A credit card chargeback doesn't last forever—not even close. Generally, the clock runs out after about 120 days from the transaction or delivery date. Think of it as a built-in safety net for everyone involved in online shopping. It gives both customers and merchants a clear, defined window to sort out disputes without leaving things hanging forever.

The Chargeback Clock: What Every Merchant Needs to Know

So, what is a chargeback time limit? At its core, it’s a deadline. It dictates exactly how long a cardholder has to formally dispute a transaction with their bank. This is a fundamental rule in the world of payments, and it’s there for a good reason: to create a fair and predictable process for everyone.

Imagine a world without these deadlines. A business could be hit with a chargeback months, or even years, after a sale. That kind of uncertainty would be a nightmare for accounting and business planning.

This "chargeback clock" really serves two key purposes:

- For Customers: It gives them a reasonable amount of time to spot and report problems. Maybe it was a fraudulent charge they didn't notice right away, a product that never showed up, or a service that wasn't what was promised.

- For Merchants: It draws a line in the sand. Once that window closes, you can finally close the books on that sale with confidence, knowing it's not going to suddenly reappear as a liability.

Understanding the Standard Timelines

Across the globe, the major card networks like Visa and Mastercard are the ones who set the maximum timeframes. This deadline is one of the most critical pieces of the entire dispute puzzle. The industry standard is typically 120 days from the original transaction date or the expected delivery date for a customer to file a chargeback. This timeline is all about striking a balance—protecting consumers without putting an endless burden on merchants.

But, as with most things in the payments world, the devil is in the details. The specific rules can vary slightly from one card network to another.

To give you a quick cheat sheet, here's a look at the standard filing deadlines for the big players.

Standard Chargeback Filing Deadlines by Card Network

This table gives you a quick summary of the typical time limits cardholders have to file a chargeback with major credit card companies.

Keep in mind, these timelines are just the starting point. As we’ll explore, the specific reason for the dispute can sometimes shift these deadlines.

To really get into the weeds of how these rules work in practice, you can dive deeper into our guide on the https://www.chargepay.ai/blog/visa-chargeback-time-limit. And if you're curious how chargebacks fit into the bigger picture of financial tech, especially within the broader landscape of AI-driven payments, that article offers some great context.

Why Chargeback Deadlines Are Necessary

Chargeback time limits aren't just some arbitrary rule the card networks came up with. They're the guardrails that keep the entire payment system fair, stable, and predictable for everyone involved. Think of them as a statute of limitations for transactions—a way to ensure disputes have a clear beginning and a definite end.

Without these deadlines, we’d be in a state of chaos. Imagine endless, open-ended disputes popping up without warning. It just wouldn't work.

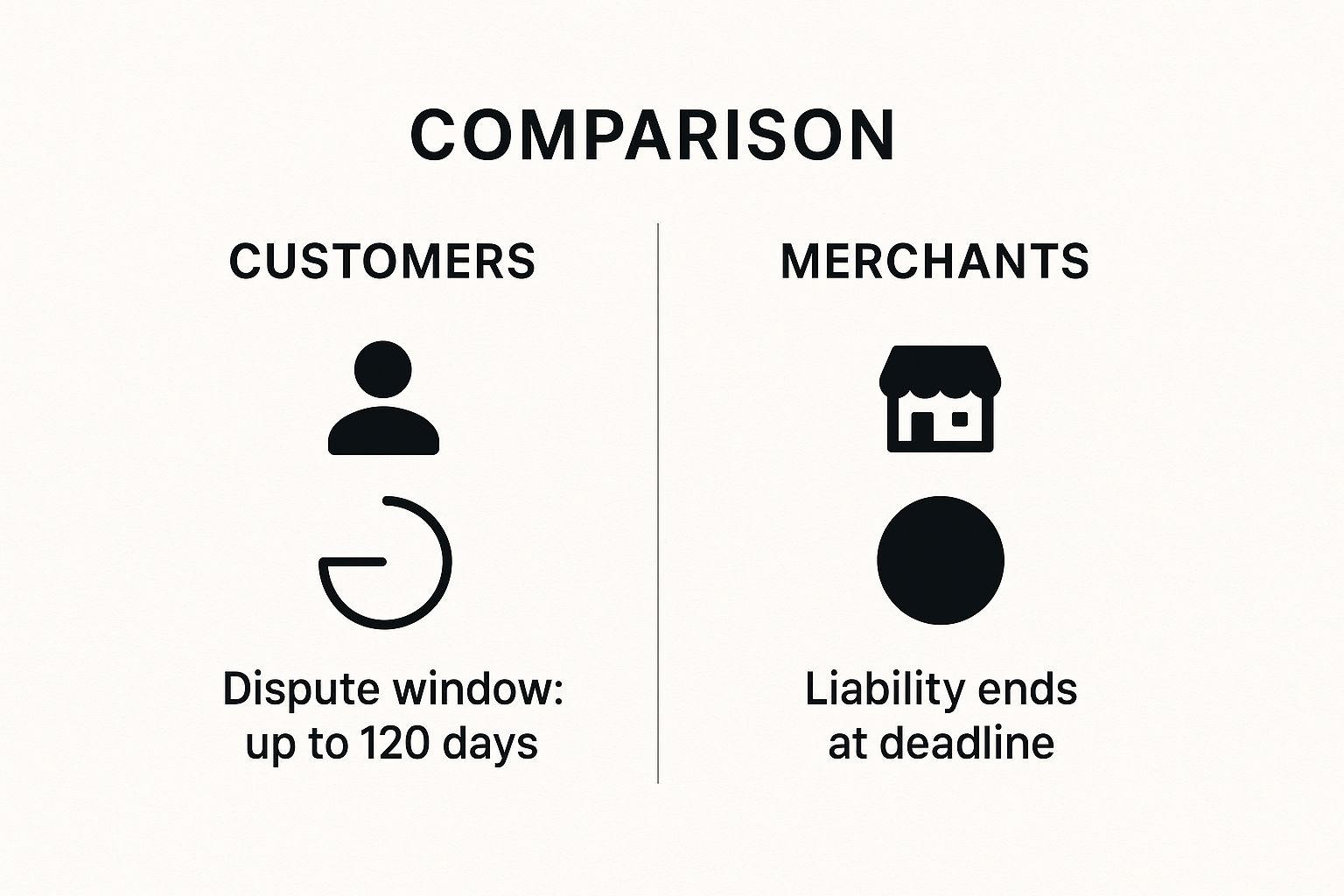

For your customers, these timelines are a critical safety net. They get a reasonable window of time, often up to 120 days, to spot and act on a problem. This could be anything from a fraudulent charge they didn't make to a product that never showed up on their doorstep. This protection is a huge part of what makes people feel safe using their cards online.

But this is a two-way street. These deadlines are just as important for you, the merchant. They prevent the absolute nightmare scenario of a transaction from months—or even years—ago suddenly clawing its way back as a chargeback. This finality is what allows you to close your books with confidence, knowing that your past revenue is actually secure.

This infographic really drives home how these deadlines create a balance, protecting both sides of the transaction.

It’s all about creating a predictable framework where both consumers and merchants know exactly where they stand.

Pushing for a Quick Resolution

At the end of the day, these deadlines encourage everyone to sort things out quickly. When both you and your customer know there's a clock ticking, it lights a fire under everyone to communicate and find a solution. It stops minor issues from dragging on forever and becoming major headaches.

This structure is vital for the health of the whole system. The average chargeback in the U.S. was around $110, with some industries seeing that number creep closer to $120. Now, consider that global payment volume is expected to blast past $79 trillion by 2030. Without these orderly timelines, managing fraud losses at that scale would be impossible. If you want to dive deeper, you can read more about these chargeback statistics and trends to see just how big the challenge is.

By setting clear boundaries, the time limit on credit card chargebacks keeps the system from grinding to a halt. It’s the mechanism that keeps transactions flowing smoothly and fairly for millions of businesses and their customers every single day.

Take these rules away, and financial planning becomes a guessing game for merchants. Worse, the trust that consumers have in digital payments would quickly start to crumble.

Breaking Down the Timelines for Each Card Network

That general 120-day rule is a great starting point, but let's be honest—when a chargeback notice lands on your desk, you need the specifics, not generalities. Each major card network—Visa, Mastercard, American Express, and Discover—plays by its own set of rules.

Getting these details right isn't just good practice; it's essential for protecting your revenue.

One of the trickiest parts is figuring out when the chargeback clock actually starts ticking. It’s not always the day of the transaction. For items with delayed shipping, the countdown might begin on the expected delivery date. In other cases, it could even start when a customer first discovers a problem with a product or service, sometimes weeks or months later.

But here’s the real kicker: your side of the equation has a much tighter deadline. While a customer might have months to file, you often have just 30 to 45 days to respond. This is why having a clear, quick-reference guide is so valuable.

Comparing the Major Card Networks

Let's get into what you can expect from each of the big players. The core ideas are similar, but the slight differences in their processes can make or break your dispute.

Visa: Cardholders generally get 120 days to file a dispute from the transaction date or expected delivery. As a merchant, your response window is a firm 30 days. Visa's system is highly structured, so hitting that deadline is non-negotiable.

Mastercard: Like Visa, Mastercard gives cardholders a 120-day window for most disputes. They’re a bit more generous on the merchant side, though, giving you 45 days to prepare and submit your case.

American Express: Amex also sticks to the 120-day rule for cardholders. But for merchants, the window shrinks to just 20 days. Amex is famous for its customer-centric approach, which makes a strong, timely response from you even more critical. You can get a deeper look at the specifics in our complete guide to American Express chargeback time limits.

Discover: Discover gives its cardholders up to 120 days to kick off a chargeback. Merchants responding to a Discover dispute also face a tight 20-day window to submit their evidence.

The key takeaway here is simple: your time to act is always much, much shorter than the customer's. If you miss your response deadline, it’s almost always an automatic loss. The funds go back to the customer, and you lose the sale for good.

Card Network Chargeback Deadlines At a Glance

To make these different rules easier to track, we've put together a simple comparison table. Think of this as your cheat sheet for whenever a new dispute notification comes in.

Getting a handle on these timelines is the first step toward building a successful chargeback management strategy. When you know exactly how much time you have, you can gather your evidence, build a compelling case, and respond with confidence before the clock runs out.

When the Standard Time Limits Change

While the 120-day rule is a solid benchmark for credit card chargebacks, it’s far from absolute. You can't just circle a date on the calendar and assume you're in the clear. Several common business scenarios can shift this timeline, sometimes stretching it out much longer than you'd expect.

These aren't rare, obscure cases; they happen every day. For merchants, this means the chargeback clock doesn't always start ticking the moment a transaction is approved.

Thinking of the 120-day window as a fixed countdown from the purchase date is one of the biggest mistakes you can make. The system is actually more flexible, designed to protect consumers in situations where a problem isn't immediately obvious.

Scenarios That Extend the Chargeback Clock

The start date for the chargeback countdown is often tied to a "triggering event," which is not always the initial purchase. This is where things can get a bit more complex.

Here are a few real-world examples that alter the typical deadline:

- Delayed Delivery or Pre-Orders: If a customer pre-orders a product that ships three months later, the 120-day clock doesn’t start until the expected delivery date. A dispute filed four months after the purchase could still be perfectly valid.

- Recurring Subscriptions: For a monthly subscription service, the clock effectively resets with each new billing cycle. A customer can dispute the most recent charge, even if they’ve been a subscriber for years.

- Services Rendered in the Future: Think about concert tickets or a vacation package bought six months in advance. The time limit begins after the event or trip was supposed to happen, not when the tickets were bought.

Latent Defects and Quality Issues

Another important exception involves products with hidden flaws. Sometimes, a defect isn’t discovered until weeks or even months after the purchase.

Imagine a customer buys an electronic gadget. It works perfectly for three months, but then it suddenly stops functioning due to a manufacturing fault. In this case, the chargeback clock may start from the date the defect was discovered, not the date of purchase. This gives the cardholder a fair chance to act when a product fails to live up to its promise over time.

These exceptions underscore a crucial point: the chargeback system is designed around the customer’s experience, not just the merchant’s transaction date. This ensures fairness when the value of a purchase isn't realized until much later.

Understanding these nuances helps you build a more robust dispute management process. Before you write off a chargeback as invalid just because of its timing, always check if one of these exceptions applies.

Knowing the difference between a standard dispute and one of these special cases is the first step in building a strong response. For more clarity on how it all begins, it helps to understand the differences between retrieval requests vs chargebacks. It can provide context on how these timelines are initiated.

How to Manage Disputes and Meet Your Deadlines

Knowing the rules is one thing, but actually managing disputes to hit your deadlines is where you protect your revenue. Staying organized and acting fast is your best defense against losing a chargeback simply because the clock ran out. It all starts with being proactive.

Don't wait for a letter in the mail. Seriously. The moment a dispute is filed, you need to know about it. Setting up instant notifications through your payment processor is the first and most critical step. This ensures the countdown doesn’t start without you even knowing the race has begun.

Create a Response Playbook

Once that notification hits your inbox, you have to move quickly. Having a pre-made checklist of compelling evidence saves precious time and stops you from scrambling to find what you need at the last minute.

Your evidence checklist should absolutely include:

- Proof of Delivery: Always have shipping confirmations and tracking numbers ready to go.

- Customer Communications: Save any emails or chat logs that show a positive interaction or confirm the customer received their order.

- Order and Transaction Details: Keep clear records of the purchase, including the results of any AVS/CVV checks.

A central system to track every dispute's due date is non-negotiable. A simple spreadsheet or specialized software can be the difference between a win and an automatic loss.

To speed things up even more, create some response templates. While every case needs a personal touch, a template with the basic structure and placeholders for evidence means you never start from scratch. This consistency helps you build a strong, professional case every single time. A solid strategy for chargeback dispute management is the foundation of this entire process.

Ultimately, getting a handle on disputes and deadlines comes down to having solid systems. It might be worth researching the best payment processing for small business solutions to streamline your operations and give you the tools you need to stay on top of every deadline.

Frequently Asked Questions About Chargeback Times

Navigating the world of chargebacks can feel like you're constantly racing against the clock. Even when you think you've got the basic rules down, tricky situations pop up that leave you scrambling for answers.

Let's clear up some of the most common questions we hear from merchants.

What Happens if a Merchant Misses the Response Deadline?

If you miss the deadline to respond, it's almost always an automatic loss. It’s that simple. The bank immediately returns the disputed funds to the cardholder, and you lose the sale without any chance to appeal.

This is exactly why reacting quickly is so critical to protecting your revenue.

Think of your response window as a non-negotiable appointment. If you miss it, the decision gets made without you, and it's never going to be in your favor.

Can a Chargeback Be Filed After 120 Days?

Yes, it absolutely can. While 120 days is the standard benchmark you hear about, the clock doesn't always start on the day of the transaction.

For example, say a customer bought concert tickets six months in advance. The filing window would likely start after the concert was scheduled to happen, not when they bought the tickets. Exceptions like this exist, though they are less common than the standard timelines.

Does the Chargeback Reason Affect the Time Limit?

It sure does. Every dispute comes with a "reason code," and these codes often have their own specific deadlines. A simple billing error might have a much shorter timeline than a claim that goods were never delivered.

The card network rulebooks spell out all of these specific timelines. That’s why the very first thing you should do is identify the reason code. Understanding your full chargeback rights and how they link to these codes is essential for building a case you can actually win.

Don't let confusing deadlines and manual processes drain your resources. ChargePay uses AI to automate your chargeback responses, ensuring you never miss a deadline and recovering up to 80% of your lost revenue. Protect your business today at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)