A bank chargeback is one of the most powerful tools you have as a consumer. It reverses a credit or debit card transaction, pulling money from the merchant’s account right back into yours.

Think of it as your bank stepping in as a referee when a purchase goes wrong. Maybe the product was faulty, a service wasn't delivered as promised, or you spotted a fraudulent charge. The key thing to remember is that this process is different from a standard refund, which you’d sort out directly with the business.

Understanding What a Bank Chargeback Is

Let's say you order a new pair of headphones online, but the package that arrives is completely empty. You try contacting the seller, but all you get is silence. This is the exact scenario where a bank chargeback becomes your best friend.

It’s a formal dispute you kick off with your bank to get your money back when a merchant doesn’t hold up their end of the bargain.

This consumer safety net was created to build trust in card payments, giving people the confidence to shop without worrying about being left out of pocket by dishonest sellers. But as e-commerce has grown, the system has become way more complex. Global chargeback cases are projected to hit a staggering 337 million—that's a 27% jump in just a few years.

This surge isn't just a headache; it's a massive financial drain, with the total value of these disputes expected to reach $41.7 billion soon.

Who Is Involved in the Chargeback Process?

A chargeback isn't a simple two-way street between you and the business. There are several players in the game, each with a specific role. Knowing who’s who helps make sense of why the process can sometimes take weeks, or even months, to finally resolve.

To clear things up, let's break down the main parties involved in a typical chargeback.

The Key Players in a Bank Chargeback

Each player has a part to play, which is why the gears of the chargeback machine can sometimes turn slowly.

One of the most common points of confusion is telling a chargeback and a refund apart. While both get your money back, a refund is a friendly agreement between you and the merchant. A chargeback, on the other hand, is a formal fight refereed by the banks. For a deeper dive, check out our guide on the key differences between a chargeback vs a refund.

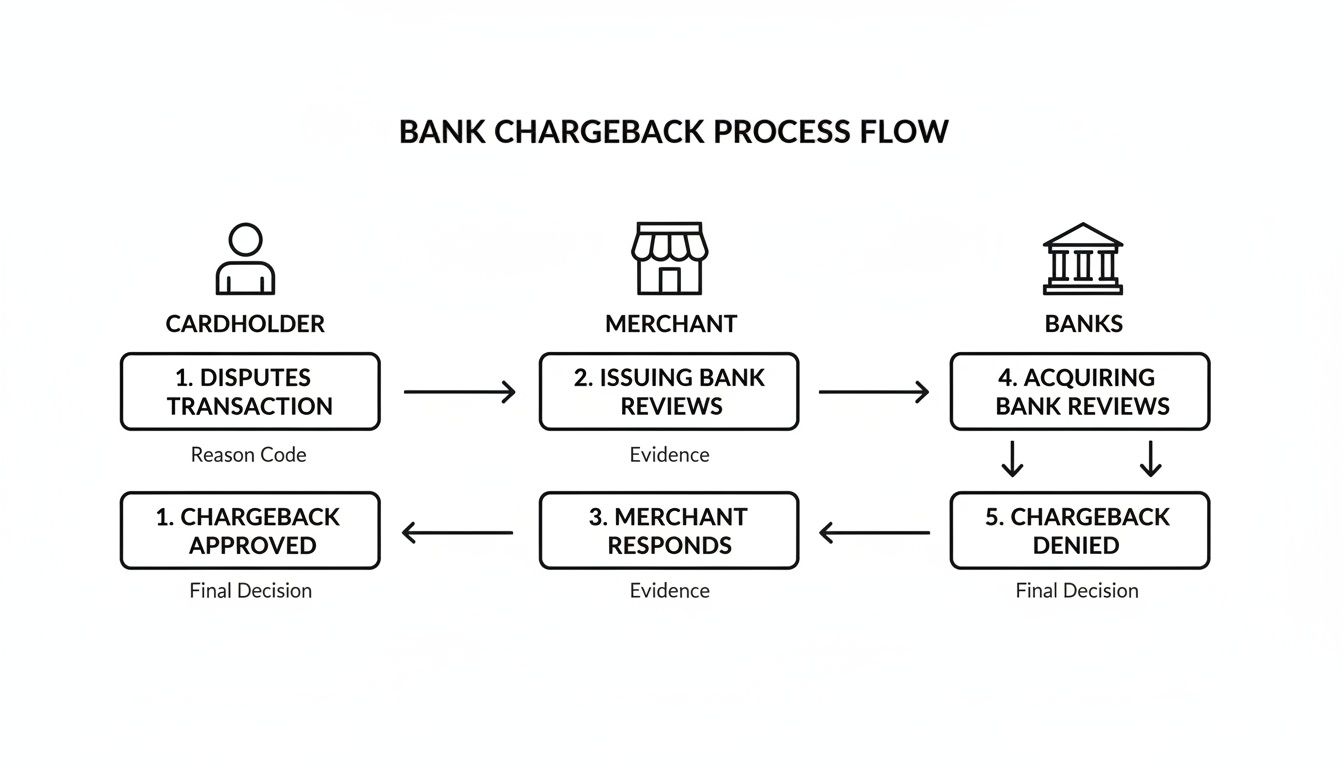

The Step-by-Step Chargeback Process Unpacked

When a customer disputes a transaction, it kicks off a formal, multi-stage process that can feel pretty confusing for everyone involved. It’s not an instant reversal. Instead, think of it as a relay race where a message and funds are passed between several key players—the cardholder's bank, the merchant's bank, and the merchant themselves.

Getting a handle on this journey is key, whether you're a customer wondering why your money hasn't reappeared or a business owner trying to figure out your next move. The whole thing is governed by strict rules and deadlines set by card networks like Visa and Mastercard.

This visual guide breaks down the typical flow of a bank chargeback, showing how the dispute moves from the cardholder to the merchant and back.

As you can see, a chargeback is a complex back-and-forth, not just a simple one-way street from the bank to the merchant.

Stage 1: The Customer Files a Dispute

It all starts when a cardholder contacts their bank—the issuing bank—to dispute a charge. They might call the number on the back of their card or log into their online banking portal. They have to provide a valid reason, like an unauthorized transaction, a product that never showed up, or a service that wasn't what was promised.

The bank takes a look at this claim. If it lines up with one of the official chargeback reason codes set by the card network, the process moves forward. At this early stage, most banks will give their customer the benefit of the doubt and proceed.

Stage 2: The Issuing Bank Investigates

Once the dispute is validated, the issuing bank usually issues a provisional credit to the cardholder's account for the disputed amount. This credit is temporary and can be yanked back later depending on how the case turns out. It's important to remember this isn't the final refund.

Next, the issuing bank officially files the chargeback through the card network (like Visa or Mastercard). The network then passes the chargeback along to the merchant's bank, which is known as the acquiring bank.

A common misconception is that the provisional credit means the customer has won. In reality, it’s just the bank holding the funds in limbo while the investigation unfolds. The final decision is still weeks, or even months, away.

The acquiring bank gets the chargeback notification and immediately debits the disputed funds from the merchant's account. They also tack on a separate chargeback fee, which can run anywhere from $15 to over $50. This fee is non-refundable, even if the merchant ultimately wins the dispute. Ouch.

Stage 3: The Merchant Responds

The acquiring bank then alerts the merchant about the chargeback. This is often the first time the business owner even learns there was a problem. From this point, the merchant is on the clock with a specific timeframe to respond, typically between 20 to 45 days.

The merchant now has two choices:

- Accept the Chargeback: If the customer's claim is valid or the merchant doesn't have the evidence to fight it, they can accept it. The provisional credit to the cardholder becomes permanent, and the case is closed.

- Fight the Chargeback: If the merchant believes the charge is legitimate, they can challenge the dispute. This is a process called representment.

Representment is all about gathering compelling evidence to prove the transaction was valid. This could be anything from shipping confirmations and delivery signatures to customer service emails or proof that a digital product was downloaded. To get a better grip on this part of the journey, you can learn more about the complete card dispute process and what it takes to build a winning case.

Stage 4: The Final Decision

The merchant bundles up their evidence and submits it to their acquiring bank. The bank then passes it back to the issuing bank through the card network. Now, it's up to the issuing bank to review all the evidence and make a final call.

If the merchant’s evidence is strong enough to poke holes in the cardholder's claim, the bank will reverse the chargeback. The money is returned to the merchant's account, and the provisional credit is taken back from the cardholder's account.

But if the bank sides with the cardholder, the chargeback stands, and the money is gone for good. In some rare cases, a merchant can escalate the dispute to arbitration, where the card network makes a final, binding decision. But be warned—this is a costly and often risky step to take.

Why Do Customers File Chargebacks?

When you hear the term "bank chargeback," it’s easy to think it's all about stolen credit cards. And while criminal fraud is definitely a big piece of the puzzle, it's not the whole story. The truth is, people dispute charges for all sorts of reasons, from legitimate problems with an order to simple, honest mistakes.

For any business owner trying to get a handle on disputes, understanding what triggers them is the first step. Sometimes the issue starts with you, the merchant. Other times it's a technical hiccup. And in the trickiest cases, it’s something else entirely.

Let’s break down the common scenarios that lead a customer to call their bank.

True Fraud and Unauthorized Transactions

This is the classic chargeback scenario. A customer scans their statement and spots a purchase they know they didn't make. Maybe a thief swiped their physical card, or their details were scooped up in a data breach and used for an online shopping spree.

For the cardholder, this is a no-brainer. They report the fraudulent charge, and their bank kicks off a chargeback to get their money back. For merchants, these are nearly impossible to win because the actual cardholder never gave the green light for the transaction in the first place.

Merchant Errors and Service Issues

Not every chargeback is a sign of something sinister. Sometimes, the merchant is genuinely at fault, and the customer files a dispute because they feel like they’ve run out of options. This category covers a whole range of common business slip-ups.

These issues often include:

- Item Not as Described: The customer was excited about a blue sweater but got a green one instead. Or that "high-quality leather" bag they ordered feels more like cheap plastic.

- Product Never Arrived: The tracking says "delivered," but the package is MIA. The customer can't get a straight answer from your support team, and their frustration grows.

- Technical Glitches: A bug on your website accidentally charges a customer twice for the same order.

- Subscription Traps: A customer signs up for a free trial but finds it nearly impossible to cancel before getting billed, leading them to dispute the charge out of sheer frustration.

In most of these situations, a quick refund could have nipped the problem in the bud. But when customer service is slow, hard to find, or just plain unhelpful, a chargeback becomes the customer's last resort. To see a full breakdown of the official reasons banks recognize, you can explore the different reasons for a chargeback.

The Challenge of Friendly Fraud

This is where things get messy. Friendly fraud, sometimes called first-party fraud, is when a customer disputes a legitimate charge that they or someone in their family actually made. It's not always malicious; sometimes, it's a genuine mistake.

A customer might simply forget about a purchase from a few weeks ago or not recognize the business name on their statement. Think about a parent who sees a charge for an in-app game purchase made by their child and immediately assumes it's fraud.

But friendly fraud can also be intentional. A customer might get a case of "buyer's remorse" and decide they want their money back without the hassle of a proper return. They know the chargeback system often sides with the cardholder, so they file a dispute claiming the product never showed up, even when it's sitting in their closet.

This has become a massive headache for online businesses. The retail and e-commerce worlds have seen chargebacks explode, with one recent analysis showing a staggering 233% increase. The most disputed items? Things like clothing and digital subscriptions. This trend is fueled in part by so-called "refund hacks" and a growing willingness to commit friendly fraud, as one-in-five consumers admitted they are more likely to dispute valid charges during tough financial times. You can discover more insights about this surge in retail chargebacks on Payscout.com.

Understanding these different motivations is the key to figuring out how to respond effectively.

How Chargebacks Really Affect a Business

For a business owner, a chargeback notification is more than just an annoying email—it's a gut punch. It’s not just a reversed sale. It’s the start of a costly, time-consuming battle that sends shockwaves through your entire operation. The initial lost revenue is just the tip of the iceberg.

Under the surface, you'll find a tangled mess of hidden fees, administrative headaches, and serious long-term risks. Getting a handle on these impacts is the first step to protecting your business from the real damage chargebacks can inflict.

The Hidden Financial Drain

The moment a customer files a chargeback, your payment processor yanks the disputed amount right out of your account. But it doesn't stop there. They also slap you with a non-refundable chargeback fee, which usually runs anywhere from $15 to over $50 per dispute.

Here's the kicker: you lose that fee even if you fight the chargeback and win. Once you add up the lost sale, the cost of the product, shipping expenses, and that penalty fee, a single chargeback can easily cost you 2-3 times the original transaction amount.

The Time and Labor Black Hole

Fighting a chargeback isn't a simple click of a button. It forces someone on your team to drop everything and play detective, digging through records for compelling evidence.

This isn't a quick search. It involves hours of gathering crucial documents like:

- Order confirmations and transaction receipts.

- Shipping labels and delivery confirmations.

- Customer service emails or chat logs.

- Proof of service or digital download records.

All this evidence has to be packaged into a professional rebuttal letter and submitted before a strict deadline. It's a massive operational drain that pulls you and your team away from what actually matters—growing your business. You can learn more about how much chargebacks hurt businesses in our detailed guide.

Your Chargeback Ratio: The Business Health Score

Maybe the most dangerous threat of all is the damage to your chargeback ratio. Think of this ratio as a "health score" for your business in the eyes of banks and card networks like Visa and Mastercard. It’s calculated by dividing the number of chargebacks you get in a month by your total number of transactions.

If that number creeps too high—typically over 0.9%—alarm bells start ringing. A high ratio tells banks that your business is risky, and that can trigger some severe penalties.

A high chargeback ratio is a major red flag for payment processors. They might hit you with higher transaction fees, force you to keep a larger cash reserve, or, in the worst-case scenario, shut down your merchant account entirely. For an online business, losing the ability to accept card payments is a death sentence.

This risk also isn't the same everywhere. For instance, Brazil's average chargeback rate is a staggering 3.48%, while the United States sits at a more manageable 0.47%. These regional differences show just how important it is to understand the specific risks in the markets you serve.

Ultimately, managing chargebacks isn’t just about winning individual disputes. It's about protecting your bottom line, your team's time, and your fundamental ability to do business.

Proven Ways Merchants Can Prevent Chargebacks

The best way to win a fight is to avoid it altogether. When it comes to a bank chargeback, this wisdom is golden. Instead of getting tangled in the time-consuming process of disputing claims, the smartest strategy is to prevent them from ever happening.

Proactive prevention protects your revenue, saves you from hefty fees, and keeps your business in good standing with payment processors. It all boils down to building trust and clarity into every step of the customer journey.

From the moment they land on your site to the day their package arrives, clear communication and excellent service are your best defenses. Let's look at some proven, practical ways you can fortify your business against these disputes.

Make Your Customer Service Easy to Find

When customers have a problem, they want a solution—fast. If your contact information is buried five clicks deep on your website, you’re practically inviting them to call their bank instead. Frustration is a major driver of chargebacks.

Make it incredibly simple for customers to reach you. Display your phone number, email address, and a link to a live chat prominently on every page. The goal is to make contacting you the path of least resistance.

Effective customer communication is vital. Some businesses are even exploring solutions like leveraging AI receptionists to prevent customer loss just to make sure they never miss a customer's attempt to connect. A quick, helpful response can turn a potential dispute into a positive customer experience.

Use Clear and Recognizable Billing Descriptors

One of the most common causes of "friendly fraud" is a confusing billing descriptor. Imagine a customer checking their credit card statement and seeing a charge from "XYZ Enterprises Inc." when they bought a product from "Cool Gadget Store." Their immediate reaction is to assume fraud and file a chargeback.

Your billing descriptor should clearly state your business name as your customers know it. Even better, include your website URL or a customer service phone number right in the descriptor. This simple tweak can prevent countless mistaken disputes.

Pro Tip: Your billing descriptor is a tiny but powerful piece of real estate. Work with your payment processor to customize it. Something like "CoolGadgetStore.com 800-555-1234" is far more effective than a generic legal company name.

Set Crystal-Clear Policies

Ambiguity is the enemy of a smooth transaction. Customers need to know exactly what to expect before, during, and after their purchase. Unclear or hidden policies on shipping, returns, and refunds are a recipe for disputes.

Your policies should be written in plain English and be easy to find on your website. Don’t hide them in the fine print.

- Shipping Policy: Provide realistic delivery timeframes and update customers if delays occur. Offer tracking information for every single order.

- Return Policy: Clearly state the conditions for returns, who pays for return shipping, and how long the process takes. An overly strict policy can push customers toward chargebacks.

- Refund Policy: Explain how and when refunds are processed. If a customer knows their refund is on its way, they’re less likely to file a dispute out of impatience.

Use Essential Fraud Prevention Tools

While great customer service helps prevent service-related chargebacks, you also need tools to stop true fraud in its tracks. Most payment gateways offer basic but highly effective fraud prevention features that you should always have enabled.

Two of the most important are:

- Address Verification Service (AVS): This tool checks if the billing address entered by the customer matches the address on file with their credit card company. A mismatch is a major red flag.

- Card Verification Value (CVV): This requires the customer to enter the three- or four-digit security code from their card. Since this code isn't stored in most databases, it helps confirm the person making the purchase has the physical card.

Activating these tools adds a crucial layer of security, making it much harder for criminals to use stolen card information on your site.

To bring these strategies together, here's a quick checklist to help you create a stronger defense against chargebacks.

Chargeback Prevention Checklist for Merchants

By combining transparent practices with smart security, you can build a strong defense that stops most chargebacks before they even begin.

How AI Is Changing the Way We Handle Disputes

For years, handling a bank chargeback felt like a manual, soul-crushing chore for merchants. It meant hours spent digging through records, trying to piece together evidence, and frantically writing responses—all while a strict deadline loomed.

But that old way of doing things is finally getting a much-needed upgrade. AI-powered tools are completely changing the game by automating the entire dispute resolution process from start to finish.

Think of it like having a brilliant, tireless assistant working for you 24/7. This isn't some far-off concept; it's the new reality for thousands of businesses right now. This technology steps in as your personal dispute manager, getting to work the second a chargeback lands in your account.

Automating the Evidence Collection

Instead of you having to drop everything to hunt down order details, the AI instantly analyzes the reason for the chargeback. From there, it automatically pulls together all the evidence needed to build a rock-solid case.

This includes everything from the initial order information and customer emails to shipping receipts and delivery confirmations. If a customer claims a package never showed up, for instance, the AI will have the tracking number and proof of delivery ready in seconds. This completely wipes out the tedious busywork that eats up so much time, letting you get back to actually running your business.

By automating evidence gathering and response generation, AI can improve a merchant's chargeback win rate by as much as 3.5 times. It transforms a reactive, stressful task into a streamlined, hands-off process.

Building a Winning Response

Once it has all the evidence, the AI doesn’t just dump a folder of files on your desk. It intelligently assembles a professional, well-structured rebuttal that is perfectly tailored to the dispute's specific reason code. It knows exactly what banks need to see to overturn a chargeback and reverse the transaction.

This saves an incredible amount of time and significantly boosts your chances of winning back lost revenue. To really see how this works in action, check out our complete guide to automated chargeback and dispute management using AI. With this kind of technology, businesses can finally fight every single illegitimate dispute without getting buried in paperwork.

Got Questions About Bank Chargebacks? We've Got Answers.

Even after you get the hang of the basics, chargebacks can still throw a few curveballs. It's totally normal to have specific questions pop up. We've gathered the most common ones we hear from both customers and merchants to give you quick, no-fluff answers.

How Long Do I Have to File a Chargeback?

This is a big one, and honestly, the answer is "it depends." As a general rule of thumb, cardholders usually have somewhere between 60 to 120 days from the day of the transaction to start a dispute.

But that window can sometimes stretch. Let's say you paid for a service that was scheduled way out in the future, or a product's delivery date came and went. In cases like that, the clock might start ticking later. The specific timelines are set by the card networks (think Visa, Mastercard, etc.) and your bank. The best advice? Act fast. The second you notice an issue, get in touch with your bank to find out their exact deadline.

Is a Chargeback the Same Thing as a Refund?

Nope, they're two completely different animals.

A refund is the friendly route. You talk directly to the merchant, explain the problem, they agree, and they send the money back to your account. It's a simple, direct conversation between you and the business.

A bank chargeback, on the other hand, is a much more formal process. It's what happens when you can't get things sorted out with the merchant, so you ask your bank to step in and forcefully take the money back. This triggers a formal investigation involving both banks and can create real headaches for the business.

Always, always try for a refund first. It’s quicker, easier, and keeps things civil. A chargeback should be your last resort when you've hit a complete dead end with the merchant.

Can a Merchant Just Refuse a Chargeback?

Not really. A merchant can’t just say "no" to a chargeback the way they might deny a refund request. Once you file a chargeback with your bank, the funds are automatically pulled from the merchant's account while things get sorted out.

What they can do is fight it. This is called representment. The merchant gathers up all their evidence—like proof of delivery or signed receipts—to show that the charge was legitimate. If they build a strong enough case, the bank might reverse the chargeback, and the merchant gets their money back.

Will a Chargeback Mess Up My Credit Score?

For you, the cardholder, the answer is almost always no. Filing a legitimate chargeback for a valid reason—like a fraudulent charge or a product that never showed up—won't ding your credit score. It’s a consumer protection feature your bank provides.

But here's the catch: don't abuse the system. If you start filing a bunch of bogus chargebacks (what the industry calls "friendly fraud"), you could run into trouble. Your bank might notice the pattern and decide to close your account, which could have an indirect impact on your credit down the road. It’s a powerful tool, so use it honestly.

Tired of losing revenue to confusing and time-consuming disputes? ChargePay uses AI to automate the entire chargeback process, recovering up to 80% of lost funds for you. See how it works at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)