Chargebacks can feel like a sudden hit to your revenue, but not every dispute is a lost cause. As an e-commerce merchant, knowing when and why to fight back is key to protecting your bottom line. It isn't just about reclaiming lost sales; it's about defending your business against friendly fraud, fixing genuine errors, and making sure you don't pay for someone else's mistake or dishonest claim. The right approach can make the difference between losing money and protecting your hard-earned income.

This guide breaks down the most common and legitimate reasons to dispute a charge. We’ll give you clear, actionable advice to help you decide when to push back and what evidence you will need to build a strong case. We will cover everything from clear-cut fraud to situations where the product you received wasn't what you ordered. Each valid reason to dispute a charge listed here comes with practical steps for platforms like Shopify and PayPal. Think of this as your playbook for turning a frustrating, often confusing process into a manageable and recoverable one. Let’s jump into the specific scenarios where challenging a charge is your best move.

1. Fraudulent Charges

The most common and clear-cut reason to dispute a charge is criminal fraud. This happens when a transaction is made using a cardholder's information without their permission, often as a result of theft, a data breach, or a phishing scam. As a merchant, understanding this type of dispute is important, even though the liability typically falls on the card issuer. It represents a direct attack on the payment system, and recognizing its patterns can help protect your business from becoming an unwitting participant.

Identifying True Fraud

Unlike other dispute reasons that can be subjective, true fraud is straightforward: the real cardholder did not authorize the purchase. This is a critical distinction from "friendly fraud," where a customer disputes a legitimate charge they made. Recognizing the difference is key to your response strategy. For more details on this distinction, you can explore the nuances of accidental friendly fraud.

Examples of true fraud include:

- Purchases made with stolen card numbers leaked from a corporate data breach.

- Transactions resulting from a customer’s card details being captured by a skimming device.

- Orders placed by a fraudster who gained account access through a phishing email.

Actionable Steps for Cardholders (and Insights for Merchants)

When a customer reports a fraudulent charge, their bank will advise them to act quickly. They should immediately report the suspicious activity, monitor their statements closely, and file a police report if identity theft is involved. For merchants, this means that by the time you receive the dispute notification, the cardholder and their bank are already treating it as a criminal matter.

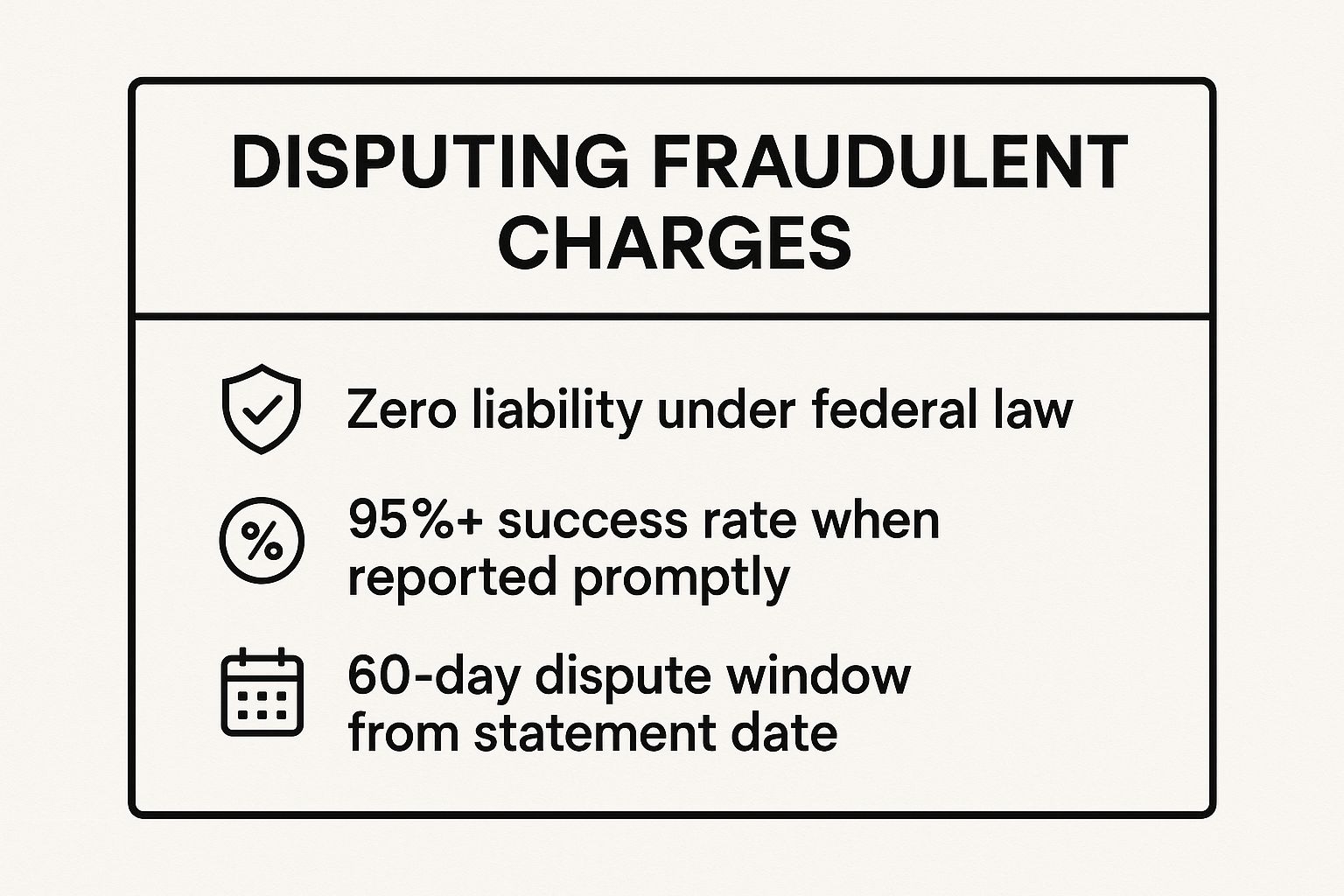

The infographic below highlights key statistics that give cardholders confidence when disputing fraudulent charges.

This data shows that federal protections and prompt reporting give cardholders a very high success rate, making it the most surefire reason to dispute a charge. As a merchant, fighting these disputes is almost always a losing battle, so your focus should be on prevention and providing evidence to the bank when requested.

2. Billing Errors

Beyond fraud, a very common reason to dispute a charge is a simple billing error. These are mistakes made by the merchant or their payment processing system, leading to incorrect charge amounts. This could be anything from a typo at the point of sale to a system glitch that processes a transaction multiple times. For merchants, these disputes are less about malice and more about getting the details right. Understanding and resolving them quickly can prevent customer frustration and protect your reputation.

Identifying Billing Errors

A billing error is any difference between what the customer agreed to pay and what they were actually charged. Unlike fraud, the customer acknowledges making a purchase but contests the final amount or frequency of the charge. The key here is the unintentional mistake that led to the incorrect billing.

Examples of common billing errors include:

- A restaurant accidentally charging $150.00 instead of $15.00 due to a decimal point error.

- An online retailer’s system glitching and processing the same order twice.

- A subscription service incorrectly charging for an annual plan instead of the selected monthly option.

- A hotel charging a room rate in the wrong currency, leading to a much higher final cost.

Actionable Steps for Cardholders (and Insights for Merchants)

When a customer spots a billing error, the recommended first step is often to contact the merchant directly to resolve it. This gives the business a chance to issue a refund or correction without escalating to a formal dispute. If that fails, the cardholder will proceed with a chargeback through their bank.

For merchants, this pre-dispute communication is a golden opportunity. Proactively fixing a billing mistake builds trust and can prevent a chargeback entirely. If a dispute is filed, providing clear documentation showing the corrected transaction or a refund can help you resolve the case. Maintaining accurate and detailed transaction records is your best defense against claims of billing errors.

3. Non-Receipt of Goods or Services

Another common and powerful reason to dispute a charge is when a customer pays for a product or service but never receives it. This issue pops up frequently in e-commerce and situations involving advance payments, where the promise to deliver is broken after payment has been secured. From a merchant's perspective, this type of dispute often points to a problem in your fulfillment process or a major service delivery failure, making it critical to address the root cause to prevent it from happening again.

Defining Non-Receipt

This reason is straightforward: the cardholder’s account was charged, but the expected goods or services never showed up. Unlike disputes over product quality, the core issue here is a complete failure of delivery. The transaction was authorized by the cardholder, but the merchant did not fulfill their end of the agreement. This is a clear violation of the merchant-customer contract and a valid basis for a chargeback.

Examples of non-receipt include:

- An online retailer takes payment for an order but never ships the items.

- A contractor accepts a deposit for a project but never shows up to begin the work.

- A customer purchases a software license but never receives the access key or download link.

- Tickets are bought for an event that is canceled, and the organizer fails to issue a refund.

Actionable Steps for Cardholders (and Insights for Merchants)

When a customer faces a non-receipt issue, their bank will require them to show that they made a good-faith effort to resolve the problem with the merchant first. This includes keeping records of all communication attempts, order confirmations, and any available tracking information. For merchants, this means that clear communication and transparent fulfillment processes are your best defense.

Merchants must maintain meticulous records of shipping and delivery. Providing compelling evidence, such as a proof of delivery document with a signature or a GPS location stamp, is often the only way to win a non-receipt dispute. Without it, the bank will almost always side with the cardholder, reinforcing this as a solid reason to dispute a charge when goods truly haven't arrived.

4. Defective or Significantly Different Products

Another valid reason to dispute a charge happens when a customer receives goods that are materially different from what was advertised, defective, damaged, or of a much lower quality than promised. This dispute type, often called "Product Not as Described," is important for merchants to understand because it directly questions the quality and accuracy of their fulfillment process. Unlike non-receipt claims, the customer acknowledges getting something, but it fails to meet the expectations set by the merchant's own product description.

Identifying a "Significantly Different" Product

This dispute reason comes down to a mismatch between the product description and the actual item received. It is not about a customer changing their mind; it is about a merchant failing to deliver on their promise. A clear, objective difference must exist. This is an important distinction, as these disputes often stem from preventable issues like poor quality control or inaccurate marketing copy. Understanding the specific product return reasons can help merchants identify patterns and address root causes.

Examples of valid "not as described" claims include:

- A piece of furniture advertised as solid oak arriving as cheaper particle board.

- A software package that is missing key features showcased in marketing materials.

- A dress described as "100% silk" that has a label indicating it is a polyester blend.

- Electronics that arrive visibly damaged due to insufficient packaging.

Actionable Steps for Cardholders (and Insights for Merchants)

When a customer receives a defective or misrepresented item, they are typically advised to contact the merchant first to try and work it out, such as a return or exchange. If the merchant is unresponsive or refuses to help, the customer then has a strong case for a chargeback. They will be asked to provide evidence, such as photos of the damage or a comparison of the product with the online advertisement.

For merchants, this means that clear communication and a fair return policy are your best defenses. When a dispute is filed, you will need to provide strong evidence that the product shipped was exactly as described. This could include quality control checklists, shipping records, and precise, unaltered product page descriptions from the time of purchase. Proactively managing customer expectations and product quality is the most effective way to prevent this common reason to dispute a charge.

5. Services Not Performed as Agreed

Another valid reason to dispute a charge occurs when a customer pays for a service that is either not rendered, is incomplete, or fails to meet the quality and terms outlined in an agreement. Unlike disputes over physical goods, service-related issues can be more subjective, but they are just as legitimate when the provider fails to uphold their end of the bargain. For merchants, especially those in service-based industries, understanding this type of dispute is essential for managing customer expectations and minimizing financial loss.

Identifying Service Agreement Failures

This type of dispute hinges on a clear breach of a service agreement, whether written or verbal. The core issue is a mismatch between what was promised and what was delivered. This is a crucial distinction from a customer simply being unhappy with a service that was performed as described. A valid dispute requires proof that the service provider did not fulfill their specific obligations.

Examples of service agreement failures include:

- A wedding photographer who fails to show up for the event.

- A contractor who leaves a home renovation project unfinished after receiving full payment.

- A digital marketing agency that does not deliver the agreed-upon reports and campaigns.

- An online course provider who cancels the course without issuing a refund to enrolled students.

Actionable Steps for Cardholders (and Insights for Merchants)

When a customer faces a service-related issue, their first step should be to attempt to resolve it directly with the service provider. If that fails, they can initiate a chargeback. They will need to provide documentation proving the service was not performed as agreed. This includes contracts, invoices, email correspondence, and photographic or video evidence of incomplete or substandard work.

For merchants, this underscores the importance of clear, detailed contracts and consistent communication. When a dispute arises, you will need to provide evidence that you fulfilled your obligations. This is a situation where having solid documentation is your best defense. Winning these types of disputes is possible, but it requires a well-organized response. To better prepare, it is helpful to learn more about how to fight chargebacks with compelling evidence.

Ultimately, this reason to dispute a charge protects consumers from paying for services that fall significantly short of what was promised. For merchants, it reinforces the need for transparent agreements and high-quality service delivery to prevent such claims from arising in the first place.

6. Cancelled Recurring Subscriptions Still Being Charged

With the explosion of subscription-based services, a frequent reason to dispute a charge is being billed after a recurring payment was properly cancelled. This happens when a customer follows a merchant’s cancellation procedure, but the automated billing system continues to process payments. For merchants, these disputes often point to a breakdown in internal processes, such as a failed communication between your customer service portal and your billing software. Understanding this issue is vital to retaining customer trust and avoiding unnecessary chargeback fees.

Identifying a Valid Cancellation Dispute

This type of dispute comes down to whether the customer followed the correct cancellation procedure as outlined in your terms of service. Unlike subjective disputes, this one is often backed by clear evidence from the cardholder showing they took the required steps to end the subscription. A legitimate cancellation dispute is not a case of a customer forgetting to cancel; it's a failure on the merchant's end to stop the billing cycle. It’s a critical distinction that separates a process error from so-called friendly fraud.

Examples of valid cancellation disputes include:

- A customer is charged for a gym membership the month after submitting a required written cancellation notice.

- A streaming service continues to bill a user who cancelled their account through the online portal and received a confirmation.

- A software-as-a-service (SaaS) subscription auto-renews even though the customer opted out of renewal and has an email to prove it.

Actionable Steps for Cardholders (and Insights for Merchants)

When a customer faces this issue, they are typically advised to present proof of cancellation to their bank. This proof can include confirmation emails, screenshots of a cancellation page, or records of communication with customer service. As a merchant, this means the cardholder is coming prepared with a documented timeline of their attempts to resolve the issue directly.

When you receive a dispute of this nature, your first step should be to review your own records. Check your CRM and billing system for any cancellation requests, support tickets, or other interactions related to the customer's account. If you find evidence of a valid cancellation that your system missed, accepting the dispute is often the most efficient path. Investigating these claims can also help you identify and fix flaws in your subscription management, which is crucial for preventing future disputes, particularly with payment systems like PayPal. You can learn more about how to prevent chargebacks on PayPal and other platforms.

7. Merchant Refusal to Honor Legitimate Refund Policies

A frustrating yet valid reason to dispute a charge is when a merchant fails to honor their own stated policies, such as a satisfaction guarantee or return window. This isn't about buyer's remorse; it's a matter of the business not upholding the terms and conditions it presented at the time of purchase. As a merchant, your policies are a promise to your customers, and failing to adhere to them can rightfully lead to a chargeback that is difficult to win.

Identifying a Policy Violation

This type of dispute comes from a broken agreement. The customer believes they have met all the necessary criteria for a return, refund, or warranty claim as outlined in your policies, but the business refuses to comply. This is a clear-cut reason to dispute a charge because the merchant has violated the contract of sale. For a deeper look into crafting clear policies, you can find helpful guidance on creating a Shopify refund policy.

Examples of a merchant violating their own policies include:

- Denying a return requested on day 15 when the advertised policy is "30-day returns."

- Refusing to honor a "100% money-back guarantee" without providing a valid reason.

- Improperly rejecting a valid warranty claim for a defective product.

- Failing to issue a promised store credit after a return has been processed and accepted.

Actionable Steps for Cardholders (and Insights for Merchants)

When a customer encounters a policy refusal, their first step should be to use all communication channels with the merchant. This includes documenting every interaction, from emails to phone calls. They should be able to prove they followed the policy's instructions, such as returning an item in its original condition within the specified timeframe.

For merchants, this highlights the critical importance of clear, accessible, and consistently enforced policies. If a customer initiates a dispute with evidence that you violated your own terms, their bank will almost certainly side with them. The best defense is to honor your word. Ensure your customer service team is well-versed in your policies and empowered to resolve these issues before they escalate to a chargeback. Providing a good customer experience is often the most effective dispute prevention strategy.

7 Reasons to Dispute Charges Comparison

Automate Your Defense and Reclaim Your Revenue

Navigating the world of chargebacks can feel like a constant battle. As we've explored, there are numerous legitimate reasons to dispute a charge, each with its own set of rules and evidence requirements. From clear-cut fraudulent transactions and simple billing errors to more tricky situations like goods arriving damaged or services not being rendered as promised, your ability to fight back effectively is crucial. Ignoring these disputes is not an option; it's a direct drain on your revenue and a threat to your merchant account's health.

The key takeaway is that every dispute tells a story. Whether it's a customer claiming they never received a package, an issue with a recurring subscription, or a product that didn't meet expectations, your job is to present the facts clearly and convincingly. This requires meticulous record-keeping, a deep understanding of dispute reason codes, and a smart approach to submitting evidence. Simply having a valid reason to dispute a charge is only half the battle; winning the dispute is what protects your bottom line.

Your Action Plan for Winning Disputes

Feeling overwhelmed by the process is normal, but letting disputes pile up is a costly mistake. Instead of reacting to each chargeback as it comes, it's time to build a proactive defense system. Here are the immediate steps you should take to turn your dispute management from a liability into an asset:

- Audit Your Processes: Review your current checkout, shipping, and customer service procedures. Where are the weak points? Strengthen your terms of service, clarify your refund policy, and ensure you're collecting essential evidence like delivery confirmations and customer communications for every order.

- Document Everything: Make it a non-negotiable habit. Save screenshots, emails, tracking information, and any other piece of data that can validate a transaction. When a dispute arises, you won't be scrambling for proof; you'll have an evidence file ready to go.

- Embrace Automation: Manually managing disputes is a time-consuming and error-prone process. As your business grows, it becomes unsustainable. The biggest step you can take to improve your win rate and save countless hours is to automate your defense.

This is where you can fundamentally shift the odds in your favor. Instead of getting bogged down in the administrative details of each individual chargeback, you can use technology to handle the heavy lifting. Platforms specifically designed for this purpose can analyze a dispute, gather the relevant evidence from your e-commerce platform, and generate a compelling response tailored to the specific reason code. This not only increases your chances of winning but also frees you and your team to focus on growing your business. By turning your defense into an automated, efficient system, you can reclaim lost revenue and secure your financial stability.

Ready to stop losing money to preventable chargebacks? ChargePay uses AI to automate the entire dispute process for Shopify and PayPal merchants, crafting evidence-based responses that boost your win rate. See how much revenue you can recover by visiting ChargePay and starting your journey to smarter chargeback management.

.svg)

.svg)

.svg)

.svg)