Think of transaction monitoring as your store's digital security guard. It's an automated system that acts as your watchdog, constantly observing every single sale your business makes and flagging anything that looks out of the ordinary. This process helps you spot potential fraud or other risks without having to manually sift through every order yourself.

What Is Transaction Monitoring

Imagine a small-town shopkeeper who knows every regular customer by name. If a stranger suddenly walked in and tried to make an unusually large cash purchase, the shopkeeper would instantly know something felt off. That's exactly what transaction monitoring does for your online business, just on a massive scale and at lightning speed.

It’s the ongoing process of analyzing financial transactions in real-time to catch suspicious activity. This isn't just a good idea—it's essential for complying with Anti-Money Laundering (AML) regulations and stopping financial crime before it hurts your bottom line. According to a report from Mordor Intelligence, the market for these systems is growing fast for a reason.

The Core Purpose of Monitoring

At its heart, transaction monitoring is all about pattern recognition. The system first learns what "normal" looks like for your customers and your business. Once it establishes that baseline, it can instantly flag anything that deviates from it.

For example, a system can automatically raise an alert if it detects:

- A long-time customer suddenly placing an order that's 10x larger than their average purchase.

- Someone trying multiple failed payment attempts before a successful one with a completely different card.

- An order coming from a high-risk country that you almost never ship to.

This proactive approach fundamentally changes how you handle fraud. Instead of reacting after the damage is done, you start stopping it in its tracks. It's a critical shift from damage control to active prevention.

Before you can choose the right tool, you need to understand the goals. Here’s a quick breakdown of what a good monitoring system should accomplish for you.

Key Goals of Transaction Monitoring

A quick summary of the main objectives of putting a transaction monitoring system in place.

Ultimately, having a solid monitoring system in place is about protecting your business from every angle—financially, legally, and reputationally.

Understanding these basics is the first step. By spotting these red flags in real time, you can protect your revenue, maintain customer trust, and stay on the right side of financial regulations.

How Transaction Monitoring Actually Works

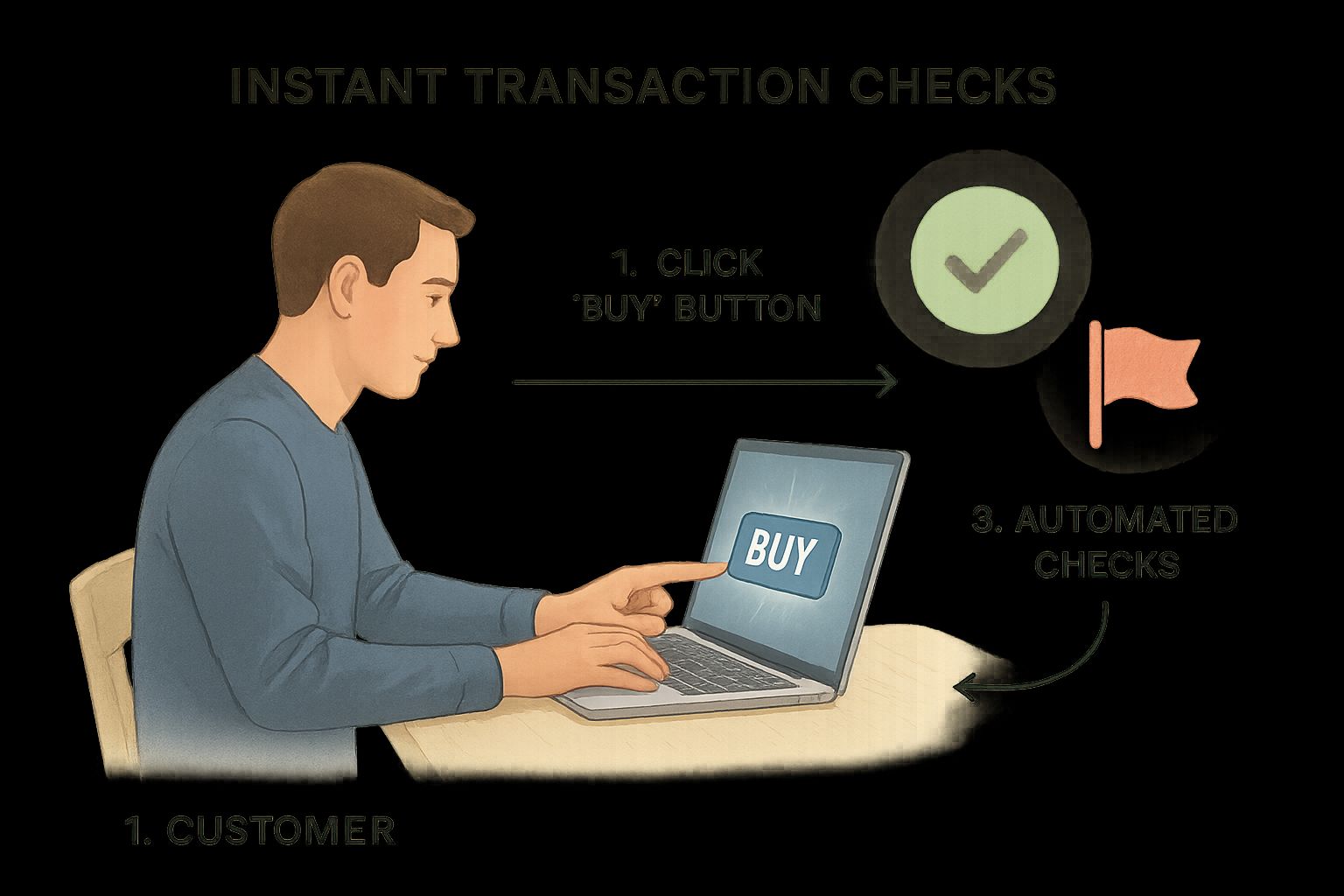

Let's walk through what happens behind the scenes during a single online purchase. The moment a customer clicks 'buy,' a whole series of automated checks kicks off, and it all happens in the blink of an eye. This isn't some slow, manual review; it's a high-speed analysis designed to protect your business without slowing it down.

The system immediately starts gathering dozens of data points. We’re talking about information on the order itself (like the purchase amount and what’s in the cart), the customer's history with your store (are they brand new or a loyal regular?), and even technical details like their IP address and the device they're using. It’s like a detective instantly collecting all the clues related to the case.

This visual shows how automated checks instantly flag or approve a transaction the moment a customer makes a purchase.

From there, the system makes a split-second decision by comparing this data against established rules and patterns to keep your business safe.

Comparing Data Against Rules

Once all that data is collected, the monitoring system checks it against a set of rules you've already defined. Think of these as your business's custom security guards—the "if-then" conditions that automatically flag anything that looks out of the ordinary.

You can set up all sorts of custom rules. Here are a few common ones:

- Transaction Value: Flag any purchase over $2,000 for a human to look over.

- Velocity Checks: Send an alert if more than three orders come from the same IP address within an hour.

- Geolocation Mismatches: Question an order where the shipping address is in New York, but the IP address is pinging from halfway across the world.

If a transaction breaks one of these rules, it gets an immediate red flag. This entire process is also heavily guided by global regulations, especially Anti-Money Laundering (AML) mandates that require businesses to spot and report suspicious activity almost instantly. This proactive approach is the backbone of many modern chargeback management tools that aim to stop disputes before they can even start.

A transaction might get flagged not for one big reason, but for a combination of small, unusual factors. For example, a small purchase from a new customer is usually fine. But if it's also from a high-risk location at 3 AM using a brand-new email, the system's suspicion level goes way up. It's this multi-layered analysis that makes modern monitoring so powerful.

The Building Blocks of a Strong Monitoring System

An effective transaction monitoring system isn’t just one piece of software. It’s a combination of different parts all working in sync. Think of it like building a fortress; you need strong walls, watchful towers, and a quick way to send signals to be truly secure. Each component plays its own unique role in protecting your business from threats.

When you understand what these building blocks are, you can more easily spot what makes a system genuinely powerful versus one that just looks good on paper. And it all starts with your data.

Customer Data and Rule Engines

The foundation of any good monitoring system is clean, organized customer data. Without a solid understanding of who your customers are and how they normally shop, your system is flying blind. This data is what provides the context to separate a perfectly normal purchase from a highly suspicious one.

From there, transaction rules come in as your first line of defense. These are the simple "if-then" conditions we talked about earlier. For instance, a rule might automatically flag any order where the billing and shipping addresses are in different countries. A core part of this is having a robust logging and monitoring policy to ensure everything is tracked consistently.

These rules aren't just about blocking bad guys; they're about creating a smarter workflow. Good rules catch the obvious threats, which frees up your team's time to investigate the trickier cases that need a human touch.

Risk Scoring and Smart Alerts

While rules are great for clear-cut cases, many transactions fall into a gray area. That’s where risk scoring comes into play. Instead of a simple pass/fail, the system gives each transaction a score based on a mix of risk factors—things like location, the value of the order, and the customer’s purchase history.

A high score doesn't automatically mean it's fraud, but it’s a big red flag that says, "Hey, this one needs a closer look."

This leads to the final, crucial piece: a smart alert system. A great system won't just flood your team with notifications for every little thing. Instead, it prioritizes alerts based on the risk score, making sure your team tackles the most urgent threats first. This kind of efficiency is a key part of modern e-commerce fraud prevention.

By combining these elements—good data, clear rules, intelligent scoring, and prioritized alerts—you create a layered defense that's both powerful and practical.

Why Your Business Can't Afford to Ignore It

So, beyond the technical jargon, what does transaction monitoring actually do for your business? To put it simply, it's a non-negotiable part of running a healthy, sustainable e-commerce store today. Ignoring it is like leaving your front door wide open—you're exposed to a world of financial and legal risks that can stop your growth in its tracks.

The most immediate win is fraud prevention. Every single fraudulent transaction you stop is revenue that stays in your pocket. This directly cuts down on the number of expensive chargebacks you have to deal with, saving you a ton of money and headaches. For any merchant who understands just how much chargebacks hurt businesses, this benefit alone is a huge motivator.

Staying Compliant and Building Trust

But it's not just about stopping fraudsters. Solid transaction monitoring is also a cornerstone of regulatory compliance. Financial authorities expect businesses to have systems in place to spot and report sketchy activities like money laundering. Dropping the ball here can lead to massive fines and serious legal trouble. Think of it as a key piece of your overall business compliance requirements.

But here’s the benefit most people overlook: customer trust. When customers feel confident that their payment info is safe, they're far more likely to click "buy" and come back for more. A secure checkout isn't just a feature; it's a powerful signal that you take their safety seriously.

The market reflects this growing importance. The U.S. transaction monitoring market hit a value of about USD 17.14 billion in 2024 and is on track to jump to nearly USD 20 billion by 2025. This explosion is fueled by the boom in e-commerce, proving just how essential this has become. You can discover more insights about this market growth on GlobeNewswire.

How AI Is Making Transaction Monitoring Smarter

Traditional transaction monitoring systems are a bit like a security guard with a very specific checklist. They’re great at spotting the obvious rule-breakers—like an order that hits a hard limit of $1,000—but savvy fraudsters quickly learn how to stay just under the radar. They know the rules and are experts at bending them without breaking them.

This is exactly where Artificial Intelligence (AI) and machine learning are changing the game. Instead of just following a static set of instructions, AI-powered systems actually learn, adapt, and evolve over time. They don't just check boxes; they look for the story behind the data.

Beyond Simple Rules

Think of it as upgrading from that security guard to a seasoned detective. An AI system can analyze thousands of data points in real time to connect seemingly unrelated dots. It might spot a subtle network of small, "normal-looking" transactions that are actually part of a much larger, coordinated fraud ring.

This is a huge leap forward. An AI can identify a brand-new fraud tactic after seeing it just once, then automatically update its defenses to block it from happening again. This self-learning ability means your protection gets smarter with every single transaction it analyzes.

AI doesn't get stuck on individual red flags. It looks at the bigger picture, analyzing a customer's entire journey and behavior to understand the intent behind a transaction, not just the numbers. This context is what separates a legitimate shopper from a fraudster.

The Real-World Impact of Smarter Monitoring

So, what does this actually mean for your business? The benefits are direct and powerful. AI-driven monitoring leads to far more accurate fraud detection.

- Fewer False Positives: AI is much better at telling the difference between a genuinely risky order and a good customer making an unusual purchase. This means fewer legitimate orders get blocked, protecting your revenue and keeping your customers happy.

- Reduced Manual Work: Because the system is more accurate, your team spends way less time manually reviewing flagged orders. This frees them up to focus on growing the business instead of chasing down alerts.

Ultimately, using AI technology to catch chargeback fraud gives you a more dynamic and intelligent defense—one that stays a step ahead of criminals.

Traditional Rules vs AI-Powered Monitoring

The shift from old-school, rule-based systems to modern AI isn't just a small upgrade; it's a fundamental change in how we approach security. The table below breaks down the key differences.

As you can see, AI-powered systems offer a proactive, intelligent defense that static rules simply can't match. They don't just follow orders; they think, learn, and protect your business more effectively.

Ready to give transaction monitoring a real shot? The good news is, you don’t need a computer science degree to get started. By breaking it down into a few common-sense steps, you can build a solid defense for your business without getting bogged down in the details. The whole point is to create a simple, effective plan you can actually start using today.

It all begins with a hard look at your own vulnerabilities. Once you know where the weak spots are, you can pick the right tools for the job and set them up to work for your specific business.

Step 1: Know Your Enemy (And Your Business)

Before you can fight fraud, you have to know what it looks like for your business. Are you getting hit with lots of small, rapid-fire transactions from stolen cards? Or are the bigger threats single, high-ticket purchases from hijacked accounts? The best way to find out is to dig into your past chargebacks and fraud incidents. Look for the patterns.

This first step is non-negotiable. It gives you a clear picture of what you’re up against, which means you can pick a system that targets your actual problems instead of wasting money on a generic, one-size-fits-all solution.

Step 2: Explore Your Toolkit

Once you know what you’re looking for, it’s time to see what tools are out there. Your options usually fall into a couple of main camps:

- Built-in Tools: Most payment processors like Shopify or Stripe offer some basic monitoring features right out of the box. For new businesses, these are a fantastic starting point.

- Specialized Software: If you need more firepower, dedicated platforms offer much more sophisticated rule engines and AI-powered analysis that can spot threats the basic tools might miss.

The right choice really comes down to your business's size and risk level. Start with what your payment processor gives you. If you find yourself drowning in manual reviews, that’s a clear sign you’re ready to upgrade to a more specialized solution.

Step 3: Set Up Smart Rules and Alerts

Finally, it's time to put your system to work by setting up rules that actually make sense for your store. Don't just grab a generic list from the internet. Use that risk profile you built in the first step to guide you. For example, if you sell high-value electronics, it’s a no-brainer to set a threshold that flags unusually large orders for a quick manual review.

Start with just a few simple, targeted rules. As your system collects more data, you can tweak them and even add more complex ones. The key is to create an alert system that is helpful, not noisy. You want it to flag only the transactions that genuinely need a second look.

Frequently Asked Questions

Even after getting the hang of transaction monitoring, a few questions always seem to pop up about how it fits into the daily grind. Let's tackle some of the most common ones we hear from business owners.

Is Transaction Monitoring Just for Big Banks?

Not anymore. It's true that big financial institutions have been using it for years to keep up with heavy regulations, but transaction monitoring is now a must-have for e-commerce businesses of all sizes.

With online fraud on the rise, any business that takes digital payments needs a solid way to protect both itself and its customers from risk. Think of it as essential security, not just a big-bank luxury.

What's the Difference Between Synthetic and Transaction Monitoring?

This is a great question, and it's easy to get them mixed up. They both play important roles, but they do very different jobs.

Synthetic Monitoring is all about being proactive. You're basically running drills on your own website, using scripts to pretend to be a user—logging in, adding an item to a cart, and so on. The goal is to catch performance hiccups before a real customer does. It answers the question: "Is my site working the way it's supposed to?"

Transaction Monitoring is about real-time security. It watches actual customer purchases as they happen to spot and shut down fraud or other fishy activity. It answers a different question: "Is this specific purchase legit and safe?"

To put it simply, synthetic monitoring is like a health checkup for your systems, while transaction monitoring is the security guard watching the door.

How Much Manual Work Is Involved?

Honestly, that depends entirely on the system you're using. Older, rule-based systems can be a real headache. They often spit out tons of false positives—flagging perfectly good orders as suspicious—which can leave your team buried in manual review work.

But modern AI-powered systems are a different story. They're much smarter, learning the unique quirks and patterns of your business to make far more accurate calls. This slashes the time you spend chasing down false alarms, freeing up your team to focus on growing the business.

Ready to stop losing revenue to chargebacks and fraud? ChargePay uses AI to automate the entire dispute process, recovering up to 80% of your lost funds without any manual work from your team. See how much you can reclaim at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)