A chargeback on a debit card is what happens when a customer disputes a transaction with their bank, and the bank yanks the funds right out of your business account. This isn't like a credit card dispute, where it's a line of credit being adjusted. We're talking about actual cash being removed immediately.

What Happens During a Debit Card Chargeback

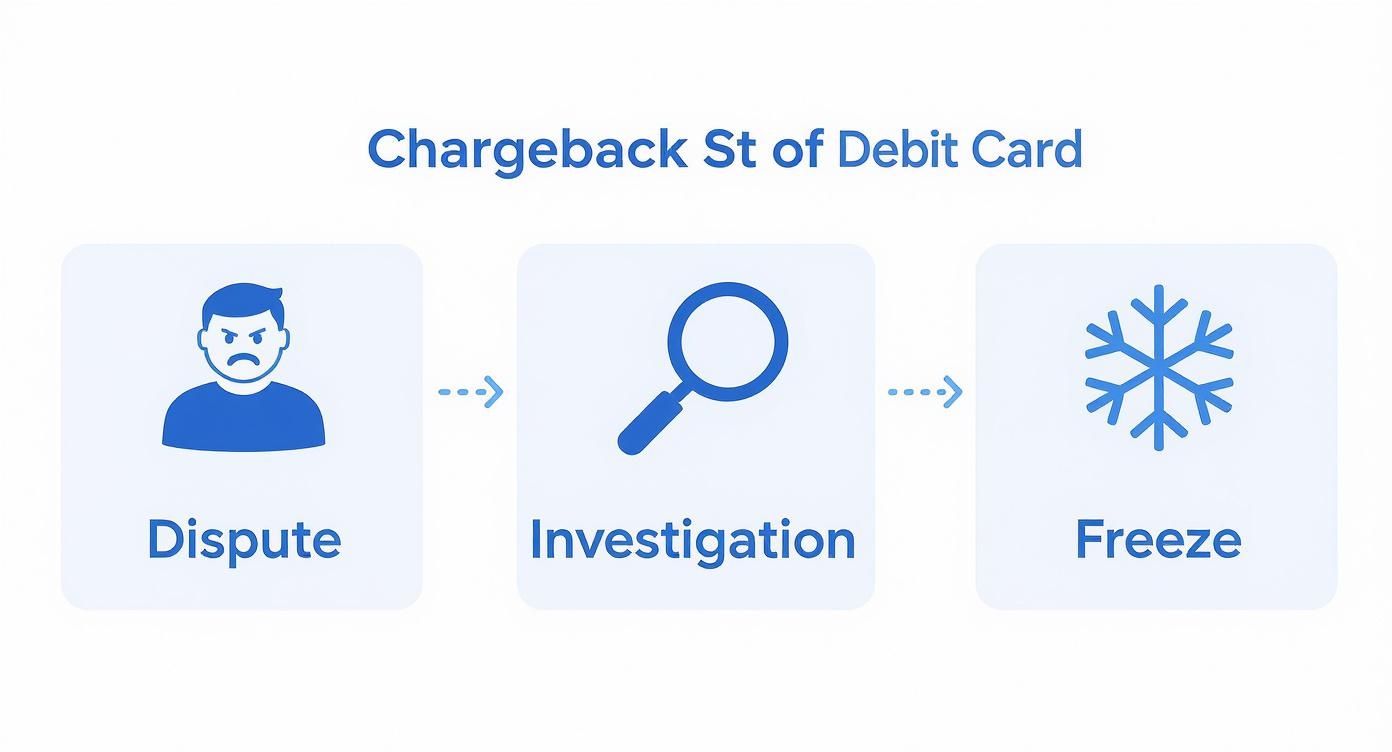

You can think of a debit card chargeback as an official replay review for a sale, kind of like in a football game. When a customer thinks a charge is wrong—maybe it's fraud, an issue with the product, or just a simple mix-up—they don't just call you for a refund. Instead, they go straight to their bank, the "referee," to officially challenge the transaction.

This call kicks off a formal investigation. The very first thing the bank does is pull the disputed money directly from your merchant account and puts it on hold. And this happens before you even get a chance to share your side of the story. Your funds are basically frozen while the bank looks over the evidence from both you and the customer.

This is the critical sequence of events: the customer complains, the bank investigates, and your funds are frozen on the spot.

As you can see, this whole process moves fast, often catching merchants completely off guard.

The Growing Challenge for Merchants

Getting a handle on this process is more important than ever. The number of disputes for both chargeback debit cards and credit cards is on the rise, thanks to the explosion in online shopping. In fact, global chargeback cases are projected to reach a staggering 337 million by 2025. That’s a huge 27% jump from 2022. This trend alone makes mastering the dispute process non-negotiable if you want to protect your revenue.

The core takeaway is simple but crucial: When a debit card chargeback is filed, your money is taken first and questions are asked later. This "guilty until proven innocent" model puts the immediate burden of proof squarely on your shoulders.

This initial phase really sets the tone for the entire dispute lifecycle. For merchants, reacting quickly and correctly isn't just a good idea—it's essential for survival. To get a bird's-eye view, you can check out our guide on the complete card dispute process.

How Debit and Credit Card Disputes Differ

Many merchants see a dispute notification and jump into action, using the same playbook for every single case. But here’s a pro tip: treating a debit card dispute like a credit card dispute is a costly mistake.

On the surface, they might look the same. A customer is unhappy, and you’re at risk of losing a sale. But underneath it all, they operate under completely different sets of federal rules that directly impact your business, your cash flow, and your strategy.

At the heart of it are two key pieces of legislation. Debit card disputes are governed by the Electronic Fund Transfer Act (EFTA), while credit card disputes fall under the Fair Credit Billing Act (FCBA). Think of them as two separate rulebooks for two different games.

This isn't just legal trivia; it changes everything. We're talking about how long a bank has to investigate, how much liability a customer has in a fraud case, and most importantly, how the money is handled from your account.

A Tale of Two Timelines

The most immediate difference you'll feel is in your bank account. As we touched on, when a customer disputes a debit card transaction, that money is pulled directly from your merchant account almost instantly. Why? Because the EFTA is designed to protect a consumer’s actual cash.

Credit card disputes, on the other hand, involve a line of credit. The disputed amount is typically suspended from the cardholder's bill while the investigation is happening. It’s a pause on a debt, not a withdrawal of cash that’s already been spent. This fundamental difference is what makes debit disputes feel so much more disruptive.

The core difference is this: a debit dispute freezes your actual cash, while a credit dispute pauses a debt collection. This is why debit card chargebacks can feel much more disruptive to your daily operations and financial planning.

The timelines for investigation and the caps on customer liability also vary significantly between the two. Understanding these nuances is the first step toward building a much smarter, more effective response strategy. For a deeper look into the specifics of credit card cases, you can explore our guide on how to win a credit card dispute.

Debit Card vs. Credit Card Dispute Regulations

To really see how these disputes stack up, it helps to put them side-by-side. The table below breaks down the most critical distinctions that every merchant needs to know.

As you can see, while there are some similarities, the source of the funds and the consumer liability rules are worlds apart. Knowing which "game" you're playing is crucial to protecting your revenue.

The Real Reasons Customers File Chargebacks

When that chargeback notification lands in your inbox, it's easy to jump to conclusions. You probably picture a scammer with a stolen credit card number. While that definitely happens, it’s only one part of a much bigger story. Figuring out why customers really file disputes is the first and most important step to stopping them before they start.

Chargebacks usually boil down to one of three main reasons. Each one has a different root cause, which means you need a unique game plan to handle it.

True Criminal Fraud

This is the one every merchant immediately thinks of. True fraud is exactly what it sounds like: a criminal gets their hands on someone's debit card details and goes on a shopping spree. The actual cardholder eventually spots the charge, has no idea what it is, and rightfully reports it to their bank.

In these situations, the chargeback is legit. Trying to fight it is almost always a losing battle. Your focus here shouldn't be on winning the dispute itself, but on beefing up your fraud detection tools to catch and block these transactions from ever going through.

Unintentional Merchant Error

This one can be a tough pill to swallow because it means the chargeback was likely your fault—and totally preventable. A huge chunk of disputes comes from simple, fixable mistakes you might not even realize you're making.

Here are a few common slip-ups you've probably encountered:

- Confusing Billing Descriptors: Your customer bought from "Glimmer Jewelry," but their bank statement shows a charge from "SPARKLE*CO LLC." They don't recognize the name and panic, assuming it's fraud.

- Shipping Delays: The order shows up weeks late, long after the customer needed it for a special occasion. Instead of bothering with a return, they just file a chargeback.

- Poor Communication: The customer couldn't find your contact info, or your return policy was a maze of confusing rules. A chargeback becomes their path of least resistance.

A lot of chargebacks are just a symptom of an unhappy customer. It's always worth digging into why customers get frustrated in the first place, and a great starting point is understanding and avoiding common customer service errors.

Intentional Friendly Fraud

This is, without a doubt, the most maddening type of chargeback for any business owner. Friendly fraud is when a customer makes a perfectly legitimate purchase with their own card, receives the product, and then disputes the charge anyway.

They might lie and claim the item never arrived, or maybe they just have a case of buyer's remorse and see a chargeback as a sneaky way to get a refund without sending the product back.

This form of "cyber shoplifting" is exploding, and some reports show it accounts for up to 70% of all chargebacks. It's a tricky problem because you’re forced to prove your own customer is being dishonest.

To get a better grip on this growing headache, you can check out our deep dive on how to spot and fight friendly fraud. Once you understand these three root causes, you can start building a smarter strategy that’s all about prevention, not just damage control.

Calculating the True Cost of a Chargeback

When you get a chargeback notification, the first thing you probably feel is the sting of the lost sale. That hurts, but it’s only the tip of the iceberg. The real financial damage from a debit card chargeback goes way deeper, piling on costs that can seriously kneecap your business.

It’s not just about giving the customer their money back. Think of each dispute as a small financial wrecking ball, swinging at your bottom line from multiple angles. To really get the full picture, you have to add up all the collateral damage.

The Hidden Financial Damage

Imagine a chargeback as a stack of bills you suddenly have to pay. The first and most obvious one is the original transaction amount that gets yanked right out of your account. But then, your payment processor starts adding to the pile.

On top of refunding the sale, you also lose the non-refundable processing fees you already paid just to handle the transaction. Then comes the real kicker: a separate, and often steep, chargeback fee. You can learn more about how this specific penalty works in our guide on what is a chargeback fee. This fee alone can run anywhere from $20 to $100 for every single incident.

And finally, there's a cost that never shows up on an invoice: your time. Every hour your team spends digging through records, writing responses, and managing the back-and-forth is an hour they’re not spending on growing the business.

The Rising Tide of Dispute Costs

This isn’t just a minor cost of doing business; it's a growing financial threat. The total impact of global chargebacks is projected to climb from $33.79 billion in 2025 to nearly $41.69 billion by 2028. For merchants like you, the cost is far more than just the price of the lost product, especially when you factor in administrative overhead and potential penalties. You can find more insights about the rising costs of disputes on b2b.mastercard.com.

When you add it all up—the lost sale, processing fees, chargeback penalties, and your team's labor—the true cost of a single chargeback can easily be two to three times the original transaction value.

If your chargeback rate starts to creep up, the consequences get even more severe. Payment processors watch this metric like a hawk. A high rate can trigger bigger penalties, like higher processing fees on all your future sales. In the worst-case scenario, they could terminate your merchant account entirely. Seeing the complete financial picture makes it clear why managing chargeback debit cards proactively isn't just good practice—it's essential for survival.

A Step-by-Step Plan to Win Your Disputes

When an unfair chargeback hits your account, it can feel like you've been robbed. And in a way, you have. But you don't have to just take the hit. You have the right to fight back through a process called representment.

Don't let the fancy term intimidate you. It just means you get to re-present the transaction to the bank, this time armed with evidence that it was a legitimate sale.

Think of it like you're building a court case. The customer's bank is the judge, and your job is to hand them a file of compelling evidence so clear and convincing that it leaves no room for doubt. Tossing together a disorganized response is a surefire way to lose. Your goal is to make it incredibly easy for the bank to rule in your favor.

This isn't just about winning back the money from a single dispute. A strong, professional representment strategy shows banks that you're a diligent merchant, which helps protect your reputation in the long run.

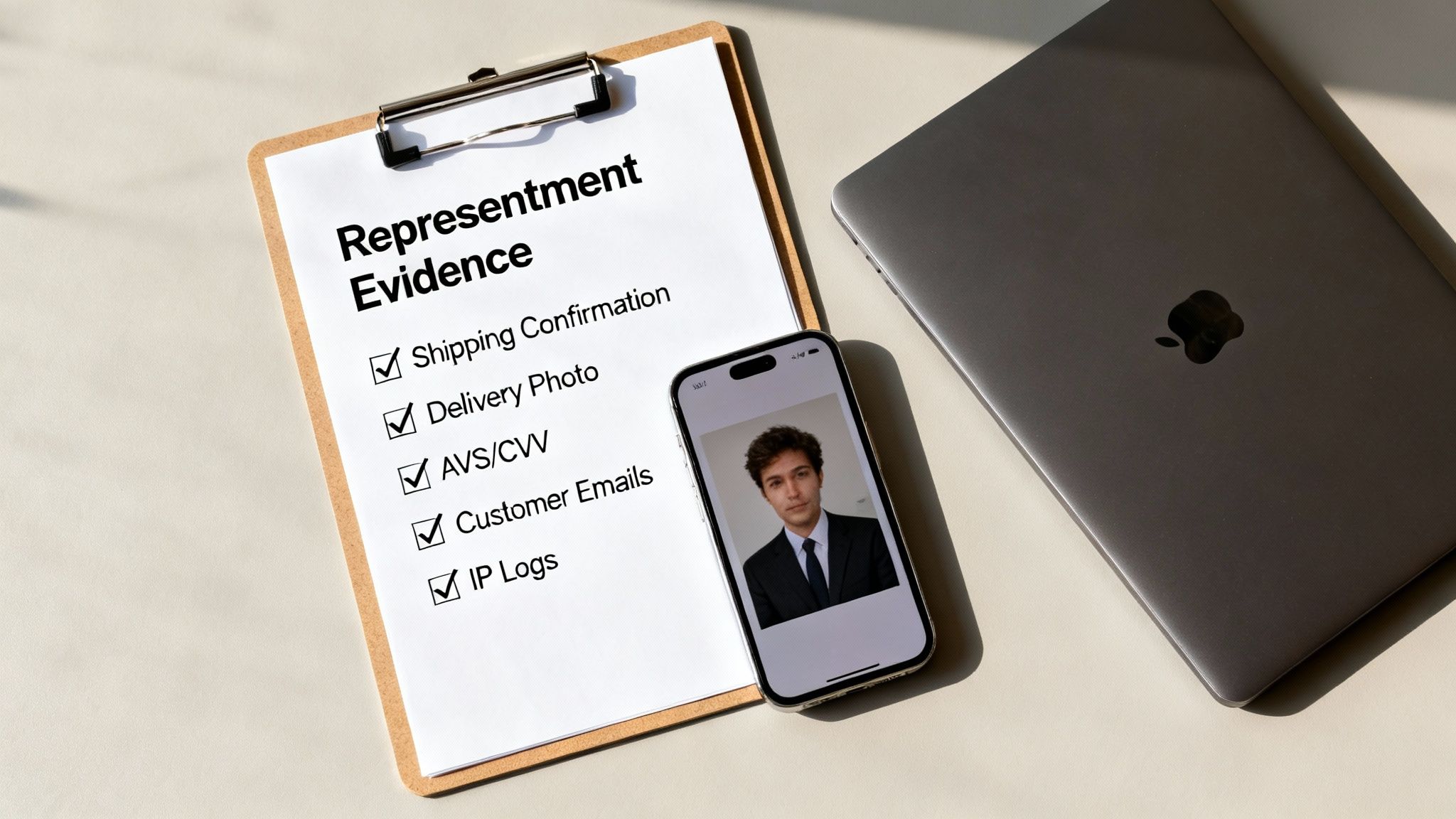

Building Your Evidence File

The secret to winning a dispute over a chargeback debit card transaction is simple: provide the right proof for the right situation. Your evidence needs to be a direct counterpunch to the customer's specific claim.

A claim of "product not received" requires a completely different defense than a claim of "unauthorized transaction." Start by looking up the chargeback reason code, then get to work gathering all the relevant documents.

Your evidence checklist should look something like this:

- Proof of Authorization: Show that the actual cardholder approved the purchase. This is where AVS (Address Verification Service) and CVV security code matches are your best friends.

- Transaction Details: Include the nitty-gritty—the exact date, time, and amount of the purchase. For digital goods, the customer's IP address and device info are gold.

- Order and Shipping Confirmations: Attach copies of every email or message you sent the customer, from the initial order confirmation to any shipping updates.

- Proof of Delivery: For physical products, this is non-negotiable. A signed delivery receipt or a clear photo of the package on the customer's doorstep is incredibly powerful.

- Customer Communication: Did the customer email you before filing the dispute? Include screenshots of any conversations, especially if they show they were happy with the product or confirmed they received it.

The goal is to paint a complete picture of the transaction from start to finish. You want to create a timeline that shows a legitimate customer made an authorized purchase and received exactly what they paid for.

Submitting a Winning Response

Once you have your evidence locked and loaded, it's time to assemble your case. Write a clear, concise rebuttal letter that summarizes why you're right. Stick to the facts and professionally explain why the chargeback is invalid.

Attach your evidence in a logical order that makes it easy for the bank's reviewer to follow the story. Remember, these reviewers look at hundreds of cases a day. A well-organized, easy-to-digest package is far more likely to get a thumbs-up than a messy pile of random files.

Fighting back against unfair chargebacks is your right as a merchant. By gathering compelling evidence and presenting it clearly, you can protect your hard-earned revenue and send a strong message to anyone trying to game the system.

How Automation Simplifies Chargeback Management

Manually fighting every single chargeback is like trying to put out a forest fire with a water pistol. It's a slow, soul-crushing process that eats up your time, energy, and resources, all while revenue is literally walking out the door. For every dispute, you're stuck digging through records, hunting for the right evidence, and racing to submit it before a non-negotiable deadline. It's an administrative nightmare that pulls you away from what you should be doing: running your business.

This is exactly where automation steps in. Modern tools built for dispute management can take over the entire representment process, transforming a manual headache into a nearly hands-off solution. Instead of you chasing down documents, these systems do all the heavy lifting.

Working Smarter, Not Harder

Automation platforms plug directly into your payment processor, whether it's Stripe, Shopify, or another provider. The moment a chargeback on a debit card lands, the system springs into action. It uses AI to instantly analyze the chargeback reason code and then automatically gathers the most compelling evidence to fight it.

This isn’t just basic data entry. The system pulls together a complete picture, including things like:

- Customer purchase history and any communication records

- AVS and CVV match results from the transaction

- Shipping confirmations and proof of delivery

- IP address logs for digital sales

From there, the system compiles all this data into a professional, ready-to-submit dispute package. Here’s a look at how a tool like ChargePay visualizes this evidence-gathering process to build the strongest possible case for you.

This intelligent approach makes sure every response is fine-tuned to win, based on exactly what the banks need to see to reverse the chargeback.

The benefits are immediate and obvious. You completely eliminate the risk of missing a response deadline, which is an automatic loss. More importantly, you dramatically increase your odds of winning. In fact, merchants often see their win rates jump significantly by putting AI-powered evidence on their side. It's all about protecting your bottom line without having to sacrifice your time. To get a deeper look at how it works, check out this complete guide to automated chargeback and dispute management using AI.

Common Questions About Debit Card Chargebacks

Dipping your toes into the world of debit card chargebacks can feel a bit like navigating a maze. As a merchant, you've probably got a ton of questions. We've compiled the most common ones we hear to give you clear, straightforward answers you can use right away.

How Much Time Do I Have to Respond to a Chargeback?

You've got a window, but it's not a big one. Typically, you'll have somewhere between 20 to 45 days to get your response in. The exact deadline depends on the card network, like Visa or Mastercard.

And trust me, this deadline is non-negotiable. If you miss it, you automatically lose the dispute. The money is gone for good. That’s why being organized and acting fast isn't just good advice—it’s essential to protecting your revenue.

Can I Stop Friendly Fraud Before It Happens?

You can’t stop it completely—that would be impossible. But you can absolutely put a serious dent in it. The secret sauce here is crystal-clear communication with your customers.

Your goal should be to make it ten times easier for a customer to contact you for help than it is to call their bank. Think about it from their perspective and put these simple but powerful steps in place:

- Use a clear billing descriptor so your company name is instantly recognizable on their bank statement. No more "What is this charge from XYZ Corp?"

- Send detailed order and shipping confirmation emails the second a purchase is made. Keep them in the loop.

- Make your return policy easy to find and even easier to understand. No confusing legal jargon.

Does Winning a Dispute Fix My Chargeback Ratio?

This is a big one, and the answer is, unfortunately, no. Your chargeback ratio is calculated based on the number of disputes filed against you, not how many you win.

Every single chargeback that gets initiated counts against your ratio, regardless of the final outcome. This is a crucial point many merchants overlook.

This is exactly why preventing disputes in the first place is the only real long-term strategy. Keeping that ratio low is absolutely vital for maintaining a healthy merchant account and staying on the right side of your payment processor.

Stop losing revenue to confusing and time-consuming disputes. ChargePay uses AI to automate the entire chargeback process, boosting your win rate and recovering your funds without any manual work. Protect your business today at chargepay.ai.

.svg)

.svg)

.svg)

.svg)