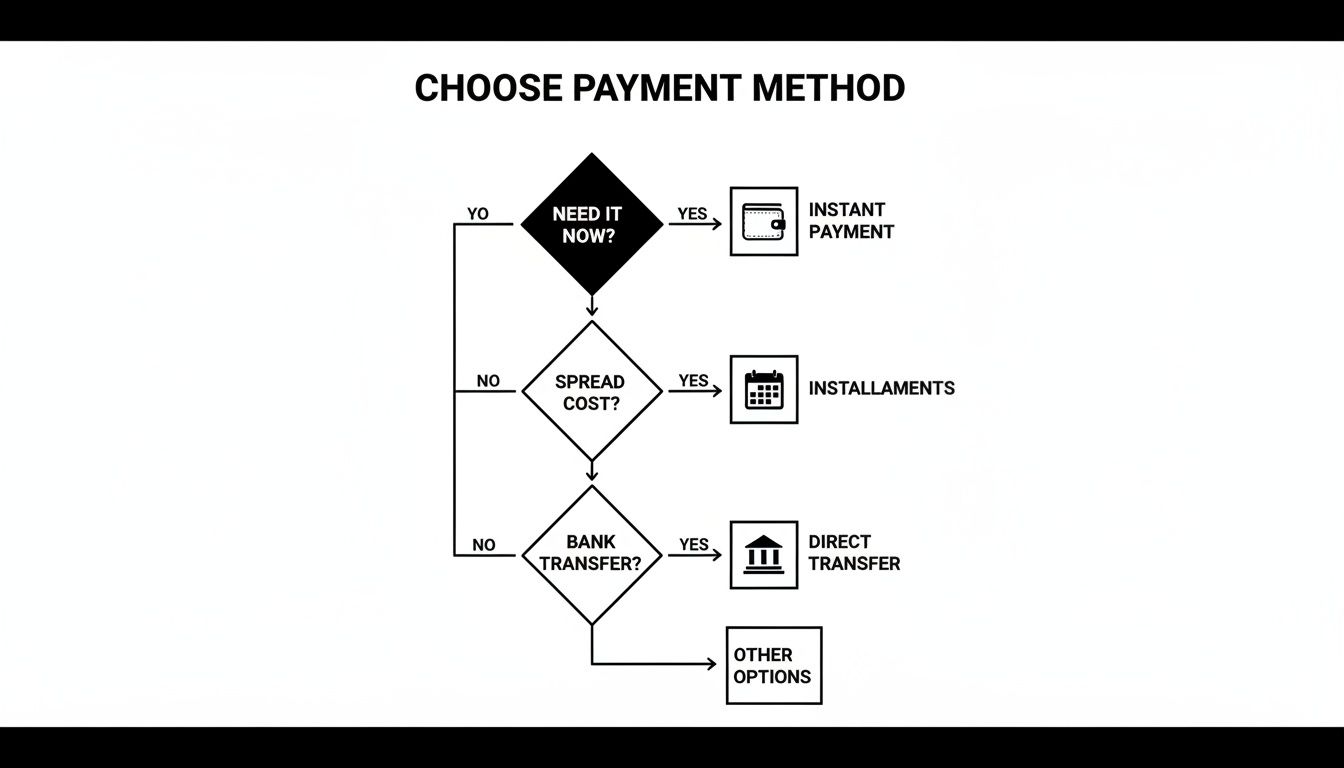

This decision tree gives you a simple way to visualize how different payment methods line up with what your customers might need in the moment, like paying instantly versus paying in installments.

As the flowchart shows, the best choice often starts with what the customer values most, which helps you decide which options to put front and center.

Understanding Risk and Settlement Speed

Chargeback risk is another huge piece of the puzzle. Some payment methods, like direct bank transfers, are "push" payments—meaning the customer has to authorize the transaction directly from their bank. This makes chargebacks nearly impossible, giving you incredible peace of mind.

On the flip side, some digital wallets and BNPL services can carry a higher risk of friendly fraud. While they're fantastic for driving sales, you need to be ready to handle potential disputes. You can learn more about how different systems help manage these complexities in our guide to payment orchestration platforms.

Finally, you have to consider settlement speed—how fast the money from a sale actually lands in your bank account.

- Bank Transfers: These are reliable but can take a few business days to clear.

- Digital Wallets: Often settle as quickly as the card behind them, usually within 1-3 days.

- BNPL Providers: Typically pay you the full amount upfront (minus their fees) within a few days. They take on the work of collecting the installments from the customer.

To help you see how these different factors stack up, here’s a quick comparison of the most common alternative payment methods.

Comparing Alternative Payment Methods for Merchants

Ultimately, choosing the right payment mix is about creating a win-win. You want to give your customers the secure, convenient options they expect while protecting your revenue and keeping your cash flow strong and healthy. It's an ongoing process of testing and tweaking to find what works best for your specific store and audience.

How to Integrate New Payments on Shopify and Stripe

Adding new payment options to your checkout used to be a major technical headache. Thankfully, those days are long gone. Platforms like Shopify and Stripe have made it surprisingly simple—often, it’s just a matter of finding the right settings page and flipping a switch.

The key is knowing where to look. Both platforms centralize payment management, letting you activate everything from digital wallets to local bank transfers from a single dashboard. This means you can go from deciding to offer a new payment method to actually accepting it in just a few minutes, not days.

As you can see, the settings are designed to be user-friendly, grouping different payment types into clear categories. This layout helps you quickly find and enable the options most relevant to your business without getting bogged down in technical jargon.

Activating Payments on Shopify

Shopify is built on simplicity, and adding new payment methods is no exception. Most of the popular alternative forms of payment are already baked right into Shopify Payments, so you can turn them on with a few clicks.

Here’s a quick walkthrough to get you started:

- Navigate to Settings: From your Shopify admin dashboard, look to the bottom-left corner and click on "Settings."

- Select Payments: In the settings menu, choose the "Payments" option. Think of this as your command center for everything related to getting paid.

- Manage Shopify Payments: Click the "Manage" button inside the Shopify Payments section. Here, you'll see a list of available options, including Shop Pay, Apple Pay, and Google Pay. Just check the boxes for the ones you want to offer.

- Add Other Methods: To add options like Klarna or other BNPL services, scroll down to the "Supported payment methods" section and click "Add payment methods." From there, you can search for and activate the specific service you want.

If you're looking to dig deeper into your options, you can learn more about the different Shopify payment processors and how they stack up.

Enabling New Options in Stripe

Stripe also makes it incredibly easy to expand your payment offerings. Its dashboard is designed to let you activate new methods globally with minimal fuss, automatically showing customers the most relevant options based on their location and device.

To add new methods in Stripe, just follow these steps:

- Go to Payment Methods Settings: Log in to your Stripe Dashboard and head over to Settings → Payment Methods.

- Turn On New Methods: You'll see a whole list of available payment methods like Klarna, Afterpay, and various bank transfer options. Simply click the "Turn on" button next to each one you want to activate. Stripe takes care of the rest.

A crucial pro tip for any platform: always run a quick test transaction after activating a new payment method. It’s a simple step that ensures everything is working correctly before your customers start using it, saving you from lost sales and headaches down the road.

Managing the Risk of Chargebacks and Disputes

While offering more ways to pay is a fantastic way to boost sales, it also opens the door to new kinds of disputes and chargebacks. Each of the alternative forms of payment has its own rulebook and unique fraud profile, which means your old strategy for handling credit card disputes might not cut it anymore.

It's a simple trade-off: more convenience for your customers can sometimes mean more complexity for you. For instance, a customer can dispute some digital wallet transactions just like a credit card purchase. But a direct bank transfer? That’s nearly impossible for them to reverse. Getting a handle on these differences is the first real step in protecting your revenue.

The Rise of Friendly Fraud

One of the biggest headaches for any online merchant is friendly fraud. This is when a legitimate customer makes a purchase but then files a chargeback, claiming they never authorized it or that the product never showed up. They're not necessarily malicious—they might have simply forgotten the purchase, not recognized your business name on their statement, or just had a case of buyer’s remorse.

With the simplicity of one-click payments and BNPL services, this problem is becoming more common. To really get a grip on the financial hit, it's crucial to understand what is chargeback fraud and how to stop it before it starts. Little things, like using clear billing descriptors and sending immediate order confirmations, can go a long way in stopping these misunderstandings from becoming expensive disputes.

Navigating Different Dispute Rules

Every payment method has its own playbook for disputes, and if you want to win, you have to know the rules. Fighting a chargeback from a BNPL provider is a completely different game with different evidence requirements than one coming through PayPal.

Here are a few key differences to watch for:

- Evidence Requirements: Some payment methods will ask for different proof of delivery or customer communication than what the traditional card networks require.

- Response Timelines: The window you have to respond to a dispute can be much shorter or longer, depending on the provider. If you miss that deadline, it's usually an automatic loss.

- Customer Communication: Certain platforms actually encourage you to talk directly with the buyer to sort things out before it ever becomes a formal dispute.

The real challenge isn't just fighting disputes—it's managing them all efficiently across a dozen different platforms. As your business grows, trying to juggle all those different rules and deadlines by hand becomes next to impossible.

Automating Your Defense for Better Results

This is where automated chargeback management becomes a total game-changer. Instead of hiring a team just to manually track down and fight every single claim, AI-powered tools can handle the whole process for you. These systems plug directly into your payment platforms, analyze each dispute the moment it arrives, and automatically pull together and submit the strongest evidence to fight back.

Automating your defense does way more than just save you time. It significantly boosts your win rate, recovering revenue you would have otherwise written off as lost. By using technology to handle the nitty-gritty of disputes across all your alternative forms of payment, you can get back to focusing on growing your business with confidence. For more ideas, check out our guide on chargeback prevention for practical tips you can use today.

Common Questions About Alternative Payments

Jumping into new payment methods is a big step, and it's totally normal to have questions. You want to make sure you're doing right by your customers and your business.

Let's cut through the noise and tackle some of the most common questions merchants ask about bringing alternative payments into their checkout. Think of this as your quick-start guide to making the right call with confidence.

Which Alternative Payment Method Is Best for My Store?

This is the big one, and the honest answer is: it really depends on who you're selling to. There’s no magic bullet here. The trick is to match the payment method to your customers.

- Selling to a younger crowd? Buy Now, Pay Later (BNPL) options like Klarna or Afterpay are huge with this demographic. They can give your average order value a serious lift.

- Have a global audience? You absolutely need to offer local digital wallets and direct bank transfers (often called A2A). Shoppers are way more likely to trust and finish a purchase when they see a familiar name at checkout.

- Dealing in high-value items? ACH or direct bank transfers are fantastic. They usually come with lower fees and have virtually zero chargeback risk, which is a huge plus for big-ticket sales.

The best place to start is your own data. Where do your shoppers live? What's their general age range? A little digging here will point you straight to the options that will make the biggest difference.

Are Alternative Payment Methods Secure for My Customers?

Yes, absolutely. In fact, in many ways, they’re even more secure than a standard credit card swipe. The major players in this space built their entire platforms on a foundation of trust and security.

Take digital wallets, for instance. They use a cool process called tokenization. This means your customer's real card number is never actually shared with you. Instead, a unique, one-time-use token handles the transaction, which dramatically cuts down the risk of data theft. Bank transfers and BNPL services add their own layers, like multi-factor authentication, to confirm a user's identity before any money moves.

Will Adding More Payment Options Really Increase My Sales?

All signs point to a resounding yes. More payment choices directly attack one of the biggest conversion killers out there: checkout friction.

When a potential customer gets to your payment page and doesn't see their go-to method, it creates a moment of doubt.

That hesitation is deadly for sales. By offering familiar, trusted options, you erase that doubt and make buying from you feel easy and natural. The data backs this up—studies consistently show that adding relevant payment methods can boost conversion rates, sometimes by 20% or more.

It's one of the simplest ways to turn more browsers into buyers without having to pour more money into your ad budget.

How Does Automated Recovery Help with These Disputes?

Even with the best security, disputes are a fact of life in e-commerce. The good news is that automated chargeback solutions are built to handle them, no matter the payment source.

These systems connect directly to gateways like Stripe and PayPal that process both traditional cards and alternative payments. When a dispute comes in, the technology doesn't care if it was from a Visa card or a digital wallet.

An AI-powered platform gets to work instantly, analyzing the transaction and pulling together the best evidence to fight the dispute. It automates the whole representment process—from gathering proof to submitting the response—saving you a ton of manual work and winning back revenue you might have otherwise written off.

Don't let the fear of disputes stop you from giving your customers the payment options they expect. ChargePay uses AI to automate your entire chargeback management process, defending your revenue across all payment methods without you lifting a finger. See how much you can recover at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)