So, what exactly is an ACH return charge? Think of it as the modern-day fee for a bounced check. It's the penalty a business pays when a customer's electronic payment fails to go through.

These fees, which can run anywhere from $2 to over $15 per return, are charged by banks or payment processors. They're meant to cover the administrative headache and cost of handling the failed transaction.

What Are ACH Return Charges Anyway?

Let’s say you run a subscription service. You go to pull a customer's monthly payment via an ACH debit, but their bank kicks it back, unpaid. That "return" instantly triggers a fee that gets passed straight to you, the merchant.

These charges are far more than just a small nuisance; they're a red flag in your payment process. Every single fee is a signal that something went wrong, and if you ignore those signals, you'll see a real loss in revenue over time. They have a sneaky way of eating into your profits, one failed transaction at a time.

Why Do These Payment Failures Happen?

Getting to the "why" is the first real step toward stopping these fees in their tracks. A payment can fail for all sorts of reasons, from a simple typo to more serious account problems. It’s usually not just one thing, but the causes often fall into a few familiar buckets.

Here are some of the most common reasons you'll see an ACH return:

- Insufficient Funds: This is the big one. The customer just didn't have enough cash in their account to cover the payment. This will come back with Return Code: R01.

- Incorrect Account Information: A simple typo in the account or routing number is enough to get the whole transaction rejected. You'll see codes like R03 or R04 for this.

- Account Closed or Frozen: Sometimes the customer has closed the account, or their bank has put a freeze on it, making it impossible to pull any funds.

- Authorization Issues: The customer might cancel their payment authorization or, in some cases, claim they never approved the debit in the first place (Return Code: R07).

While ACH returns are typically technical failures, some can feel a lot like chargebacks, especially when a customer disputes the transaction. To get a better handle on the key differences, it helps to understand what a return item chargeback is and how it affects your business.

Each one of these scenarios ends the same way: a returned payment and a fee tacked on for your trouble. The good news is that once you start spotting patterns in why your payments are failing, you can build a solid strategy to cut them down.

Decoding the Most Common ACH Return Codes

When an ACH payment bounces, it doesn't just vanish. The bank sends it back with a specific three-character message called an ACH return code. Think of these codes as tiny diagnostic reports, telling you exactly why the transaction failed.

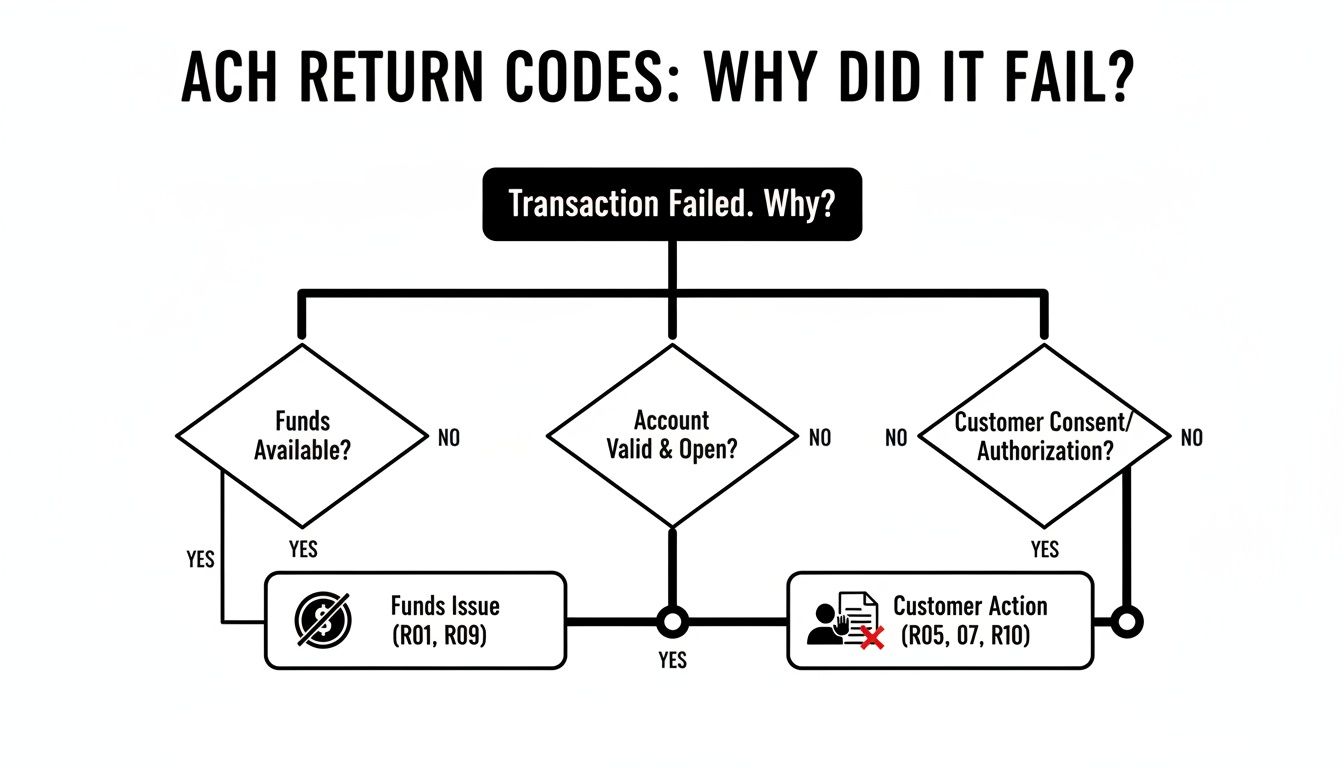

You don't need to memorize a dictionary of codes. In reality, most returns fall into one of three common-sense buckets: issues with the customer's funds, problems with their account information, or an action the customer took themselves.

Grouping them this way helps you stop guessing what went wrong. It gives you a clear path to understanding the root cause so you can figure out your next move.

Insufficient or Unavailable Funds

This is, hands down, the most common reason for a failed ACH payment. Your payment request hit the customer's account, but there just wasn't enough cash to cover it. It’s the digital version of a bounced check.

The two main codes you'll see here are:

- R01 – Insufficient Funds: The account balance was too low when the payment was processed. This is the code merchants run into most often.

- R09 – Uncollected Funds: The money is technically in the account, but it hasn’t cleared yet. For instance, a recent deposit is still pending, so the funds aren’t actually available to be withdrawn.

These returns are frustrating but are often just a timing issue. In many cases, you can simply notify the customer and try the payment again in a few days.

An R01 or R09 code points to a funding issue, but sometimes customers dispute charges for other reasons, triggering a totally different kind of reversal. You can learn more about how a payment reversal works and what it means for your business.

Invalid or Incorrect Account Information

Sometimes, the payment fails before it even gets a chance to look for funds. This happens when the banking details you have are just plain wrong. A single typo in an account or routing number is all it takes to get an instant rejection.

Common codes for bad information include:

- R02 – Account Closed: The bank account you tried to pull from is no longer active.

- R03 – No Account/Unable to Locate Account: The account number you used doesn’t exist at that bank, or it’s linked to the wrong name.

- R04 – Invalid Account Number: The structure of the account number is wrong (for example, it has the wrong number of digits).

When you see these codes, it’s a hard stop. You absolutely cannot retry the payment until you get updated, correct information directly from your customer.

Customer-Initiated Returns

The final group of returns is triggered by an action the customer took themselves. These are more serious because they usually signal a dispute or a change of heart, and they demand immediate attention and careful communication on your part.

The key codes in this category are:

- R07 – Authorization Revoked by Customer: Your customer previously gave you permission to debit their account but has since told their bank to block all future payments to you.

- R08 – Payment Stopped: This is like stopping a check. The customer put a stop payment order on this one specific transaction.

- R10 – Customer Advises Not Authorized: This one's a big deal. The customer is claiming they never approved the charge in the first place.

For banks that process these transactions, staying on top of regulatory updates, like the evolving 2026 Nacha Rules, is crucial for interpreting these codes correctly and staying compliant. As a merchant, knowing what each code means helps you avoid bigger problems down the road.

Common NACHA Return Codes and What They Mean for You

To make things easier, we've put together a quick-reference table. It breaks down the most frequent return codes you'll encounter, what they mean in plain English, and whether you can try running the payment again.

This table should cover the vast majority of ACH returns you'll see. By understanding these codes, you can quickly diagnose payment failures and take the right steps to fix them.

How Much These Fees Actually Cost Your Business

When an ACH payment bounces, the damage goes way beyond just the missing revenue. The first thing you'll feel is the sting of the ACH return charges themselves, which is like adding insult to injury. These fees aren't coming from just one place, either; they often involve a whole chain of financial institutions.

The customer's bank (the RDFI) might ding you with a fee for the failed attempt. Then, your own bank or payment processor (the ODFI) will pass that cost right along to you—often tacking on their own fee for the trouble. So for one failed payment, you could be getting hit with penalties from multiple directions.

This flowchart gives you a quick visual breakdown of why a payment might fail in the first place, which is the key to understanding the costs involved.

As you can tell, the reasons for a return fall into a few clear buckets. Each one requires a different game plan to stop it from happening again.

The Direct Cost of a Single Return

So, what’s the real damage? A single ACH return fee can run you anywhere from $2 to over $15. A $5 fee might not sound like much, but for businesses running hundreds or thousands of transactions a month, it's a classic case of death by a thousand cuts.

Think about it this way: if you have 500 subscribers on a monthly plan and just 2% of those payments fail each month, you're looking at 10 returns. With an average fee of $10 per return, you’re losing $1,200 a year on fees alone. That’s before you even try to chase down the actual subscription revenue you lost.

These direct fees feel a lot like the penalties you see with credit cards. It's helpful to understand the difference between an ACH return fee and what a chargeback fee is, because while both can seriously hurt your bottom line, they stem from completely different problems.

The Hidden Costs You Can't Ignore

The fee you see on your statement is just the tip of the iceberg. The real threat from a high return rate comes from the hidden, long-term consequences that can put your business's financial health at risk.

Here’s what’s really at stake:

- Higher Processing Rates: If your return rate starts creeping up past the acceptable threshold set by NACHA (usually 0.5% for unauthorized returns), your payment processor will flag you as a high-risk merchant. To cover their own risk, they'll likely jack up your processing fees across the board.

- Account Termination: In a worst-case scenario, a processor might decide you're just too risky to work with and shut down your merchant account completely. This can stop your ability to accept payments cold, essentially crippling your business overnight.

These compounding costs make one thing crystal clear: managing ACH returns isn't just about saving a few bucks here and there. It’s about protecting your ability to process payments and ensuring the long-term survival of your business.

The Hidden Business Problems Caused by ACH Returns

The fee for an ACH return is annoying, for sure. But it’s the operational domino effect that really hurts your business. A single failed transaction kicks off a chain reaction, pulling your team away from their real jobs and putting a strain on your entire operation.

Think about it. It’s not just a payment issue; it's a problem that trickles down to your finance, customer service, and even sales teams.

When an ACH payment fails, someone has to drop what they’re doing and investigate. Your finance team spends valuable time digging through records to figure out what went wrong. Then, they have to manually update billing information—a tedious process that’s ripe for human error. This isn't just a one-off task; it's a recurring drain on productivity.

Disruptions to Cash Flow and Customer Trust

Beyond the manual labor, ACH returns punch unpredictable holes in your cash flow. The revenue you were counting on to make payroll or pay suppliers suddenly vanishes, forcing you to scramble. That instability makes financial forecasting a nightmare and can halt your ability to invest in growth.

Even more importantly, a failed payment creates a genuinely bad customer experience. Imagine a customer’s subscription getting canceled or their service interrupted because their payment didn't go through. It’s frustrating for them and reflects poorly on your brand, making you seem unreliable. This is one of the many ways a chargeback can hurt your business, as unresolved payment issues often escalate.

The impact of a failed transaction goes far beyond the immediate fee. It erodes customer trust, interrupts service delivery, and consumes valuable team resources that could be focused on innovation and growth.

The Broader Financial Risk

This isn't a problem that's going away. In fact, it's getting worse. Global chargeback volumes are exploding, projected to surge to a staggering 324 million by 2028—that’s a 24% jump in just three years. This trend is fueled by the boom in online transactions, which are naturally more prone to these kinds of issues.

This highlights a critical point for merchants: every failed payment, whether an ACH return or a chargeback, contributes to a risk profile that payment processors watch like a hawk. A high return rate isn't just a financial drain. It's a red flag to processors that your business might be a liability, potentially leading to higher fees or even getting your account shut down.

Managing these returns proactively isn't just good housekeeping—it's essential for safeguarding your revenue and your business's future.

Practical Ways to Prevent ACH Return Charges

Knowing what causes ACH returns is one thing, but actively stopping them from happening is where you really start protecting your bottom line. The good news? You don't have to just accept these fees as a cost of doing business. A few smart tweaks to your payment process can dramatically cut down your return rate.

A surprising number of returns boil down to simple, avoidable mistakes—think a customer mistyping their account number. Others pop up because of bad timing or a breakdown in communication. By getting in front of these common issues, you can build a much more reliable payment system that keeps failures to a minimum and your cash flow strong.

Fortify Your Intake Process

Your first line of defense against ACH return charges is making sure the customer data you collect is right from the start. It’s a whole lot easier to block bad information from entering your system than to clean up the mess after a payment fails.

A simple but surprisingly effective trick is to use a dual-entry system on your payment forms. Just asking a customer to type their account and routing numbers twice can catch a ton of typos before they become a real problem. That tiny bit of friction upfront can save you a massive headache later.

The goal is to create a validation firewall. You want to stop invalid account numbers, closed accounts, and other data errors before a transaction is ever submitted to the ACH network.

Taking it a step further, using a bank account verification service is a game-changer. These tools can confirm in real-time that a bank account is valid and in good standing before you even try to process the first payment. This immediately weeds out closed or non-transactional accounts that would have been a guaranteed return.

Sharpen Your Communication Strategy

You’d be amazed how many returns—especially for insufficient funds (R01) or revoked authorizations (R07)—can be prevented with clear, consistent communication. When customers know exactly when a charge is coming, they're far less likely to have an empty account or to panic and stop the payment.

Here are a few simple communication tactics that punch well above their weight:

- Send Pre-Debit Notifications: An automated email or text message sent 2-3 days before a recurring payment is scheduled gives your customers a heads-up to make sure the funds are there.

- Use Clear Billing Descriptors: Make sure the name that shows up on your customer's bank statement is one they’ll instantly recognize. A cryptic company name is a fast track to a customer reporting the charge as unauthorized.

- Make Cancellation Easy: Give customers a dead-simple way to cancel their subscriptions. If they feel trapped, they're more likely to just call their bank to revoke authorization, which triggers a more serious type of return for you.

One of the most effective ways to prevent ACH return charges is by adopting supplier payment automation, which slashes manual errors and smooths out the entire payment process. When you automate key parts of your workflow, you cut down on the human errors that so often lead to costly returns. Pairing this with effective transaction monitoring solutions gives you real-time insights to spot and fix problems before they blow up.

Frequently Asked Questions About ACH Returns

Even with the best planning, ACH returns can still throw a wrench in your operations. It’s only natural to have questions. This quick Q&A section covers the most common ones we hear from merchants, giving you straightforward answers when you need them.

Can I Dispute an ACH Return Charge?

This is a big one, but the short answer is almost always no. It's tough to dispute the fee itself because, from the bank's perspective, it's a legitimate charge for their work in processing a failed transaction. Think of it like paying a delivery service that attempted to drop off a package, even if the recipient wasn't home—the service was still performed.

Your energy is far better spent tackling the root of the problem. For example, if a customer revokes their authorization (an R07 return), your best move is to contact them directly with a copy of their original payment agreement. The goal isn’t to fight over a small bank fee; it’s to recover the much larger payment and get their billing details corrected for the future.

What Is the Difference Between an ACH Return and a Chargeback?

They might feel similar since both reverse a payment, but they're completely different animals.

An ACH return is a technical failure within the banking network. It's an automated process triggered by things like insufficient funds, a closed bank account, or even just a typo in the account number. The system is essentially saying, "Sorry, this transaction can't go through."

A chargeback, on the other hand, is a manual dispute initiated by the customer through their credit card company. It’s almost always related to the product or service itself, with common reasons being "product not delivered" or "unauthorized credit card transaction." Chargebacks involve a formal, often lengthy dispute process, come with much steeper fees, and carry harsher penalties for merchants.

How Quickly Will I Know About an ACH Return?

You can generally expect to find out about an ACH return within 2 to 5 business days. While NACHA rules allow for a longer window for certain return types, the most common ones—like insufficient funds (R01)—are usually flagged pretty quickly.

Your payment processor will let you know as soon as they get the notice from the banking network. This is exactly why it’s so critical to keep a close eye on your payment dashboard. Consistent monitoring allows you to spot these issues the moment they happen so you can kick off your customer outreach right away.

How Can I Automate My Response to a Failed Payment?

Automation is your single most powerful ally in managing failed payments and softening the blow of ACH return charges. Most modern payment platforms, like Stripe or PayPal, let you set up automated workflows that handle these hiccups without you having to lift a finger.

Here are a few ways you can automate your response:

- Automated Emails: You can set up your system to instantly fire off an email to a customer the moment their payment fails. This message can clearly explain the problem and include a simple link for them to update their payment details on the spot.

- Smart Retries: For subscription businesses, this is a game-changer. Many platforms can be configured to automatically retry a failed payment a few days later. This simple step often catches customers who just had a temporary cash flow issue.

- Dunning Management: For a more sophisticated strategy, dunning software automates a whole series of communications. It can send multiple reminders over a specific period, intelligently retrying the charge at times when it’s most likely to succeed, maximizing your chances of recovering the payment.

By automating your response, you can turn a potentially lost customer into a successful recovery. It transforms a reactive, manual chore into a proactive, revenue-saving system.

This hands-off approach not only frees up your team's time but also creates a professional and non-confrontational experience for your customers, helping you keep them around for the long haul.

Dealing with failed payments and their fees is a constant battle. At ChargePay, we use AI to automate the entire chargeback and payment dispute process, recovering lost revenue for you without any manual work. Protect your revenue hands-free with ChargePay.

.svg)

.svg)

.svg)

.svg)