A chargeback notification can feel like a direct hit to your bottom line, but a well-crafted response is your best defense. That response comes in the form of a letter of rebuttal—the single most important tool you have to fight back, present your side of the story, and reclaim revenue from unfair claims.

Think of it as your formal, evidence-backed argument explaining exactly why a chargeback should be reversed.

Why Mastering Rebuttal Letters Is a Must

When that dispute email lands in your inbox, it's easy to feel frustrated. You made a sale, shipped the product, and did everything right, yet your money is suddenly yanked from your account. This isn't just about losing the sale amount, either. Chargebacks pile on added fees that can quickly chew through your profits.

These disputes don't just happen randomly. They almost always fall into a few common buckets that every online merchant eventually deals with.

The Real Reasons Behind Disputes

Getting a handle on why chargebacks happen is the first step toward fighting them effectively. While some are legitimate, many are anything but.

- Legitimate Customer Issues: A customer might file a dispute if they genuinely didn't receive an item, the product arrived damaged, or it was completely different from what they ordered. These are often preventable with clear communication and solid fulfillment.

- True Fraud: This is when a stolen credit card is used for a purchase. As the merchant, you're usually not at fault, but you're still on the hook for the financial loss unless you can prove the transaction was legitimate.

- Friendly Fraud: This is the most maddening type. It's when a customer buys something, receives it, and then files a chargeback claiming they never authorized it or didn't get the item. They essentially get your product for free, and it's a massive, growing problem for online businesses.

A strong letter of rebuttal acts as your official statement to the bank. It turns a messy "he said, she said" situation into a clear, evidence-based case that separates fact from fiction and gives you a real shot at winning your money back.

The Financial Stakes Are Higher Than You Think

A single chargeback costs a lot more than just the original sale. When you factor in the non-refundable processing fees, the chargeback fee from your processor, and the operational cost of your team's time, the real price tag gets ugly, fast.

Here’s a quick breakdown of how those hidden costs can stack up.

The True Cost of a Single Chargeback

Ignoring chargebacks or just firing off weak responses is a costly mistake. The numbers don't lie: Mastercard's 2025 State of Chargebacks Report found that while merchants challenge 54% of disputes, they only win about 20% of them. Meanwhile, card issuers win 75% of the time.

That gap represents a massive opportunity. With global chargeback volumes expected to hit 324 million by 2028, getting good at this is something you just have to do.

Improving your win rate isn't about luck—it's about strategy. By understanding why disputes happen and presenting a clear, evidence-backed case, you can dramatically improve your odds. You can find more insights by reading our article on how often merchants win chargeback disputes. This guide will show you exactly how to do it.

The Anatomy of a Winning Rebuttal Letter

Let's move from theory to action. A winning rebuttal letter isn't just a quick email you fire off; it's a structured, professional document designed to persuade a bank investigator. You have to think of it like building a small legal case—every word and piece of evidence must support your claim without overwhelming the reader.

The person reviewing your case is likely sifting through dozens, if not hundreds, of disputes a day. Your single most important job is to make their job easier. Present a clear, logical, and undeniable argument. A jumbled, emotional, or confusing letter will almost certainly get tossed aside, no matter how strong your evidence actually is.

Start with a Clear and Concise Summary

Your opening paragraph is the most crucial part of the entire letter. Don't bury the lead. It needs to immediately state why you're writing and summarize exactly why the chargeback is invalid.

Get straight to the point. This opening needs to include:

- The original transaction date and amount.

- The chargeback case number for reference.

- A direct statement addressing the customer's claim (the reason code).

- A quick summary of the evidence you're providing to shut it down.

For instance, if the chargeback reason is "Product Not Received," your opening should state that you're contesting the dispute and have attached proof of delivery, complete with a tracking number and signature confirmation. This immediately frames the argument and tells the reviewer exactly what to look for in your evidence package.

A strong opening acts as a roadmap for the bank investigator. By clearly stating your position and referencing your key evidence upfront, you guide them toward the conclusion you want them to reach—that the chargeback is illegitimate.

Present Your Evidence in a Logical Flow

After the summary, the body of your letter of rebuttal needs to present your evidence in an organized way. This isn't the place to just dump a folder of random files and hope for the best. You need to walk the investigator through your proof, piece by piece, explaining how each document methodically builds your case.

Use bullet points or a numbered list to outline each piece of evidence you're submitting. Make sure to clearly label your attachments (e.g., "Attachment A: Order Invoice," "Attachment B: Delivery Confirmation") and reference them directly in your letter.

Example Evidence Flow:

- Order Details (Attachment A): Start by proving a legitimate order was placed. This includes the customer's name, billing/shipping address, and the items purchased.

- Payment Authorization (Attachment B): Show the payment was properly authorized. Include details like AVS (Address Verification System) and CVV match results.

- Customer Communication (Attachment C): If you have emails or chat logs, include them here. This shows you engaged with the customer and tried to resolve any issues.

- Proof of Shipment and Delivery (Attachment D): For physical products, this is your knockout punch. Provide the tracking number and a direct link to the carrier's confirmation page showing the item was delivered to the customer's address.

This structured approach makes your argument easy to follow and adds a layer of professionalism that builds your credibility. For a more detailed breakdown, our guide to the proper rebuttal letter format provides even more structure and examples.

Maintain a Professional and Factual Tone

It's completely normal to be frustrated, especially when you're dealing with what feels like "friendly fraud." But letting that emotion seep into your rebuttal letter is a critical mistake. Bank investigators respond to cold, hard facts—not feelings.

Avoid accusatory language ("the customer is lying") or subjective statements. Stick to objective, verifiable facts supported by your documentation.

Instead of this: "The customer is obviously trying to scam us. They received the product and are now lying to get it for free."

Try this: "The evidence provided confirms the product was delivered to the cardholder's verified address on [Date], as confirmed by the signature on file with the shipping carrier (see Attachment D)."

The second statement is professional, fact-based, and far more persuasive. It lets the evidence speak for itself, which is exactly what an investigator wants to see. A calm, professional tone shows you're a serious merchant with organized business practices, which can seriously influence the outcome in your favor.

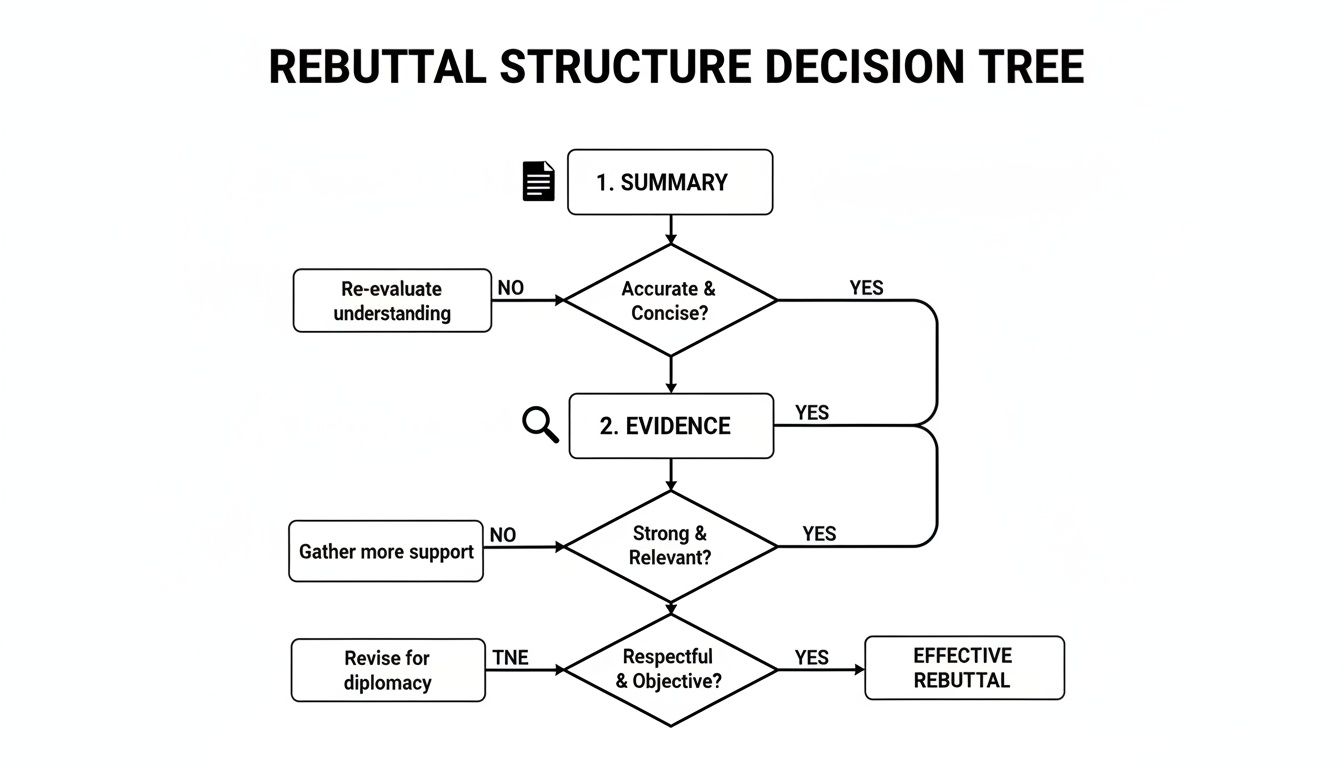

Your Essential Evidence Checklist for Common Disputes

Evidence is the heart and soul of any successful letter of rebuttal. Let's be honest, without concrete proof, your letter is just your opinion, and opinions don't win chargebacks. To build a winning case, you have to match the right evidence with the right dispute reason.

This isn't about throwing everything you have at the wall and hoping something sticks. It’s about a surgical approach where each piece of evidence directly disproves the cardholder's claim. Think of yourself as a detective building an undeniable case file for the bank investigator.

The flowchart below breaks down the core structure your rebuttal should follow. You start with a clear summary, back it up with solid evidence, and deliver it all with a professional tone.

Following this structure makes your argument logical and easy for an investigator to follow, guiding them straight to the proof that invalidates the dispute.

To make this even more practical, let’s look at what you need for the most common chargeback reasons you'll face.

Evidence for "Product Not Received" Disputes

This is one of the most common chargebacks you'll see, but thankfully, it's also one of the easiest to fight with the right documentation. Your entire goal here is simple: prove the item made it to the customer's address.

Your primary evidence should always be:

- Shipping Confirmation: Provide the tracking number from a reputable carrier (like UPS, FedEx, or USPS). A direct link to the carrier’s live tracking page is even better.

- Proof of Delivery: This is your knockout punch. You need a screenshot of the tracking page showing the "Delivered" status, the date, time, and the full delivery address.

- Signature Confirmation: If you have it, a copy of the recipient's signature is nearly impossible for an issuer to argue against.

To really bolster your case, add secondary evidence like screenshots of any customer service emails where you provided the tracking info to the customer before they filed the dispute. And when you're compiling all your evidence, using professional tools for documentation like various receipt templates can make your submission look much more credible.

Tackling "Product Not as Described" Claims

This one can feel a bit more subjective, so your evidence needs to be crystal clear. The customer is claiming what they received doesn't match what you advertised. Your job is to prove it does, point by point.

Start by gathering screenshots from your website as it appeared at the time of purchase.

- Product Page Evidence: Get a clean screenshot of the product description, including all specifications, dimensions, materials, and colors. Be ready to highlight the specific details the customer is disputing.

- High-Quality Product Photos: Include the exact photos the customer would have seen before buying. If they claim the color is wrong, your photos need to show the color accurately under neutral lighting.

- Your Return Policy: Provide a screenshot of your return or refund policy. This shows the customer had a clear path to resolve the issue directly with you but chose a chargeback instead.

The key here is to create a side-by-side comparison for the bank investigator. Show them what you promised on your product page and then, if possible, show proof of what the customer received. If you have any emails offering a return or exchange, include those to show you acted in good faith.

Disproving "Fraudulent Transaction" Allegations

When a customer claims they never authorized a purchase, your evidence needs to connect the legitimate cardholder to that specific transaction. You're looking for data points that prove the order wasn't placed by some random fraudster.

Gather these critical data points from your payment processor:

- AVS and CVV Match Results: Show the results for the Address Verification System (AVS) and Card Verification Value (CVV) from checkout. A "Full Match" on both is powerful evidence that the legitimate cardholder made the purchase.

- IP Address Geolocation: Provide the IP address used to place the order and its physical location. If it matches the cardholder's billing or shipping city, it strongly suggests a legitimate purchase.

- Previous Order History: Has this customer ordered from you before? Presenting a history of successful orders using the same card, shipping address, and IP address makes a "friendly fraud" claim much harder to believe.

Understanding the full timeline of how these claims work is crucial. You can get a deeper dive into the complete card dispute process to better prepare your case. By compiling this digital footprint, you create a compelling narrative that makes it much harder for a customer to falsely claim they were a victim of fraud.

Evidence Matrix for Common Chargeback Reasons

Navigating which evidence to submit for each chargeback reason can feel overwhelming. This quick-reference table matches common chargeback types with the essential proof you need to build a strong rebuttal. Think of it as your cheat sheet for gathering compelling evidence.

This matrix isn't exhaustive, but it covers the heavy hitters. Always aim to provide the primary evidence listed, and use the secondary evidence to build an even more airtight case against the dispute. A well-documented rebuttal is your best defense.

Practical Templates You Can Adapt and Use Today

Let’s be honest, staring at a blank page is the worst part of fighting a chargeback. You know you need to respond, but figuring out what to say can be paralyzing.

To get you started, we’ve put together a few solid templates you can adapt. Think of these as a starting point—they’re structured to be professional, clear, and easy for a bank investigator to digest.

Below are samples for three of the most common dispute reasons you're likely to see. I’ve added some notes to each one on how to personalize the language and build a strong narrative with your evidence.

Template for "Product Not Received"

This claim is a classic, but it's also one of the most winnable if you have your ducks in a row. Your one and only job here is to prove, without a doubt, that the package made it to the customer's verified address.

Subject: Rebuttal for Chargeback Case #[Your Case Number]

Dear [Issuing Bank Name],

We are writing to contest the chargeback for case #[Your Case Number] regarding a transaction of $[Amount] on [Date of Transaction]. The customer's claim is "Product Not Received," but our records and carrier data confirm the order was successfully delivered.

The following evidence is attached to prove delivery:

- Attachment A: The original order invoice, showing the customer's name, billing address, and the shipping address they provided.

- Attachment B: Shipping confirmation from [Carrier Name] with tracking number [Tracking Number]. This proves the item was shipped to the address from the order.

- Attachment C: A screenshot from the carrier's tracking page showing the package was delivered on [Delivery Date] at [Delivery Time]. The delivery address listed matches the shipping address perfectly.

This documentation clearly shows we fulfilled our end of the transaction. We respectfully request the reversal of this chargeback.

Sincerely,

[Your Name]

[Your Business Name]

Fighting "Product Not as Described" Claims

With this one, the burden of proof is on you to show that your product page was an honest and accurate reflection of what the customer bought. Your mission is to dismantle any claim of misrepresentation.

Subject: Rebuttal for Chargeback Case #[Your Case Number]

Dear [Issuing Bank Name],

This letter is in response to chargeback case #[Your Case Number] for $[Amount] on [Date of Transaction]. The cardholder claims the "Product Was Not as Described." We dispute this claim and have provided evidence showing the product was accurately represented on our website.

To support our position, we've attached the following:

- Attachment A: Screenshots of the product page as it appeared when the customer ordered, highlighting product features, dimensions, materials, and photos.

- Attachment B: The order confirmation email we sent, which restates the exact product details.

- Attachment C: A screenshot of our return policy. This shows the customer had a clear and easy path to resolve their issue directly with us, which they chose not to take.

This evidence confirms our product description was accurate and transparent. For more ideas on how to frame your arguments, check out our deep-dive on rebuttal letter templates for different situations. Based on the proof provided, we request that this chargeback be reversed.

Sincerely,

[Your Name]

[Your Business Name]

Disproving "Fraudulent Transaction" Allegations

When you see a "fraud" claim, your goal is to connect the legitimate cardholder to the transaction. You need to show that all signs point to them making the purchase themselves.

The goal here is to build a digital footprint. By presenting data points like AVS/CVV matches and IP geolocation, you create a compelling case that makes a "friendly fraud" claim look highly improbable.

Subject: Rebuttal for Chargeback Case #[Your Case Number]

Dear [Issuing Bank Name],

We are contesting chargeback case #[Your Case Number] for $[Amount] from [Date of Transaction]. The customer has claimed this was a "Fraudulent Transaction," but our verification data strongly indicates the purchase was authorized by the cardholder.

The following data points confirm the transaction's legitimacy:

- AVS and CVV Match: The transaction passed with a "Full Match" for both the Address Verification System (AVS) and the CVV code. This confirms the person who placed the order had the physical card and knew the correct billing address.

- IP Geolocation: The order was placed from the IP address [IP Address], which geolocates to [City, State/Country]. This location is a direct match with the cardholder's billing address.

- Order and Shipping Details: The order was also shipped to the cardholder's verified billing address, further linking them to this transaction.

This combination of data creates a very strong case for a legitimate transaction made by the actual cardholder. We kindly ask that you review this evidence and reverse the chargeback.

Sincerely,

[Your Name]

[Your Business Name]

Where to Send Your Rebuttal Letter: Platform-Specific Guides

Writing a killer letter is only half the battle. The other half is getting it submitted correctly. Every payment platform has its own dashboard, deadlines, and weird little quirks you need to know about.

Making a simple technical mistake—like uploading the wrong file type or missing a deadline by a few minutes—can get your case thrown out before a human ever even sees your evidence.

Knowing your way around the platform is something you have to do. Let’s break down how to handle rebuttal submissions on the big three: Shopify, Stripe, and PayPal.

Responding to Disputes in Shopify

Shopify does a pretty good job of making the dispute process straightforward. They centralize everything right inside your admin dashboard. The moment a chargeback hits, you’ll get an email alert and a notification in your Shopify admin.

From there, head to the Orders section and click on the disputed order. You'll see a big button that says Submit response. Shopify’s interface is designed to hold your hand through the process, prompting you to add specific evidence and write your rebuttal text directly into their form.

Key Shopify Tips:

- Follow Their Lead: Use the guided form. Shopify tailors the required evidence fields based on the chargeback reason code, which helps you stay focused on providing only the most relevant info.

- Check Your File Types: Stick to the basics: PDF, JPEG, or PNG. Don't get fancy with obscure file types that a bank’s ancient system might not be able to open.

- Deadlines Are Final: That deadline you see in your Shopify admin is set in stone. I always recommend submitting your full response at least 24-48 hours early. You never know when a last-minute technical glitch will pop up.

Submitting Your Rebuttal on Stripe

Stripe's dashboard is a data goldmine, which is fantastic for building a strong case. When a dispute is filed, you’ll find it under the Payments > Disputes section.

Stripe’s approach is less guided than Shopify's. You get a more open-ended text box and a file uploader, which offers flexibility but demands you be extremely organized. The best practice here is to upload your polished letter of rebuttal as the main document, then attach all your supporting evidence as separate, clearly named files.

For a much deeper dive into this, check out our guide on handling a https://www.chargepay.ai/blog/stripe-chargeback.

A pro tip from Stripe itself: try compiling all your evidence into a single, well-organized PDF. This prevents the bank investigator from having to download and piece together a dozen different attachments, making their job—and your win—a lot easier.

How to Handle PayPal Disputes

PayPal's process is a bit of a different animal because everything happens within its own closed ecosystem, called the Resolution Center. You'll get a notification, and the case will appear there. PayPal gives you clear options: accept the dispute, issue a refund, or fight back by providing proof.

When you choose to fight, you’ll be prompted to upload evidence directly to the case file. Be concise. PayPal's response fields often have character limits, so keep your written summary short and to the point. Let your attached documents do the real talking. For a better understanding of how these platforms operate in the grand scheme of things, it’s worth consulting sources with deep payment processing expertise.

The financial motivation to get this right is huge. Some merchants just write off small disputes, but that’s a dangerous habit. Data shows that while 46% of chargebacks are auto-accepted, fighting the rest results in a win about 20% of the time. In a market where disputes are projected to hit 337 million by 2025, that 20% is a massive amount of recovered revenue.

Given that the true cost of a single chargeback can be around $190, letting even small disputes slide is like leaving money on the table.

No matter which platform you're on, the core principles are the same. Be fast, be professional, and make it incredibly easy for the reviewer to understand your side of the story. A clean, organized submission through the right portal is the final, crucial step to turning a potential loss into a win.

Common Questions About Rebuttal Letters Answered

Once you get into the swing of handling disputes, you'll notice the same questions pop up over and over. Let's run through some of the most common things merchants ask about crafting and managing their letters of rebuttal. Nailing these details can seriously boost your win rates.

How Long Should My Letter of Rebuttal Be?

Keep it short and sweet. Your main summary should ideally fit on a single page. The entire goal is to make it dead simple for the bank investigator to see your side of the story and find the proof they need without digging.

Put yourself in their shoes: they're sifting through hundreds of these cases. A document that's clean, organized, and scannable is going to be way more persuasive than a five-page essay.

A few formatting tricks can make a world of difference:

- Clear Headings: Use simple labels like "Transaction Details" or "Proof of Delivery" to guide their eyes.

- Bullet Points: Don't write a paragraph when a bulleted list of evidence will do.

- Bold Text: Make critical info like tracking numbers or order IDs impossible to miss by bolding them.

It's all about the quality of your proof, not the quantity of your words.

What Are the Biggest Mistakes to Avoid?

The most common blunders are painfully simple, but they're instant deal-breakers. The absolute worst? Missing the submission deadline. It doesn't matter if your evidence is rock-solid; if it's late, you've automatically lost.

Submitting incomplete or irrelevant evidence is another frequent slip-up. If the customer's claim is "Product Not Received," your entire letter needs to be a laser-focused argument proving delivery. Don't go off on a tangent about their past purchase history unless it directly proves they received this package.

The biggest unforced error, though, is letting emotion creep into your response. It's so tempting to vent, especially when you're sure it's friendly fraud, but it will never, ever help your case. Stick to the facts. Present your evidence calmly and let the documentation speak for itself.

Is It Worth Fighting Low Value Chargebacks?

More often than you'd think, yes. Spending 30 minutes to fight a $15 chargeback might feel like a waste of time, but you have to look at the bigger picture.

When you consistently fight every single illegitimate dispute, you send a clear signal to banks and processors: you run a tight ship and you're paying attention. This can actually improve your standing as a merchant over time and help keep your overall chargeback ratio down. A lower ratio means fewer penalties and a much healthier account.

Of course, that time investment is a real cost. This is exactly where automation tools come in, making it possible to fight every dispute without sinking hours of manual work into it. Once you take the labor cost out of the equation, fighting even the smallest chargebacks becomes a smart financial move that tells fraudsters you're not an easy target.

Can I Automate the Process of Writing These Letters?

Absolutely, and for most growing businesses, you should. Manually writing a unique letter for every dispute is a massive time-drain and, frankly, it’s hard to maintain quality and consistency. As you scale, it becomes completely impossible to keep up.

Modern AI-powered solutions can handle the whole rebuttal process for you. Here’s how they typically work:

- Gathering Evidence: The system automatically pulls all the necessary data—order details, AVS/CVV results, shipping info, customer communications—right from your e-commerce and shipping platforms.

- Generating the Letter: Using the specific reason code for the chargeback, the AI drafts a professional, persuasive rebuttal letter structured exactly the way banks want to see it.

- Submitting the Case: The platform can then submit the whole evidence package directly to your processor's portal, making sure nothing is missed and everything is on time.

This doesn't just save a ton of time; it can dramatically lift your win rate by using data-backed strategies that are proven to work. It lets you get back to focusing on your business instead of getting bogged down in endless dispute paperwork.

Stop losing revenue to tedious, manual chargeback disputes. ChargePay uses AI to automatically generate and submit winning rebuttal letters for you, recovering up to 80% of lost funds hands-free. See how much you can reclaim by visiting https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)