A payment reversal is exactly what it sounds like: funds from a transaction are returned to the customer's account. It's the financial equivalent of hitting "undo" on a sale after the money has already been processed. This is a big-picture term that covers everything from a simple, merchant-approved refund to a more complicated bank-led dispute.

What is a Payment Reversal?

Think of it like returning a book to the library. You checked it out (the customer made a purchase), but for whatever reason, it needs to go back on the shelf (the payment gets reversed). The money travels from your business account right back to where it started—the customer's account.

This whole process can kick off for a few different reasons.

Sometimes, it's an honest mistake. Maybe your system accidentally double-charged a customer for a single coffee. Or, a customer might be unhappy with their purchase and ask for their money back directly. In more serious cases, a transaction might get flagged for potential fraud, triggering a reversal to protect the cardholder.

As digital payments get faster and more common, so do these reversals.

With instant payments projected to cover over 22% of all global non-cash transactions by 2028, the time merchants have to catch errors before a payment settles is shrinking. This trend only adds to the operational headache of managing reversals effectively.

Getting a handle on what a payment reversal means is the first step for any merchant. While the end result is always the same—money is returned—the "how" and "why" behind it can be wildly different. We break down the specifics in our guide on the differences between a chargeback vs a refund vs a reversal.

Quick Guide to Payment Reversal Types

To clear things up, not all reversals are created equal. Each type has a different trigger and is initiated by a different party, which is crucial for merchants to understand.

Here’s a simple breakdown of the most common types you'll encounter:

As you can see, the key difference often comes down to who starts the process and why. Understanding these distinctions helps you respond appropriately and protect your business from unnecessary revenue loss.

The 3 Flavors of Payment Reversals

While "payment reversal" is the catch-all term for money heading back to a customer, it's not a one-size-fits-all situation. Think of it like this: not all returns are created equal. Getting to grips with the three main types—refunds, chargebacks, and authorization reversals—is key, because each one plays out very differently for you as a merchant.

Refunds: The Friendly Reversal

A refund is the simplest and most common type of reversal. It's a straightforward, cooperative agreement between you and your customer. Someone returns a sweater that didn't fit, and you willingly send the money back to their card. It’s a voluntary move on your part.

Because you're the one kicking off the process, a refund is actually a sign of good customer service. The original payment has already settled in your account, so the refund is treated like a brand-new transaction going the other way. That's why it can sometimes take a few business days to pop up in the customer's account.

Chargebacks: The Forced Reversal

Now, a chargeback is a whole different beast—and a much more serious one. This isn’t a friendly handshake; it’s a forced clawback of funds started by the customer's bank, completely bypassing you at first.

Chargebacks get triggered when a customer disputes a transaction directly with their bank. The reasons vary, but common ones include suspected fraud, an item that never showed up, or a service that wasn't what they paid for. The bank immediately pulls the money from your account while they investigate, slapping you with extra fees and putting a black mark on your record with payment processors.

Authorization Reversals: The Vanishing Hold

The third type is an authorization reversal, which is less of a returned payment and more of a canceled hold. When a customer uses their card, a temporary hold (an authorization) is placed on their funds. If you catch an error before the transaction settles—say, the item they ordered is actually out of stock—you can simply reverse that authorization.

The money never actually left the customer's account, so the hold just vanishes. It's clean, quick, and avoids all the drama of a refund or chargeback.

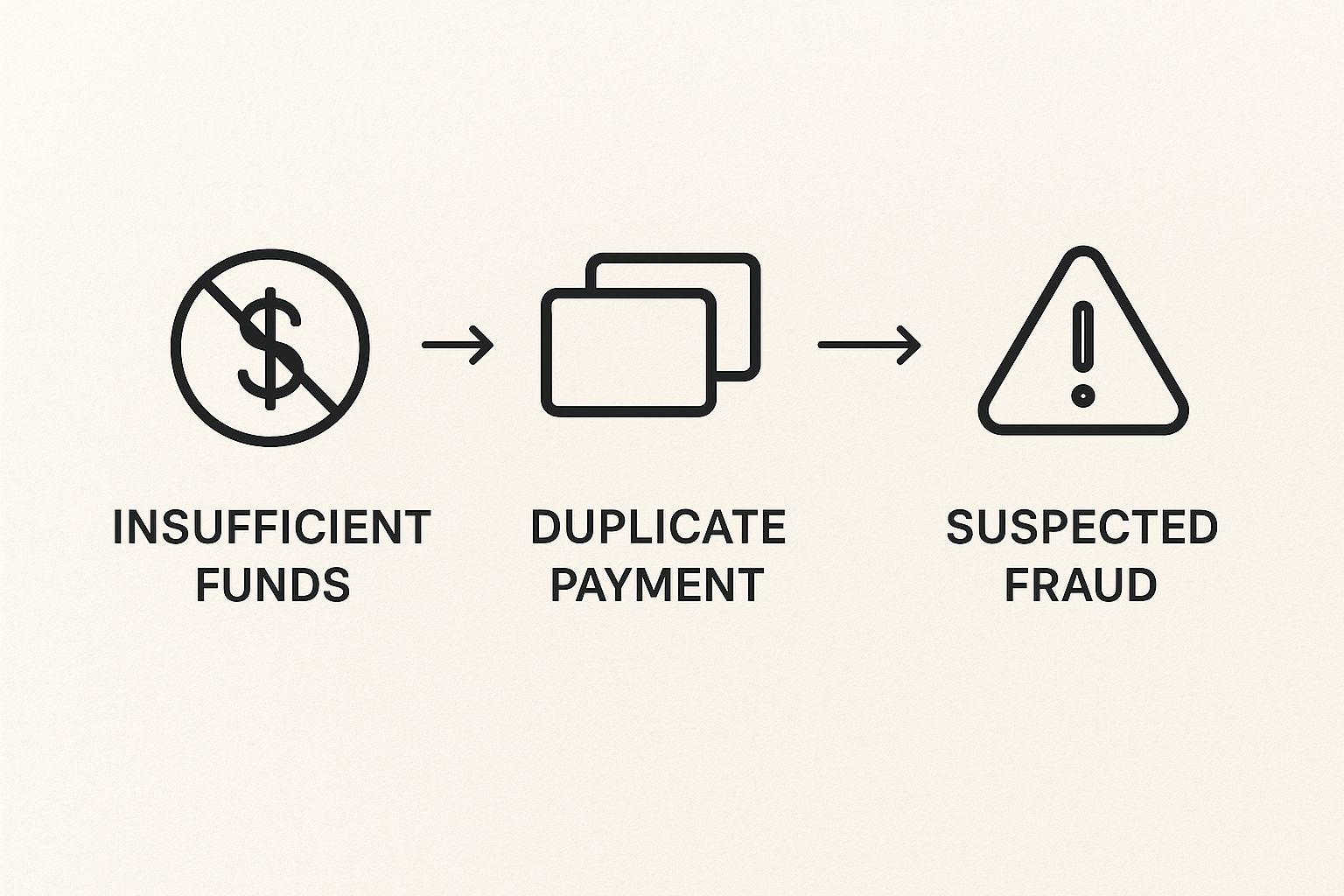

This image breaks down some of the most common reasons a reversal might get triggered.

As you can see, the triggers range from simple processing mistakes to more serious fraud issues, and each path leads to a very different kind of reversal.

Why Payments Get Reversed in the First Place

So, you know the different types of reversals, but what actually kicks them off in the real world? A payment reversal isn't some random glitch; it's a direct response to a specific problem somewhere in the transaction chain. For any business owner who wants to keep their revenue safe, getting to the bottom of these triggers is the absolute first step.

Most of the time, payment reversals boil down to one of four main culprits. Each one tells a different story about what went wrong.

The Four Main Causes of a Payment Reversal

Let's unpack the common reasons a customer, their bank, or even you might have to hit the reverse button on a transaction.

Customer Disputes: This is, by far, the most common trigger. A customer might dispute a charge because their order was a no-show, the item arrived broken, or it simply wasn't what they were promised. Think about it: if someone orders a blue jacket but gets a red one, they have every right to start the reversal process.

Suspected Fraud: Banks and payment processors are always on high alert for shady activity. If a crook uses a stolen credit card to buy something from your store, the legitimate cardholder will eventually spot the charge and report it. This kicks off a reversal that, unfortunately, lands right back on your plate.

Processing Errors: Hey, technology isn't perfect. Sometimes, a system glitch might accidentally charge a customer twice for the same thing. Or maybe a cashier fumbles and keys in the wrong amount at the register. These are usually honest mistakes that a quick refund or authorization reversal can fix.

Clerical and Technical Glitches: This bucket covers all the small but frustrating mix-ups. A classic example is an unclear billing descriptor on a customer's bank statement. If a charge shows up as "XYZ Corp" instead of "The Corner Cafe," a confused customer might assume it's fraud and dispute it, even though they loved their latte.

It's worth pointing out that not all reversals, especially chargebacks, are legitimate. In fact, some studies suggest that as many as 80% of chargebacks could be "friendly fraud"—when a customer disputes a perfectly valid charge.

This is exactly why having a proactive game plan is so important. A growing number of businesses are now using automated tools for effective chargeback fraud prevention to plug these kinds of revenue leaks. Once you understand where the problem is coming from, you can start building a much stronger defense.

How Reversals Create Real Problems for Businesses

From a customer’s point of view, getting a payment reversed is a pretty straightforward fix. But if you're a business owner, a reversal—especially a chargeback—is so much more than a simple refund. It kicks off a frustrating and expensive chain reaction that can seriously damage a business.

Think about it like this. Say you run a small online shop selling handmade crafts. A single chargeback isn't just one lost sale; it's a triple hit to your bank account. First, you lose the revenue from the sale itself. Second, you've probably already shipped the item, so the inventory is gone, too. And to top it all off, your payment processor will slap you with a separate chargeback fee, which can run anywhere from $15 to $100.

More Than Just Lost Money

The financial sting is bad enough, but the damage doesn't stop there. Every single chargeback acts like a black mark against your merchant account. Payment processors like Visa and Mastercard are always watching your chargeback ratio—that’s the percentage of your transactions that get disputed.

If that ratio creeps too high, you risk being labeled a "high-risk" merchant. This can trigger higher processing fees, frozen funds, or in a worst-case scenario, having your merchant account shut down entirely. For any business that sells online, losing the ability to accept credit cards is basically a death sentence.

And this isn't a small problem. We're talking about massive numbers. Global payment fraud losses hit a staggering USD 442 billion in 2023, with reversals being a huge part of that figure. Even with billions being poured into prevention, honest merchants often get caught in the middle.

A few chargebacks here and there might not seem like a big deal, but they create a pattern. Too many of them send a signal to banks that something might be wrong with your products, customer service, or security, eroding the trust you absolutely need to operate.

Learning how to manage these disputes effectively is non-negotiable for survival. Many businesses are now turning to specialized chargeback management tools to automate their defense and hang on to their revenue. Without a solid strategy in place, a handful of customer disputes can quickly spiral into a genuine threat to your entire business.

Practical Ways for Businesses to Prevent Reversals

Reacting to reversals after they happen is one thing, but what if you could stop them before they even start? Getting ahead of disputes isn’t just about protecting your revenue; it’s about building real, lasting trust with your customers.

The secret is making the entire customer experience as clear and smooth as possible. You’d be surprised how small tweaks in communication and transparency can stop a simple misunderstanding from snowballing into a costly chargeback.

Sharpen Your Communication

Your first line of defense is just talking to your customers clearly. Seriously. Confusion is the seed for so many disputes, so your goal is to pull it out by the roots.

- Write Crystal-Clear Product Descriptions: Be brutally honest and incredibly detailed about what you're selling. Use high-quality photos, list dimensions and materials, and point out any potential quirks. You want your customer’s expectations to perfectly match reality.

- Make Your Billing Name Obvious: This one is huge. Make sure the name that shows up on a customer's bank statement is one they'll actually recognize. A charge from "Awesome Gadgets" is a lot less scary than one from "AG LLC," which a customer might flag as fraud without a second thought.

Bolster Your Processes

Strengthening your internal processes is all about catching potential problems—like errors or outright fraud—before they ever reach the customer.

A proactive approach is absolutely essential in today's fast-moving payment world. The global payments market is on track to hit USD 5.34 trillion by 2030, thanks to the explosion of digital wallets and instant payments. But all that speed and volume just create more opportunities for disputes to pop up. You can dig deeper into this growth in the latest market report.

Simple security checks, like always requiring the CVV code, can filter out a surprising amount of fraudulent purchases. On top of that, providing amazing, easy-to-find customer service gives an unhappy customer a direct line to you for a solution, instead of them going straight to their bank.

For more advanced strategies, you might want to check out our guide on comprehensive chargeback prevention.

Frequently Asked Questions About Payment Reversals

Alright, let's wrap things up by tackling some of the most common questions we hear about payment reversals. This should help clear up any lingering confusion for shoppers and business owners alike.

How Long Does a Payment Reversal Take?

The timeline for a payment reversal can really vary, depending on what kind it is. An authorization reversal, which is just a canceled hold on your card, can disappear in a few hours.

If a merchant issues you a refund, you'll typically see it pop up on your statement in about 3-7 business days.

The longest process by far is a chargeback. Because it involves a formal investigation between your bank and the merchant's bank, it can take anywhere from 30 days to several months to be fully resolved.

Can a Payment Reversal Be Canceled?

It really depends on the situation. If a customer kicks off a chargeback but then works things out directly with the merchant, they can call their bank and ask to cancel the dispute. Once the investigation is well underway, though, it becomes much harder to stop.

Refunds, on the other hand, are pretty much final once the merchant has processed them. This is exactly why direct communication between a business and its customer is always the best first step—it can prevent a simple issue from escalating.

Is a Payment Reversal the Same as a Refund?

Nope, but it's an easy mix-up to make. A refund is just one type of payment reversal.

Think of it this way: all refunds are reversals, but not all reversals are refunds.

Here’s the key difference that matters:

- A refund is a friendly, voluntary action. The merchant agrees to give you your money back.

- A chargeback, another type of reversal, is involuntary. The customer’s bank forces the money back from the merchant because of a dispute.

This distinction is crucial for business owners because the impact of a friendly refund is worlds apart from a forced chargeback. For even more detailed answers, you can always explore our complete list of frequently asked questions for merchants.

Are you tired of losing revenue to confusing and time-consuming chargebacks? ChargePay uses AI to automate the entire dispute process, recovering up to 80% of your lost funds without you lifting a finger. See how much you can recover by visiting https://www.chargepay.ai today.

.svg)

.svg)

.svg)

.svg)