Let's get straight to the point. Think of Stripe Chargeback Protection as an insurance policy for your online sales. For a small fee on each transaction, Stripe essentially agrees to cover the full amount and any dispute fees if a customer's bank files a fraudulent chargeback. This saves you from both the financial sting and the headache of fighting it.

What Is Stripe Chargeback Protection Really?

If you run an online business, you know that chargebacks are, unfortunately, part of the game. Before we dig into Stripe's solution, it’s a good idea to be clear on exactly what a chargeback is. It’s simply a payment reversal that gets kicked off by a customer's bank after they dispute a charge on their statement.

Stripe Chargeback Protection is an optional service built to be your financial safety net, specifically for fraudulent disputes. Imagine you're a trapeze artist performing high above the ground; one slip, and the fall is a big deal. A fraudulent chargeback is that slip. With this protection, Stripe is holding the net for you.

You pay a small, predictable fee on every transaction. In return, Stripe takes the financial hit from any eligible fraudulent chargebacks. This means you don't lose the original sale amount, and you also get to skip the standard dispute fee, which is usually $15 per incident on Stripe.

The Cost-Benefit Trade-Off

Stripe rolled out this program to help merchants like you deal with the often steep costs tied to disputes. For a fee of 0.4% per transaction, you're basically transferring the risk of certain types of fraud over to Stripe. It also means you get to sidestep the whole process of gathering and submitting evidence for those covered cases.

To go deeper on this, you can read our detailed guide on how Stripe Chargeback Protection works for sellers.

This protection is especially valuable because it covers the two most painful parts of a fraudulent dispute: the lost revenue from the sale and the extra chargeback fee slapped on by the payment network. You won't have to get into the time-sucking back-and-forth with the bank for these specific claims.

Key Insight: The real value of Stripe Chargeback Protection isn't just about the money—it's about getting your time back. It handles the financial side of eligible fraud disputes automatically, freeing you up to focus on growing your business instead of wrestling with endless paperwork.

A Clear Before-and-After Look

To really see the value, let's compare the financial hit of a single $100 fraudulent chargeback with and without the protection. The difference is pretty stark.

Stripe Chargeback Protection at a Glance

Here’s a quick breakdown of what happens to your bottom line when a $100 fraudulent chargeback hits.

As the table makes clear, a single fraudulent dispute can cost you way more than the original transaction was even worth. But with Stripe's protection, the financial damage is cut down to just the small, predictable fee you paid upfront.

How The Protection Process Actually Works

So, what really happens behind the curtain when a customer files a dispute? The beauty of Stripe Chargeback Protection is its automation. It’s designed to be a completely hands-off experience for you—a huge departure from the manual, often stressful, process of fighting a chargeback on your own.

Let's walk through the entire journey, from the moment a customer pays to the second Stripe steps in. Think of a traditional chargeback fight like a frantic scramble to find receipts and emails after your store has been "robbed." With Stripe's protection, it's more like having a security system that automatically handles the incident for you.

When a customer disputes a charge with their bank, that bank sends a formal chargeback notification. Normally, this is where your work would begin, launching you into a race against the clock to gather evidence and build a case. But with this protection active, Stripe's systems immediately get to work on your behalf.

The Automated Defense System

The process is built for speed and efficiency, taking the burden completely off your shoulders for eligible disputes. Stripe’s system doesn't just sit around waiting for you to act; it springs into action the moment a fraudulent chargeback is identified.

It's a massive shift from the old way of doing things. Instead of you spending hours or even days digging through order histories, shipping confirmations, and customer communications, you do… well, nothing. For covered claims, there is no evidence to submit and no stressful paperwork to fill out.

This automated process is the core of what makes Stripe Chargeback Protection so valuable. It not only saves you from a potential financial loss but also gives you back your most precious asset: your time. While you focus on your customers and products, Stripe manages the dispute quietly in the background.

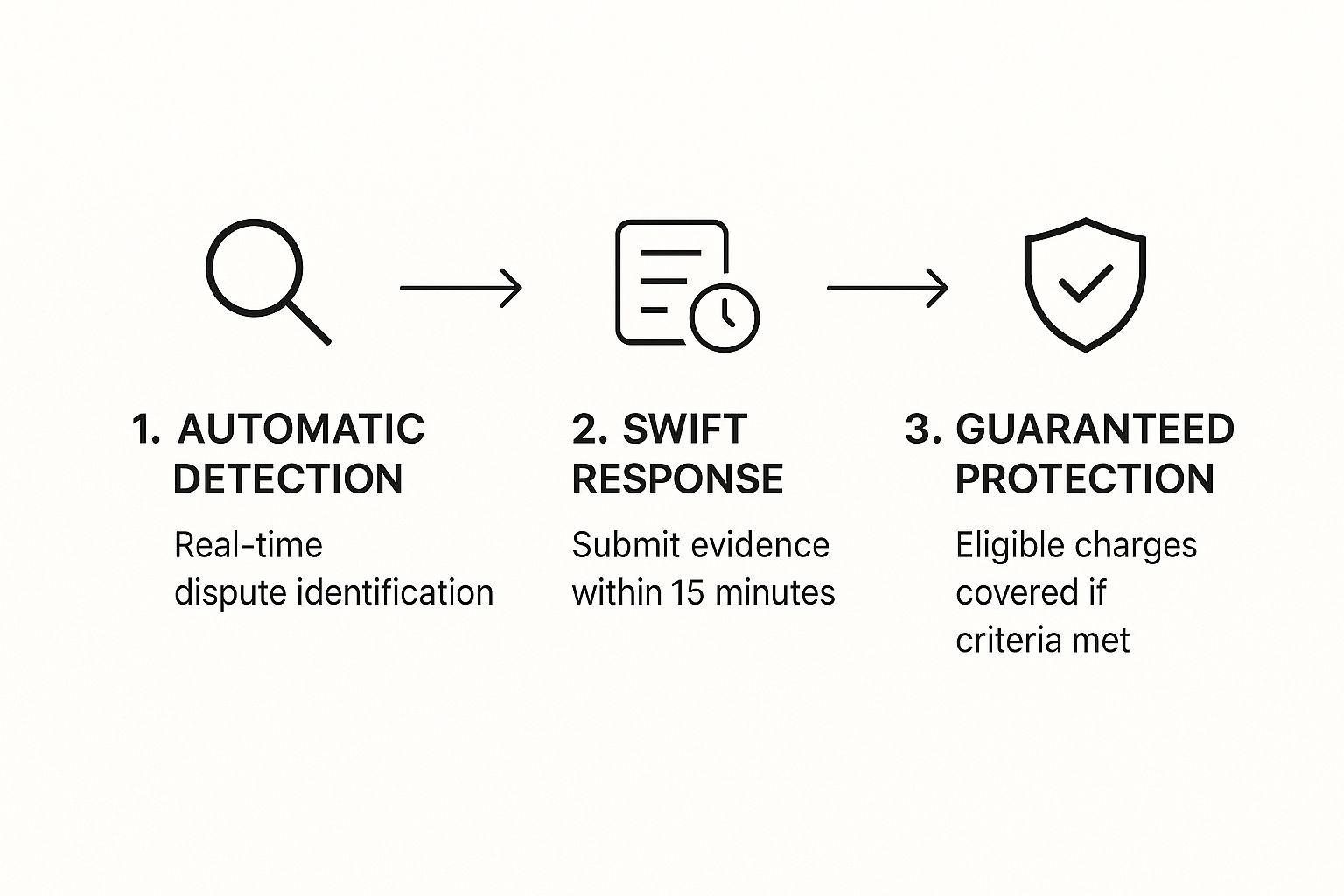

This infographic breaks down the core stages of how the automated protection works.

As you can see, Stripe instantly detects the dispute, submits the necessary evidence for you, and guarantees protection if the charge is eligible—all without you lifting a finger.

A Step-by-Step Breakdown

To really appreciate the automation, let's detail the sequence of events for a covered fraudulent dispute:

A Dispute is Filed: A customer gets in touch with their bank to dispute a transaction, claiming it was fraudulent. The bank then kicks off a chargeback against your Stripe account.

Stripe's System Takes Over: Instead of just sending you a notification and starting the clock, Stripe's internal system automatically identifies the chargeback reason code. If the code lines up with one of the covered fraud-related categories (like "Fraudulent Transaction"), the protection process is triggered.

Instant Financial Shielding: The moment Stripe confirms the dispute is eligible for protection, your account is shielded. The disputed amount and the $15 dispute fee are immediately covered by Stripe. You won't see those funds get pulled from your account.

The Bottom Line: For any chargeback covered by Stripe Chargeback Protection, you pay nothing. The disputed amount and the associated fee are handled entirely by Stripe. You get to keep the revenue from the original sale as if the dispute never even happened.

This hands-free approach is a game-changer, especially for businesses dealing with a steady stream of fraud-related claims. It stops revenue leakage in its tracks and cuts out the operational drag of dispute management. It's crucial to remember, however, that this protection is specifically for fraud. For a deeper dive into a more comprehensive defense, you can explore our guide on effective chargeback fraud prevention strategies.

Understanding the True Cost and Fees

When you're looking at any new service for your business, the first question is always the same: "What's it going to cost me?" Stripe Chargeback Protection is pretty straightforward with its pricing, but getting the full picture means looking past just the percentage. It’s really about weighing a small, predictable fee against a massive, unpredictable expense.

The main cost is a flat 0.4% fee on every single transaction you process. This is on top of Stripe's usual payment processing fees (typically 2.9% + $0.30 per transaction). So, for a $100 sale, you'd pay an extra $0.40 for the protection.

This fee gets charged whether a chargeback happens or not. Think of it as the price you pay for the peace of mind that if a fraudulent dispute pops up, Stripe has your back.

The Standard Dispute Fee You Avoid

To really see the value in that 0.4%, you need to know what you’re up against without it. Any time a customer files a chargeback and you don't have this protection, Stripe hits you with a standard, non-refundable dispute fee. In the United States, this fee is $15 per incident.

That’s a flat $15 loss, completely separate from the original transaction amount you also lose. This fee alone can flip a profitable sale into a painful loss, making the Stripe Chargeback Protection fee look like a small price for predictability.

The Trade-Off: You're essentially swapping an unpredictable $15 dispute fee (plus the lost sale) for a predictable 0.4% protection fee on all your sales. For most businesses dealing with fraud, this is a very smart financial move.

Running the Numbers for Your Business

Let's break this down with a couple of real-world examples. The value of the protection really shines when you look at your own average sale price and volume.

- Average Sale: $50

- Protection Fee per Sale: $0.20 (0.4% of $50)

- Cost to protect 100 sales: $20

- Cost of one unprotected chargeback: $65 ($50 lost sale + $15 fee)

In this scenario, the business pays $20 to protect $5,000 in sales. Just one fraudulent chargeback would have cost more than three times the total protection fees they paid for all 100 transactions. This shows just how quickly the chargeback issue can become a serious problem for your bottom line.

- Monthly Sales: 500 transactions

- Average Sale: $100

- Total Monthly Revenue: $50,000

- Total Monthly Protection Fee: $200 (0.4% of $50,000)

Here, the store owner invests $200 a month for complete peace of mind from fraudulent disputes. If they were getting just two fraudulent chargebacks a month, their unprotected cost would be $230 (two lost $100 sales + two $15 fees). The protection not only covers this but shields them from any more fraud disputes without costing them a penny extra.

By running these numbers for your own business, you can see the potential return on investment clear as day. It’s a simple calculation that helps you decide if the 0.4% fee is a worthwhile trade for getting rid of the financial shock and operational headache of fraudulent chargebacks.

Who Is Eligible and What Are the Limits?

Stripe's Chargeback Protection sounds like a great safety net, but it's not a free-for-all. Before you jump in, you need to know who gets invited to the party. Think of it like a members-only club—you have to meet certain criteria to get past the velvet rope.

The biggest rule is that protection only covers payments made through specific Stripe products. To qualify, your transactions absolutely must go through either Stripe Checkout or Payment Links. If you're running a custom API integration for your checkout process, those sales are, unfortunately, on their own.

This isn't an arbitrary rule. It's Stripe's way of ensuring its own advanced fraud detection systems, which are baked right into Checkout and Payment Links, get the first look. They need to analyze the transaction and assess the risk before they can put their money on the line to protect you.

Key Eligibility Gates to Pass

Stripe has a pretty clear checklist for eligibility, and straying from it can leave you exposed right when you thought you were covered. It’s not just about the tools you use, but also about how you use them.

For starters, your business needs to be based in an eligible region, which right now includes the United States and most of Europe. You also can't just cherry-pick which transactions to protect. You can't, for example, route only your high-risk sales through the protection program while processing your "safe" ones normally. It’s an all-or-nothing deal for your qualifying sales.

Here are the core requirements you have to meet:

- Mandatory Tools: All transactions must be processed using Stripe Checkout or Payment Links. This is the most important one.

- Geographic Location: Your business must be located in the U.S. or an eligible European country.

- No Discriminatory Routing: You can't pick and choose which transactions get protection. It must be applied across the board.

- Adherence to Terms: Your business has to be in full compliance with Stripe’s Terms of Service. Any violation can get you disqualified immediately.

If you miss any of these points, the Stripe chargeback protection you were counting on won't be there when you need it.

The All-Important Annual Protection Cap

Now for what might be the most critical limitation: the annual protection limit. Stripe doesn’t offer a bottomless pit of coverage. There's a hard yearly cap on the total amount they'll reimburse you for fraudulent chargebacks, designed to protect both you and Stripe from runaway fraud.

Stripe sets these limits based on the currency you operate in. For most businesses in the United States, the annual protection cap is $25,000. Once you hit that number, any fraudulent chargebacks you get for the rest of the year are completely on you—that means you eat the cost of the lost sale and the dispute fee.

To get a feel for how these limits work in different regions, here's a quick look at the annual protection caps for various currencies.

Stripe Protection Annual Limits by Currency

As you can see, the cap varies depending on your business's primary currency, so it's vital to know your specific limit.

Crucial Takeaway: The annual cap is a hard stop. It’s essential to monitor your covered chargebacks throughout the year to know where you stand. If your business faces fraud levels that approach this limit, you'll need a backup plan.

This limit resets every year, but it clearly shows that this service is best suited for businesses dealing with moderate levels of fraud. If you have extremely high sales volumes or operate in a high-risk industry, you might burn through that cap pretty quickly. For a more complete defense, it’s smart to look into other chargeback management tools that can work alongside Stripe's offering and cover disputes that fall outside its protection.

The Gaps Where Stripe Protection Falls Short

While having a safety net for fraudulent disputes is a huge relief, it's critical to understand that Stripe Chargeback Protection isn't an unbreakable shield. Think of it like a specialized tool in your toolbox; it’s fantastic for one specific job—handling certain types of fraud—but totally ineffective for others. Believing it’s a cure-all for every dispute is a fast track to some nasty, unexpected losses.

The program is laser-focused on one thing: chargebacks filed with a “fraudulent” reason code. This means if a customer claims they never authorized a transaction, you’re probably covered. But the world of chargebacks is much bigger and more complicated than that.

So many disputes have nothing to do with stolen credit cards. They actually stem from customer service issues, shipping delays, or problems with product quality. Stripe’s protection offers absolutely no help in these common scenarios, leaving you to fight them the old-fashioned way.

Common Disputes That Fall Through the Cracks

The list of chargebacks that Stripe doesn't cover is longer than most merchants realize. For these disputes, you are completely on your own, responsible for both the lost sale amount and the $15 dispute fee.

Getting a handle on these gaps is the first step toward building a more complete defense strategy. Let’s look at the most common types of chargebacks that will bypass your Stripe protection completely:

- Product Not as Described: The customer gets the item but claims it doesn't match the photos or description on your website.

- Service Not Rendered: A customer pays for a service—like a consultation or a digital course—but says they never received it.

- Defective Product: The item arrives broken, damaged, or just doesn't work as advertised.

- Subscription Cancellation Issues: A customer insists they canceled their subscription but got charged again anyway.

- Unrecognized Transaction: The customer genuinely doesn’t recognize your business name on their statement and disputes the charge, even if it was legitimate.

All of these represent valid customer concerns (at least from their point of view) that fall squarely outside the fraud category. Stripe's program won't step in, and you'll have to manage the entire dispute process yourself.

The Growing Problem of Friendly Fraud

There’s another major gap, and it's a big one: friendly fraud. This is when a legitimate customer makes a purchase, receives the product, and then files a chargeback anyway. They might do this out of buyer’s remorse, to avoid paying for return shipping, or simply because they know they can often get away with it.

Key Insight: Because friendly fraud disputes are often initiated under non-fraud reason codes like "Product Not Received," they aren't covered by Stripe Chargeback Protection. This leaves you completely exposed to one of the most common and frustrating types of revenue loss.

Chargebacks put a huge financial weight on merchants, and friendly fraud is a primary driver. In fact, it accounts for over 70% of all chargebacks, with simple buyer's remorse being behind 65.3% of those cases. These are precisely the kinds of disputes that Stripe's fraud-centric protection is not designed to handle, leaving a significant vulnerability in your defenses.

This reality check isn't meant to knock Stripe's service, but to highlight its specific purpose. It’s a great tool for a particular problem. For everything else, you still need a robust strategy to manage non-fraud disputes. Beyond what Stripe offers, you can even learn how to cut chargebacks dramatically with a single email strategy. Knowing these limitations is key to realizing that a complete defense requires more than one layer of protection.

Going Beyond Stripe With an AI-Powered Solution

Stripe Chargeback Protection is a solid tool for what it does—covering very specific types of fraudulent disputes. But as we've seen, it leaves some pretty big gaps in your defenses. This is where a more advanced, AI-powered service like ChargePay steps in, not as a replacement, but as a powerful partner to create a truly complete chargeback management system.

Think of it this way: Stripe’s protection is like a security guard posted at your front door, trained to spot one specific type of threat. ChargePay, on the other hand, is like a full-building security system with cameras on every floor, actively monitoring and responding to all potential issues—from clear-cut fraud to tricky service disputes. It fills the gaps that Stripe's program was never really designed to cover.

Automating the Fight for Every Single Dispute

The real difference-maker here is the automation and scope. While Stripe’s service is great for covering the cost of eligible fraud claims, it doesn't do a thing for the majority of other disputes. I'm talking about claims over product quality, services not rendered, or that all-too-common problem of "friendly fraud." These are the chargebacks you’re still stuck fighting by hand, which drains your time and your bank account.

This is exactly the problem ChargePay was built to solve. It plugs directly into your Stripe account and uses AI to automate the entire dispute response process for all kinds of chargebacks.

Here’s a glimpse of what that looks like in practice:

- Automatic Evidence Gathering: The second a chargeback hits, ChargePay’s AI springs into action. It instantly pulls all the relevant data from your Stripe account and any other platforms you’ve connected.

- Compelling Response Generation: Next, it builds a customized, evidence-backed dispute response specifically tailored to the chargeback's reason code. No templates here.

- Automated Submission: Finally, the fully-formed response is automatically submitted to the bank on your behalf. All of this happens without you lifting a finger.

To truly go beyond Stripe's built-in features, an AI-powered solution needs to connect with different data sources seamlessly. This often relies on slick data communication methods, like a solid webhook integration, to make sure real-time data flows smoothly for instant and accurate dispute responses.

Recovering Revenue You Thought Was Lost

At the end of the day, the goal is simple: get more of your revenue back with way less effort. Because ChargePay fights every single dispute—not just the narrow slice covered by Stripe’s program—it opens up a whole new stream of reclaimed income. It’s especially potent against friendly fraud, where a legitimate customer disputes a valid charge.

The Power of AI: By analyzing thousands of data points from past disputes, ChargePay's AI has learned what kind of evidence makes banks tick. It knows how to craft arguments that have the highest probability of winning, seriously boosting your success rate on claims you might have lost or not even bothered to fight before.

This intelligent approach means you stop leaving money on the table. For a deeper dive into how this all works, check out our guide on how AI technology can catch chargeback fraud and bolster your defenses.

By pairing Stripe's fraud protection with ChargePay's all-encompassing automation, you create a powerful, two-layered defense that saves you time, recovers more revenue, and protects your business from every angle.

Got Questions? We’ve Got Answers.

Jumping into any new service, like Stripe Chargeback Protection, is bound to bring up a few questions. That's completely normal. Let's walk through some of the most common things merchants wonder about so you can get a crystal-clear picture of how it all works.

Do I Have to Sign Up for Stripe Chargeback Protection?

Nope, you don't. Stripe Chargeback Protection is a purely opt-in service, meaning it's not turned on by default. You have to go into your Stripe Dashboard and actively enroll.

Before you do, it's smart to weigh the 0.4% per-transaction fee against your current fraud situation. Is the cost a fair trade for the peace of mind it offers? Because it isn't automatic, the ball is entirely in your court.

Can I Use This With My Shopify Store?

Yes, you can, but there's one major string attached. The protection only kicks in for sales processed directly through Stripe Checkout.

So, if you’re using Shopify, you need to make sure your payment integration is set up to use Stripe’s own hosted payment pages. If you use another gateway or a custom setup that sidesteps Stripe Checkout, those transactions won't be covered. The protection is tied to Stripe's advanced fraud tools, which live inside their checkout experience.

What Happens if I Hit My Annual Protection Limit?

This is a really important detail to grasp. Stripe puts a yearly cap on the total amount of chargebacks they'll cover for you. For businesses in the US, that limit is $25,000.

Once you hit that $25,000 ceiling in covered fraudulent chargebacks, the protection essentially goes dormant until the next year. Any fraudulent disputes you get after that point are on you to handle, and that includes paying the standard $15 dispute fee for each one. It's a good idea to keep an eye on your dispute dashboard to see how close you're getting to the limit.

Important Takeaway: Think of the annual limit as a hard stop. If you deal with a high volume of fraud and think you might blow past that cap, you'll need another plan in place to handle the disputes that Stripe won't cover.

Does This Protection Cover Every Single Chargeback?

This is probably the biggest "gotcha" of the whole program: no, it absolutely does not. Stripe Chargeback Protection only covers disputes that have a "fraudulent" reason code. It’s built specifically for those classic cases where a card was stolen and used without the owner's permission.

It will not help you with chargebacks related to:

- Product issues (like "item not as described")

- Service complaints (e.g., "service not provided")

- Subscription cancellations gone wrong

- Friendly fraud, where a real customer disputes a charge they actually made

For all those other, much more common, types of disputes, you’re back in the ring, fighting the chargeback on your own and eating the loss if you don't win.

While Stripe’s protection is a decent starting point, it leaves you vulnerable to the vast majority of dispute types. For complete, hands-off automation that fights every single chargeback—from friendly fraud to service claims—ChargePay is the real solution. Our AI-powered system plugs right into Stripe to recover up to 80% of your lost revenue, all without you lifting a finger.

Protect your revenue and automate your chargeback defense with ChargePay today!

.svg)

.svg)

.svg)

.svg)