A chargeback fee is the penalty your payment processor hits you with every single time a customer disputes a transaction. You can think of it as an administrative fee that covers the bank's cost for having to investigate and reverse the sale. It’s a direct punch to your revenue, right on top of losing the money from the original sale.

Understanding The Cost Of Chargeback Fees

So, what actually happens when a customer files a chargeback? It kicks off a formal dispute process that ropes in multiple parties—the customer's bank (the issuer) and your bank (the acquirer). That process isn't free.

To cover the operational costs of all that back-and-forth communication and moving funds around, your payment processor charges you that chargeback fee.

This isn't a fee you can negotiate. It's typically pulled from your merchant account the moment the dispute is filed, long before anyone decides if the claim is even legitimate.

More Than Just a Fee

That initial chargeback fee is really just the tip of the iceberg. Each dispute triggers a domino effect of losses that go way beyond that one penalty. To get the full picture, you have to look at the total cost.

Let's break down the true cost of a single chargeback incident. It's often shocking to see how quickly the expenses add up beyond just the fee itself.

The True Cost of a Single Chargeback

As you can see, a single $50 transaction can easily end up costing your business well over $100 once you factor in the lost sale, the product, and the fee.

These aren't just hypotheticals; they represent a very real and growing expense for merchants. For example, it costs financial institutions an average of $9.08 to $10.32 to handle each dispute, and you can bet that cost is passed down to you. The direct fees you'll pay typically range from $20 to $100 per incident, depending on your processor and risk profile.

To see exactly how this plays out with a major processor, check out our complete guide on the Stripe chargeback fee.

Why Chargebacks Happen and Who Pays the Price

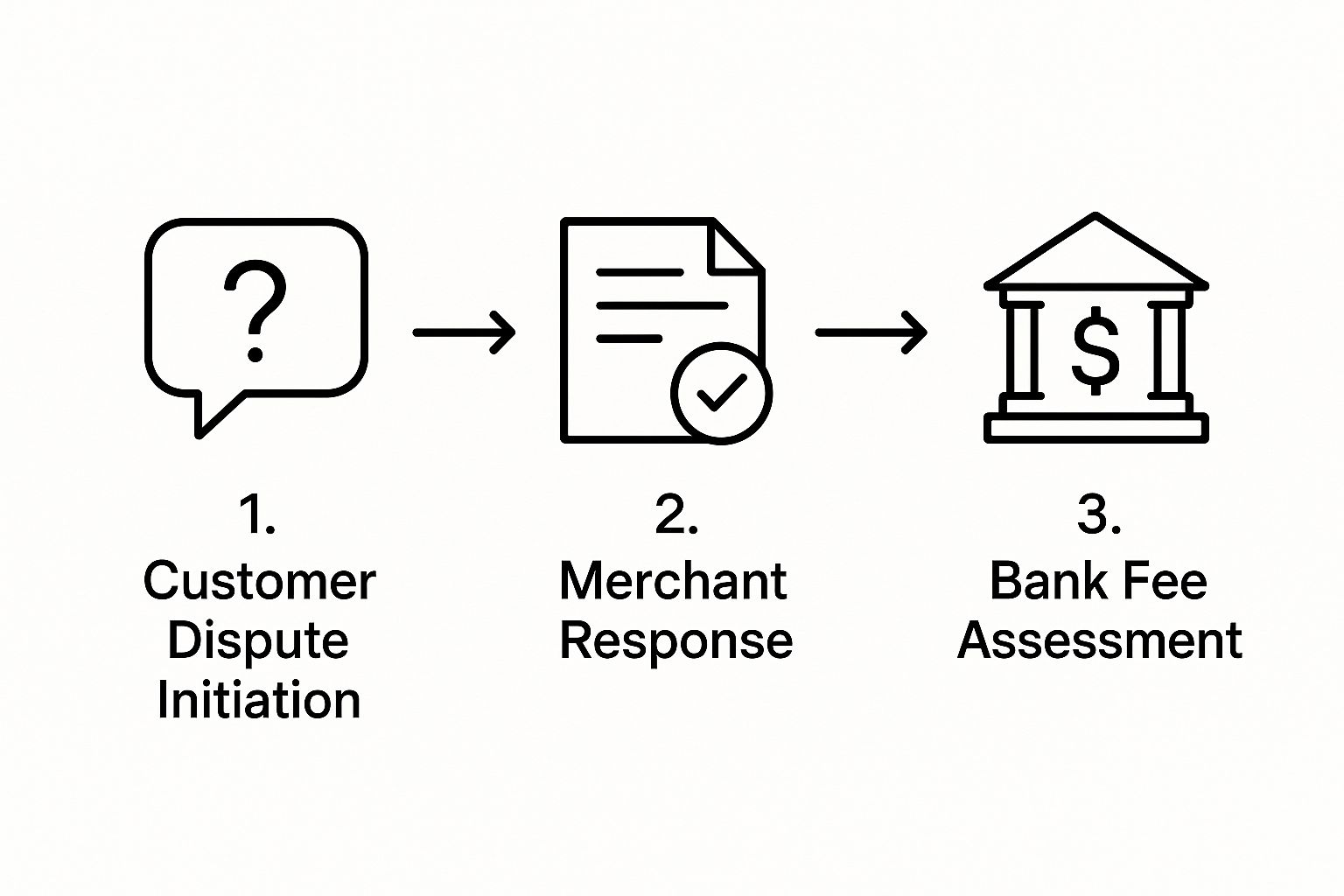

Chargebacks don't just appear out of thin air. They're the direct result of a customer calling their bank to dispute a charge, kicking off a formal process that almost always leaves you, the merchant, holding the bill.

Think of it as a chain reaction. The customer talks to their bank, their bank talks to the card network (like Visa or Mastercard), and the card network talks to your bank. Every step in that chain has administrative costs, which is why your payment processor hits you with a chargeback fee to cover all the back-and-forth.

The whole thing flows from a customer dispute straight to a fee on your end.

As you can see, the process starts with the customer and ends with a cost for you, which is why the financial responsibility ultimately lands on your shoulders.

Common Triggers for Chargebacks

While every dispute has its own story, most chargebacks boil down to a handful of common reasons. Getting a handle on these root causes is your first line of defense.

Some disputes are pretty black-and-white, like when a criminal uses a stolen credit card to make a purchase. Others are just the result of simple merchant errors that could have been avoided.

Here are some of the most frequent culprits:

- Criminal Fraud: A fraudster gets their hands on stolen card details and uses them in your store.

- Product Not Received: The customer swears they never got the item they paid for.

- Not as Described: The product shows up, but it looks nothing like the pictures or description on your site.

- Technical Issues: A glitch in the system leads to a duplicate charge or the wrong billing amount.

- Unrecognized Charge: The customer sees your business name on their statement, doesn't recognize it, and assumes it’s fraud.

Fraud is a massive piece of the puzzle. In fact, about 45% of all chargebacks are tied to some kind of fraudulent activity. That number is split almost evenly between third-party criminals and fraud committed by the actual cardholder. With how easy it is to dispute a charge online these days, this problem has only gotten worse for merchants.

The Rise of Friendly Fraud

Beyond the clear-cut cases of fraud or merchant error, there’s a growing headache known as friendly fraud. This is when a completely legitimate customer buys something, receives it, and then files a chargeback anyway.

Why would they do this? Maybe they forgot about the purchase, didn't recognize your company's name on their bill, or—more often than we'd like to admit—they just want to get something for free. It’s basically cyber shoplifting.

No matter the customer's motive, the result for you is identical: you lose the revenue from the sale, you lose the product, and you get slapped with a chargeback fee.

Because it comes from a real customer using their own card, this type of chargeback is incredibly tough to catch with traditional fraud prevention tools. To get a better grip on this tricky situation, you can learn more about how to spot and fight friendly fraud in our detailed guide.

Calculating the Real Financial Impact on Your Business

That initial chargeback fee you see on your statement? It’s just the tip of the iceberg. While seeing a $20 to $100 penalty stings, the true financial damage goes much, much deeper, sending ripples across your entire business.

Think of it this way: a single chargeback isn't just one deduction. It's a cascade of losses that stack up fast. First, you instantly lose the revenue from the original sale. That’s the most obvious hit to your bottom line.

But it doesn't stop there. You’re also out the wholesale cost of the product you shipped, which is probably gone for good. On top of that, you have to factor in the operational costs—the hours your team spends digging up evidence and fighting the dispute instead of focusing on growing your business.

The Hidden Costs and Long-Term Risks

When you add it all up, the real cost of a single chargeback is often two to three times the original transaction value. This multiplier effect is what makes them so destructive, but believe it or not, the financial pain can get even worse over time.

Card networks like Visa and Mastercard keep a very close watch on how many chargebacks you get compared to your total transactions. This is your chargeback ratio.

If that ratio creeps too high, you risk getting flagged and placed into a high-risk monitoring program. These programs are designed to penalize merchants who generate too many disputes, and the consequences are severe.

You could be slapped with steep monthly fines, hit with significantly higher processing fees on every single transaction, or forced into stricter review processes that delay your access to funds.

In a worst-case scenario, if you can’t get your chargeback ratio under control, your payment processor could terminate your merchant account entirely. That means losing the ability to accept credit card payments—a devastating blow for any business. The fallout from even one dispute goes far beyond a simple fee; it’s a direct threat to your sustainability and growth. To understand this further, read our article exploring how chargebacks hurt businesses.

The Global Scale of the Problem

This isn’t just a headache for individual merchants; it’s a massive drain on the entire eCommerce industry. Projections show that in 2025, chargebacks are set to cost online businesses a staggering $33.79 billion globally.

That number is expected to jump to $41.69 billion by 2028—a nearly 24% increase in just three years. Merchants in North America, particularly the U.S., feel this pain most acutely, shouldering about 10% of the global volume and losing an estimated $4.61 billion to chargebacks alone. You can find more insights on these chargeback statistics and their trends on Chargeflow.io.

How Chargebacks Play Out in the Real World

Numbers and ratios on a spreadsheet are one thing. But seeing how a chargeback fee can drain a real business's bank account makes the impact hit home. Let's walk through a few common scenarios to see how these disputes go from a simple customer complaint to a costly problem for the merchant.

Each story gives a little flavor of the different kinds of chargebacks you might see, from legitimate product issues to the infuriating world of friendly fraud.

Example 1: The Small Ecommerce Store

Let's imagine "Cozy Candles," a small online shop selling handmade candles. A customer orders a $40 candle set. A week later, they file a chargeback, claiming the product was "not as described" because the scent wasn't as strong as they'd hoped.

The second that dispute is filed, the store's payment processor yanks the $40 from their account and tacks on a $25 chargeback fee. Now, the owner of Cozy Candles is on the hook to prove their product description was accurate.

- The Claim: Product not as described.

- The Merchant's Response: They dig up product photos, the original online description, and the customer’s order confirmation to send as evidence.

- The Result: Despite their efforts, the bank sides with the customer. Cozy Candles is out the $40 sale, the $15 it cost to produce and ship the candles in the first place, and the non-refundable $25 fee. That’s a total loss of $80 on a single order.

Example 2: The Subscription Box Service

Now, let's look at "SnackBox," a service that ships curated snacks for $30/month. A long-time subscriber gets their box but files a chargeback, saying they never authorized the recurring payment. This is a classic case of friendly fraud.

Instantly, SnackBox is down $30 from the sale and dinged with a $20 chargeback fee. Their team has to scramble to find the customer's original sign-up agreement.

This kind of thing happens all the time. The customer gets the product and knows perfectly well they signed up, but they use the chargeback system to get a freebie without the hassle of contacting the company or returning the items. It’s a massive headache for any business with a recurring revenue model.

SnackBox submits the digital receipt showing the customer explicitly agreed to the monthly billing terms. Thankfully, the evidence is rock-solid, and they win the dispute. They get the $30 back, but that $20 fee is gone for good. Even winning the fight still costs them money.

Example 3: The Digital Agency

Finally, picture a digital marketing agency that just finished a $1,500 website project. A week after launch, the client files a chargeback for "services not rendered," claiming they were unhappy with the final website.

The agency immediately loses the $1,500 payment and gets hit with a $35 fee. The stakes are way higher here. They have to respond with the signed contract, a trail of emails showing client approvals at every stage, and a link to the live, fully-functioning website they built.

Fortunately, their meticulous record-keeping pays off, and the bank reverses the chargeback. The agency gets its $1,500 back, but just like SnackBox, they're still out the $35 fee. On top of that, they lost several hours of valuable team time that could have been spent on paying client work.

Your Action Plan to Reduce Chargeback Fees

Feeling helpless as chargebacks pile up is one of the most frustrating parts of running a business. But you don't have to just sit back and accept them as a necessary evil. The real secret is shifting from a reactive mindset—dealing with disasters as they happen—to a proactive one.

With the right game plan, you can stop a huge number of disputes before they even get started. This action plan is all about giving you concrete, easy-to-implement strategies to build a stronger defense and protect your hard-earned revenue.

Fortify Your Pre-Transaction Defenses

Let's be honest: the best way to handle a chargeback is to make sure it never happens in the first place. The good news is that most preventative measures are surprisingly simple. It all boils down to clear communication and being transparent with your customers.

Take a moment and walk through your entire checkout process as if you were a customer. Is everything totally clear? Even the smallest bit of confusion can be the seed of a future dispute.

Here are some of the most effective tactics you can put in place today:

Write Crystal-Clear Product Descriptions: Be brutally honest about what you're selling. Use high-quality photos from every angle, and give detailed specs like dimensions and materials. The goal is simple: leave no room for a customer to claim the item was "not as described."

Use a Recognizable Billing Descriptor: What name shows up on your customer's credit card statement? If your business is "Awesome Gadgets Inc." but your billing descriptor is "AGI-WEB," you’re just asking for confused customers to file a chargeback. Make it obvious.

Provide Stellar Customer Service: Make it ridiculously easy for a customer to get in touch with a problem. A visible phone number, email address, or live chat can turn a potential chargeback into a simple refund request. If they can't find you, they'll go straight to their bank.

Master Your Post-Chargeback Response

Even with the best defenses, some chargebacks are simply going to slip through. When a dispute lands on your desk, how quickly and effectively you respond is everything. This is where having your evidence organized and ready to go makes all the difference.

Building a strong representment case is your chance to fight back and reclaim your money. It's not just about winning one dispute; it's about sending a message that you take illegitimate claims seriously. A well-documented response shows the bank you're a diligent and trustworthy merchant.

Your response has to be tailored to the specific reason code for the chargeback. For example, a "product not received" claim requires completely different evidence than a fraud claim.

To build an airtight case, you need to gather compelling evidence, such as:

Proof of Delivery: Always, always use tracked shipping. A delivery confirmation that includes a signature is one of the most powerful weapons you have against "product not received" claims.

Customer Communications: Save everything. That means all emails, chat logs, and support tickets. If a customer was raving about the product a week before filing a dispute, that's a powerful contradiction to their claim.

Order and Transaction Details: Be ready to provide invoices, receipts, and any AVS/CVV verification results from the initial transaction. This helps prove the actual cardholder was involved.

By putting these strategies into practice, you can finally take control of the dispute process. For a deeper look, our guide on how to avoid chargebacks offers even more advanced techniques to protect your business.

Common Questions About Chargeback Fees

Even when you feel like you've got a handle on things, the world of chargebacks can still throw you a curveball. It’s totally normal to have questions about the little details, especially when it comes to how these fees actually hit your bottom line.

To clear the air, we've broken down some of the most common questions we hear from merchants. Nailing these fundamentals is the first step to managing disputes like a pro and protecting your business.

Can I Get a Chargeback Fee Refunded if I Win the Dispute?

This is easily one of the most common—and frustrating—questions merchants ask. The short answer? Almost never. Even when you build a rock-solid case, fight back, and win the dispute, that initial chargeback fee is typically non-refundable.

Think of the fee less like a penalty and more like an administrative cost. Your payment processor charges it to cover the time and resources they spent managing the entire dispute process. Whether you win or lose, they still had to put in the work.

That said, there are always exceptions. Some merchant agreements might have a clause about this, so it never hurts to check your contract or just ask your processor directly. Don't assume it's a lost cause without confirming their specific policy.

What Is a Chargeback Ratio and Why Is It Important?

Your chargeback ratio is one of the most vital signs of your business's health, at least from the perspective of card networks like Visa and Mastercard. The math is simple: it’s the number of chargebacks you get in a given month divided by your total transactions for that same month.

So, if you processed 1,000 transactions and got hit with 10 chargebacks, your ratio is 1%.

This number is a huge deal because it's the primary way card networks decide how risky you are to work with. If your ratio starts creeping above their threshold—which is often around 0.9%—you’re in danger of being flagged as a "high-risk" merchant.

Once you land in a high-risk monitoring program, a whole mess of problems follows. We're talking steep monthly fines, significantly higher processing fees on every single sale, and in the worst-case scenario, having your merchant account shut down completely.

What Is the Difference Between a Chargeback and a Refund?

Both end with the customer getting their money back, but for you, the merchant, they are worlds apart. The real difference comes down to who’s involved and how the whole thing gets started.

A refund is a simple, direct conversation between you and your customer. They contact you, you agree to return the funds, and everyone moves on. It's a normal part of business and doesn't come with any surprise penalties or fees.

A chargeback, on the other hand, is a forced reversal that happens behind your back. The customer skips talking to you and goes straight to their bank to dispute the charge. This kicks off a formal, complicated process involving multiple banks and the card networks. To get the full picture, check out our deep dive on the differences between a chargeback vs refund.

By its very nature, a chargeback is an adversarial process. You don't just lose the sale—you also get slammed with that non-refundable chargeback fee, and the dispute dings your all-important chargeback ratio. It’s a triple threat to your business.

Tired of watching chargeback fees eat into your profits? ChargePay uses AI to automate the entire dispute process, helping you recover up to 80% of lost revenue without lifting a finger. See how our hands-free solution can boost your win rates and protect your bottom line at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)