AVS, or Address Verification Service, is a simple but surprisingly powerful security check that works its magic in just a few seconds during an online sale. Its main job? To make sure the billing address a customer types in matches the one their credit card company has on file. Think of it as your first line of defense against would-be fraudsters.

What Is AVS and Why Does It Matter for Your Store?

Imagine AVS as a quick ID check at your digital checkout counter. When a customer enters their card details, your payment system doesn't just look at the available funds. It also pings the customer's bank with a simple question: "Hey, does the address they just gave me match what you have?"

This check is hyper-focused on the numeric parts of the address—specifically the street number and the ZIP code. It’s not trying to figure out if a house actually exists or if the street name is spelled right. It's a straightforward, automated numbers game built to sniff out a very common type of fraud.

A Simple But Powerful Fraud Filter

Let’s say a thief gets their hands on a stolen credit card number, expiration date, and CVV code. More often than not, they won't have the cardholder's exact billing address. When they try to buy something from your store and punch in a fake address or their own, the AVS check is likely to come back with a mismatch. This failure immediately raises a red flag, giving you the chance to block a shady transaction before it turns into a painful chargeback.

This one simple step adds a crucial layer of security by:

- Verifying the Buyer: It helps confirm that the person making the purchase is much more likely to be the legitimate owner of the card.

- Reducing Chargebacks: By catching fraudulent orders before they’re even processed, you cut down on the "unauthorized transaction" disputes you'll have to fight later.

- Protecting Your Revenue: Fewer chargebacks mean more of your hard-earned cash stays right where it belongs—in your account.

An AVS check is basically an automated bouncer for your online store. It quickly checks if a customer's 'credentials' (their billing address) line up with the 'guest list' (the bank's records), helping to keep troublemakers out.

Let's break it down even further.

AVS at a Glance

AVS is all about a quick, automated comparison. It's not a foolproof system, but it's an incredibly effective first filter. Here's a quick summary of what it does and doesn't do.

Ultimately, AVS provides a strong signal—either "things look good" or "you might want to take a closer look"—without slowing down the checkout experience for your legitimate customers.

The Growing Importance of Verification

The need for tools like AVS is exploding as e-commerce keeps growing. The Address Verification Software (AVS) market was valued at a massive US$11.86 billion in a recent year, and experts predict it will climb at a compound annual growth rate (CAGR) of 11.75% in the years ahead. This boom is fueled by online merchants like you who are getting serious about stopping fraudulent chargebacks.

In today's online world, using systems like AVS is just as important as the other essential e-commerce website components. By adding this simple verification step, you’re not just protecting your bottom line; you’re building a safer, more trustworthy place for your real customers to shop. For a deeper look at protecting your store, check out our guide on comprehensive e-commerce fraud prevention strategies.

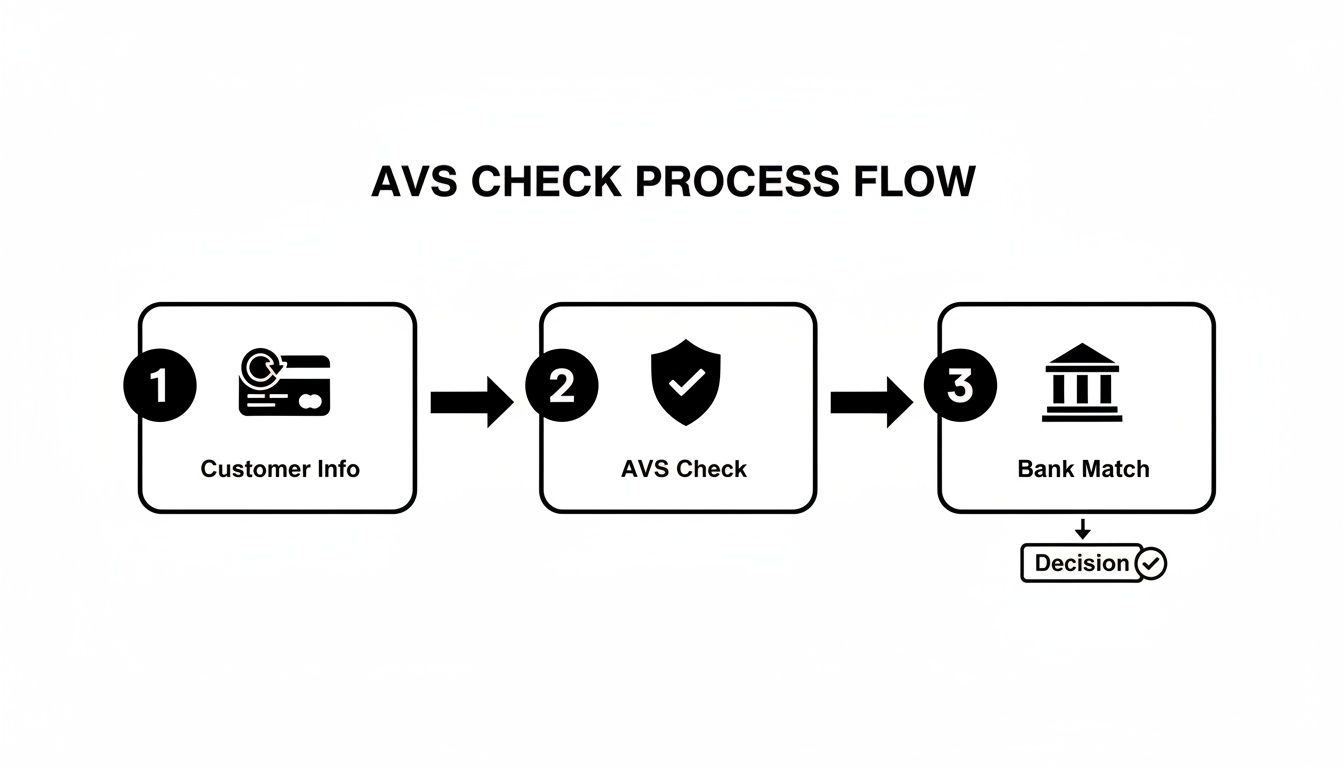

How an AVS Check Works During a Transaction

Ever wonder what happens in those few seconds after a customer hits ‘Pay Now’? It’s a lightning-fast, invisible conversation between your store, your payment processor, and the customer’s bank. The Address Verification Service (AVS) plays a starring role in this quick security handshake.

Think of AVS as an automated game of matching numbers. When a customer types in their credit card details and billing address, your payment gateway doesn't bother sending the entire street name or city. Instead, it just pulls out the numerical parts: the street number (like 123 in 123 Main St) and the ZIP code (like 90210).

These numbers get bundled up with the payment authorization request and zipped over to the credit card’s issuing bank. This all happens behind the scenes in a split second, completely invisible to your customer.

The Bank's Instant Reply

Once the bank gets the request, its system does a quick, simple comparison. It checks the street number and ZIP code you sent against the official billing address it has on file for that specific cardholder.

Then, the bank sends back a single-letter AVS response code. This code is its verdict, telling your payment system how well the numbers lined up. It could signal a perfect match, a partial match, or a total mismatch.

The whole three-step journey is really that straightforward.

As you can see, the AVS check is a direct line of communication that confirms key details without ever slowing down the checkout experience.

Your Store Makes the Final Call

Now, this is the most important part: the AVS check itself doesn't approve or decline the transaction. The bank still authorizes the payment based on whether the customer has enough funds. The AVS code is just extra information—a risk signal—sent back to you.

It’s up to you what happens next. Based on that AVS code, your payment gateway follows the rules you’ve set. You might configure it to automatically approve perfect matches, flag partial matches for a quick manual review, or instantly reject transactions with a clear mismatch.

This setup puts you in the driver’s seat, letting you balance tight security with a smooth customer checkout. The entire AVS check happens in a blink, making it an incredibly powerful tool for stopping fraud in card-not-present sales where you can't physically see the card.

By understanding this simple flow, you can see how AVS provides a solid first line of defense against fraudsters who might have a stolen card number but don’t know the exact billing details.

Decoding the Most Common AVS Response Codes

AVS response codes can feel a bit like a secret language sent back from the bank, but they’re your key to making smarter, data-driven decisions about potentially risky transactions. Learning what these single-letter codes mean is like learning to read the signals that separate legitimate customers from fraudsters.

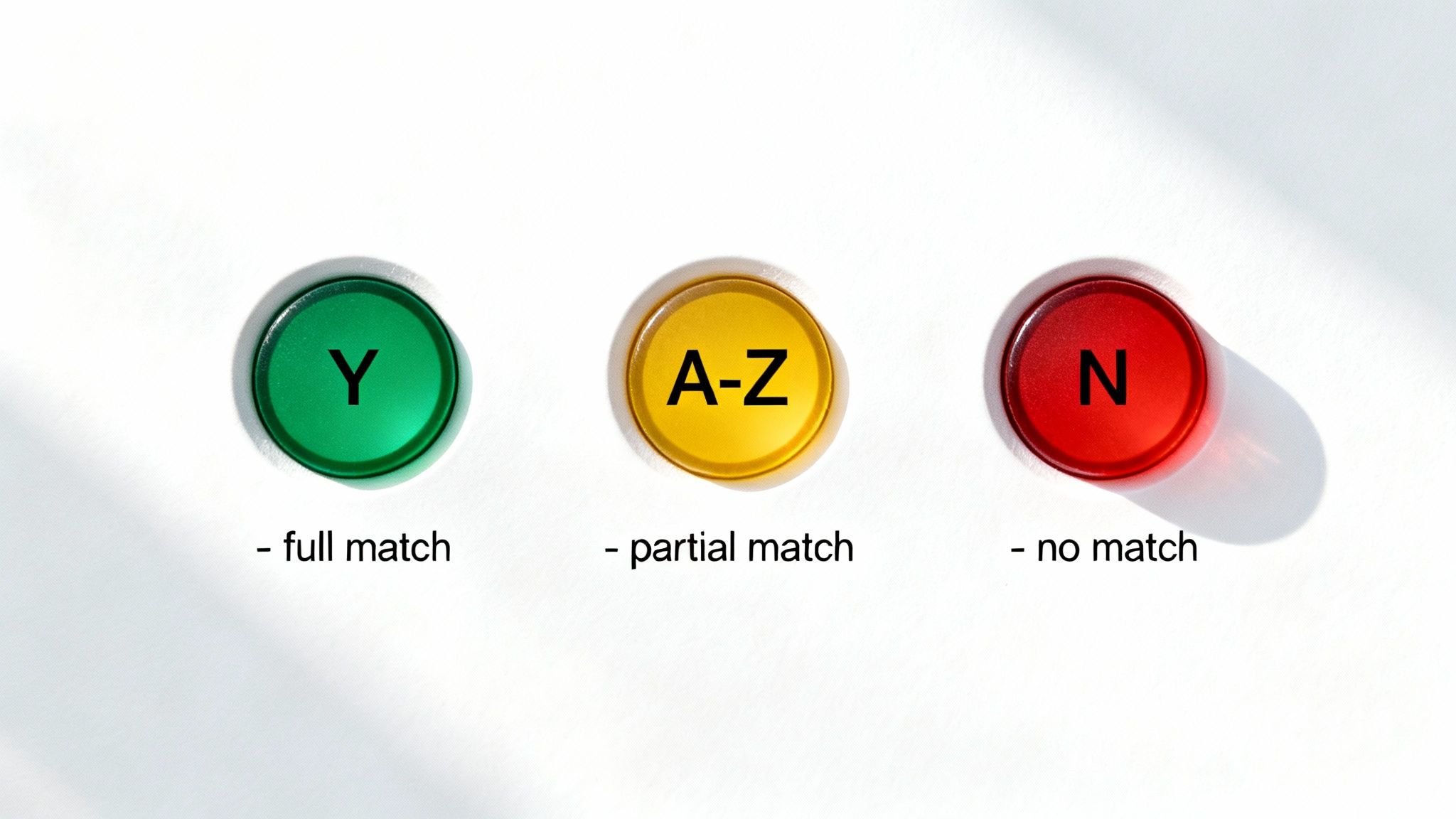

To keep it simple, we can group the most common AVS codes into a familiar “traffic light” system. This helps you quickly size up the risk level of a transaction and decide what to do next without any guesswork.

Green Light Codes: Full Match

Getting a green light from your AVS check is the best possible outcome. It signals a very low risk of fraud because the information your customer provided lines up perfectly with what their bank has on file.

- Code Y - Full Match: This is the gold standard. It means both the street number and the ZIP code the customer entered are an exact match.

- Recommended Action: Approve the transaction confidently. A 'Y' code is a strong sign that the person making the purchase is the real cardholder.

This level of verification is especially critical in markets like North America, which commands a massive 37% of the global Address Verification Software market. In the US, financial institutions and merchants using platforms like Shopify rely heavily on AVS to comply with strict regulations, helping to cut down on fraudulent claims by an estimated 25-40%. You can dig into more market insights from the Address Verification Software market report.

Yellow Light Codes: Partial Match

Yellow light codes are where you need to pay a bit more attention. These codes mean some of the information was correct, but not all of it. This isn’t an automatic red flag for fraud—it could be a simple typo, a customer who recently moved, or someone using a work address. Still, it warrants a moment of caution.

- Code A - Address Match Only: The street number (e.g., 123) matches, but the ZIP code does not. This can easily happen if a customer mistypes their ZIP.

- Code W/Z - ZIP Code Match Only: The ZIP code matches, but the street number does not. This is also common with typos or if someone enters a general company address instead of a specific office number.

For these partial matches, you’ve got a few options.

Recommended Action: Manually review the order. Instead of an automatic decline, which could turn away a legitimate customer, flag these transactions. Take a look at other risk factors like the order value, shipping address, or the customer's purchase history before making a final call.

Red Light Codes: Mismatch or Error

A red light code is a clear warning sign. It points to a major mismatch between the information provided and the bank's records, suggesting a high probability of fraud.

- Code N - No Match: This is the most straightforward red flag you can get. Neither the street number nor the ZIP code matches what the bank has on file.

- Recommended Action: Decline the transaction. A full mismatch is a very strong signal that the person using the card isn't the authorized owner. Approving these orders opens you up to a huge risk of a chargeback.

On top of that, you might see codes that point to a technical issue rather than a customer error.

- Code U - Unavailable: The card-issuing bank couldn't provide AVS information. This is pretty common with international cards where AVS isn't fully supported.

- Code S - Service Not Supported: The card issuer doesn't participate in AVS. This also happens a lot with cards from outside the US, UK, and Canada.

To make things even easier, here’s a quick-reference guide to help you remember the most critical codes and what to do when they pop up.

Common AVS Response Codes and What to Do

By translating these codes into clear, actionable steps, you can fine-tune your AVS address verification rules. The goal is to strike that perfect balance between blocking fraudsters and giving your real customers a smooth checkout experience. This proactive approach turns AVS from a simple feature into a strategic tool for protecting your revenue.

Where AVS Falls Short and How Fraudsters Get Through

While AVS is a fantastic first line of defense against fraud, it’s not a silver bullet. Thinking of it as an impenetrable wall is a mistake; it's much more like a sturdy fence with a few well-known gaps. Understanding these limitations is the key to building a fraud prevention strategy that actually works.

One of the biggest blind spots is that AVS only checks numbers, not letters. It compares the street number and ZIP code, completely ignoring the street name, city, or apartment number. A fraudster could enter "123 Fake Street" instead of "123 Main Street," and as long as the numbers "123" and the correct ZIP code match the bank's records, it could still pass as a partial match.

The International Blind Spot

Another massive limitation is geography. AVS is primarily a standard in the United States, United Kingdom, and Canada. Outside of these countries, support from issuing banks is inconsistent at best.

When you process an international order, you'll often get an AVS response code like 'U' (Unavailable) or 'S' (Service Not Supported). This doesn't mean the transaction is fraudulent, but it does mean one of your key verification tools is offline. Fraudsters are well aware of this and often use internationally issued cards specifically to bypass AVS checks.

Relying solely on AVS for international sales is like trying to navigate a new city with a map of your hometown. You're missing the critical information needed to make a safe and informed decision.

When Fraudsters Have All the Right Information

The most challenging scenario is when a fraudster has a complete set of stolen data. If a criminal gets their hands on a stolen credit card number, CVV, and the cardholder's exact billing address from a data breach, AVS will see it as a legitimate transaction.

This is because AVS isn't designed to know who is entering the information, only that the information itself is correct. When a full data set is compromised, the transaction will sail right through an AVS check, resulting in a fraudulent order that you ship and a chargeback you'll almost certainly lose. These situations can sometimes be mistaken for other issues, like friendly fraud, so it helps to understand the nuances.

On top of that, AVS doesn't help with other compliance needs. While it's great for tackling billing address issues, other crucial measures like age verification for online sales are necessary to address specific legal challenges and deter bad actors targeting age-restricted products.

These gaps don't make AVS worthless—far from it. They simply highlight why it should never be your only line of defense. It's an essential first step, but a truly secure e-commerce store needs a multi-layered approach to outsmart modern fraud tactics.

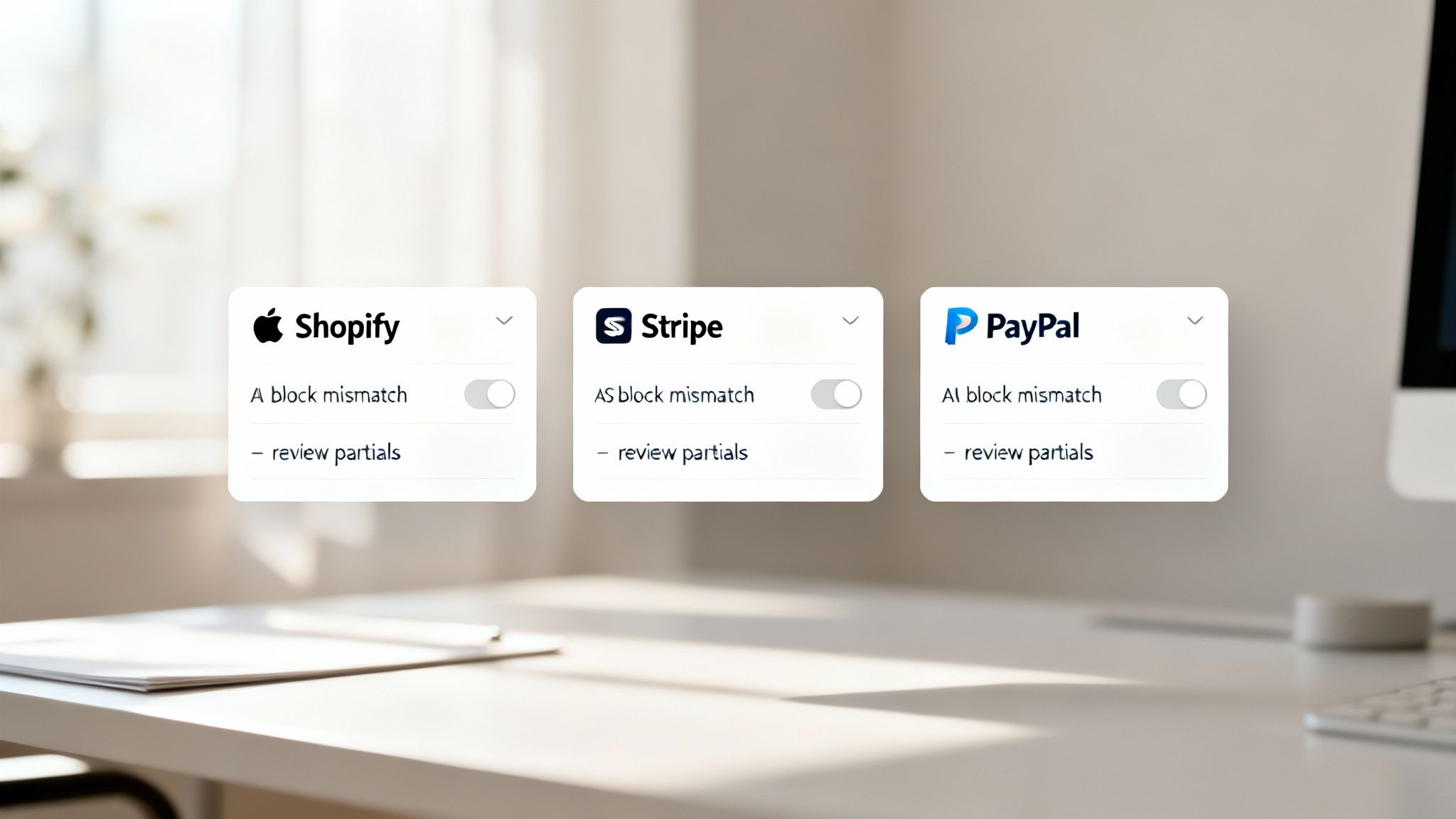

Setting Up AVS on Shopify, Stripe, and PayPal

Ready to put AVS to work protecting your store? Let's be honest, activating and tweaking your Address Verification Service settings is one of the fastest and most powerful moves you can make to start shutting down fraud. Most major payment platforms have these controls built right in, giving you the power to set the rules for how your store handles address mismatches.

The goal is to find that perfect balance between iron-clad security and a smooth checkout for your customers. You want to automatically reject transactions that are obviously fraudulent without accidentally blocking legitimate shoppers who just made a simple typo.

Let's walk through how to find and configure these settings on Shopify, Stripe, and PayPal.

AVS Setup for Shopify Payments

If you’re on Shopify Payments, good news—AVS is already working for you behind the scenes. Shopify automatically runs AVS checks as part of its native fraud analysis. But you can—and should—refine how it behaves by setting up a few simple rules.

You'll find these options in your Shopify admin dashboard. Just head over to Settings > Payments > Manage. In the fraud prevention section, you'll see two key AVS-related checkboxes:

- Decline charges that fail AVS postal code verification: This is your strictest, most effective rule. If the customer’s ZIP or postal code doesn't match what their bank has, the transaction is instantly blocked.

- Decline charges that fail AVS street address verification: This rule blocks any transaction where the numeric part of the street address is wrong.

For maximum security, you can enable both. This setup is incredibly aggressive against fraudsters who have stolen card details but don't have the complete, correct billing address. If you're weighing your options, our guide on Shopify Payments vs. Stripe dives deeper into the nuances between these platforms.

Configuring AVS Rules in Stripe

Stripe gives you much more fine-grained control over your AVS address verification rules, letting you create custom logic using Stripe Radar. By default, Stripe performs an AVS check on every transaction but doesn't automatically block them. You have to tell it what to do.

To set up rules, pop over to your Stripe Dashboard and go to Radar > Rules. Here, you can build custom rules with a simple “if-this-then-that” structure. For instance, you could create a rule that looks like this:

Block if :avs_postal_code_match: == 'fail' AND :avs_street_match: == 'fail'

This rule tells Stripe to automatically decline any transaction where both the street number and the ZIP code fail the AVS check—a full 'N' mismatch. You could also create rules to flag partial mismatches for manual review, giving you a chance to look at other risk signals before deciding to approve or decline.

Customizing AVS in PayPal

PayPal also includes AVS in its fraud management toolkit, especially for merchants using services like PayPal Payments Pro. You can find your settings in your PayPal account under Account Settings > Website payments > Payment receiving preferences.

Here, you get to set your risk controls and tell PayPal how to handle transactions based on different AVS responses. You can choose to:

- Accept all payments, no matter what the AVS result is (not recommended).

- Deny payments that get a full mismatch ('N' code).

- Flag transactions with partial matches ('A' or 'Z' codes) so you can review them.

For most businesses, setting PayPal to deny transactions with a full mismatch is a solid and effective starting point. This ensures you’re protected from the most blatant fraud attempts.

Getting these settings right is more important than ever. The Address Verification Software market is projected to grow from USD 6.65 billion to USD 12.1 billion in just nine years, a surge driven by merchants trying to curb the $50 billion lost annually to failed deliveries and fraud. You can check out more details about this market growth on marketresearchfuture.com. Taking a few minutes to configure these AVS settings gives you direct control over your store's security.

Beyond AVS: How ChargePay Secures Your Revenue

AVS address verification is a fantastic gatekeeper for your online store. Think of it like a bouncer at your checkout, checking IDs and turning away obvious imposters before they can cause any trouble. By filtering out transactions with mismatched billing info, you stop a huge chunk of fraud before a sale is even finalized.

But what happens when a fraudulent transaction looks legitimate? What about the disputes that still slip through, even with perfectly tuned AVS rules? This is exactly where your revenue protection strategy needs a powerful second layer.

From Prevention to Recovery

Think of your security as a two-part system. AVS is your proactive defense—it works right at the point of sale to stop fraud before it happens. It’s fast, efficient, and catches a ton of common fraud attempts.

But AVS isn’t a silver bullet. It’s powerless against a savvy fraudster who has stolen a complete set of card details, including the correct billing address. Even more importantly, AVS can't do a single thing about friendly fraud, where a real customer makes a purchase and then disputes the charge later on. These disputes sail right past your preventative measures and slam your bottom line as chargebacks.

This is where ChargePay steps in.

While AVS works before a sale is finalized, ChargePay works after a sale is disputed. It’s not about preventing the transaction anymore; it’s about recovering the revenue you’re at risk of losing.

ChargePay is your post-transaction recovery expert. The moment a chargeback lands in your account, our system gets to work.

How AVS and ChargePay Work Together

A strong AVS address verification setup cuts down on the number of fraudulent transactions that turn into chargebacks. ChargePay then takes on the disputes that inevitably get through, creating a complete revenue protection cycle.

Here’s how they complement each other:

- AVS Prevents Obvious Fraud: It acts as your front-line filter, blocking transactions where the billing address details are clearly wrong.

- ChargePay Recovers Disputed Revenue: For disputes that slip past AVS—like friendly fraud or cases with fully stolen data—ChargePay uses AI to automatically build and submit compelling evidence on your behalf.

This dual approach means you’re not just stopping fraud at the door, but you’re also winning back money from the disputes you can’t avoid. By automating the evidence-gathering and submission process, ChargePay takes the manual headache out of fighting chargebacks, so you can focus on growing your business.

A complete strategy involves both prevention and recovery. For a deeper dive into how automation is changing the game, explore our guide to building a chargeback management system with AI. This combination is the key to truly securing your revenue.

Frequently Asked Questions About AVS

Even when you've got a handle on how AVS address verification works, some questions always pop up. Let's tackle the most common ones merchants ask so you can put AVS to work in your store with more confidence.

Can AVS Stop All Fraud?

Nope, and it was never meant to. Think of AVS as a solid lock on your front door—it's fantastic for stopping a casual thief from walking in, but a determined pro will still try to find another way. AVS is your first line of defense, great for catching fraudsters who have a stolen card number but don't know the matching billing address.

But it’s completely powerless against a fraudster who has the full package: the card number, CVV, and the exact billing address, usually scooped up from a data breach. It also does nothing to stop friendly fraud, where a legitimate customer disputes a charge they actually made. That’s why AVS should always be just one layer in a much broader security strategy.

What Is the Difference Between AVS and CVV?

Think of AVS and CVV as two different security guards checking different pieces of ID. They work together, but they’re looking for completely separate things.

- AVS (Address Verification Service): This guard checks the billing address the customer types in against the one the bank has on file. It basically confirms, "Does this person know where the real cardholder lives?"

- CVV (Card Verification Value): This is that little 3- or 4-digit code on the card itself. This guard is checking for one thing: "Does the person making this purchase have the physical card in their hand?"

A thief might snag a credit card number and address from an online database, letting them pass the AVS check. But without the actual card, they won't have the CVV. On the flip side, someone who steals a physical wallet has the CVV but might not know the billing ZIP code. Using both checks together throws up a much bigger wall against fraud.

Does AVS Work for International Sales?

This is a big "it depends." The reliability of AVS varies a lot from country to country. It’s a rock-solid tool in the United States, United Kingdom, and Canada, where it’s widely supported.

Once you go beyond those borders, support from international banks gets spotty. For many sales outside those core countries, you’ll get AVS codes like 'U' (Unavailable) or 'S' (Unsupported). This simply means the customer’s bank doesn't participate, so you can't rely on it. In these situations, you have to lean more heavily on other signals like the CVV match, IP geolocation, and the customer's order history.

Will Strict AVS Rules Hurt My Sales?

They absolutely can if you're not careful. Cranking your AVS rules up to the max can lead to false declines—turning away legitimate customers who just made a simple typo or moved recently. For example, if you automatically block every transaction that doesn't return a perfect 'Y' match, you're going to frustrate good customers and send your conversion rates plummeting.

The trick is finding a healthy balance. A smart, common strategy is to automatically decline transactions with a complete mismatch (Code N) but to flag partial matches (like Codes A or Z) for a quick manual review. This approach lets you stop the most obvious fraud without slamming the door on real customers.

While AVS is a great tool for stopping fraud before it happens, it can't do anything to get your money back from disputes that sneak through. That's where ChargePay comes in. We use AI to automatically fight and win chargebacks for you, giving you a complete system for protecting your revenue. Protect your business and recover lost revenue with ChargePay.

.svg)

.svg)

.svg)

.svg)