First-party fraud is one of those frustrating problems that can sneak up on you. It’s when a legitimate customer—someone who willingly bought from you—turns around and disputes the charge, claiming it was unauthorized, the item never showed up, or it wasn't what they ordered.

The real kicker? They’re being dishonest to get their money back while often keeping the product. Because the person committing the fraud is your actual customer, it’s a uniquely tricky situation. They aren't some anonymous hacker using stolen card details.

Understanding This Insider Threat

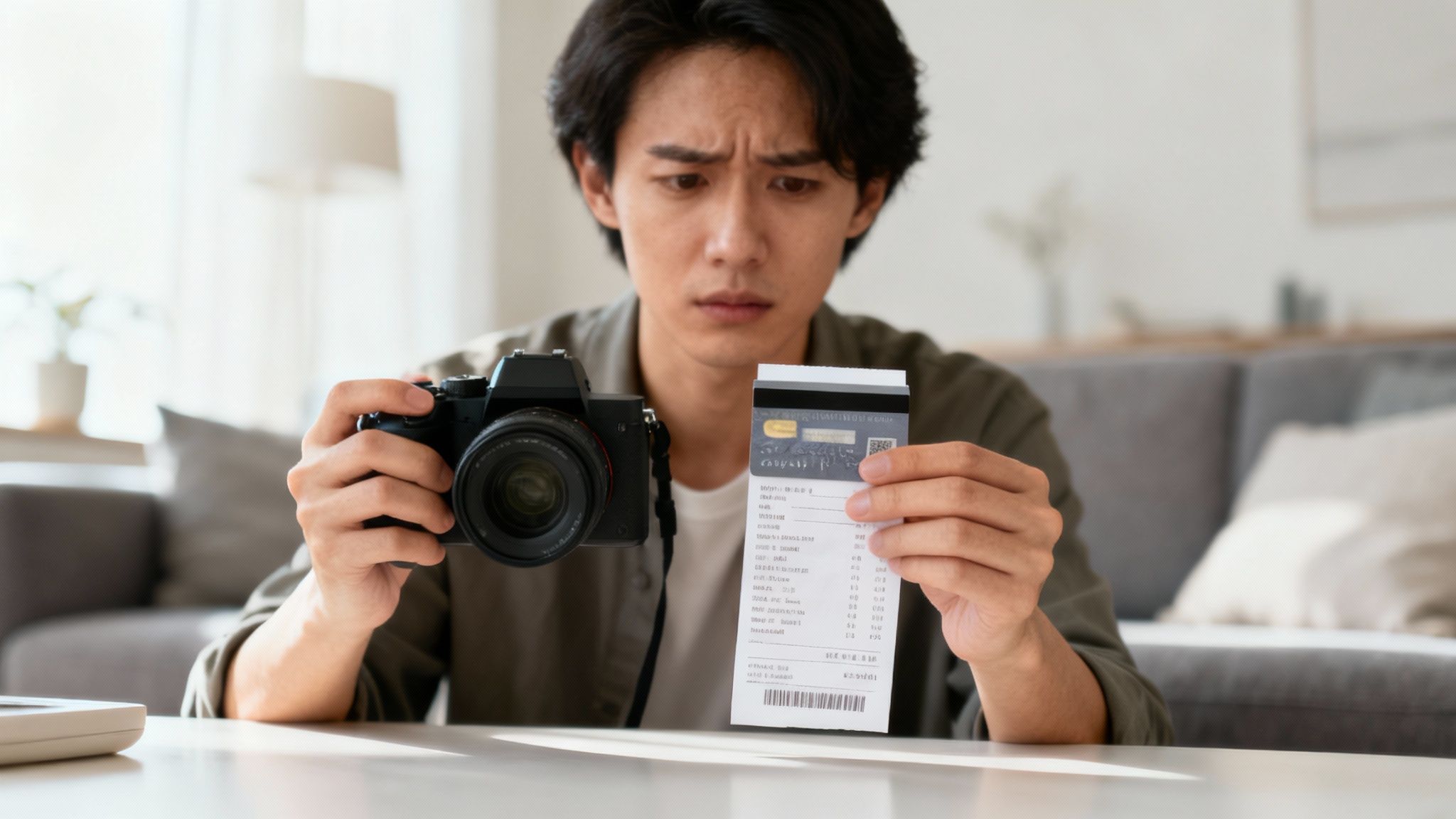

Here’s a classic example: someone buys a brand-new camera right before their big vacation. They use it, take all their photos, and then call their bank to claim the charge was fraudulent. The bank reverses the payment, and you’re forced to issue a refund. The customer gets their money back and keeps the camera. That’s first-party fraud in a nutshell.

This isn’t just a rare annoyance; it’s exploding into a major global problem. According to a recent cybercrime report, first-party fraud now accounts for a staggering 36% of all reported fraud attacks worldwide in 2024. That's a huge jump from just 15% the year before. You can dig into the numbers yourself in the full LexisNexis® Risk Solutions report.

How It Differs From Other Fraud

The biggest difference comes down to who’s behind the keyboard. In traditional fraud, a criminal uses stolen credentials to make a purchase. With first-party fraud, the legitimate cardholder is the one making the false claim. This makes it incredibly tough for standard security checks to catch.

Because the transaction is made by the actual customer, everything looks legitimate on the surface. Their name, address, and payment details all check out, so they fly right past the initial verification steps. The whole thing just looks like a normal customer service issue at first glance.

This type of fraud often gets labeled "friendly fraud," but there's nothing friendly about its impact on your business. It's a direct hit to your revenue and creates serious operational headaches. It also overlaps heavily with what’s known as chargeback fraud. To see how these concepts are linked, check out our guide on what is chargeback fraud and how it affects merchants like you.

First Party Fraud vs Third Party Fraud

To really see the difference, it helps to put them side-by-side. One is an attack from the inside, while the other is a classic external threat.

Ultimately, third-party fraud is about stolen identity, while first-party fraud is about a legitimate identity being used for a dishonest purpose.

The True Cost of First-Party Fraud

When you get hit with first-party fraud, the damage goes way beyond the price tag of the item you sold. Losing the product is just the tip of the iceberg; the real financial gut punch comes from a wave of hidden costs that quietly drain your profits.

Each fraudulent dispute kicks off a chain reaction of expenses that many merchants don't even see coming.

For starters, you’re on the hook for non-refundable chargeback and payment processing fees for the original transaction. You’ve basically paid to get ripped off. Get enough of these, and your payment processor might start seeing you as a "high-risk" merchant, slapping you with permanently higher fees on all future sales.

More Than Just a Refund

Beyond the direct fees, there's the massive operational headache. Your team has to sink precious time and resources into gathering evidence, writing rebuttals, and managing the whole dispute circus. We’re talking hours that could have been spent growing the business, now wasted on a manual, often frustrating, process with no guarantee of a win.

To make matters worse, these losses are often miscategorized in the books, making the problem nearly impossible to track.

Many businesses just write these incidents off as 'bad debt' or chalk them up to 'customer service issues.' But that masks the truth: this is intentional fraud, and mislabeling it hides a serious threat to your business’s financial health.

The cumulative impact is staggering. In the United States alone, first-party fraud is estimated to cost merchants and financial institutions more than $100 billion every year. It's a massive, underreported drain on the economy. You can dig into more data on the staggering scale of this fraud on seon.io.

Getting a handle on these compounding costs is the first step. You start to see that fighting chargebacks isn't just about winning individual disputes—it’s about protecting your entire business model from the ground up. Learning how much chargebacks truly hurt businesses paints a clearer picture of why getting ahead of this problem is so critical.

Recognizing Common First Party Fraud Schemes

To stop first-party fraud, you first have to know what you’re looking for. This isn't some single, sophisticated hack; it's a collection of different schemes, all designed to exploit standard return and refund policies for a customer's personal gain. Once you understand the common tactics, you can start spotting the red flags.

Think of these schemes as the digital version of common retail scams. They just happen to thrive in the anonymous, fast-paced world of e-commerce, where it’s a lot harder to verify a customer's story.

Common Tactics You Might See

Here are a few of the most prevalent schemes that might already be hitting your bottom line:

- Chargeback Fraud: This is the most direct form of first-party fraud, often called "friendly fraud." A customer makes a legitimate purchase with their own card, receives the item, and then files a chargeback with their bank. They’ll falsely claim the transaction was unauthorized or they never got the product.

- "Item Not Received" Claims: Sometimes called "digital shoplifting," this happens when a customer receives their order but tells you it never arrived. Without solid proof of delivery, many merchants feel cornered into issuing a refund or sending a replacement, letting the fraudster keep the original item for free.

- Return Fraud & Wardrobing: This is a classic retail trick brought online. "Wardrobing" is when someone buys an item—usually clothing, jewelry, or an accessory—for a one-time use and then returns it for a full refund. This tactic is especially common after major events or holidays.

When dealing with something like return fraud, it's worth remembering that some people will go to great lengths to make their claim look legitimate. They might even use online tools like generic point-of-sale receipt templates to create convincing fake evidence.

To help merchants visualize the most common schemes customers use, we've put together a quick summary table.

Types of First Party Fraud Schemes

These schemes aren't just minor annoyances; they have a real, compounding financial impact.

The infographic below breaks down how the costs of these schemes snowball far beyond the initial price of the product.

As the visual shows, for every fraudulent claim, you don't just lose the product's value. You also absorb processing fees, risk higher future fees from your payment processor, and waste valuable team time investigating the claim. Getting familiar with the different forms of these chargeback scams is the first, most critical step in building a strong defense.

Why This Fraud Is So Hard to Catch

So, what makes first-party fraud such a nightmare for merchants? It all comes down to a simple, frustrating fact: the person committing the fraud looks exactly like your best customer.

Unlike obvious fraud involving stolen cards or hacked accounts, these transactions don't set off any alarm bells. The fraudster uses their real name, their actual shipping address, and their own credit card. From a security perspective, everything checks out. They sail right through the initial fraud filters because, on paper, they are a legitimate customer making a perfectly normal purchase.

The Problem of Proving Intent

The real challenge isn’t spotting a suspicious transaction in the moment; it’s proving a customer's dishonest intent after the damage is done. Their purchase history might be completely clean, with no prior issues, which makes their claim of a problem seem like an unfortunate, one-off event rather than a calculated scam.

This throws merchants into a frustrating "he said, she said" scenario. You’re convinced a customer is lying, but they stand by their story that the package never arrived or the charge wasn't theirs. Without rock-solid proof, it's your word against theirs.

First-party fraud is particularly difficult to detect and prevent because it involves individuals who, on the surface, are legitimate customers with established relationships to the business. Unlike other forms of fraud—such as identity theft or account takeover—first-party fraudsters use their own real identities and often have a history of normal transactions, making their fraudulent activities blend in with regular customer behavior. Discover more insights on how to tackle first-party fraud without overwhelming your fraud team on sardine.ai.

Standard fraud prevention tools are built to catch external threats, not abuse coming from inside your own customer base. For example, even advanced security measures have their limits here. You can learn more about what 3-D Secure authentication is and see how it’s great at verifying the cardholder's identity, but it can't stop that same cardholder from filing a false claim later. This is exactly why so many businesses feel completely powerless against this type of fraud.

Actionable Strategies to Prevent First-Party Fraud

Alright, we've talked about what first-party fraud is. Now, let’s shift gears and focus on how to stop it. Building a solid defense starts with using your own data to spot sketchy behavior before it drains your bank account.

Take a look at your customer histories. You can often find patterns that signal a higher risk. Keep an eye out for accounts with a crazy number of returns or multiple disputes fired off in a short time. These aren't smoking guns, but they are definitely red flags that tell you to look closer.

Strengthen Your Procedural Defenses

Beyond digging into data, simple tweaks to your day-to-day processes can make a huge difference. The goal is to create a crystal-clear paper trail that makes it nearly impossible for a customer to win a false claim. You want undeniable proof from the second they click "buy."

Here are a few foundational improvements you can make right away:

- Improve Order Confirmation: Don't just send a basic "thanks for your order" email. Get detailed. Include the specific items, total cost, and both billing and shipping addresses. This creates an immediate record that the customer saw and acknowledged the purchase.

- Mandate Delivery Confirmation: This is non-negotiable, especially for high-value items. Always ship with a method that provides tracking and, ideally, requires a signature on delivery. It’s your single best defense against bogus "I never got it" claims.

- Clarify Return Policies: Make your return and refund policies impossible to misinterpret. Plaster them on your checkout page and give them a dedicated spot on your site. This shuts down any "I was confused" arguments before they start.

The most effective prevention combines procedural rigor with clear communication. When customers know you have thorough records and firm, fair policies, it often deters opportunistic fraud before it's even attempted.

A big piece of this puzzle involves setting up effective cyber security measures for your business. A secure system doesn't just protect customer data; it adds another layer of integrity to every transaction, which can be a lifesaver when you're investigating a dispute.

Automate and Escalate Smartly

Let's be real—if you're dealing with a growing number of disputes, trying to track every single order by hand is a recipe for burnout. This is where automation tools come into play.

An automated system can be set up to flag high-risk orders based on rules you define. Think things like a mismatch between the IP address location and the shipping address, or an unusually massive first-time order. This lets your team zero in on the orders that actually need a human eye before they’re shipped out the door.

If you're ready to build a truly robust defense, check out our complete guide on chargeback fraud prevention strategies. Putting these steps into action will help you hang on to your revenue and cut down on the headaches that come with fighting dishonest claims.

Got Questions About First-Party Fraud? We’ve Got Answers.

Let's wrap things up by tackling some of the most common questions business owners have about this tricky topic. Getting clear, straightforward answers can give you the confidence to start identifying and fighting first-party fraud.

Is First-Party Fraud the Same as Friendly Fraud?

Yes, for the most part. The terms are often used interchangeably in the industry to describe the same core problem: a legitimate cardholder disputing a legitimate charge.

"Friendly fraud" is just a more common nickname for first-party fraud, especially when it ends in a chargeback. It’s called "friendly" because the claim comes from what looks like a normal, happy customer—not some shadowy hacker. But don't let the name fool you. The customer's intent is dishonest, and the financial hit to your business is very real.

Can Small Businesses Realistically Fight This?

Absolutely. You don't need a massive fraud department to protect your revenue. Your most powerful weapon is simply meticulous record-keeping.

Fighting fraudulent chargebacks isn't about being confrontational. It’s about protecting the business you've worked so hard to build. Good customers get it, and clear evidence stops the bad ones in their tracks.

Always use delivery confirmation with tracking numbers. Save every bit of customer communication, especially emails and chat logs. And make sure your return and refund policies are crystal clear and easy to find on your website. When a chargeback hits, respond immediately with every piece of evidence you have. More often than not, solid proof that you delivered on your promise is all it takes for the bank to side with you.

How Can I Tell a Real Customer Issue from Fraud?

This is the toughest part, but it usually boils down to patterns versus one-off problems. A genuine customer issue is typically a single, isolated event. That customer is almost always willing to talk to you directly to find a solution because all they want is their problem fixed.

Fraud, on the other hand, often leaves a trail of red flags. Here are a few things to watch for:

- Repeat Offenders: Have you seen multiple chargebacks or a wave of refund requests from the same person, email, or address? That’s a huge warning sign.

- Suspicious Return Rates: An account with a crazy-high return rate compared to your average customer is worth a closer look.

- Radio Silence: Fraudsters often go straight to their bank without ever trying to contact you. A legitimate customer with a real problem will almost always reach out to you first.

Digging into a customer's history and behavior is your best bet for telling them apart. A single hiccup is probably just that—a hiccup. A pattern of problems? That’s likely something more deliberate.

Will Fighting Chargebacks Upset My Good Customers?

Not at all. In fact, fighting fraudulent chargebacks shows that you run a serious, professional business—something your good customers will respect. The goal isn't to create friction or make things difficult; it's to protect your business from being exploited.

The best approach is a clear, fair, and consistently enforced policy on returns and disputes. Genuine customers with legitimate issues will appreciate the straightforward communication and process. Meanwhile, anyone trying to commit fraud will be quickly deterred when they realize you're prepared to defend every sale with solid evidence.

Ready to stop losing revenue to dishonest disputes? ChargePay uses AI to automate the entire chargeback process, generating winning responses to reclaim your money without you lifting a finger. Learn how you can recover up to 80% of lost funds and protect your business today.

.svg)

.svg)

.svg)

.svg)