Fraud prevention for ecommerce is all about protecting your online store from the financial black holes that deceptive activities create. It involves a mix of smart strategies and the right tools to spot and stop bogus transactions before they do any damage. Think of it as safeguarding your revenue while keeping your customers' trust intact. A solid defense isn't a luxury; it's a must-have for any online business.

Why Fraud Prevention Matters More Than Ever

If you're running an online store, you're a digital shopkeeper. And just like a brick-and-mortar store owner worries about shoplifters, you face a similar—though sneakier—threat every single day. The problem is, digital shoplifting is far more sophisticated and can be absolutely devastating to your bottom line.

This isn't just about a few lost dollars here and there. The impact of fraud sends ripples through your entire operation, creating headaches that go way beyond the initial lost sale.

The Hidden Costs of Ecommerce Fraud

When a fraudulent order slips through the cracks, you don't just lose the product. You're also slapped with chargeback fees from your payment processor, which pile up fast. Those are the obvious hits, but the damage doesn't stop there.

Just look at the other consequences:

- Wasted Time and Resources: Every fraudulent claim means investigation, paperwork, and back-and-forth with banks. That's time you and your team should be spending on growing the business.

- Damaged Brand Reputation: If customers start feeling unsafe on your site because of fraud, the trust you’ve worked so hard to build can evaporate in an instant.

- Strained Bank Relationships: A high chargeback rate can land you in the "high-risk" category with payment processors. This can lead to steeper fees or, in a worst-case scenario, losing your merchant account entirely.

The scale of this issue is staggering. Global ecommerce fraud is on track to cause $48 billion in losses every year by 2025. That number alone should tell you how critical robust security has become. In fact, most online retailers are now juggling five or more fraud detection tools just to keep up.

In short, effective fraud prevention isn't just a techy add-on; it's a core business function. It's about protecting your assets, preserving your reputation, and making sure your customers feel secure every time they click "buy."

Recent laws like the Understanding the INFORM Consumers Act also underscore how seriously this problem is being taken, especially in online marketplaces. It's clear that from both a business and regulatory perspective, staying ahead of fraudsters is non-negotiable.

Ultimately, understanding how does chargeback hurt businesses is the first step toward building a stronger, more resilient store.

Understanding Common Ecommerce Fraud Schemes

To really protect your online store, you first have to know what you're up against. Think of it like a security guard learning to spot counterfeit money—once you know the common tricks, you become much harder to fool. Fraudsters have a diverse playbook, but most of their schemes fall into a few key categories.

Recognizing these patterns is the first step in building a solid defense. Each scam works a little differently, targeting various weak points in the ecommerce process, from the checkout page all the way to your returns department.

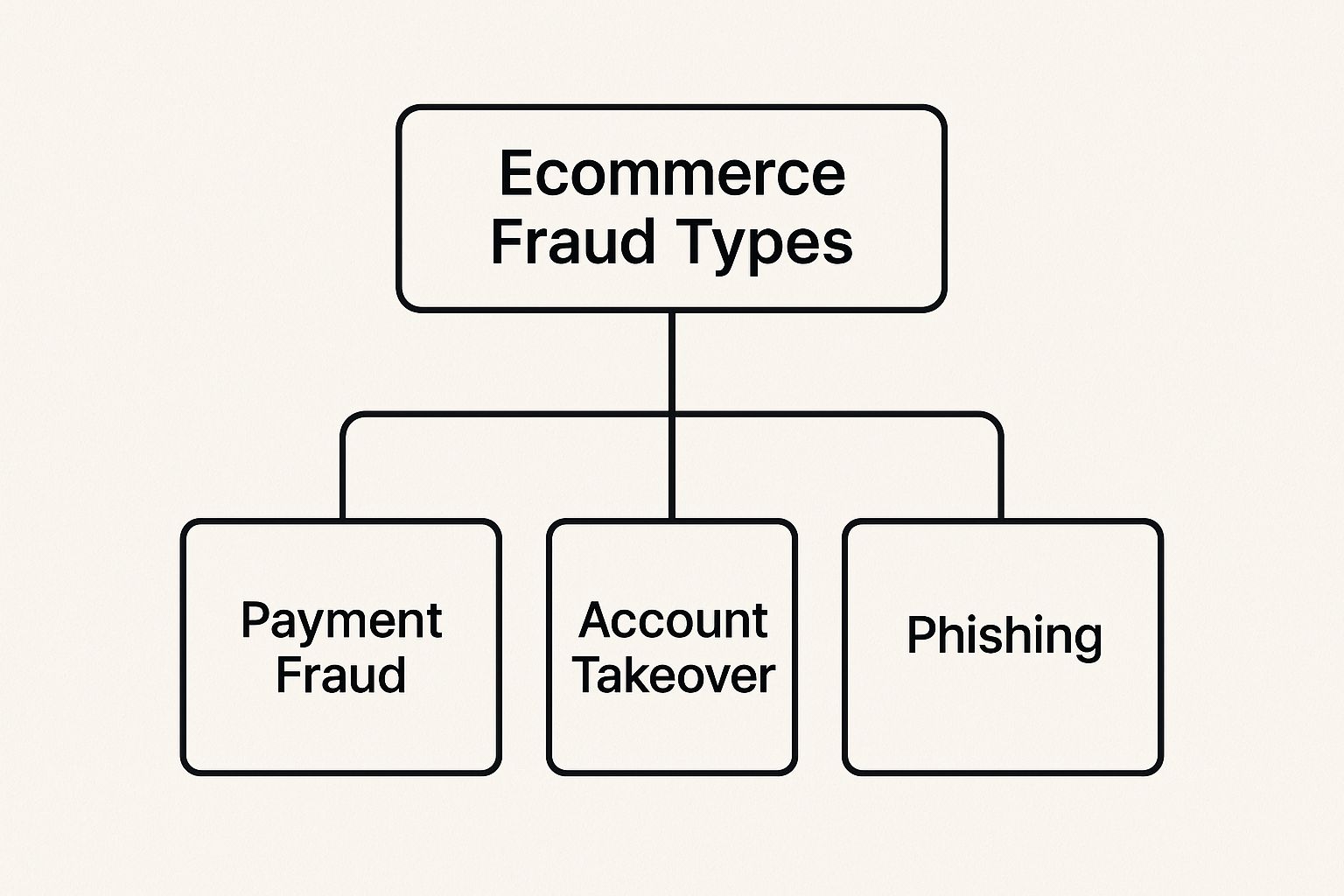

This visual breaks down the main branches of ecommerce fraud.

As you can see, the threats fan out from payment fraud and account takeovers to sneaky phishing schemes, each posing a unique risk to your business.

To help you get a quick handle on these threats, here's a simple breakdown of the most common schemes.

Common Ecommerce Fraud Schemes at a Glance

This table gives you the lay of the land, but let's dig into what each of these looks like in the real world.

Credit Card Fraud: The Classic Theft

This is the one most people think of when they hear "ecommerce fraud." A scammer gets their hands on stolen credit card details—maybe from a data breach, a phishing scam, or the dark web—and uses them to buy things from your site.

Their goal is simple: get the goods before the real cardholder notices the charge and reports it.

When the legitimate cardholder eventually disputes the charge, you're hit with a chargeback. That means you lose the product, you lose the revenue from the sale, and you get stuck paying a painful chargeback fee. It's a triple whammy.

Account Takeover Fraud

Think of Account Takeover (ATO) as the digital version of a home invasion. A fraudster gains unauthorized access to a real customer's account on your store, often by using login credentials stolen from other website breaches.

Once they're in, they can cause all sorts of chaos:

- They might place orders using the customer's saved payment info, shipping products to a new address.

- They could steal personal information or change account details to lock the real user out.

- Sometimes, they use the account's good standing and purchase history to make their fraudulent orders look more legitimate.

ATO is especially damaging because it hurts both your business and your loyal customers, eroding the trust you've worked so hard to build.

Friendly Fraud: The Accidental Threat

Not all fraud is malicious. Friendly fraud is what happens when a legitimate customer disputes a valid charge they actually made. This can happen for a few reasons: they don't recognize the transaction on their bank statement, they forgot about a recurring subscription, or a family member used their card without asking.

While the intent isn't to steal, the outcome for you is exactly the same: a chargeback. The customer gets their money back, and you lose the product and the revenue. Understanding the nuances of this is crucial, and you can learn more about it here: https://www.chargepay.ai/blog/friendly-fraud.

Even though it’s called "friendly," this type of fraud has a very real financial impact. It blurs the line between a customer service issue and outright deception, making it one of the trickiest problems for merchants to solve.

Return Fraud: Abusing Your Policies

A generous return policy is fantastic for honest customers, but it can also be a magnet for scammers. Return fraud is all about exploiting your policies for financial gain.

This scheme comes in many forms, from returning stolen merchandise for a cash refund to sending back a used or damaged item and claiming it arrived that way. Some people even practice "wardrobing"—they buy an item, wear it once, and then return it for a full refund.

This problem is growing at an alarming rate. Online returns have ballooned into a colossal $890 billion issue, with abusive returns jumping by 64% in the first half of 2025 alone. These figures show just how massive the financial drain from unchecked return abuse can be.

Phishing Schemes: The Deceptive Lure

Phishing is less about direct transaction fraud and more about stealing information. Scammers create fake emails or websites that look like they're from your brand or a trusted partner (like a shipping carrier or payment processor).

Their goal is to trick customers—or even your own employees—into revealing sensitive information like passwords or credit card numbers. A critical part of defending your store is getting familiar with phishing attack prevention strategies.

Once a fraudster has this information, they can easily use it to commit account takeover or credit card fraud, turning one successful trick into multiple headaches for you and your customers.

Building Your First Line of Defense Against Fraud

Alright, you've seen the playbook fraudsters use. Now it's time to build your defense.

Think of it like securing your house. You wouldn't install a state-of-the-art laser grid before you put good, solid locks on your doors and windows. The same exact logic applies to protecting your online store. You have to start with the fundamentals.

These first layers of security are your bread and butter, catching the majority of clumsy, low-effort fraud attempts before they ever become a headache. The best part? Many of these essential tools are already built into your payment processor, just waiting for you to flip the switch.

This is all about making your store a tougher target than the next one. Let’s get those digital locks in place.

Start with the Built-In Basics

Your payment processor isn't just a way to get paid; it's your first partner in the fight against fraud. Most of them come equipped with some basic, but incredibly effective, fraud-fighting features. You just need to make sure they're turned on and set up right.

These tools work by checking the simple details of a transaction to see if everything lines up. It's the digital version of a cashier checking the signature on the back of a credit card.

Here are the two non-negotiable features you need to enable right now:

- Address Verification Service (AVS): This is a simple but powerful check. It confirms whether the billing address the customer entered matches the address their bank has on file for that card. A mismatch is a huge red flag, because a fraudster with a stolen card number is very unlikely to know the real owner's billing address.

- Card Verification Value (CVV): That little three- or four-digit code on the back of the card? That's the CVV. Requiring it proves the person making the purchase physically has the card in their hand, which stops criminals who have only managed to get their hands on a list of stolen card numbers.

Flipping on AVS and CVV checks is one of the easiest, highest-impact moves you can make in your fraud prevention for ecommerce strategy. It's low effort, high reward.

Set Up Simple Rule-Based Filters

With the basic checks in place, your next move is to create a few simple, automated rules. Think of these as your store's personal bouncers, looking for specific red flags and turning away trouble at the door.

These are simple "if-then" commands that automatically flag or block transactions based on criteria you set. They don’t need to be complicated to be effective—they just need to spot the most common patterns of sketchy behavior.

By creating a few smart rules, you can automate a huge chunk of your fraud screening. This frees you and your team up to focus your energy on the small number of high-risk orders that actually need a human eye, instead of drowning in hundreds of perfectly fine transactions.

Here are a few powerful, easy-to-implement rules to start with:

- Flag Mismatched Addresses: Set up a rule to automatically flag any order where the billing address doesn't match the shipping address. Now, there are plenty of legitimate reasons for this—people send gifts all the time. But it's also a classic move for fraudsters, so it always deserves a quick second look.

- Monitor High-Value First-Time Orders: A brand-new customer placing an unusually large order should immediately raise an eyebrow. Set a realistic threshold (say, any first-time order over $500) that automatically triggers a manual review before you ship anything.

- Watch for Rapid Repeat Purchases: Criminals with a fresh stolen card often test it with several small purchases in a short amount of time. A rule that flags multiple orders from the same IP address or customer account within a few minutes can stop them cold.

- Check International Orders: Selling globally is fantastic, but international orders almost always carry a higher risk. You can create a simple rule to flag all orders from countries where you've seen high fraud rates in the past, just so you can give them a quick manual check.

These foundational layers—AVS, CVV, and a few smart rules—create a surprisingly strong barrier against the most common types of fraud. They are your essential first line of defense, protecting your bottom line and giving you a solid security foundation to build on.

Using Smart Tools for Fraud Detection

Basic rules and manual checks are a fantastic starting point for fraud prevention, but they can only take you so far. As your business grows, so does the sophistication of the fraudsters trying to hit your store. To stay ahead, you need to bring in smarter, more dynamic tools that can adapt on the fly.

Think of it this way: your basic rules are like a simple checklist at the door. But smart tools are like an experienced security guard who can spot trouble based on subtle cues and a gut feeling. These advanced systems work quietly behind the scenes, analyzing complex patterns that a simple rule—or even a human—would completely miss.

This is where you seriously level up your defense. You’ll move from a static set of rules to a living, learning security system. Let's look at the technologies that make this happen and how they protect your bottom line without getting in your customer's way.

Harnessing the Power of AI and Machine Learning

The terms "AI" and "machine learning" get thrown around a lot, but the concept is actually pretty straightforward. In fraud prevention for ecommerce, a machine learning system is trained on mountains of transaction data—both good and fraudulent—from thousands of different businesses.

This allows it to learn what a "normal" purchase looks like for your specific store and what just smells fishy. For example, it might pick up on the fact that fraudulent orders for your products often happen between 2 AM and 4 AM, use a particular email domain, and ship to a certain zip code. A human would probably never connect those dots, but an AI sees the pattern in an instant.

Machine learning isn't just about spotting fraud patterns we already know about; it's about predicting new ones. As criminals change their tactics, the system learns and adapts. This means your defenses actually get stronger with every single transaction it analyzes.

This self-improving nature is what makes AI such a game-changer. It automates the heavy lifting, freeing you up to focus on growing your business while it silently blocks emerging threats. The ability to automatically handle disputes is a huge plus, and you can learn more in our complete guide to automated chargeback and dispute management using AI.

Getting to Know Your Customers' Devices

Another powerful tool in the modern fraud prevention arsenal is device fingerprinting. This technology gathers anonymous information about the device a customer is using—things like their operating system, browser type, and even screen resolution.

This data is then mashed together to create a unique "fingerprint" for that specific device. It's like giving a customer's phone or computer its own digital ID.

So, how does this actually stop fraud?

- Spotting Known Bad Actors: If a device has been used for shady transactions on other websites, it will be flagged as high-risk the moment it shows up at your store.

- Catching Account Takeover: If a loyal customer suddenly logs in from a brand-new, unrecognized device, the system can trigger an extra verification step to make sure it’s really them.

- Blocking High-Volume Attacks: It can detect if one single device is trying to use dozens of different credit cards—a classic sign of a fraudster burning through a list of stolen card numbers.

Device fingerprinting adds a crucial layer of context to every order, helping you tell the difference between a loyal customer on their new laptop and a criminal trying to cover their tracks.

Analyzing How Users Behave

Finally, there’s behavioral analytics. This technology doesn't care so much about what a user buys, but how they do it. It analyzes the way a person clicks, types, and moves around your website, looking for subtle signals that suggest they aren’t a real shopper.

Think about how you shop online. You browse a bit, compare a few products, maybe add something to your cart and come back later. Fraudsters behave completely differently. They're almost always in a huge rush, trying to cash out before a stolen credit card gets canceled.

Behavioral analytics looks for the tell-tale signs of this hurried, unnatural activity. Things like:

- Copy-Pasting Information: A real customer types their name and address. A fraudster, on the other hand, will often copy-paste it from a file full of stolen info.

- Erratic Mouse Movements: Unusually fast or jerky mouse movements can be a dead giveaway that you're dealing with a bot, not a person.

- A Mad Dash to Checkout: A brand-new visitor who goes straight to your most expensive item and tries to check out in under a minute is a massive red flag.

By analyzing these tiny micro-behaviors, these systems can assign a risk score to a shopping session before a purchase is even attempted. It's a proactive approach that helps you stop fraud at the earliest possible stage, often before a transaction is even submitted.

Balancing Security with a Great Customer Experience

You’ve set up your defenses and have smart tools ready to spot fraudsters. That’s great, but there’s a delicate dance to perform here. If your security is too aggressive, you risk frustrating and turning away the very people you want to serve—your legitimate customers.

This is the central challenge in modern fraud prevention for ecommerce: protecting your business without creating a difficult, clunky checkout process. The goal is to build a fortress that keeps criminals out but leaves the front door wide open for your trusted shoppers.

It's all about finding that perfect middle ground where security feels reassuring, not restrictive.

Understanding Checkout Friction

In the ecommerce world, friction is anything that makes the buying process slower, harder, or more confusing. Think of long, complicated forms, unexpected verification steps, or, worst of all, a legitimate payment getting declined.

Each point of friction is like a hurdle in the checkout lane. A few small ones might be fine, but too many will cause shoppers to simply give up and abandon their carts. Your best customers—the ones with their payment info ready to go—expect a fast and effortless experience.

The key is to apply friction strategically. You want a smooth, frictionless path for good customers while placing obstacles directly in the way of potential fraudsters. This selective approach is what separates a smart security system from a clumsy one.

This means you can’t treat every single transaction with the same level of suspicion. A loyal customer making a typical purchase should sail right through, while a suspicious-looking, high-value order might need an extra look.

The Airport Security Analogy

A great way to think about this is to compare it to airport security. The vast majority of travelers—your legitimate customers—pass through a quick, standard screening. Their journey is designed to be as efficient as possible.

However, a small number of passengers get flagged for additional screening based on certain risk factors. This targeted approach keeps everyone safe without forcing every single person to endure a lengthy, invasive search.

Your fraud prevention should work the same way. The goal isn't to put every customer through a rigorous identity check. Instead, you use your tools to identify the tiny percentage of transactions that are genuinely high-risk and only apply extra security measures to them.

Strategies for a Smooth and Secure Checkout

So, how do you put this into practice? You need a system that can accurately separate good customers from bad actors in real time, applying friction only when absolutely necessary.

Here’s how to build a better checkout experience:

- Implement Dynamic Friction: Use smart tools that assign a real-time risk score to each transaction. Low-risk orders are approved instantly. Only high-risk orders trigger an extra step, like a one-time password sent via SMS.

- Offer Multiple Payment Options: Giving customers choices like digital wallets (Apple Pay, Google Pay) can slash friction. These methods often have their own security built-in, making them both convenient and safe.

- Communicate Clearly: If an order gets flagged for manual review, don't leave the customer in the dark. A simple, polite email explaining you're verifying their order for their own protection can turn a potentially bad experience into a positive one that builds trust. Excellent communication is a core part of the best practices in customer service, and it absolutely applies here.

Ultimately, a secure checkout doesn't have to be a slow one. When customers feel their information is protected without having to jump through hoops, it strengthens their confidence in your brand.

The impact of getting this wrong is huge; 63% of fraud executives report higher customer churn due to fraud-related issues, while 64% see a negative impact on conversion rates. Balancing security and experience isn't just good practice—it's essential for growth.

Answering Your Top Ecommerce Fraud Questions

Diving into the world of ecommerce fraud can feel like opening a can of worms. As you start to build your defenses, questions about costs, processes, and what's actually achievable are bound to pop up. Let's tackle some of the most common questions we hear from business owners.

Getting these fundamentals right is a massive step toward creating a solid fraud prevention for ecommerce strategy that actually works.

How Much Should I Budget for Fraud Prevention Tools?

There’s no magic number here. Your budget really hinges on your sales volume, what industry you're in, and your store's overall risk profile. The good news? For many smaller businesses, the foundational tools like AVS and CVV checks are already baked into your payment processor's service, often at no extra cost.

Once you start to scale, a good rule of thumb is to set aside between 0.5% and 2% of your total annual revenue for a more robust fraud prevention solution. A great starting point is to look at your current chargeback rate. If the money you're losing to fraud is more than the cost of a prevention tool, it’s a pretty clear signal that it’s time to invest.

Many modern tools also use tiered pricing, which is great because it lets you scale your investment as your business grows.

What Is a Chargeback and How Do I Fight One?

Think of a chargeback as a forced refund. It’s a transaction reversal kicked off by a customer's bank after they dispute a charge on their statement. It doesn't just pull the money back; it also hits you with extra fees and penalties.

To fight one, you have to prove the original transaction was legit. This process is called representment, and it’s your chance to submit compelling evidence that tells your side of the story.

To successfully fight a chargeback, you'll need evidence like shipping confirmations with tracking numbers, any customer emails or chat logs related to the order, and proof of AVS/CVV matches from the transaction.

Moving fast is absolutely critical, as there are strict deadlines for submitting your evidence. You won't win every single time, especially against a determined fraudster, but keeping organized and detailed records seriously boosts your odds of reversing the chargeback. To get a better handle on this, we highly recommend you learn more about what is chargeback fraud and protect your revenue.

Can I Completely Eliminate Fraud from My Store?

In a perfect world, maybe. But in the real world, wiping out fraud entirely just isn't a realistic goal for any online business. The true aim of fraud prevention isn't elimination; it's smart risk management. The goal is to shrink fraud down to an acceptable level that doesn't tank your profitability.

Think of it this way: a 100% fraud-proof system would likely be so strict and rigid that it would block tons of legitimate customers from buying from you. You could easily end up losing more in sales than you'd ever save by stopping those few fraudulent transactions.

The key is to build a layered, intelligent strategy that maximizes security while minimizing friction for your good customers. The goal shouldn't be zero risk, but smart risk management that protects your bottom line and keeps shoppers coming back.

Ready to stop losing revenue to fraudulent chargebacks? ChargePay uses AI to automate the entire dispute process, generating winning evidence to recover your funds hands-free. See how much you can reclaim by visiting https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)