When you find a suspicious charge on your credit card statement, it's easy to feel like you're in for a fight. But here's the thing: you have more power than you think. The key to winning is understanding the game and building a rock-solid case from the get-go. It all comes down to knowing why you're challenging the charge and laying out your evidence clearly for your card issuer.

Your Action Plan For A Winning Dispute

Seeing a charge you don't recognize is frustrating, but don't panic. The system is actually set up to protect you, and if you have a clear strategy, you can navigate it successfully. Think of this as your playbook—we're going to demystify the entire process so you can challenge any bogus charge with total confidence.

Your very first move is to figure out exactly what kind of problem you're dealing with. This isn't just about picking the right category; it frames your entire argument.

Fraudulent Charges vs Billing Errors

Is the charge from a merchant you've never even heard of? That’s almost certainly fraud. This is what happens when a thief gets ahold of your card details and goes on a shopping spree. Your job is simple: report it immediately. Your bank will shut the card down and go after the criminal activity.

But what if the charge is from a place you know, but the amount is off? Or maybe a promised refund never showed up, or the product you received was a dud. That's a billing error. In this case, your beef is with the merchant's mistake or failure to deliver, not with a random crook.

Making this distinction is critical because it helps you tell the right story to your credit card company.

The Fair Credit Billing Act (FCBA) is your best friend here. It gives you the legal firepower to dispute billing errors. And the system works—one study found that nearly 96% of consumers win their most recent dispute when they use the process correctly.

Know Who Is Involved

To come out on top, you need to understand the three main players in this little drama:

- You (The Cardholder): Your role is to act fast, gather your proof, and present the facts clearly. No emotion, just evidence.

- The Merchant: They get a chance to defend the charge by providing their own evidence to prove it was legit.

- Your Card Issuer: The bank is the referee. They look at the evidence from both sides and make the final call.

By getting a handle on these roles and the type of dispute you're filing, you're already setting yourself up for a much better outcome. For a deeper look at the tactics involved, our guide on how to win a credit card dispute has even more detailed strategies. Next up, we'll get into the nitty-gritty of building your case with solid proof.

Gathering Evidence to Build Your Case

Let's be blunt: a successful dispute isn't won with strong feelings; it's won with cold, hard facts. You need to think of yourself as a detective building a case file. Your goal is to hand the credit card issuer a neat, organized package of proof so compelling that they have no choice but to rule in your favor.

This goes way beyond just digging up the original receipt. You need to document everything related to the transaction and, just as importantly, your attempts to resolve the problem with the merchant first. The more relevant details you provide, the harder it is for the merchant to poke holes in your story.

Your Essential Evidence Checklist

Every dispute is unique, so the exact evidence you need will change depending on the situation. That said, a few key documents form the foundation of almost any solid case. Your first move should be to gather digital or physical copies of everything you can find.

Here’s a practical checklist to get you started, broken down by common dispute types:

- For "Item Not as Described": Start by taking screenshots of the original product listing, highlighting every promise the merchant made. Then, grab your phone and take clear photos or videos of the item you actually received. Show exactly how it fails to live up to the description.

- For "Duplicate Charge": This one is usually pretty straightforward. All you need is a copy of your credit card statement clearly showing the two identical charges, including the transaction dates, merchant names, and amounts.

- For "Services Not Rendered": Pull together any contracts, service agreements, or email correspondence that outlines the scope of work. Just as crucial, include any communication showing you tried to follow up with the provider to find out what was going on.

No matter the reason, keeping a detailed log of every single interaction with the merchant is a game-changer. Note the date, time, who you spoke with, and a summary of what was discussed. This log is powerful because it proves you made a good-faith effort to resolve the issue directly before escalating.

Documenting Digital and Service-Based Disputes

Proving a problem with a physical item is one thing, but what about digital products or services that never materialized? The key is to capture evidence that clearly shows a failure to deliver on a promise. This is where you might need to get a bit more creative.

For a buggy software subscription, for example, you could take screen recordings of the glitches or errors you're experiencing. If a marketing agency didn't deliver the promised results, you can use their own lackluster reports (or lack thereof) against them as proof.

Key Takeaway: Your evidence needs to tell a clear, chronological story. Start with the initial purchase, show the problem, and end with your attempts to get it fixed with the merchant. An organized file makes it painfully easy for the bank’s investigator to see the facts.

Once you compile all this evidence, you'll need to present it clearly, often by writing a summary of your case. For guidance on structuring this all-important document, our article on creating an effective rebuttal letter provides an excellent starting point.

Ultimately, the goal is to leave zero room for doubt. If you can show the card issuer exactly what went wrong with clear, undeniable proof, you've already dramatically increased your odds of winning. A well-prepared case file is your single most powerful tool in this process.

How to File Your Dispute Correctly

You've done the legwork, gathered your evidence, and built a solid case. Now it’s time to make it official and submit your claim. How you file your dispute is just as important as the proof you’ve collected. A clear, factual, and professional submission makes it much easier for the bank's investigator to understand your side and, hopefully, rule in your favor.

The key is to present your case without letting emotion take over. It’s easy to get frustrated, I get it. But sticking to the facts will make your argument infinitely stronger. Think of it less as telling a story and more as presenting a logical argument backed by the evidence you already have in hand.

Choosing Your Filing Method

Most banks give you a few different ways to kick off a dispute, and each has its pros and cons. You’ll want to pick the one that best suits your situation and helps you present your evidence most effectively.

- Online Portal: This is almost always the fastest and most efficient way to go. You can upload your documents directly, and you get an instant digital record of your submission. It’s perfect if all your proof is already in a digital format.

- By Phone: Talking to a real person can be helpful for clarifying details, but it's a pain for submitting evidence. If you go this route, always follow up the call with a written summary and make sure you get a case reference number.

- Certified Mail: A formal letter is the old-school approach, but it has its place. It creates a serious paper trail and is often recommended by the Federal Trade Commission, even if you’ve already filed online. This method just adds a layer of official seriousness to your claim.

Stating Your Case Clearly and Factually

When you write your dispute summary, get straight to the point. Start with the basics: the transaction amount, the date, and the merchant’s name. From there, give a concise, step-by-step account of what happened. You have to resist the urge to use angry or emotional language—it just distracts from the facts.

Your goal is to be persuasive, not confrontational. A calm, logical explanation backed by your neatly organized evidence is your best shot at winning a dispute with your credit card company.

Pro Tip: Keep a copy of everything you submit—the dispute form, any letters, all of it. Having your own complete file is a lifesaver if you need to follow up or appeal a decision later on.

And remember, you're not alone in this. In 2023, U.S. consumers disputed a staggering 105 million credit card charges, worth an estimated $11 billion. That number is only expected to climb, which shows just how common it is for people to challenge incorrect charges. You can see more data on this trend in the full Wall Street Journal report.

Avoiding Common Filing Mistakes

Even with rock-solid evidence, simple mistakes can completely derail your claim. One of the biggest pitfalls is missing the deadline. Under the Fair Credit Billing Act (FCBA), you generally have 60 days from the statement date to file your dispute, so don’t wait.

Another common error is submitting an incomplete claim. Before you hit send, double-check that you've included all your evidence and filled out every single required field on the form. Leaving out one key detail can cause unnecessary delays or even get your claim denied outright. For a deeper dive into the mechanics of this process, check out our guide on how to fight a chargeback.

Navigating the Process After You File

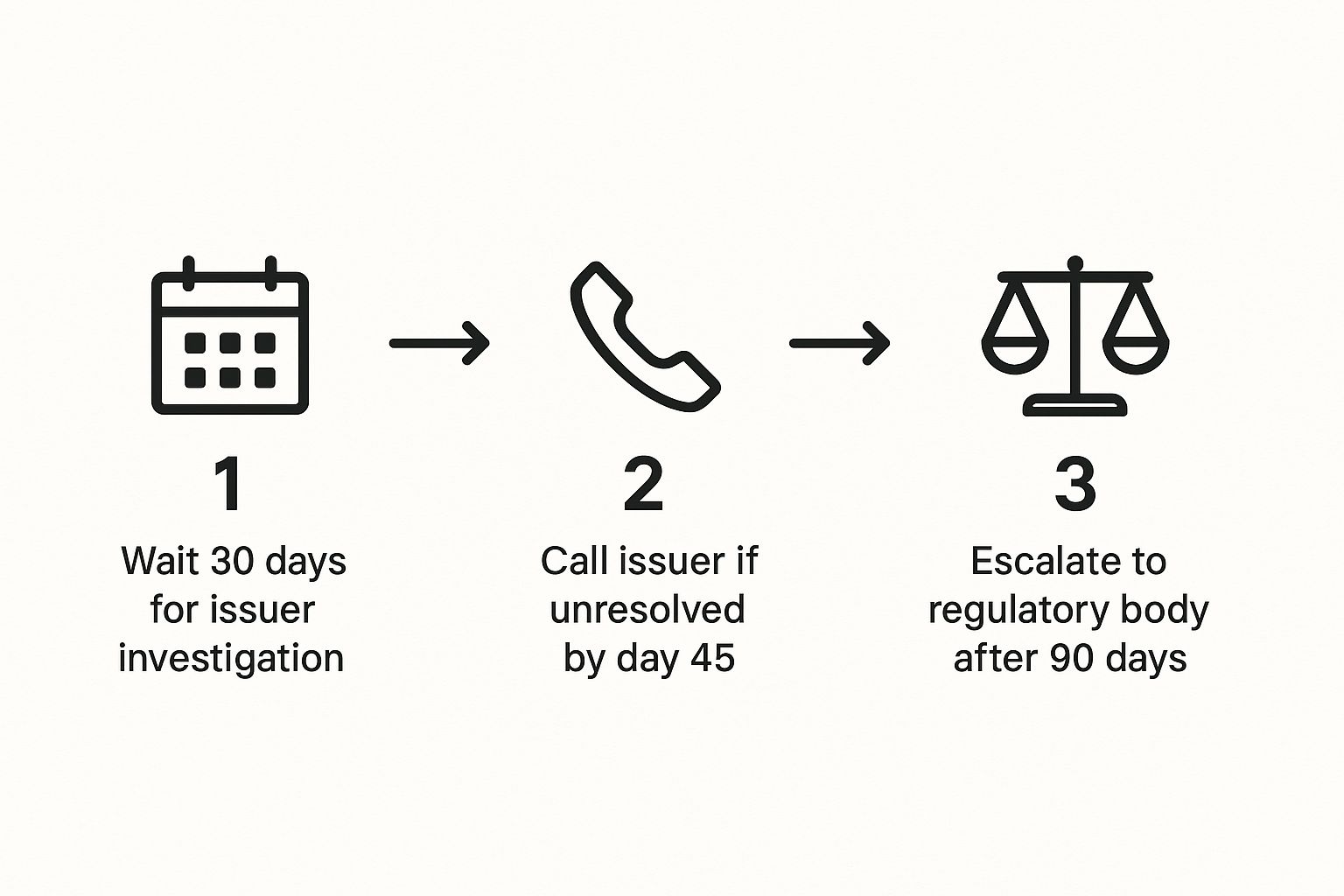

You've gathered your evidence and officially filed the dispute. It's tempting to breathe a sigh of relief and just wait it out, but your job isn't quite done yet. Staying proactive is a huge part of learning how to win a credit card dispute. Think of it this way: the game isn't over; it's just moved into the investigation phase, where your bank is the referee between you and the merchant.

This is where the clock starts ticking on their end. By law, your credit card issuer has to acknowledge your dispute within 30 days. From there, they have two billing cycles (but no more than 90 days) to resolve the whole thing. During this window, the merchant gets their chance to argue that the charge was legitimate.

What Happens Behind the Scenes

While you're waiting, you'll probably see a provisional credit pop up in your account for the disputed amount. It’s a nice sight, but don't treat it as a final win just yet. This is a temporary courtesy from the bank. If you ultimately lose the dispute, they'll reverse that credit, and you’ll be on the hook for the charge again.

Meanwhile, the merchant is busy building their own case. They'll be submitting any proof they can find—things like delivery confirmations, signed receipts, or even IP address logs from online purchases. This is exactly why your initial evidence needs to be so solid; you're essentially preempting their arguments. Understanding the other side's playbook can give you a real edge. You can learn more about how often merchants actually win chargeback disputes to get a sense of what you're up against.

This graphic gives you a solid timeline for keeping your dispute on the radar.

The key takeaway here is a mix of patience and persistence. You need to give the process time to work, but you can't just let your case fall through the cracks.

When and How to Follow Up

Being organized and politely persistent shows your card issuer you’re serious about this. It's not about pestering them; it’s about making sure your case doesn’t get lost in the shuffle.

Pro Tip: Whenever you call to follow up, have your case number ready. It’s a simple thing, but it saves everyone time and helps the customer service rep pull up your file instantly. It makes the whole conversation smoother.

Here's a simple, proactive follow-up schedule I recommend to keep things moving without being annoying. Staying organized is half the battle, and a good checklist can be your best friend during this waiting game.

Your Dispute Follow-Up Checklist

This checklist isn't about rushing the bank—it's about making sure you're an active participant in the process. A little bit of organized persistence can make a world of difference in the final outcome.

What to Do If Your Dispute Is Denied

Getting that denial letter feels like hitting a brick wall. But here's a secret from my years in this space: a denial is often just the beginning of the next phase, not the end of the road. Don't give up. It’s time to get strategic and push back with a well-planned appeal.

Your first move is to figure out why you lost. The bank is required to send you a written explanation for their decision. This letter is your new roadmap. It will spell out the specific reasons for the denial and, crucially, reference the evidence the merchant provided to win them over.

Requesting the Merchant's Evidence

You have every right to see the exact proof the merchant used against you. Get on the phone with your card issuer and formally request a copy of all the documentation they received from the merchant. This could be anything from a signed receipt and delivery confirmation to website usage logs.

Once you have their evidence in hand, you can build a targeted rebuttal. Did they provide a delivery confirmation? Great. Your new argument can point out that the package was left at the wrong address or that the signature clearly isn't yours. This is your chance to directly counter their claims, point by point.

It’s worth noting that businesses put up a fight. In fact, businesses that contest chargebacks win about 45% of the time. Interestingly, their success often depends on the transaction size; they win nearly 47% of disputes for small purchases under $30 but only about 28% for high-dollar transactions over $300. You can learn more about these chargeback statistics on Chargeback.io.

When to Escalate to a Regulatory Body

If your appeal to the credit card company also gets shot down, it's time to bring in the heavy hitters. You can—and absolutely should—file a formal complaint with the Consumer Financial Protection Bureau (CFPB). The CFPB is a government agency designed specifically to protect consumers like you.

Filing a complaint is a serious step that gets your bank’s attention, fast. The process is straightforward and can be done entirely online. You'll explain your situation, upload your evidence, and detail the steps you’ve already taken. The CFPB then forwards your complaint to the financial institution, which is legally required to respond.

Filing with the CFPB isn't just venting; it's a formal escalation that forces your bank to take a second, much more serious look at your case. Many consumers find that a previously unresponsive bank suddenly becomes much more cooperative once the CFPB is involved.

This process adds a powerful layer of oversight to your dispute. Sometimes, this is the final push needed to turn a denial into a win. And if you suspect the initial charge was a case of deliberate deception, it's also helpful to understand the nuances between friendly fraud versus chargeback fraud as you build your case.

Your Top Credit Card Dispute Questions, Answered

Even with the best game plan, it's natural to have a few questions rattling around. When you're in the thick of it, some common "what ifs" and "how longs" always seem to pop up. Let's get those cleared up right now.

Think of this as your personal FAQ for the dispute process. Getting these details straight will give you the confidence to see your claim through to the end.

How Long Do I Have to File a Dispute?

This is probably the most critical question, and the answer comes straight from federal law. Thanks to the Fair Credit Billing Act (FCBA), you have 60 days to dispute a charge.

Now, here's the important part: that 60-day clock starts ticking from the day your credit card statement with the error was mailed to you, not from the date you actually made the purchase.

My advice? Don't wait. The faster you act, the more seriously your claim is taken and the easier it is to pull together fresh, convincing evidence. While some card companies might give you more time, treating that 60-day window as a hard deadline is your safest move.

Will a Dispute Hurt My Credit Score?

Let's put this worry to rest: filing a legitimate credit card dispute will not hurt your credit score. Not one bit. This process is a consumer right, and you’re never penalized for using the protections you’re entitled to.

While the bank is investigating, you don't have to pay the disputed amount or any interest that piles up on it. The issuer can't report that specific charge as delinquent or send it to collections.

Just remember to pay the rest of your bill on time. Any charges you aren't disputing are still your responsibility, and missing those payments will absolutely ding your score.

Key Takeaway: The dispute process is designed to protect you, not punish you. As long as you follow the rules and pay the undisputed portion of your balance, your credit score is safe.

Is a Dispute the Same as a Chargeback?

You’ll hear people use these terms as if they're the same thing, but they're actually two different stages of the process. Getting the lingo right helps you understand where you are in the journey.

Here’s a simple way to think about it:

- A dispute is what you file. It’s the initial step where you raise your hand and tell your card issuer, "Hey, something isn't right with this charge."

- A chargeback is what the bank does. After investigating your dispute and finding it valid, the bank executes the chargeback—forcefully reversing the transaction and pulling the money from the merchant's account back into yours.

So, you file a dispute with the goal of getting a chargeback. Winning your dispute is the trigger that makes the chargeback happen and gets your money back for good.

For businesses struggling with the complexities of managing disputes, ChargePay offers a hands-free solution. Our AI-powered system automates the entire chargeback representment process, recovering lost revenue without any manual effort on your part. Stop losing money to fraudulent claims and operational headaches. Discover how ChargePay can boost your win rates and protect your bottom line.

.svg)

.svg)

.svg)

.svg)