Getting a debit card chargeback notification can feel like a punch to the gut. Unlike a simple refund request, a chargeback from a debit card is a forced reversal that yanks funds directly from your account, often weeks after you thought a sale was settled. It's a formal dispute, and it demands your immediate attention.

Your First Moves After a Debit Card Chargeback

That notification email or dashboard alert kicks off a very short, very strict timeline. You can't afford to ignore it; failing to respond means you automatically lose the dispute and the money is gone for good. The first 24 to 48 hours are absolutely critical. What you do in this initial window can make all the difference between winning back your revenue and writing it off as a loss.

Immediately Identify the Reason Code

Every single chargeback is tagged with a specific "reason code." Think of this as a message from the customer's bank telling you exactly why they're disputing the charge. It might be something like "Transaction Not Recognized" or "Product Not Received."

Don't just glance at the code—dig in and understand what it actually means. This code is your roadmap. It dictates the kind of evidence you need to start gathering to fight back. For example, a "Product Not Received" claim is a clear signal to go find that tracking number, while a "Not as Described" claim means you need to pull up product photos and descriptions from your site.

Gather Your Initial Evidence Fast

Once you know the why from the reason code, it's a race against the clock to gather the what—your proof. Don't put this off. Records get buried, and crucial details can be forgotten. Your immediate goal is to piece together the story of a perfectly legitimate transaction.

Start with the basics:

- Order Details: Pull the original order, including the exact date, time, and purchase amount.

- Customer Information: Get the customer's name, email, shipping address, and billing address on file.

- Transaction Data: Look for the authorization details. Did you get a match on the AVS (Address Verification System) and CVV checks? Those are powerful pieces of evidence right from the start.

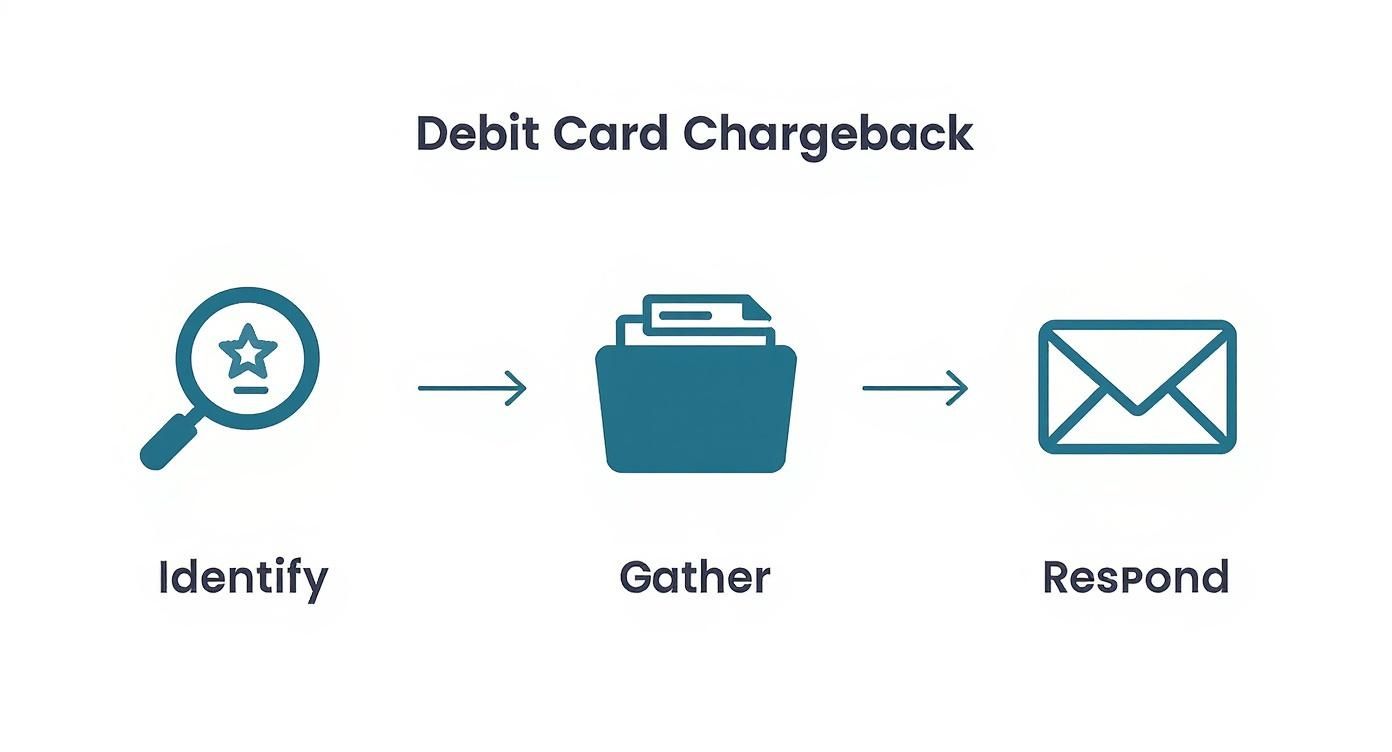

This infographic breaks down the simple, three-step flow every merchant should have locked down when a dispute hits.

This core process—Identify, Gather, Respond—is the foundation of any solid chargeback defense.

Dig Deeper for Compelling Proof

The basic transaction data is just your starting point. To build a case that actually wins, you need to add context and prove you delivered on your promise. The more specific and relevant your evidence is to the reason code, the better your chances are.

A winning dispute isn't just about having evidence; it's about presenting a clear, logical narrative that directly refutes the customer's specific claim. Make the bank reviewer's job easy by connecting the dots for them.

Let's talk about the kind of proof that really moves the needle:

- Proof of Delivery: For any "Product Not Received" claim, a tracking number showing "delivered" to the customer's address is non-negotiable. A delivery photo showing the package on their doorstep? Even better.

- Customer Communications: Did the customer email you before filing the chargeback? You need to include those conversations. They're especially powerful if they show the customer was happy or never mentioned the problem they're now claiming.

- Website and Policy Screenshots: If the claim is "Not as Described," grab screenshots of the exact product page the customer ordered from. You should also include your shipping and refund policies to prove the terms were clear from the beginning.

It helps to see how these initial steps fit into the bigger picture. You can learn more about the complete card dispute process in our detailed guide. Every piece of evidence you collect works together to tell one simple story: this was a valid sale. Getting that story straight is your only job in this first phase.

Building a Winning Chargeback Dispute

So, you've gathered all your files and screenshots. The next step is turning that raw data into a rock-solid, persuasive argument. This whole process is officially called representment, but I prefer to think of it as building an open-and-shut case for a judge. In this scenario, the judge is a reviewer at the customer's bank.

Your entire goal is to make their job as easy as humanly possible. These reviewers see dozens, if not hundreds, of these disputes every single day. A disorganized mess of files is an instant "no." But a clear, professional case that hits the customer's claim head-on? That’s how you get their attention and win.

The absolute cornerstone of your dispute package is the rebuttal letter. This isn't just a cover sheet; it's your opening argument and the summary of your entire case. It’s your one shot to frame the story in your favor right from the start.

Crafting a Powerful Rebuttal Letter

Your rebuttal letter needs to be short, factual, and laser-focused on the specific chargeback reason code. This is not the place for emotional language or long-winded stories about the customer. Stick to the cold, hard facts of the transaction and lay them out logically.

A killer letter follows a simple, effective structure:

- Introduction: Get right to the point. State the case number, transaction date, and amount right at the top.

- The Claim: Briefly mention the customer's claim (e.g., "The customer is claiming they never received the product.").

- Your Counter: Immediately punch back with your strongest piece of evidence (e.g., "However, our records and the attached FedEx proof of delivery confirm the package was delivered to the customer's verified address on [Date].").

- Evidence Summary: Bullet point the evidence you’ve attached and explain what each document proves.

This direct approach helps the reviewer grasp the entire situation in seconds. You’re not making them dig through attachments to piece the story together; you're handing them the completed puzzle. For a more detailed guide, check out this helpful example of a rebuttal letter to get you started.

https://www.chargepay.ai/blog/example-of-a-rebuttal-letter

Think of your rebuttal letter as the roadmap for your evidence. It should walk the bank reviewer through your proof, step-by-step, leaving zero doubt about the transaction's legitimacy.

Getting this right is more important than ever. The number of chargebacks globally is exploding, with projections expecting to see 337 million cases by the end of 2025. This flood is mostly thanks to the e-commerce boom and the fraud pressure on card-not-present (CNP) sales, which now account for 63% of all merchant revenue worldwide. With that much noise in the system, a professional, clear submission is the only way to stand out.

Organizing Your Evidence for Maximum Impact

How you organize your evidence is just as critical as what evidence you have. A random jumble of screenshots and receipts is a guaranteed way to lose. Your evidence needs to tell the story of the transaction in a logical, chronological order.

Try structuring it like this:

- The Order: Kick things off with the customer placing the order. Include screenshots of the product page, your checkout page showing your terms of service, and the order confirmation email you sent.

- The Payment: Next, show the successful payment authorization. If you have AVS and CVV match confirmations, make sure to highlight them.

- The Fulfillment: Follow up with the shipping confirmation and, crucially, the proof of delivery from the carrier that includes a valid tracking number.

- The Communication: Did you talk to the customer? Add any email chains or chat logs you have from before or after the purchase.

- Your Policies: Wrap it up with a clean screenshot of your return and shipping policies from your website.

This chronological flow makes your case intuitive. Each piece of evidence builds on the last, creating an undeniable paper trail of a legitimate sale.

Common Mistakes to Avoid in Your Submission

Even with mountains of proof, simple slip-ups can cost you the dispute. When you're fighting a chargeback from a debit card, avoiding these common pitfalls is absolutely essential.

- Missing the Deadline: This is the #1 mistake merchants make, and it’s the costliest. If you miss the submission window, you lose. No exceptions.

- Sending Disorganized Files: Don't just upload a folder of random attachments. Combine everything into a single, clearly labeled PDF.

- Ignoring the Reason Code: Your response has to be tailored. If the claim is "Product Not Received," evidence proving the product's quality is useless. Focus your entire argument on refuting that specific reason.

- Providing Too Little (or Too Much): Find the sweet spot. A one-sentence response won’t cut it, but a ten-page novel is overkill. Stick to the essential, most compelling proof.

By sidestepping these errors and presenting a professional, well-organized case, you dramatically boost your odds of winning the dispute and getting your money back.

How to Handle Disputes on Stripe, Shopify, and PayPal

Fighting a chargeback from a debit card isn't a one-size-fits-all process. The platform you use to take payments completely changes the game—each has its own dashboard, its own rules, and its own unique quirks. Let's break down the exact steps for the big three: Stripe, Shopify, and PayPal.

Knowing the specific workflow for your platform is a massive advantage. It means you can respond faster, submit the right evidence the first time, and avoid simple mistakes that could cost you the dispute before it even starts.

Navigating Stripe Chargebacks

Stripe is all about efficiency. When a dispute lands in your account, you'll find it right in your Dashboard under the "Disputes" section. Stripe does a great job of laying out the claim type, the amount at risk, and, most critically, your response deadline.

They make submitting evidence incredibly straightforward, either through their API or a simple upload form. Your goal here is to provide concise, high-quality proof. Stripe's review system favors clean, easily readable files, so don't just dump a folder of messy screenshots on them.

- Evidence is Your Weapon: For physical products, a tracking number with confirmed delivery is your silver bullet. For services, you need to show proof of use, like login records, project updates, or signed service agreements.

- Package it Neatly: I always recommend combining all your evidence—customer emails, delivery confirmations, screenshots—into a single, well-organized PDF. It makes the reviewer's job easier, and that can only help your case.

Stripe's documentation is top-notch, but you can get even more granular insights from our deep dive into the Stripe chargeback process. They give you a solid framework, but winning still boils down to the strength of your evidence.

Managing Disputes in Shopify

If you're on Shopify Payments, chargeback management is woven directly into your admin panel. You can find everything you need under Orders > Chargebacks. Think of Shopify as a helpful intermediary between you and the payment processor, guiding you through the chaos.

Shopify has a guided response process that prompts you for the specific info needed for different claim types. This structure is fantastic for making sure you don't miss anything obvious.

Shopify’s system walks you through the steps, but don't just fill in the blanks like a robot. Use the text fields to write a clear, compelling summary of events. Tell the story of the transaction from your perspective.

Winning Disputes in PayPal's Resolution Center

PayPal’s process is a bit of an island because it all happens within its own ecosystem. You'll manage everything through the Resolution Center, and you have to pay close attention to their specific terminology and timelines. A customer can open a "Dispute" first, which is your chance to resolve it directly with them before it escalates into a formal "Claim."

Once it becomes a claim, you're back in familiar territory: respond with evidence. PayPal places a huge emphasis on proof of shipment and delivery.

- Know Your Protections: Get familiar with PayPal's Seller Protection program. If you follow its rules to the letter (like shipping only to the address on the transaction details page), you might be covered even if you lose the dispute.

- Don't Wait: The deadlines in the Resolution Center are non-negotiable. Always respond to both the initial dispute and any escalated claims before time runs out.

Chargeback Evidence Checklist by Platform

While the process differs, the type of evidence needed is often similar across platforms. However, each one has its own priorities. Here’s a quick-reference table to help you focus your efforts where they matter most.

Submitting compelling evidence that aligns with what each platform values is the key to swinging a decision in your favor.

It’s crucial to remember that winning disputes isn't just about recovering a single transaction. A high volume of unresolved disputes can have serious consequences for your account's health, sometimes leading to devastating issues like handling an Amazon seller account suspension. Proactive dispute management is about protecting your entire business.

Recognizing and Fighting Friendly Fraud

Not every chargeback is a clear-cut case of a stolen card or a service that genuinely failed to deliver. Some of the most frustrating disputes come from perfectly legitimate customers—people who received their product, used your service, and then disputed the charge anyway.

This is the tricky world of friendly fraud, and it’s a massive headache for merchants.

It’s called "friendly" because there isn't necessarily malicious intent, at least not in the traditional sense. Often, a customer simply doesn’t recognize your business name on their statement. Other times, they forgot about a recurring subscription or maybe a family member used their card without telling them. Then there's simple "buyer's remorse," where a chargeback seems like a quicker, easier way to get a refund than going through your official returns process.

No matter the reason, the outcome for you is the same: a lost sale, a painful chargeback fee, and another hit to your merchant account's health. Fighting this kind of chargeback from a debit card requires a more surgical approach than a typical fraud case.

Spotting the Telltale Signs

Friendly fraud can be tough to pin down, but years of experience show there are common patterns to look for. The moment a dispute notification hits your inbox, ask yourself a few key questions.

- Did the customer contact you first? This is the big one. A customer with a legitimate issue will almost always reach out for a refund or a replacement before calling their bank. A chargeback that appears out of the blue is a major red flag.

- Is there a history of disputes? Some customers are, unfortunately, serial disputers. If your payment platform allows, check their order history for any previous chargebacks.

- Does the order seem normal? Does this customer have a history of successful, undisputed orders with you? Ironically, friendly fraudsters are often long-time customers who know exactly how the system works.

The rise of friendly fraud is a serious threat. Visa estimates that this type of dispute can account for up to 75% of all chargebacks. In 2023 alone, the average cardholder filed 5.7 chargebacks, with each dispute valued at around $76. You can discover more insights about this growing issue and why it’s so critical for merchants to address. Learn more about the 2025 cardholder dispute index from financialit.net

The Right Evidence to Fight Back

When you're up against a friendly fraud claim, your evidence needs to prove one thing above all else: that the legitimate cardholder authorized the purchase and received the value. You aren't fighting a thief; you're reminding a customer (and, more importantly, their bank) about a valid transaction they made.

Here’s the kind of proof that actually works:

- AVS and CVV Confirmations: Show that the correct billing address and security code were entered at checkout. This is strong evidence that the actual cardholder was present for the purchase.

- IP Address Logs: Match the IP address from the time of purchase to the customer's shipping address location. It helps paint a complete picture.

- Past Order History: A history of previous, undisputed orders sent to the same address is incredibly compelling. It establishes a clear, positive relationship with the customer.

- Delivery Confirmation with Photo: This is your silver bullet against "product not received" claims. Nothing beats a photo showing the item physically at their address.

- Customer Communications: Always include any emails or chat logs, especially if the customer discussed the product or acknowledged receiving it.

Fighting friendly fraud isn’t just about winning back one sale. Every chargeback you let slide encourages this behavior and hurts your reputation with payment processors. By building a strong, evidence-based case, you protect your revenue and your business's long-term health. If this topic is important to you, you might be interested in our dedicated article on how to handle friendly fraud.

Simple Ways to Prevent Chargebacks From Happening

Fighting a chargeback from a debit card is a defensive game. But the best defense? A really good offense. Preventing disputes before they even start saves you an incredible amount of time, money, and stress.

The good news is you don’t need a complex, expensive strategy. A few straightforward, proactive steps can make a massive difference. The idea is to build trust and eliminate any chance of confusion, from the moment a customer lands on your site to the day they check their bank statement.

Make Your Billing Descriptor Crystal Clear

I've seen it a thousand times: a customer scans their statement, sees a charge from a name they don't recognize, and immediately assumes it's fraud. It’s one of the most common—and easily avoidable—reasons for a chargeback.

Your billing descriptor is the name that shows up on their statement, and it needs to be instantly recognizable. If your store is "Patty's Pet Palace" but your legal business name is "PJP Enterprises LLC," you’re asking for trouble. Use your store name, a clear abbreviation, or even your website URL.

A clear, easy-to-identify billing descriptor is your first line of defense against "Transaction Not Recognized" disputes. It stops confusion dead in its tracks.

Provide Outstanding and Accessible Customer Service

When a customer has a problem, who do you want them to call first? You, or their bank?

Your goal is to always be the first choice. Excellent, easy-to-reach customer service is one of the most powerful chargeback prevention tools you have. Don't hide your contact info. Put your phone number, email address, and a contact form link right in your website's header and footer. If a customer knows they can get a quick, helpful response from you, they have zero reason to escalate things to their bank.

Be Upfront with Your Policies

Hidden fees, murky return rules, and vague shipping timelines are basically invitations for disputes. Customers who feel like they've been misled are far more likely to file a chargeback. Transparency is your best friend here.

- Shipping Policy: Clearly state your processing times and estimated delivery windows. And provide tracking numbers for every single order. No exceptions.

- Return and Refund Policy: Your policy should be easy to find and even easier to understand. Use plain English to explain deadlines, conditions, and how to start a return.

- Product Descriptions: Be honest and hyper-detailed. Use high-quality photos from every angle and write descriptions that leave no room for doubt.

Being upfront builds trust and manages expectations from the get-go. This is how you avoid those frustrating "Product Not as Described" or "Services Not Rendered" claims. For a deeper look into this topic, explore our comprehensive guide on https://www.chargepay.ai/blog/how-to-prevent-chargeback.

Use Essential Security Tools

While many chargebacks come from customer confusion or frustration, genuine fraud is still a real threat. A couple of basic security checks are simply non-negotiable for any business that takes payments online.

These tools are standard practice and your payment processor expects you to use them:

- Address Verification System (AVS): This tool checks if the billing address entered by the customer matches the one their card issuer has on file.

- Card Verification Value (CVV): This requires the customer to enter that little three or four-digit security code on their card, proving they physically have it.

These simple checks are powerful roadblocks for fraudsters using stolen card numbers. The cost of a chargeback isn't trivial; travel and hospitality see the highest average value at $120. While the United States has the highest average chargeback value at $110, its rate is a moderate 0.47%, which is actually below the industry average of around 0.65%. These numbers show exactly why having strong preventative measures in place is so critical, no matter what you sell.

Common Questions About Debit Card Chargebacks

Even with a solid game plan, a chargeback from a debit card can throw some curveballs. Let's clear the air and tackle the questions that trip up merchants most often. Getting these answers straight can save you from making costly mistakes down the road.

How Long Do I Have to Respond to a Chargeback?

The clock starts ticking immediately, and it’s not on your side. You typically have between 7 to 21 days from the moment you’re notified to get your evidence in.

This isn't a friendly suggestion—it's a hard cutoff set by the card networks (think Visa or Mastercard) and enforced by your payment processor.

Miss this window, and you’ve automatically lost. It doesn’t matter if your evidence is airtight. A late submission is an instant forfeit. Always check the specific deadline listed in the chargeback notification from Stripe, Shopify, or PayPal and treat it as non-negotiable.

Is It Worth Fighting a Small Chargeback?

Yes. A thousand times, yes. It might feel like a poor use of your time to fight over a $15 or $20 sale, but trust me, fighting every single chargeback is absolutely critical for the long-term health of your business.

There are two massive reasons for this.

First, every single chargeback you get—win or lose—hits your chargeback ratio. If that number creeps over the industry threshold (usually around 0.9%), processors will start seeing you as "high-risk." That can lead to much higher fees, processors holding your funds, or even shutting down your merchant account entirely.

Second, fighting every claim, especially the ones that smell like friendly fraud, sends a clear message. It tells potential fraudsters you aren't an easy target, which can discourage them from trying the same thing again.

What Is the Difference Between a Chargeback and a Refund?

This is a core concept every merchant has to grasp. They both end with the customer getting their money back, but the journey to get there is night and day.

- A Refund: This is a peaceful resolution between you and your customer. They reach out with a problem, and you voluntarily return their money. The issue is handled directly, with no banks getting involved.

- A Chargeback: This is a forced reversal kicked off by the customer's bank. The customer goes over your head, straight to their financial institution, to dispute the charge.

A chargeback is always worse than a refund. It comes with non-refundable fees (even if you win!) and damages your standing with payment processors. Your goal should always be to get customers to contact you first so you can resolve things directly.

Can a Customer File a Chargeback After My Return Period?

Unfortunately, yes. This is a frustrating reality of eCommerce. Your store's return policy and the bank's chargeback rules are two completely different things, operating on separate timelines.

A customer’s right to dispute a charge is governed by card network rules, which can give them 120 days or more from the transaction date. While you should absolutely include your return policy in your evidence to show the customer ignored your terms, it’s not a silver bullet. The bank has the final say and will make its decision based on the complete picture.

Fighting chargebacks manually is a soul-crushing drain on your time and resources. ChargePay uses AI to handle the entire dispute process for you, from generating evidence-packed responses to submitting them on your behalf. Stop losing revenue and start protecting your business—without lifting a finger. Learn more about how ChargePay can boost your win rate.

.svg)

.svg)

.svg)

.svg)