A friendly fraud chargeback is one of the biggest headaches for many business owners. It happens when a customer disputes a perfectly valid charge on their credit card, triggering a refund while they still get to keep the product or service they bought.

This isn’t like when a thief uses stolen card details—this dispute comes directly from the actual cardholder.

What Is a Friendly Fraud Chargeback

Imagine someone enjoying a full three-course meal at your restaurant, then claiming on the way out that they never got any food. Sounds wild, right? But that’s exactly what a friendly fraud chargeback is.

That "friendly" bit is misleading. It just means the dispute comes from a real customer, not a criminal with stolen identity details. But trust me, the impact on your business is anything but friendly.

These chargebacks can happen for all sorts of reasons—from honest mistakes to deliberate schemes. Figuring out these motivations is the first real step to protecting your business.

Why This Type of Chargeback Happens

Not every friendly fraud case is malicious. Plenty are accidental and stem from simple confusion. Then there are those that are full-on attempts to get something for free.

Here are the most common reasons:

- Buyer’s Remorse: The customer regrets the purchase and finds it easier to call their bank than go through your return process.

- Unrecognized Billing Descriptors: A charge shows up as something generic like "WEB SVCS INC" instead of your brand, so they assume it’s fraud.

- Family Member Purchases: A child or spouse uses the card without the owner knowing. When the bill arrives, the cardholder sees an unknown charge and disputes it.

- Forgotten Subscriptions: A free trial or recurring service renews, and the customer forgets to cancel before they dispute the charge months later.

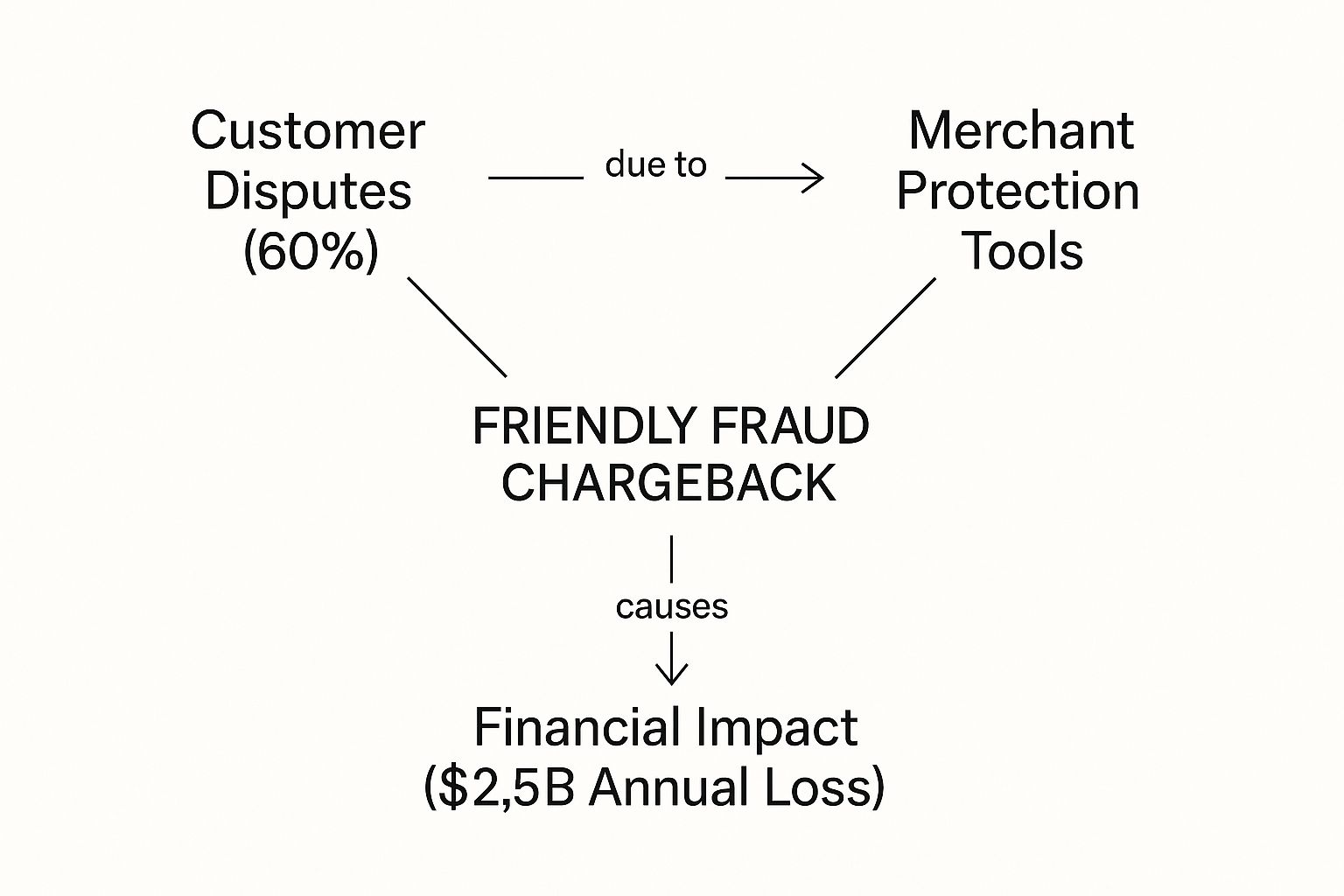

This concept map breaks down how friendly fraud works and the financial toll it takes on merchants like you.

As you can see, the volume of these disputes adds up to billions in losses every year, so having protective tools in place is crucial.

Friendly fraud, also known as first-party fraud, isn't a minor inconvenience. It's the single biggest driver of chargebacks for merchants—responsible for a staggering 70% to 79% of all chargebacks filed.

That means most of your disputes aren’t from hackers in a dark room—they’re from your own customers. To get the full picture of how it compares to outright criminal fraud, check out our guide on chargeback fraud.

Friendly Fraud vs Criminal Fraud At A Glance

Not all fraud is the same. This table breaks down the key differences.

Knowing the difference matters, because your approach for a confused customer is very different from how you fight a criminal attack.

Why Friendly Fraud Chargebacks Are a Silent Revenue Killer

A friendly fraud chargeback might look like a small hit, but it’s a hidden poison. On the surface, you lose one sale. Dig deeper, and the fallout is far worse—turning a refund into a costly, revenue-sucking nightmare.

Think of it as a chain reaction. For every dollar a customer reclaims through a friendly fraud dispute, you lose much more. The sale amount is just the start.

The True Cost of a Single Chargeback

Imagine a customer buys a $100 product from your online store. A few weeks later, they file a chargeback claiming they never received it—even though it was delivered.

Here’s how that $100 sale turns into a much bigger loss:

- The Initial Sale Amount ($100): The bank removes this money from your account.

- The Chargeback Fee ($20–$100): Your processor charges you a penalty—let’s say $40.

- Product and Shipping Costs ($60): You’re out the cost of the product and shipping.

- Operational Costs ($50+): Your team spends hours gathering proof, drafting a response, and submitting documentation.

So that $100 sale ends up costing you $250—a 150% loss. It’s more than a refund; it’s a serious financial leak. To see how deep these ripple effects go, read our article on how chargebacks hurt businesses.

The Snowball Effect on Your Business

One or two incidents might be manageable, but repeated disputes can wreck your finances. And the problem is growing: global chargeback volumes are projected to hit 261 million in 2025 and 324 million by 2028.

Beyond the direct hit, there’s a bigger danger:

A high chargeback ratio can threaten your relationship with payment processors, risking your ability to accept credit cards.

- Higher Processing Fees: You could be labeled “high-risk” and charged more per transaction.

- Account Termination: In the worst case, your merchant account gets shut down, cutting off your ability to process cards and crippling your business.

Ignoring friendly fraud is like ignoring a crack in a dam—each dispute weakens your financial foundation until it finally gives way. Fighting these disputes isn’t just about recouping a few dollars—it’s about protecting your bottom line and your future growth.

Common Triggers of a Friendly Fraud Chargeback

Friendly fraud chargebacks usually start with a small issue that boils over into a dispute. Identifying these triggers is the first step to plugging revenue leaks.

Think of them as unlocked doors. Most people pass by, but some will walk right in. Lock these doors one by one, and you’ll stop a lot of disputes before they start.

Unclear Billing Descriptors

This is one of the biggest culprits. A customer sees a charge from "WEB SVCS" or a random code and assumes it’s fraud.

They have no idea it’s just your payment processor’s default name. All they see is “unknown charge” and call their bank. Boom—you’re fighting a chargeback.

For example, a customer buys a $30 digital art print from “Creative Canvases.” A month later, their statement shows "CC ONLINE PAYMENTS LLC." They forget the purchase details and flag it as fraud, sparking a friendly fraud chargeback.

Purchases by a Family Member

A child might use a parent’s saved card details to make an in-game purchase, or a spouse might place an order and forget to mention it. When the cardholder reviews their statement, they see a charge they don’t recognize and dispute it.

These cases aren’t malicious—they’re genuine mix-ups. Learn more about this in our guide to accidental friendly fraud.

Convenience matters. One survey found 72% of cardholders admit the easy dispute process led them to file a chargeback instead of contacting the merchant first.

Forgotten Subscriptions or Trials

“Set it and forget it” subscriptions are great for revenue, but bad for memory. A free trial converts to a paid plan, the customer forgets, and then disputes the charge months later.

A Difficult Refund Process

Sometimes customers turn to chargebacks out of pure frustration. If your refund process is a maze of forms with slow replies, they’ll choose the fastest route—their bank. In these cases, a chargeback is a symptom of a poor experience, not fraud.

Common Friendly Fraud Scenarios And Solutions

Tackle these triggers, and you’ll not only fight chargebacks but build a smoother experience that keeps customers happy.

Manual Strategies to Prevent Friendly Fraud Chargebacks

It’s tempting to write off friendly fraud as an unavoidable cost. But you can stop a big chunk of these disputes before they even start with a few hands-on tactics.

It all comes down to clarity, communication, and making things ridiculously easy for your customers—like clear signs in a store that guide them straight to checkout rather than the service desk.

Polish Your Billing Descriptors

Fixing your billing descriptor is one of the fastest wins. That line on the credit card statement should instantly remind customers of their purchase.

Checklist for a great descriptor:

- Use Your Brand Name: Lead with the name they know (e.g., "COZY KNITS").

- Add a URL: If space allows, include something like "COZYKNITS.COM".

- Include a Phone Number: Gives customers a direct line to you instead of the bank.

Craft Simple and Clear Policies

If your return policy is buried in legalese, customers will skip it and call their bank. Make your policies obvious, fair, and painless. If a refund from you is easier than a chargeback, disputes drop.

Merchants lose not only the sale but also face fees and costs up to $70 per dispute. With only an 18% net recovery rate on successful disputes, prevention is always better.

Send Timely and Detailed Confirmations

Every email you send is a chance to remind customers what they bought and build trust.

Essential emails:

- Order Confirmation: Immediate, with an itemized list, total cost, and your clear brand name.

- Shipping Confirmation: Include tracking number and link so they can follow their package.

These messages create a paper trail. If they forget the purchase, these reminders jog their memory and stop them from disputing.

Offer Responsive and Accessible Support

Top-notch customer service is your best defense. Make your contact info impossible to miss—footer, contact page, and in every confirmation email. A quick chat can solve issues before they become disputes.

Using proactive customer feedback collection tools helps you catch problems early and shows customers you’re listening.

Automating Chargeback Disputes with ChargePay

Manual tactics are critical, but they can feel like plugging holes in a leaky bucket. As orders grow, managing every interaction by hand eats up time and energy.

That’s where automation comes in. It doesn’t replace your smart manual work—it supercharges it, acting like an assistant that never sleeps, never errs, and handles all the paperwork in seconds. That frees your team to focus on growth, not disputes.

How Automation Elevates Your Defense

Winning a friendly fraud chargeback is all about timely evidence. Manually, you scramble to find proof—emails, order details, delivery confirmations. It’s messy and often incomplete.

Automation, using tools like ChargePay, changes the game. Instead of you chasing evidence, the system pulls it all together instantly.

The moment a chargeback is filed, an automated system can bundle all necessary proof into one compelling package, eliminating human error and stress from the process.

Now you’re not just reacting—you’re always ready.

The ChargePay Advantage

ChargePay handles the entire dispute lifecycle, turning a multi-step headache into a hands-off process. It hooks up to your payment platforms and gathers the critical data you need to win.

It automatically collects:

- Delivery and Tracking Confirmations: Pulls shipping details and proof of delivery from carriers like USPS, FedEx, and UPS.

- Customer Communications: Finds and includes relevant emails or support tickets.

- IP Logs and Geolocation Data: Shows purchases made from the customer’s usual location.

- Order and Billing Information: Compiles AVS/CVV checks and confirms matching addresses.

With these elements, ChargePay builds a robust response formatted precisely for Visa, Mastercard, and other card networks. Check out our complete guide to automated chargeback management for more details.

Giving You Back Time and Revenue

The biggest benefit isn’t just higher win rates—it’s time saved. Instead of hours spent on admin, your team can focus on marketing, product development, and building customer relationships.

Pair your manual prevention tactics with automation, and you’ve got a powerful, two-pronged defense: fewer disputes to fight, and the best possible chance to win the ones that slip through.

How to Protect Your Business

Tackling friendly fraud doesn’t mean overhauling everything. A few targeted tweaks can have a huge impact on your margins.

First, clarity: make sure your billing descriptors are unmistakable—your brand name front and center so customers know who’s charging them.

Then, smooth out the customer experience:

- Make Refunds Easy: Getting a refund from you should be simpler than filing a chargeback.

- Communicate Early and Often: Send detailed order and shipping confirmations right away.

- Be Easy to Reach: Don’t hide your contact info—make live chat or phone support a click away.

Think of friendly fraud as a manageable business challenge, not an inevitable cost. Stay vigilant and use automation to handle the disputes that still slip through.

If you want a broader look at fraud patterns and how they vary by region, our research on Americas Fraud Capitals is worth exploring.

FAQ

Here are clear answers to the most common questions merchants have about friendly fraud chargebacks.

Is It Illegal to Commit Friendly Fraud

Friendly fraud sits in a gray zone, but disputing a valid purchase is considered wire fraud. Convincing a bank to reverse a legitimate payment technically breaks the law.

Banks rarely take these cases to criminal court—intent is hard to prove—so they stay in the civil chargeback system. Your best defense is a strong paper trail: order confirmations, shipment records, and customer communications.

Will I Get My Money Back if I Win a Chargeback Dispute

Yes. If you win your representment, the bank returns the original transaction amount to your merchant account.

Remember, though, the non-refundable chargeback fee you paid stays with the bank. That’s why stopping a chargeback before it hits often saves you more than any successful appeal.

Recovering the sale is great, but avoiding the fee and the back-and-forth headache is even better.

Can I Block Customers Who File Friendly Fraud Chargebacks

Absolutely. Think of it as a bouncer at your checkout. Flag or blacklist repeat offenders in your ecommerce platform or payment gateway. That cuts off a major source of losses and discourages serial chargeback abusers.

How Quickly Do I Need to Respond to a Chargeback

Missing the deadline is like missing a tax payment—late means lost. Card networks typically give you 20 to 45 days to submit your evidence.

Let the clock run out by even one day and you forfeit the dispute. Automated tools help track deadlines so your response goes in on time, every time.

Stop letting friendly fraud drain your revenue. ChargePay fights and wins your chargeback disputes automatically, recovering up to 80% of lost funds without you lifting a finger. See your potential recovery at ChargePay.

.svg)

.svg)

.svg)

.svg)