So, you've spotted a wonky charge on your credit card statement and you're wondering, "How long do I have to fight this thing?" The short answer is you generally have about 120 days from the transaction or delivery date to file a chargeback, but it's rarely that simple.

Think of it less as a hard deadline and more as a flexible window. The exact amount of time you have can shift based on your card network (like Visa or Mastercard), your bank's specific policies, and, most importantly, why you're disputing the charge in the first place. Acting fast is always your best bet.

Why Chargeback Time Limits Are Not Simple

That "time limit for a credit card chargeback" isn't a single, straightforward number. It's a moving target, and understanding what makes it move is key to getting your money back.

Imagine it's a countdown clock. For a product that never showed up at your door, that clock might start ticking on the expected delivery date, not the day you ordered it. If it's a fraudulent charge you just discovered, the clock starts the moment you spot it on your bill.

Key Factors That Influence Your Deadline

These rules exist for a good reason: they give you a fair shot at disputing errors while also protecting merchants from having to deal with ancient claims. The big card networks set the overarching guidelines, but don't be surprised if your own bank has slightly tighter rules.

Here are the main moving parts that determine your specific window to act:

- The Card Network: Visa, Mastercard, and American Express each have their own rulebooks. They're often similar, but the devil is in the details.

- The Reason for the Dispute: A chargeback for a busted gadget will have a different timeline than one for a stolen card number.

- The Transaction Date vs. Delivery Date: The clock doesn't always start when you pay. For services or goods delivered later, it might start when the item was delivered or when the service was supposed to happen.

The Fair Credit Billing Act (FCBA) gives you a legal safety net, requiring you to dispute billing errors within 60 days of receiving the statement. But here's the good news: the card networks usually give you a more generous window, often landing around that 120-day mark.

Getting a handle on these factors cuts through the confusion. It gives you a clear roadmap to follow, ensuring you don't miss your chance to reclaim your funds.

Chargeback Time Limits at a Glance

To make things a bit clearer, let's break down the typical time limits you can expect from the major players for some common dispute scenarios. Keep in mind, these are general guidelines—your specific situation could still vary.

This table gives you a solid starting point. The key takeaway? The clock is ticking, but you usually have a decent amount of time to get your dispute filed. The most important thing is to take action as soon as you realize there's a problem.

How Major Card Networks Set Their Deadlines

When you're staring at a frustrating charge on your statement, the situation feels incredibly personal. But the rules dictating your time limit for a credit card chargeback aren't set by your bank—they come from the massive networks behind the logo on your card, like Visa, Mastercard, and American Express. Each one plays by its own rulebook, which means the deadline to act can change depending on which piece of plastic you used.

Think of these networks as different sports leagues. While the goal is the same (settling disputes fairly), the exact rules of the game can vary. One network might give you a pretty generous window for a certain type of dispute, while another could be much stricter.

Visa and Mastercard Timelines

For the most part, Visa and Mastercard operate in the same ballpark. They generally give cardholders up to 120 days to file a chargeback for common problems like outright fraud or products that just never showed up. This 120-day clock usually starts ticking from the date the transaction was processed or from the day you expected to get your hands on your goods or services.

But here's the catch: the reason for your dispute is a huge factor. The time limits for credit card chargebacks can shrink depending on the specifics of what went wrong. For instance, Visa's 120-day window can drop to just 75 days for issues like a declined authorization that still got charged to your account.

In a similar vein, Mastercard might shorten its 120-day limit to 45 days if the problem is tied to a lost or stolen card. These different timelines are all about balancing consumer rights with merchant protection, so getting a handle on them is crucial.

The American Express Approach

American Express has built a reputation for its customer-first policies, and this often shines through in its dispute process. While they've moved closer to the 120-day standard for many types of disputes, their internal systems can sometimes offer a bit more flexibility.

Unlike Visa and Mastercard, which act as go-betweens for thousands of different banks, Amex is both the network and the bank that issues the card. This structure gives them more direct control over the whole process. Because of this, it's always smart to understand the specific nuances of their system. If you're an Amex cardholder, it's worth checking out our guide on American Express chargeback time limits.

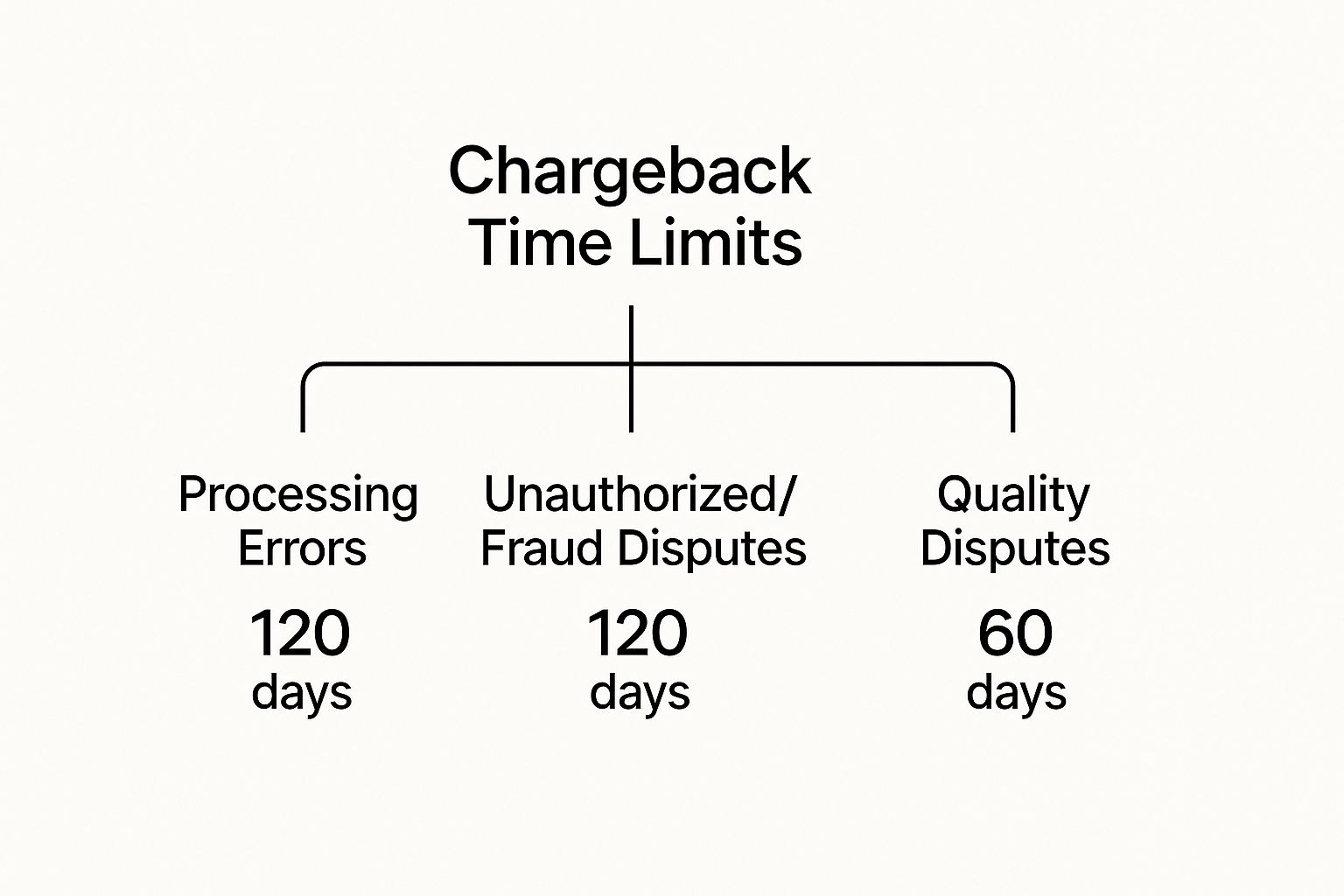

This diagram gives you a quick visual of how different dispute types can have wildly different timelines, even within the same network.

As the image shows, while things like processing errors and fraud often share a 120-day window, a dispute over the quality of a product could have a much tighter deadline.

Key Takeaway: Never assume the time limit is the same for every situation. The type of dispute you file directly impacts how fast that countdown clock is ticking, and knowing these differences can be the deciding factor in whether you get your money back. Your card's network sets the maximum time allowed, but the nature of your claim determines your actual deadline.

Why Your Reason for the Dispute Matters

Not all disputes are created equal, and the reason you file a chargeback is a massive factor in determining your deadline. Think of the time limit for a credit card chargeback as a flexible rule, not a concrete one. The clock doesn't always start ticking the moment you swipe your card.

Instead, it often begins when you could have reasonably known there was a problem. This whole system is built around fairness. After all, you can’t know a product is defective until it arrives, and you definitely can't report a fraudulent charge until you see it pop up on your statement.

The card networks get this. That’s why they have different timelines for different situations, all neatly categorized by what the industry calls reason codes.

When the Countdown Clock Actually Starts

Figuring out the starting point of your dispute window is arguably the most important detail. Getting this wrong could mean you miss your deadline entirely. For some issues, the clock begins immediately. For others, it’s delayed until a specific event happens—or, more accurately, fails to happen.

Here’s a breakdown of common scenarios and when their clocks typically start ticking:

- Unauthorized Transaction: The clock starts from the date the transaction appears on your statement. You can’t dispute a charge you don’t know about, so the timeline is tied to the moment you were notified.

- Product Not Received: The countdown begins on the expected delivery date. If a merchant promised your package by June 15th and it's a no-show, your 120-day window starts from that date, not when you placed the order back in May.

- Defective Merchandise: The timeline usually starts from the date you received the item. This gives you a fair shot to open the package and realize the product doesn’t work as advertised.

- Recurring Billing Error: For that gym membership you canceled but were still charged for, the clock starts on the date of that specific incorrect billing.

Common Dispute Scenarios Explained

Let's walk through a few real-world examples to see how this plays out.

Imagine you bought tickets for a concert that was six months away. If the artist cancels a week before the show, your dispute window doesn't start from the day you bought the tickets. It starts from the date the service (the concert) was supposed to be provided.

This is a critical distinction that can extend your time limit for credit card chargeback by months. Another common situation is friendly fraud, where a customer disputes a legitimate charge, sometimes by mistake and sometimes not.

For merchants, understanding these nuances is key to protecting your bottom line. If you're a business owner, learning more about how to spot and fight chargeback fraud is a must.

The Big Picture: The "why" behind your dispute dictates the "when" of your deadline. The system is designed to give you a fair shot by starting the clock only when you could have realistically identified the problem. Always connect your reason for the dispute to the appropriate starting date to ensure you file within the correct window.

A Global Look at Chargeback Behavior

Chargebacks are a headache for businesses everywhere, but the problem looks wildly different depending on where you are in the world. Things like local laws, how people shop online, and common fraud tactics all stir the pot, creating unique chargeback situations from one country to the next.

If you’re a merchant selling across borders or a shopper buying internationally, getting a handle on these global dynamics is essential. It explains why some international orders get flagged for extra scrutiny and why banks are so laser-focused on fraud prevention. It's a fascinating peek into how economics and culture shape risk, showing that the same transaction can be perfectly safe in one country and a huge gamble in another.

Why Geography Changes the Game

The differences from country to country can be massive. Chargeback rates swing wildly, painting a clear picture of the risks merchants are up against. As of mid-2023, the global average for chargebacks hovered around 0.60% of all credit card transactions.

But that's just an average. Take a look at the extremes:

- Brazil is grappling with one of the highest rates at a staggering 3.48%.

- Mexico isn't far behind, with a rate of 2.81%.

- Meanwhile, major economies like China and Japan have incredibly low rates, around 0.18%.

- The United States sits somewhere in the middle at about 0.47%.

You can dig into more of these numbers over at clearlypayments.com. This kind of data is gold for merchants, helping them figure out where to beef up their fraud prevention and where they can breathe a little easier. There's a clear trend here—emerging markets with booming e-commerce often get hit with higher chargeback rates as fraudsters flock to new opportunities and shoppers dispute deliveries more often.

High-Risk Industries and International Sales

Some industries are just natural magnets for disputes, and that risk gets amplified when you start selling internationally. The travel sector, for instance, is famous for its high chargeback numbers, fueled by cancellations, service disagreements, and the sheer complexity of cross-border payments.

For merchants, selling globally isn't just about shipping products; it's about understanding and managing a diverse range of consumer behavior and risk. A strategy that works in a low-dispute country like Japan will likely fail in a high-dispute market like Brazil.

Businesses selling digital goods or services face their own set of headaches. How do you prove you delivered something that isn't physical? It's tough, and that ambiguity makes these transactions a prime target for friendly fraud—when a customer disputes a charge they actually made. This problem gets even trickier when you factor in different cultural norms around online shopping and what consumers feel they're entitled to.

If you're in one of these high-risk fields, you can't just wing it. You need a solid game plan. Successfully navigating these challenges means getting a deep understanding of international payment trends. You can get a closer look at how specific sectors deal with this by reading about chargeback management in the travel industry.

At the end of the day, while the time limit for credit card chargeback rules from the card networks are the same for everyone, the human behaviors driving those chargebacks are intensely local.

Practical Steps for Consumers and Merchants

Knowing the rules of the game is one thing, but playing it well is another. Whether you’re a cardholder who’s just spotted a sketchy charge or a merchant trying to protect your bottom line, what you do—and when you do it—is everything. The time limit for a credit card chargeback waits for no one, so being prepared can be the difference between a win and a loss.

For both sides of the transaction, a proactive mindset is your best bet. Handling disputes the right way from the start saves time, money, and a whole lot of future headaches.

Actionable Advice for Consumers

Before you dial up your bank, take a deep breath. A little prep work can make your dispute almost bulletproof. Your mission is to build such a clear, undeniable case that the bank has no choice but to rule in your favor.

Here’s a quick game plan to follow:

- Talk to the Merchant First: This is square one. Your bank is almost guaranteed to ask if you've tried sorting it out with the seller directly. A quick email or phone call is often the fastest path to a refund and can solve the whole mess without a formal chargeback.

- Gather Your Evidence: It’s time to become a detective. Collect every piece of paper and digital trail you can find. We're talking receipts, order confirmations, shipping info, photos of a broken product, and any emails or chat logs with the merchant.

- Move Quickly: Sure, you might have up to 120 days, but don’t let that lull you into waiting. The sooner you report the problem, the more credible your claim looks. Memories fade and records get buried, so file that dispute as soon as your evidence is in order.

Proactive Strategies for Merchants

For merchants, the best defense is a great offense. Preventing chargebacks before they even start is way more effective—and cheaper—than fighting them later. Think of stellar customer service and crystal-clear communication as your secret weapons.

The most successful merchants are obsessed with the customer experience, from the first click to post-purchase support. If you make it easy for customers to get help, you slash the odds they’ll ever feel the need to file a chargeback.

This proactive approach has never been more critical. We’re seeing a massive surge in chargeback activity, particularly for online stores and travel companies. The travel industry was hit with a staggering 816% increase in chargebacks in the first quarter of 2024 compared to last year, and e-commerce disputes weren't far behind with a 222% jump.

When a dispute finally does hit your dashboard, your response needs to be just as organized as the consumer's claim. You need to fire back with compelling evidence that proves the charge was legit—think proof of delivery, signed receipts, or customer service logs. If you're looking for more ways to fortify your business, our guide on how to avoid chargebacks is packed with valuable strategies.

Just remember, a swift, well-documented response is your best shot at winning.

Common Questions About Chargeback Time Limits

Navigating the rules around the time limit for a credit card chargeback can feel a bit like trying to solve a puzzle. To clear up any lingering confusion, let's tackle some of the most common questions that pop up for both consumers and merchants.

What Happens If I Miss the Chargeback Deadline?

Simply put, you're likely out of luck. If you miss the filing deadline set by your card network, you generally lose your right to dispute the charge through the official chargeback system. Your bank's hands are tied at that point.

This is exactly why acting quickly is so critical. Your only remaining option is to try and resolve the issue directly with the merchant, but without the leverage of a potential chargeback, this can be much more difficult.

Does the Clock Start from the Transaction or Delivery Date?

This is a fantastic question, and the answer depends entirely on why you're filing the dispute. The system is designed to be fair, so the clock doesn't always start ticking the moment you pay.

- For issues like fraud or billing errors, the timeline usually starts the moment the transaction is posted to your statement.

- For problems with goods or services, the clock often starts from the date you received the item or when the service was supposed to happen.

This distinction is crucial because it can significantly extend your filing window, especially for items you've ordered well in advance.

Can a Merchant Change the Chargeback Time Limit?

Not a chance. A merchant has absolutely no power to change the official chargeback time limit. These deadlines are set and enforced by the credit card networks like Visa and Mastercard, not individual businesses.

While a merchant can always offer you a refund or store credit outside of the formal process, they can't alter the bank's official dispute window. Their return policy and the chargeback timeline are two completely separate things.

It's a common misconception, but a store's 30-day return policy has no bearing on your 120-day chargeback window. The chargeback is a right granted by your card issuer, not the retailer.

Are the Time Limits the Same for Debit and Credit Cards?

They are often similar but are governed by different federal laws, which is a key difference. Understanding this can help you decide how to pay for major purchases.

Credit card chargebacks are primarily protected by the Fair Credit Billing Act (FCBA), which offers robust protections and generally longer timeframes. On the other hand, debit card disputes fall under the Electronic Fund Transfer Act (EFTA). This law has different rules and often features shorter, stricter deadlines for reporting issues. Because of this, using a credit card can offer an extra layer of security for purchases where a dispute might be likely.

Ultimately, winning a dispute often comes down to presenting a clear, well-documented case within the correct timeframe. For a deeper dive into crafting a winning argument, check out our guide on how to win a credit card dispute.

Stop losing revenue to confusing chargeback rules. ChargePay uses AI to automate the entire dispute process, generating winning responses and recovering up to 80% of your lost funds—all without any manual work. Protect your business and get started today at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)