Ever glanced at your business statement and been stopped in your tracks by a "chargeback fee"? If so, you're not alone. The first time you see one, it’s easy to wonder what exactly it is.

Think of it as a non-refundable penalty that your payment processor charges you every single time a customer disputes a transaction. This fee is completely separate from the actual refund and is meant to cover the administrative costs the bank incurs handling the dispute.

Understanding Your First Chargeback Fee

When a customer files a chargeback, it kicks off a formal, multi-step process that pulls in their bank, your bank, and the card networks (Visa, Mastercard, etc.). The chargeback fee is simply the price you pay for that process to happen. It's not the refund itself; it's a service charge from your payment processor for the time and effort they spend investigating the claim.

Here's an easy way to think about it: a refund is a simple two-way street between you and your customer. A chargeback, on the other hand, is a forced reversal that brings in outside parties to mediate the disagreement. And that mediation isn't free.

The core purpose of the chargeback fee is to cover the operational costs tied to the dispute. It exists whether you win or lose the case, making prevention the best strategy.

This cost is a direct hit to your profits. Even if you fight the chargeback and win—proving the charge was legitimate and getting the original sale amount back—you typically will not get the chargeback fee back.

Who Actually Charges the Fee?

It’s a common mix-up to think the customer’s bank is the one sending you the bill. The reality is, the fee comes from your own financial partners.

This could be:

- Your Payment Processor: Companies like Stripe, PayPal, or Square charge this fee for managing the dispute on your behalf.

- Your Merchant Acquirer: This is the bank that gives your business a merchant account to accept card payments in the first place. They pass the costs of the dispute process down to you.

These fees are pretty much non-negotiable and usually land somewhere between $15 to $100 per incident. The exact amount depends on your provider, your industry's risk profile, and your business's own chargeback history. For any merchant taking card payments, getting a handle on this hidden cost is the first step to protecting your bottom line.

How Much Chargeback Fees Actually Cost You

Thinking about chargeback fees as a single, fixed number is a common mistake. In reality, the cost can swing pretty wildly. It’s less of a flat fee and more of a "dispute penalty" that changes based on a few key things.

The biggest factors are who you use for payment processing, which card network is involved (like Visa or Mastercard), and—this is a big one—your business's track record with disputes. If you have a history of frequent chargebacks, processors see you as a higher risk and will almost always hit you with steeper fees for every new incident.

Key Factors Determining Your Fees

The final number you pay is a cocktail of different costs. It's a classic case of reading the fine print; a processor might lure you in with low transaction rates, only to make their money back on high dispute fees.

Here’s what really moves the needle on your chargeback costs:

- Payment Processor Policies: Every provider, from Stripe to PayPal, has its own fee schedule. You can expect to see anything from a $15 fee to well over $35 per incident.

- Card Network Rules: Visa, Mastercard, and American Express all have their own fee structures that processors have to follow. Guess who that cost usually gets passed on to? You.

- Your Chargeback History: A clean record is your best friend. The fewer disputes you have, the better your chances of keeping those fees low. But if your chargeback ratio starts climbing, expect those penalties to get more painful.

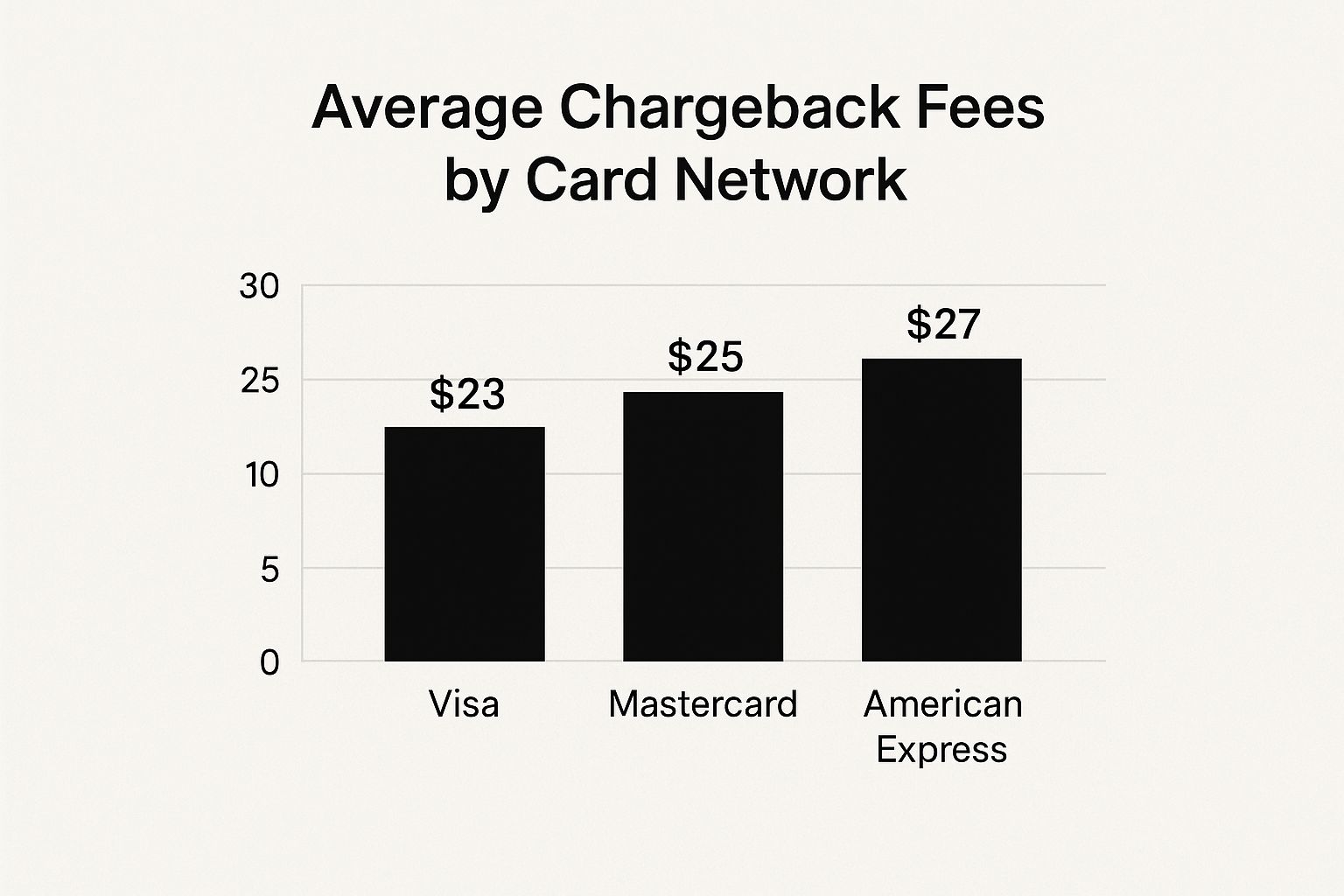

Just look at how much the fees can vary depending on the card network alone.

As you can see, while they're all in a similar ballpark, American Express tends to have the highest average cost. And these are just the administrative fees. They don't even touch on the internal costs the banks are eating.

Each chargeback costs financial institutions between $9.08 and $10.32 on average to process. This figure doesn't even account for the employee hours spent managing the dispute. For certain sectors, like travel, the average chargeback value can soar to $120 per transaction. You can learn more about the true cost of a chargeback directly from Mastercard's own insights.

It just goes to show how one single disputed sale can quickly balloon into a significant financial hit once you start adding up all the associated costs.

Typical Chargeback Fee Ranges by Provider Type

To give you a clearer picture, the fees you'll face often depend on the type of payment provider you're working with. Here’s a quick breakdown of what you can generally expect.

As you can see, the choice of provider has a direct impact on your bottom line when a dispute arises. Choosing a partner that fits your business's risk profile is crucial for managing these costs effectively.

Why Your Customers Are Filing Chargebacks

If you want to get a handle on chargeback fees, you first have to get inside your customers' heads. Why are they filing disputes in the first place? It almost always boils down to one of three reasons, and each one needs a different game plan.

Let's start with the most common culprit: legitimate merchant errors. These are the honest-to-goodness mistakes that, while completely accidental, sour the customer experience and push them toward a chargeback.

- Fulfillment Mistakes: A customer orders a blue shirt but gets a red one. If your return process is a maze, a chargeback suddenly looks like the quickest way out for them.

- Technical Glitches: A bug on your website double-charges a customer for the same order. When they see two identical charges on their statement, they’ll naturally dispute one.

- Unclear Billing Descriptors: The charge on their statement shows up as "SP*MERCH-TX" instead of "Your Awesome Gadget Store." If they don't recognize the name, they'll assume it's fraud.

Fraud and Customer Confusion

Beyond simple slip-ups, you’ll run into more complex chargeback triggers. Criminal fraud is what most merchants picture—a thief using stolen credit card numbers to go on a shopping spree at your expense.

But a far more common and maddening problem is friendly fraud. This is when a customer disputes a charge that was actually completely valid. Sometimes it’s an innocent mistake; maybe their teenager used the card without asking, or they simply forgot they made the purchase.

But friendly fraud can also be intentional. A customer might get your product, love it, and still file a chargeback just to get their money back for free. It's a practice some call "cybershopflifting." Getting a grip on this behavior is key, and you can dive deeper into how to identify and combat friendly fraud to protect your business.

By pinpointing the real reason for a dispute—whether it's a simple shipping error, a confused customer, or deliberate fraud—you can build a much smarter strategy to stop chargebacks before they even start.

The Real Damage Chargebacks Do to Your Business

That initial chargeback fee you see? It's really just the tip of the iceberg. The real damage to your business runs much deeper, creating a ripple effect that touches everything from your bank account to your daily operations. For every single dispute, you’re instantly out the sale revenue plus that non-refundable fee.

Think of it like a slow leak in a boat. One chargeback might not seem like a big deal, but they add up fast. Each dispute also drains your most valuable resource: time. Your team has to drop what they’re doing, hunt down evidence, and fight a battle they're statistically likely to lose anyway.

Beyond the Fees: The Threat to Your Merchant Account

The most serious danger isn't just the direct financial hit; it’s the threat to your ability to do business at all. Payment processors keep a close eye on your chargeback ratio—that's the percentage of your transactions that end up as a dispute.

If this ratio creeps over their limit (usually around 1%), you get flagged as a high-risk merchant. This can set off a chain reaction of painful consequences that make it much harder to run your business.

These penalties often include:

- Higher Processing Rates: Your processor will start charging you more for every single transaction to offset their perceived risk.

- Mandatory Cash Reserves: You might be forced to keep a hefty chunk of your own money in a reserve account, held by the processor, just to cover potential future disputes.

- Account Termination: In the worst-case scenario, your processor can shut down your merchant account entirely. This means you can no longer accept credit or debit card payments, bringing your sales to a screeching halt.

Losing your merchant account is a devastating blow that can be incredibly difficult to recover from. Understanding exactly how chargebacks hurt your business is the first step toward building a strong defense and protecting your long-term stability.

Practical Ways to Reduce Your Chargeback Fees

The only real way to cut down on chargebacks—and the fees that come with them—is to get ahead of the problem. You don't have to just sit back and accept these costs as a normal part of doing business. By putting a few smart strategies in place, you can build a strong defense that protects both your revenue and your customer relationships.

Your main goal should be to stop disputes before they even have a chance to begin. Think about it: a chargeback is often just a symptom of a communication breakdown. One of the biggest areas you can improve is your customer service. For instance, using better tools for managing customer orders and requests better can make a huge difference, often stopping issues from ever escalating to a formal dispute.

Adopt Proactive Prevention Methods

Your best defense against chargebacks is a good offense. This starts with making every part of your business as transparent and secure as you can. When you remove the common reasons for customer confusion and frustration, you'll see disputes drop.

Here are four key strategies you can put into practice right away:

Use Clear Billing Descriptors: Make sure the name that shows up on a customer's credit card statement is one they'll actually recognize. A generic code like "WEB*PAYMENT" is a recipe for a chargeback. Instead, it should clearly state your store's name, something like "Bob's Bike Shop." This simple change prevents a ton of "I don't recognize this charge" disputes.

Provide Excellent Customer Service: You need to make it incredibly easy for customers to get in touch with you if there's a problem. Display your phone number, email address, and live chat options where everyone can see them. A quick refund is always, always cheaper than a chargeback fee.

Think of it this way: a customer with a problem will always look for the path of least resistance. If contacting your support team is easier than filling out their bank's dispute form, you win.

Keep Detailed Transaction Records: Hold on to thorough records for every single sale. This means customer communications, shipping confirmations with tracking numbers, and proof of delivery. This evidence is your best ammo if you ever need to fight an illegitimate chargeback.

Implement Fraud Detection Tools: Don't ignore the security features your payment processor offers. Activating Address Verification Service (AVS) and requiring the Card Verification Value (CVV) for every transaction are simple but powerful layers of security. They make it much harder for fraudsters to make a purchase.

By weaving these practices into your daily operations, you’ll be in a much stronger position to stop disputes in their tracks. For an even more detailed guide, check out our article on how to avoid chargebacks and protect your bottom line.

Your Questions About Chargeback Fees Answered

To wrap things up, let's tackle some of the most common questions merchants have about those pesky chargeback fees. Getting quick, clear answers helps you handle disputes with more confidence and protects your business from unnecessary costs.

Can I Get a Chargeback Fee Refunded?

This is a big one, but unfortunately, the answer is almost always no.

The chargeback fee itself is non-refundable, even if you win the dispute and get the original sale amount back. This fee is what your processor charges for their administrative time managing the case. It’s a perfect example of why preventing the chargeback in the first place is a much better financial strategy than fighting it.

What Is a Good Chargeback Rate for a Business?

Most payment processors and card networks consider a chargeback rate below 1% of your total monthly transactions to be acceptable. Think of it as the magic number to stay under.

If your rate consistently climbs above this threshold, you risk getting labeled a "high-risk" merchant. This can trigger a cascade of problems, like higher processing fees, mandatory cash reserves, or even having your account shut down entirely. The stakes are particularly high depending on your industry.

In Q1 2024, the travel and lodging sector saw an incredible 816% increase in chargebacks compared to the previous year, while e-commerce overall faced a 222% rise. You can discover more insights about these chargeback statistics and what they mean for merchants.

What Is the Difference Between a Chargeback and a Refund?

The key difference really comes down to who’s involved.

A refund is a direct, two-way agreement between you and your customer. You agree to return their money, and it's generally seen as a sign of good customer service. It's a conversation.

A chargeback, on the other hand, is a forced transaction reversal kicked off by the customer through their bank. It completely bypasses you, pulling in banks and card networks to settle the dispute. This formal, multi-party process is exactly why it always comes with that punitive chargeback fee. For a deeper look at how specific platforms handle this, check out our guide on managing PayPal chargebacks.

Stop letting disputes drain your revenue and time. ChargePay uses AI to automate chargeback representment, boosting your win rate and recovering lost funds hands-free. Start for free and see how much you can reclaim.

.svg)

.svg)

.svg)

.svg)