So, you're wondering how long a chargeback will tie up your revenue and demand your attention?

Let's get right to it. The short answer is anywhere from a few weeks to several months, but you can typically expect most disputes to wrap up within 60 to 90 days. Think of it like a package making its way through multiple shipping hubs—each stop on the journey adds time.

The Real Answer to How Long Chargebacks Take

When a customer disputes a charge, it kicks off a formal process that loops in multiple parties, from your bank to their bank and the card networks themselves. This isn't like a simple refund you handle directly. It's a multi-stage journey, and each step has its own clock. Getting a handle on these phases is the first step to setting realistic expectations.

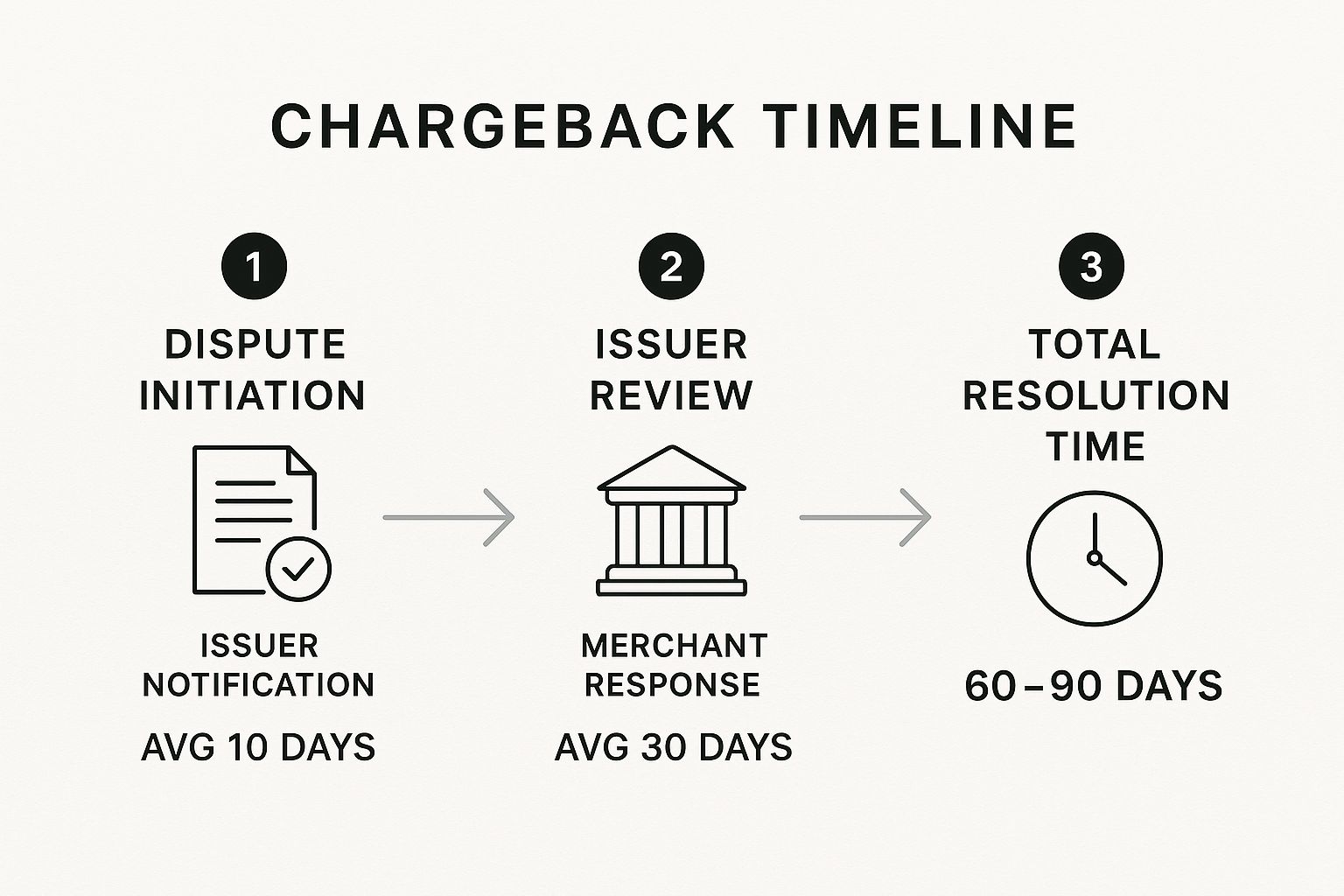

This visual breaks down what that journey looks like and how long each stage usually takes.

As you can see, the total resolution time often stretches to two or three months. A big chunk of that time is dedicated to the issuing bank's review and the window you have to respond.

For a clearer picture, let's break down the key stages and their typical timeframes in a simple table.

A Quick Look at the Chargeback Timeline

This table gives you a simplified view of the chargeback process, offering a quick reference for what’s happening at each step and how long it might take.

This timeline shows that from start to finish, the process is built to give every party enough time to investigate and respond, which is why it can feel so drawn out.

All in all, the entire lifecycle from the initial dispute to the final decision can easily take 30 to 90 days—and sometimes even longer if the case gets complicated or escalates. For merchants, these long waits create operational headaches and uncertainty around cash flow.

Ultimately, these timelines aren't just random waiting periods. They are governed by strict rules set by the major card networks, which dictate the official chargeback time limit for each stage of the process.

Navigating the Chargeback Process Step by Step

Now that you have the big picture, let’s zoom in on the actual journey a dispute takes. Knowing how long chargebacks take really comes down to understanding the path they travel. The process can feel a little complicated, but it’s mostly just a series of handoffs between a few key players.

Think of it like a relay race. The baton—your customer’s dispute—is passed from one runner to another, and each leg of the race has its own set of rules and timelines.

The Key Players and Their Roles

First, let's meet the team involved in every single chargeback. Each one has a specific job to do, and that's what shapes the overall timeline.

- The Cardholder: This is your customer, the person who kicks the whole thing off by disputing a charge with their bank.

- The Issuing Bank: This is the cardholder's bank (think Chase, Bank of America, etc.). They take the first look at the dispute and decide if it’s valid enough to move forward.

- The Acquiring Bank: This is your bank, the one that processes your credit card transactions. They get the chargeback notice from the issuing bank and pass it along to you.

- The Card Network: Picture Visa or Mastercard here. They act as the referees, setting the rules and deadlines that everyone has to play by. You can dive deeper into the specific steps in our guide on the Visa chargeback process.

- You, the Merchant: Your job is to step up and respond with solid evidence to prove the original transaction was legitimate.

This flow chart gives you a great visual of how these players interact, from the initial dispute all the way to the final resolution.

As you can see, there’s a lot of back-and-forth communication. It’s this multi-step validation between banks and networks that makes the whole thing take weeks, or even months, to sort out.

The Step-by-Step Breakdown

The entire process unfolds in a very specific sequence, and each step is on the clock.

A chargeback begins the moment a customer contacts their bank. From that point on, a timer starts ticking. Typically, you’ll have between 20 to 45 days to respond once you’re notified, but this can vary depending on the card network.

- Dispute Initiation: The cardholder calls their bank to dispute a charge. Simple as that.

- Issuer Review & Provisional Credit: The issuing bank reviews the claim. If it looks legit, they often give the customer a provisional credit while they investigate.

- Chargeback Notification: The dispute travels through the card network to your acquiring bank. They then notify you and pull the disputed amount from your account.

- Merchant Response (Representment): This is your shot to fight back. You’ll need to submit compelling evidence to make your case.

- Final Decision: The issuing bank reviews your evidence and makes the final call. If they side with you, the funds are returned. If not, the provisional credit to the customer becomes permanent.

Why Some Chargebacks Drag On for Months

Ever had one chargeback wrap up in a few weeks, while another seems to stick around forever? You're not alone. While it’s nice to think about an "average" timeline, the reality is that a few key factors can seriously stretch out the process, turning a simple dispute into a months-long headache.

Think of it like a detective case. A straightforward, open-and-shut case gets solved quickly. But one with conflicting stories, messy evidence, and lots of back-and-forth? That’s going to take a much longer investigation. The same idea applies here.

The Reason Code Dictates the Timeline

Not all disputes are created equal. The reason a customer files a chargeback is probably the biggest factor in how long the chargeback will take. Different reason codes demand different kinds of evidence from you, which completely changes how complex the bank's investigation will be.

- Fraud Claims: When a customer claims a transaction was "unauthorized," you're typically asked to provide technical proof. Think IP addresses, AVS verification codes, and CVV matches—data points to prove the real cardholder was involved.

- Service Disputes: On the other hand, claims like "product not received" or "product not as described" are way more complicated. Now you're on the hook for proof of delivery, tracking numbers, original product descriptions, and copies of customer emails. Just gathering all that documentation takes more time.

A fraud claim can often be proven or disproven with hard data. But a dispute over service quality can easily spiral into a drawn-out "he said, she said" scenario, tacking weeks onto the timeline.

Responsiveness and Escalations

A chargeback’s timeline also depends heavily on how quickly everyone involved gets their act together. Any delay—whether from the customer, their bank, your bank, or even you—can stall the entire process. If any party misses a deadline to submit information, everything grinds to a halt.

And it gets longer if your initial response (your representment) is denied. If you're confident you have a solid case, the dispute can be escalated.

The next stage is often pre-arbitration, a final attempt to resolve the issue before it goes to the card network for a binding ruling. This step alone can add another 30 days or more to the process.

This escalation adds a whole new layer of review and communication, guaranteeing a much longer wait. If you want to get a better handle on this part of the process, you can read more about pre-arbitration in our detailed guide: https://www.chargepay.ai/blog/pre-arbitration

It’s also worth noting that higher-value transactions tend to get a closer look. For instance, the U.S. has the highest average chargeback value at $110. These larger disputes naturally trigger more detailed investigations from the banks, which extends the resolution time for everyone involved.

How Industry Affects Chargeback Timelines

A chargeback isn't a one-size-fits-all problem. So, when people ask, "how long do chargebacks take?" the honest answer is... it depends. A huge factor is your industry, as some business sectors are just naturally magnets for complex, drawn-out disputes.

Your specific business model has a direct line to the kinds of claims you’ll face and the evidence you'll need to dig up to fight them.

For instance, high-risk industries like travel and hospitality often get stuck with longer resolution times. Think about it: a dispute over a canceled flight or a disappointing hotel stay is rarely simple. It often requires a mountain of documentation, which means more back-and-forth between the banks.

Where Timelines Differ Most

Certain industries just have unique hurdles that can really stretch out the chargeback process. It all comes down to the nature of what’s being sold.

- E-commerce and Digital Goods: Proving you delivered a software key or in-game item is a lot trickier than showing a tracking number for a physical package. That gray area can drag out an investigation.

- Subscription Services: Disputes here are often about recurring billing. Customers might claim they canceled or didn't authorize a charge, forcing you to pull up their entire history with your service.

- High-Value Items: It's simple, really. Big-ticket purchases get more attention from the banks. They’ll spend more time poring over the evidence from both sides, which slows everything down.

And this isn't slowing down. Recent data showed a mind-boggling 816% rise in travel and lodging chargebacks in Q1 2024 compared to last year. E-commerce wasn't far behind, with disputes jumping 222%, often fueled by friendly fraud. You can see more on these chargeback statistics on chargeback.io.

These industry-specific headaches mean your average timeline could look totally different from a business in another field. The unique challenges of digital assets, for example, are a big reason we're seeing a spike in chargebacks in the gaming industry.

Knowing these nuances ahead of time is half the battle. It helps you get ready for the specific kinds of disputes you're most likely to see.

Actionable Steps to Speed Up Resolutions

Feeling stuck in the chargeback waiting game is incredibly frustrating. But you have more control over the timeline than you might think. While you can't exactly force the banks to move faster, you can take practical steps to sidestep some disputes and definitely speed up the ones that do happen. The whole game is about being proactive, not reactive.

It all starts long before a dispute is even filed. A few simple preventative measures can stop many chargebacks in their tracks, completely eliminating the long, painful wait for a resolution.

Prevent Disputes Before They Start

Let's be honest: the fastest chargeback is the one that never happens. Putting a few key strategies in place can seriously cut down on the number of disputes you receive, which directly shortens the total time your team spends putting out these fires.

- Use Clear Billing Descriptors: Ever looked at your own credit card statement and thought, "What on earth is that charge?" Your customers do it too. A confusing descriptor like "WEB SVCS" instead of "YourStoreName" is a super common trigger for disputes. Make it obvious who you are.

- Implement Simple Fraud Tools: You don't need a fortress, just a locked door. Basic security checks like Address Verification Service (AVS) and CVV verification are essential. They help confirm the person making the purchase is the actual cardholder, which is your first line of defense against true fraud chargebacks.

Respond with Speed and Precision

When a chargeback inevitably lands in your lap, how you react is everything. A fast, well-organized reply doesn't just improve your odds of winning; it can also trim unnecessary days or weeks off the process.

The single most important rule is to never miss a deadline. Card networks give you a specific window to respond—often somewhere between 20 and 45 days. If you miss it, you automatically lose. No appeals, no second chances.

To build a strong case quickly, you need to zero in on compelling evidence that directly shuts down the customer’s claim. If they say "product not received," your job is to show up with tracking numbers and proof of delivery. A vague response won't cut it.

This is where understanding the art of chargeback representment can be the difference between a quick win and a drawn-out, painful loss. When you act decisively and arm yourself with solid proof, you shorten the time your revenue is trapped in limbo.

Wrapping Up: How to Take Control of Chargeback Timelines

So, when you're wondering how long a chargeback takes, the real takeaway is that you're not just a bystander. While the whole affair can drag on for one to three months, your actions play a huge role in that timeline.

Think of it less as a fixed waiting period and more as a series of stages. The speed of each stage depends on the dispute reason, how quickly the banks move, and—most importantly—how solid your evidence is. A sharp, well-documented response can stop a dispute from escalating and getting stuck in limbo.

Ultimately, you want to turn a process that feels out of your control into something you can actively manage. Here’s a quick final checklist to keep timelines short:

- Prevent Them First: Use crystal-clear billing descriptors so customers recognize your charges instantly.

- Move Fast: Never, ever miss a representment deadline. Time is not on your side.

- Bring the Receipts: Tailor your evidence to the specific reason code. One size does not fit all.

Focusing on these key areas gives you the best shot at a faster, more favorable outcome. It’s how you keep your revenue where it belongs and your business running without unnecessary bumps in the road.

Frequently Asked Questions

Got a burning question about how long chargebacks really take? Let's jump into some of the most common things merchants ask us about the process and its timelines.

Can a Chargeback Be Resolved in Under 30 Days?

It can, but it's not the norm for the full, formal dispute. A super-fast resolution usually happens in a couple of specific scenarios: you might decide to accept the dispute right away, or the customer might have a change of heart and withdraw their claim.

There's also a quicker path using pre-dispute alerts. These tools give you a heads-up before a formal chargeback is filed, letting you issue a refund and settle things in just a few days.

What Is the Longest a Chargeback Can Take?

Strap in for this one. A really messy, complex chargeback can drag on for six months or even longer. This is what happens when a dispute goes all the way to arbitration.

Think of arbitration as the final showdown where the card network—like Visa or Mastercard—steps in to make the final, binding call. These marathon disputes are pretty rare, but they can pop up, especially with high-value sales or claims where both sides are digging in their heels.

Does the Card Network Affect the Timeline?

Absolutely. Each card network plays by its own rulebook. Visa, Mastercard, and American Express all have their own specific deadlines and procedures.

For example, the window a customer has to file a dispute might be different from one network to the next, and so will the time you have to respond. While the overall stages are similar, these little variations in the rules can definitely stretch or shorten the timeline.

Tired of the waiting game? ChargePay uses AI to automate the entire dispute process, helping you win more chargebacks and get your revenue back faster. See how it works at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)