A well-crafted rebuttal letter template is your best weapon in the fight against costly chargebacks. It’s not just about filling in blanks; it’s a clear, professional framework for presenting your evidence, which can dramatically increase your chances of getting your money back and protecting your business.

Why a Rebuttal Strategy Isn't Optional

Let’s be real—chargebacks are one of the most maddening parts of running a business. They feel like a sudden, unfair penalty, and it's tempting to just write off the loss and move on.

But treating chargebacks as just another "cost of doing business" is a massive mistake. Every chargeback you accept isn't just a lost sale; it's a black mark on your merchant account's health.

Ignoring them can snowball into higher processing fees or, in the worst-case scenario, account termination. This is where having a proactive rebuttal strategy, with a solid rebuttal letter at its core, becomes something you absolutely need.

Flipping the Script on Chargebacks

Think of your rebuttal letter less like paperwork and more like your official case file. It’s your one shot to tell your side of the story directly to the card issuer, backed by cold, hard facts. An emotional, disorganized, or incomplete response is incredibly easy for a bank to dismiss.

On the other hand, a professional, evidence-based letter makes their job easier and makes your business look credible and diligent.

This isn’t just about winning a single dispute; it’s about building a system for defending yourself. Having a go-to rebuttal letter template means you can respond quickly and effectively every single time, without scrambling to start from scratch.

A proactive approach transforms you from a passive victim of chargebacks into an active defender of your revenue. It sends a clear message that you track your transactions and are prepared to contest baseless claims.

This shift in mindset is crucial. Effective chargeback dispute management is a core business function, just like marketing or customer service. It directly protects your bottom line and ensures the long-term stability of your payment processing relationships.

The impact of a well-prepared letter is huge. Industry data shows that merchants who use well-crafted rebuttal letters see up to a 70% higher success rate in their disputes. Getting your response in quickly, usually within the typical 7-to-11-day window, is also a key piece of the puzzle.

The Rebuttal Letter Template That Actually Works

Alright, let's get right to it. You're here for a clear, copy-and-paste rebuttal letter template that gets the job done. I can't stress this enough: a well-structured letter is your first and best shot at making a good impression on the bank employee reviewing your case. It absolutely has to be professional, to the point, and easy for them to follow.

This isn't the time to write a long, emotional essay about how unfair the situation is. It’s all about presenting the cold, hard facts in a way that makes it simple for the reviewer to see things your way and agree with you. Your goal is to show them, as quickly as possible, that the transaction was legitimate and the chargeback has no merit.

Here’s a look at a simple but incredibly effective rebuttal letter template we use.

Notice how it immediately lays out the essential information. It states the purpose of the letter and then clearly lists the attached evidence. Every single element is designed to make the reviewer's job as easy as possible.

Deconstructing the Template

Let’s quickly break down why this structure works so well. Each part has a very specific job, guiding the reviewer through your argument logically. Think of it like you're a lawyer building a case—you're laying down each piece of evidence, one by one, leaving no room for doubt.

The template is really just three core parts:

The Introduction: This is where you hit them with the key details right up front. The case number, transaction date, and the disputed amount need to be right at the top. This gets the reviewer oriented in seconds and shows you're organized.

The Body: Here, you tackle the chargeback reason code head-on. Briefly explain why the customer's claim is incorrect, and then—this is crucial—list your evidence. Using a bulleted list for your attachments makes it instantly scannable and digestible.

The Conclusion: All you need is a simple, professional closing. Offer to provide more information if they need it and make sure your contact details are there.

This whole format respects the reviewer's time. These people deal with hundreds of cases a day, and a letter that cuts straight to the facts is a breath of fresh air.

A great rebuttal letter doesn’t just list evidence; it tells a clear story. It should read like this: "Here is the claim, here is why it’s wrong, and here is the proof."

Why Every Single Sentence Matters

Every word you write in your rebuttal letter has to serve a purpose. Cut out the fluff, the emotional language, and any unnecessary details about your business. For instance, never say something like, "We're a small family business and this chargeback is really hurting us."

Instead, stick to the facts. A much more powerful statement is, "We are contesting this chargeback with the attached proof of delivery, which includes the customer's signature."

The first approach is subjective and easy to ignore; the second is factual and compelling. Winning a dispute is 100% about the evidence you can provide. For a deeper dive into the strategies that work, check out our complete guide on how to win a credit card dispute.

Remember to keep your sentences and paragraphs short. Long blocks of text are intimidating and can cause the reviewer to skim right over important details. Use formatting like bold text for key info like the chargeback reason code to make it pop. This simple, structured approach is your best bet for turning a potential loss back into revenue.

How to Gather Evidence That Wins Disputes

Even the most perfectly worded rebuttal letter template is just words on a page without solid proof to back it up. The evidence you provide is the heart of your dispute, and gathering it methodically is the only way to build a case that’s impossible to ignore.

Think of yourself as a detective. Your mission is to collect compelling evidence that directly demolishes the customer’s specific claim. You need to show the bank reviewer, with cold, hard facts, that the transaction was legitimate and the chargeback has no merit.

Digital and Transactional Proof

For any online business, your most powerful evidence lives in the digital footprints left during the purchase. These data points are your first line of defense, capable of poking immediate holes in common claims like fraud or unauthorized use.

Start with the basics—the core transaction details:

- Order Confirmation and Receipts: Always include the invoice or welcome email you sent to the customer right after they checked out.

- AVS and CVV Match Results: This is huge. Show the bank that the Address Verification System (AVS) and Card Verification Value (CVV) checks came back as a match. It’s strong proof the actual cardholder was involved.

- IP Address Logs: Note the IP address used for the purchase. If you can show it matches the customer’s billing location, you’ve just added another powerful layer to your defense.

These pieces build a strong foundation, but to truly lock down a win, you often need to dig a bit deeper.

Proof of Delivery and Customer Interaction

If the chargeback reason is "product not received," your shipping documentation is everything. Don't just throw a tracking number at them. Provide a screenshot of the final delivery confirmation showing the date, time, and full address.

Got a signature confirmation? Even better. That’s your silver bullet.

Beyond delivery, look at your direct communications. Any conversation you had with the customer can be incredibly persuasive.

- Emails or Chat Logs: Did the customer email you for support? Did they ask a question about the product in your site’s chat? Any interaction where they acknowledge the purchase or product is gold.

- Customer Account History: If they’re a repeat customer, point that out! Show their purchase history, especially if they’ve successfully ordered from you before using the same card and shipping details.

The key is to organize all this evidence to tell a clear, logical story. Your rebuttal letter should act as the guide, walking the reviewer through your proof step-by-step, making it impossible for them to arrive at any other conclusion but yours.

Every piece of evidence you add makes your position stronger. For a more detailed look at building an airtight case, check out our complete guide on how to fight a chargeback. By being meticulous and organized, you turn a simple rebuttal letter into a powerful, revenue-recovering tool.

Tailoring Your Rebuttal for Different Chargeback Claims

A one-size-fits-all approach just doesn’t cut it with chargebacks. The reason code behind the dispute completely changes the story you need to tell, which means your rebuttal letter template has to be flexible. You need to tweak the language and shuffle your evidence to build a targeted, compelling case for each specific scenario.

Think of it this way: fighting a "fraudulent transaction" claim requires a totally different playbook than a "product not as described" dispute. The core template gives you a solid foundation, but the details you plug in are what will actually win the fight.

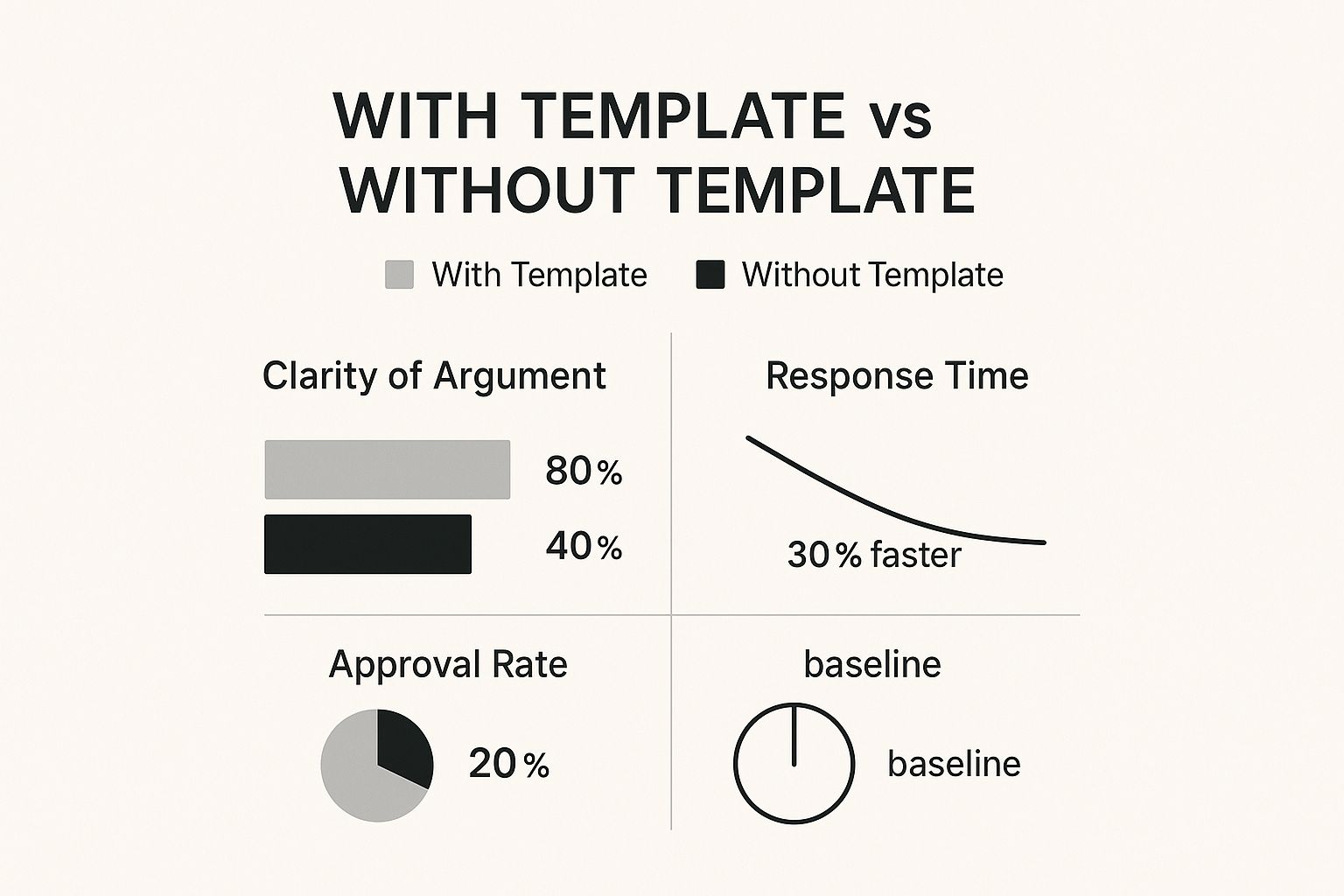

This isn't just theory—it has a real, measurable impact on your win rates. The data below clearly shows the difference between using a structured, adaptable template and winging it every time.

As you can see, a templated approach brings clarity, slashes your response time, and gives your approval rate a serious boost. It's a system built for winning.

To make this practical, let's break down how to handle the most common chargeback reasons you'll face.

When the Claim Is Fraud

This is probably the most frequent chargeback you'll see. When a customer claims a transaction was fraudulent, your single goal is to prove the legitimate cardholder was involved. Your rebuttal letter needs to be a laser-focused presentation of every piece of evidence connecting that person to the purchase.

Key evidence to lead with:

- AVS and CVV Match Results: This is your opening punch. A successful match is powerful proof that the person who placed the order had the physical card in their hands.

- IP Address Geolocation: Show that the IP address used to make the purchase matches the customer's billing or shipping address. It’s another strong link.

- Customer Communication: Did they email you? Open a support ticket? Any communication where the customer discusses their order helps prove they were aware of the transaction.

Your summary statement in the letter should be direct and confident: "The transaction was verified with a matching CVV and originated from an IP address consistent with the cardholder's known location."

For "Product Not as Described" Claims

Here, the customer isn't saying they didn't buy it; they're claiming what showed up wasn't what they were promised. Your job is to prove your product was represented accurately and fairly.

Your rebuttal should be built around:

- Product Descriptions and Images: Pull screenshots directly from the product page the customer ordered from. Show the bank exactly what they saw.

- Order Confirmation: Include the confirmation email that details precisely what they bought—size, color, model number, everything.

- Customer Acknowledgment: This is gold. If the customer left a positive review or sent a happy email before filing the dispute, it completely undermines their claim.

Interestingly, the skill of writing a compelling rebuttal letter isn't just for ecommerce. A 2024 study found that these letters are a vital tool in scientific research for correcting errors and upholding integrity. It's a universal method for quality control, which you can read more about in this article on how rebuttal letters ensure quality assurance.

Handling "Subscription Canceled" Disputes

This one is a classic for SaaS companies and subscription box services. The customer swears they canceled their service but you charged them anyway. Your evidence must prove two things: they agreed to your terms, and they failed to cancel according to your stated policy.

Your goal isn't just to present evidence; it's to make it impossible for the reviewer to ignore your side of the story. Tailor every word and attachment to dismantle the specific claim being made.

For these subscription disputes, you absolutely must include:

- Terms of Service Agreement: Show the screenshot where the customer checked the "I agree" box for your subscription and cancellation policy.

- Cancellation Policy: Provide a clean, easy-to-read copy of your policy, highlighting the exact steps required to cancel.

- Account Activity Logs: This is your knockout blow. Present logs showing the customer logged in or used the service after the date they claimed to have canceled.

By customizing your rebuttal letter template for each unique scenario, you turn a simple form into a strategic weapon. It allows you to directly address—and defeat—the specific reason for the dispute every single time.

To help you gather the right proof, here’s a quick-reference checklist for the most common dispute types.

Evidence Checklist for Common Chargebacks

Having the right evidence on hand is half the battle. This table should make it easier to quickly assemble a strong case no matter what kind of chargeback lands on your desk.

Little Tweaks to Boost Your Win Rate

Having a solid rebuttal letter and the right evidence is half the battle, but it's the small details in your approach that often tip the scales in your favor. Winning a dispute isn’t just about checking off boxes; it’s about making it incredibly easy for the bank reviewer to see things your way and agree with you.

First things first: a calm, professional tone is non-negotiable. It’s incredibly frustrating when you know a chargeback is bogus, but letting that emotion bleed into your response is a huge mistake. A venting, angry letter only makes you look unprofessional and can bias the reviewer against you before they even glance at your evidence.

Always stick to the facts. Present your case logically and calmly. This signals that you're a serious merchant who handles business professionally, which instantly boosts your credibility.

Speed and Clarity Are Your Best Friends

One of the most powerful habits you can build is responding quickly. Every chargeback has a strict deadline, and dragging your feet until the last minute is just asking for trouble. Submitting your response well before the cutoff shows you’re organized and on top of your game. Even better, it gives the reviewer plenty of time to go through your case without feeling rushed.

Clarity is just as critical. Bank employees are swamped, reviewing hundreds of these cases every single day. A long, rambling letter packed with irrelevant details will get skimmed at best, meaning your most important points will probably be missed.

So, keep your rebuttal short, sweet, and to the point.

- Use bullet points to make your key pieces of evidence pop.

- Bold important info like the transaction ID or a delivery confirmation number.

- Keep paragraphs short—just a sentence or two—to make the whole thing easy to scan.

Your goal is to build a rebuttal package so clear and well-organized that the reviewer can grasp your entire argument in less than 60 seconds. Simplicity is what wins disputes.

Focus on What Matters—and Nothing Else

Every single sentence and piece of evidence you submit needs to directly address the chargeback reason code. If the customer is claiming "product not received," don't waste precious space talking about how much they loved a different product they bought last year. Focus exclusively on proving delivery.

Irrelevant details just create noise and risk confusing the person making the decision. Before you hit submit, do a final read-through and ask yourself: "Does this piece of information directly help disprove the customer's claim?" If the answer is no, cut it. A lean, focused rebuttal is always more powerful than one bloated with fluff.

This disciplined approach won't just improve your win rate; it also makes the whole process less of a headache. When you have a system, managing disputes becomes a straightforward task instead of a chaotic scramble. For a deeper dive into getting ahead of these issues, you can learn more about effective chargeback fraud prevention in our detailed guide.

Common Rebuttal Questions Answered

Even with the perfect rebuttal letter template ready to go, you're bound to have questions. Let's be honest, the chargeback process can feel like a maze, but a few key details can give you the confidence to handle any dispute that lands on your desk. My goal here is to clear up some of the most common points of confusion I see merchants struggle with.

One of the biggest anxieties is always the timeline. Knowing your deadlines is non-negotiable—miss one, and you’ve lost automatically, no matter how solid your evidence is.

How Long Do I Have to Respond?

The window you have to submit your rebuttal is surprisingly tight. You're usually looking at just 7 to 20 days from the moment the chargeback is filed. This timeframe isn't set in stone; it can vary depending on the card network and your payment processor, so you absolutely must check the specific deadline in your chargeback notification.

My best advice? Don't wait. The moment that notice hits your inbox, start pulling your evidence and drafting your rebuttal. Submitting everything well before the final day helps you sidestep any last-minute technical glitches or other headaches.

Can I Win a Chargeback for Digital Products?

Yes, you absolutely can. The evidence just looks a little different. Since you can't provide a shipping confirmation or a delivery signature, your proof has to pivot to digital access and usage.

To build a winning case, you'll need to gather evidence like:

- Server logs that show the customer logged into their account.

- Download records confirming they accessed the digital file.

- Email correspondence where you delivered a service or the customer acknowledged they received it.

The whole point is to paint a clear picture showing the customer got and used what they paid for. This is especially crucial for fighting back against so-called "friendly fraud," where a real customer disputes a charge they actually made.

There's a common myth that disputes over intangible goods are a lost cause. That’s just not true. With the right digital proof, your case can be just as compelling as one for a physical product.

What Happens If I Lose the Dispute?

If the bank rules in the customer's favor, those disputed funds are gone for good. But the damage doesn't stop there. That loss also dings your chargeback ratio, a metric that payment processors watch like a hawk.

If your chargeback ratio climbs too high, you could be looking at steeper processing fees or, in a worst-case scenario, having your merchant account shut down entirely. This is exactly why fighting every single winnable dispute is so vital for the long-term health of your business. You might get a chance to appeal through a process called pre-arbitration, but it's often a complex and expensive road to go down.

Tired of the manual grind of fighting chargebacks? ChargePay uses AI to automatically generate and submit winning dispute responses for you, recovering up to 80% of your lost revenue without you lifting a finger. See how it works at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)