Look, the best way to handle a chargeback is to stop it from ever happening. Winning disputes after the fact is a painful, uphill battle. A truly solid strategy is proactive, built on three core pillars: crystal-clear communication, smart fraud detection, and top-notch customer service. It’s all about setting the right expectations and catching trouble before it starts.

The True Cost of a Chargeback

It’s easy to look at a chargeback and just see the lost sale. You refund the transaction, and that's the end of it, right? If only it were that simple. The reality is that the financial hit goes way deeper, creating ripple effects that can harm your business from every angle.

And this isn't a small problem—it's a massive, growing one. Global chargeback volume is on track to jump by 24% between 2025 and 2028, rocketing to a mind-boggling 324 million transactions annually. In 2023, these disputes drained about $117 billion from businesses worldwide. Mastercard’s research really lays out the scale of this challenge.

It’s So Much More Than Just a Lost Sale

For every single chargeback, your payment processor slaps you with a non-refundable fee. You have to pay this penalty whether you win or lose the dispute. That's just the start. The hidden costs pile up fast, and they hurt.

A chargeback isn't just a financial transaction reversed; it's a direct hit to your profit margin, operational efficiency, and your standing with payment networks. Viewing it as a simple refund is a critical mistake.

Think about the operational drain. Your team has to stop what they're doing to dig up evidence, craft rebuttal letters, and track the dispute's progress. That’s precious time they could have spent on marketing, product development, or customer support—activities that actually grow your business. Instead, they're stuck in damage control mode.

The Real Danger: Your Merchant Account

Beyond the immediate cash crunch, every chargeback nudges your chargeback-to-transaction ratio higher. If that ratio creeps above the 1% threshold, card networks like Visa and Mastercard will flag your business as "high-risk."

That’s when the real trouble begins:

- Higher Processing Fees: Banks suddenly see you as a liability and start charging you more for every single transaction you process.

- Frozen Funds: Your payment processor might decide to hold a chunk of your revenue in a reserve account just in case more chargebacks come through.

- Account Termination: In a worst-case scenario, you could lose your merchant account entirely, leaving you unable to accept credit card payments at all.

Getting a handle on these costs is step one. To really understand the penalties involved, you need to learn more about what a chargeback fee is and why it's such a big deal. A proactive prevention strategy isn't just about saving money on a few lost sales; it's about protecting the long-term health and viability of your entire business.

Build Your Defense with Clear Policies

A surprising number of chargebacks don't start with fraud or malice—they start with a simple misunderstanding. Your first and most powerful line of defense is creating business policies that are so clear they leave no room for confusion. This is where you set expectations from the very first click.

Think of your policies—return, refund, and shipping—as a vital part of the customer experience. They shouldn't be buried in the footer, written in dense legal jargon that no one understands. Make them easy to find, simple to read, and display them at key moments, like on your product pages and during checkout. When customers know exactly what to expect, they’re far less likely to panic and file a chargeback if something goes sideways.

Make Your Policies Visible and Easy to Understand

Vague language is your worst enemy here. Forget phrases like "returns accepted within a reasonable time." What does that even mean? You need to be specific and direct.

- Define your return window clearly: State the exact number of days a customer has to start a return, like "30 days from the date of delivery."

- Explain the required condition: Do items need to be unused, in the original packaging, or have tags still attached? Spell it out.

- Outline the refund process: Let them know how and when they'll get their money back. Is it store credit or a refund to their original payment method? How long does it usually take?

Crafting a solid policy is non-negotiable. If you're on Shopify, our guide to creating a rock-solid Shopify refund policy offers a detailed walkthrough to get it just right. The goal is to answer your customer's questions before they even have a chance to ask.

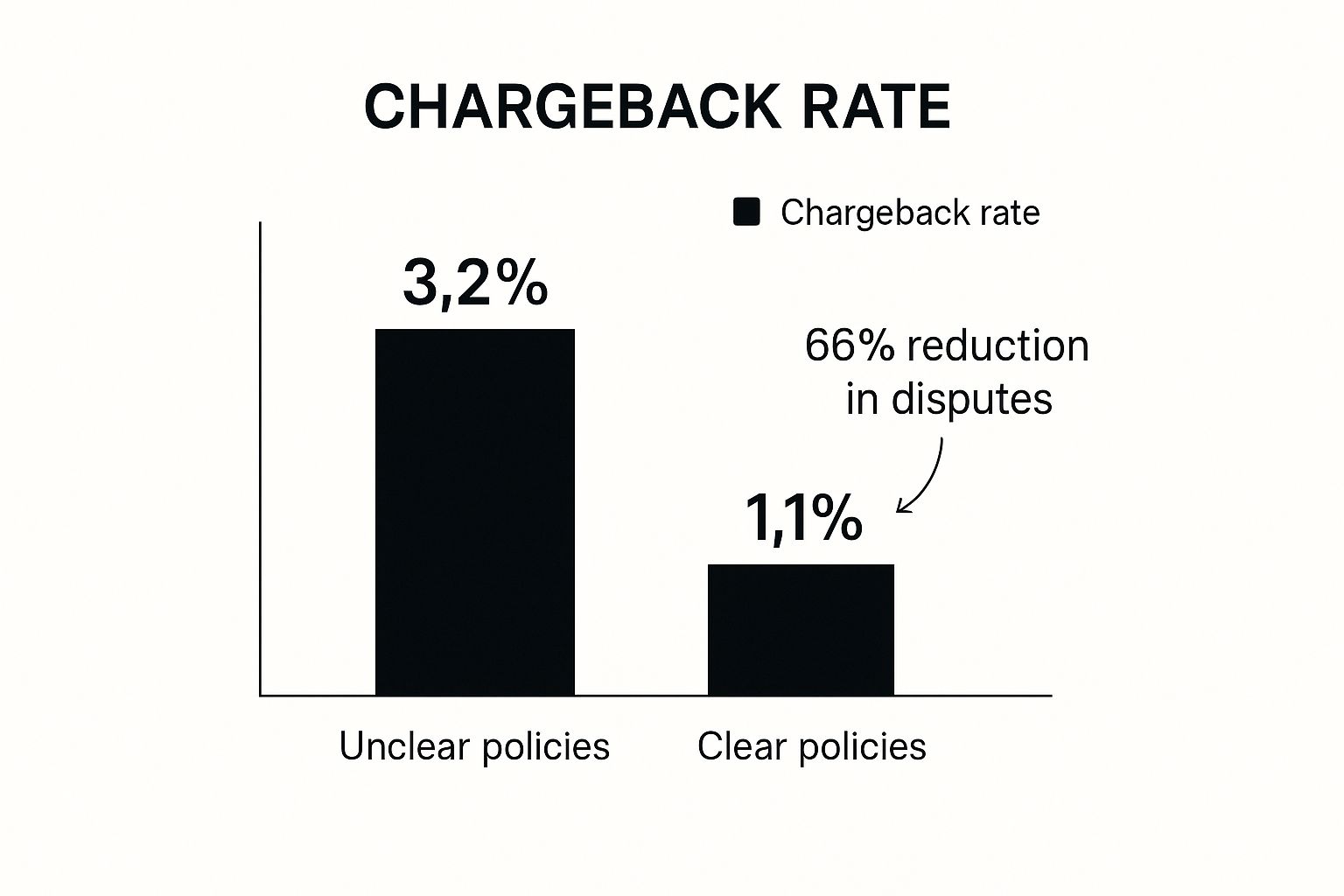

The difference this kind of clarity makes is staggering.

As the data shows, just moving from unclear to clear policies can slash your chargeback rate by more than 66%. That's a massive win that directly protects your bottom line.

Don't Overlook Your Billing Descriptor

Your work isn't done once the policies are written. One of the most common, and frankly, most frustrating causes of "friendly fraud" is a billing descriptor that a customer doesn't recognize. This is that short line of text that pops up on their credit card statement.

If a customer sees "XYZ Corp" on their statement when they bought from "Brenda's Beautiful Baskets," their first reaction is often to assume fraud and call their bank.

Make sure your billing descriptor is instantly recognizable. It needs to clearly state your store's name—the one your customers actually know you by. A simple tweak here can prevent countless unnecessary chargebacks and save you a world of headaches. When it comes to chargebacks, proactive communication is always your best bet.

Spot Fraud Without Blocking Good Customers

Here's the tricky part of running an online store: you have to stop criminals from walking out the door with your products, but you can't treat every shopper like a suspect. Go too hard on security, and you'll frustrate legitimate customers until they just give up and buy elsewhere. It's a real tightrope walk.

The secret is building a smart, layered security net. It’s about catching the obvious red flags without creating a checkout experience full of hoops for everyone else to jump through.

Your first line of defense starts with the absolute basics. These are non-negotiable for any e-commerce business and will weed out a surprising amount of low-level fraud.

- Address Verification System (AVS): This is a simple check. Does the billing address the customer typed in match the one their bank has on file? A mismatch is a classic sign of a stolen card.

- Card Verification Value (CVV): That little three or four-digit code on the back of the card is a game-changer. Requiring it proves the customer has the physical card, making life much harder for fraudsters who only managed to snag the card number.

While these checks are essential, they won't stop a determined fraudster. That’s why you need to dig a little deeper.

Looking For Suspicious Patterns

Think of yourself as a detective. Fraudsters often leave a trail of clues, and with the right tools, you can spot behavior that just doesn't add up.

For instance, a brand-new customer suddenly placing several high-ticket orders and demanding overnight shipping should set off alarm bells. This is where order velocity analysis is so powerful. It keeps an eye on how many orders a single customer (or IP address) places in a short time. A sudden, frantic spike is a huge red flag.

Another dead giveaway is location. IP geolocation tools instantly tell you where in the world an order is coming from. If the IP address is in Ukraine, the billing address is in Ohio, and the shipping address is in Florida... you've almost certainly got a problem. That's an order that needs a manual review, stat.

The goal isn't to block every order with a single red flag. It's about using a combination of signals to build a risk score. A small mismatch might be an honest mistake, but multiple inconsistencies strongly suggest fraud.

To help you choose the right tools, here’s a quick rundown of some common fraud detection methods.

Essential Fraud Detection Tools at a Glance

Each of these tools provides a different piece of the puzzle, giving you a more complete picture of the transaction's risk level.

Adopting Advanced Fraud Prevention

Beyond those methods, device fingerprinting is an incredibly powerful technique. It creates a unique digital ID for the computer, phone, or tablet placing an order. If you see ten different "customers" with ten different credit cards all placing orders from the exact same device, you've caught a fraud ring in the act.

Want to go even deeper? Our guide on fraud prevention for ecommerce breaks down more advanced strategies to protect your store.

The need for these systems is only growing. The travel industry recently saw a staggering 816% spike in chargebacks, and e-commerce wasn't far behind with a 222% jump. Protecting your payment process is critical, which means implementing robust security and compliance measures, including PCI DSS is just part of doing business today.

By layering these tools, you create a formidable defense that keeps fraudsters out while letting your real customers shop with confidence.

Turn Great Support into Fewer Disputes

So much of our focus is on getting the customer to click "buy." But what happens right after that click is just as critical for your bottom line. When a customer feels ignored or frustrated after a sale, their next call isn't always to you—it’s often straight to their bank.

This is where excellent, accessible customer support becomes one of your most powerful tools against chargebacks.

Think about it from their perspective. A package is delayed, an item shows up damaged, or they just have a simple question about their order. If they can’t easily find a way to contact you, that small bit of friction can quickly boil over into a full-blown dispute. The key is to make it incredibly simple for them to reach a real person who can actually help.

Make Your Support Easy to Find and Use

Your contact information shouldn't be a hidden treasure. You need to display your support options—email, a phone number, a live chat widget—everywhere. Put it on your website header and footer, in order confirmation emails, and even on your packing slips.

A customer who gets a quick, empathetic response from your team is a customer who feels heard. That simple act of communication can stop a potential chargeback dead in its tracks.

Multi-channel support is the name of the game here. Some people prefer the immediacy of live chat, while others want to hear a human voice over the phone. Offering multiple avenues ensures you meet customers where they are, making it a no-brainer for them to seek a solution directly with you first.

Turn Problems into Positive Experiences

Look, no business is perfect. Shipments get delayed. Products sometimes arrive with a dent. How you handle these moments is what separates a loyal, repeat customer from a frustrating chargeback statistic.

When a customer reaches out with an issue, your team's response needs to be built on two things: empathy and speed. Acknowledge their frustration first, then immediately pivot to solving the problem. Ditch the defensive tone and adopt a helpful one.

Here’s how a quick interaction for a damaged item should go:

- Customer: "My order just arrived, and the corner is smashed!"

- Support Rep: "Oh no, I'm so sorry to hear that. That's definitely not the experience we want for you. Can you send me a quick photo? I'll get a replacement sent out to you today—no need to even return the damaged one."

This approach does two crucial things: it validates the customer's feelings and provides an immediate, hassle-free solution. You’ve just turned a negative situation into a reason for them to trust your brand even more.

Mastering these interactions is a core part of running a successful online store. You can explore more best practices in customer service to really sharpen your team's approach. The goal is to solve the problem so effectively that filing a chargeback never even crosses their mind.

Using Tech to Deflect and Resolve Disputes

Even with perfect policies and stellar customer support, some disputes are simply going to happen. It's an unavoidable part of e-commerce. But that doesn’t mean you have to sit back and wait for a formal chargeback to hit your account.

Modern tech gives you a way to get ahead of the problem, turning a potential dispute into a simple resolution.

Think of it as an early warning system. Instead of being blindsided by a chargeback notification from your bank, you get a heads-up the moment a customer contacts their bank to question a charge. This opens a small but crucial window of opportunity for you to act first.

These systems are known as Chargeback Alerts. They're powered by major dispute resolution networks from companies like Verifi (owned by Visa) and Ethoca (owned by Mastercard). When you integrate with these services, they act as a bridge between you and the issuing banks.

How Chargeback Alerts Work

The process itself is straightforward but incredibly powerful. When a cardholder from a participating bank initiates a dispute, the network sends an immediate alert directly to you or your service provider.

This alert gives you a chance to review the transaction and issue a full refund on the spot. By refunding the customer before the bank formally processes the dispute, you prevent it from ever becoming an official chargeback.

You might lose the sale, but you avoid the chargeback fee, the negative mark on your merchant account, and the entire time-consuming representment process. It's a strategic retreat that protects your long-term health.

This approach has a proven track record. Between 2020 and 2021, the average chargeback ratio in the U.S. dropped by over 17%, largely because merchants started adopting prevention tools. In fact, Verifi was used in a staggering 97.11% of prevention cases, showing just how vital this technology has become.

Choosing the Right Integration Partner

Integrating directly with networks like Verifi and Ethoca can be complex, which is why most merchants choose to work with certified partners like ChargePay. A good partner simplifies the entire process, connecting you to these powerful networks and managing the alerts for you.

When you're looking for a provider, there are a few key things to look for:

- Broad Bank Coverage: Make sure the service connects to both Verifi and Ethoca. This gives you the widest possible coverage of issuing banks and catches more potential disputes.

- Automation Rules: The best systems let you set up rules to automatically refund certain alerts, like those for low-value orders. This saves you a ton of manual work.

- Clear Reporting: You need detailed analytics to see exactly how many chargebacks were prevented and, most importantly, how much money you’ve saved in fees.

By automating this process, you create a safety net that catches disputes before they can do any real damage. To get a deeper understanding of how this all works, check out our complete guide to automated chargeback and dispute management using AI.

Beyond alert systems, it's also worth exploring other tech solutions. For instance, understanding how chatbots can help improve customer retention can add another layer to your prevention strategy by resolving customer issues before they even think about a chargeback.

Got Questions About Chargeback Prevention? We've Got Answers.

Even when you feel like you've got a handle on your chargeback strategy, a few nagging questions can pop up and create uncertainty. It's totally normal. Getting the little details right is what separates a good prevention plan from a great one.

Let's clear the air and tackle some of the most common questions we hear from merchants. Think of this as your quick-reference guide for those tricky "what if" scenarios.

What's Really the Difference Between a Chargeback and a Refund?

This is easily the most important distinction to grasp. A refund is a conversation between you and your customer. They ask for their money back, you agree, and you process it. It's a customer service moment that you control from start to finish.

A chargeback, however, is a completely different beast. It’s a forced payment reversal kicked off by the customer’s bank, completely cutting you out of the loop. A third party—the bank—steps in, and you’re hit with non-refundable penalty fees no matter the outcome.

The core difference comes down to control. With a refund, you're in the driver's seat. With a chargeback, you've been shoved into the passenger seat while your business takes a financial hit.

Can You Actually Prevent Friendly Fraud?

Ah, friendly fraud. That's the industry term for when a customer disputes a charge they actually made, and it's one of the most maddening parts of running an e-commerce business. While you can't read a customer's mind and stop every single instance, you can absolutely make your business a much harder target.

The best defense is a layered one. You need to build a rock-solid paper trail.

- Use Crystal-Clear Billing Descriptors: Does the name on their credit card statement scream your store's name? It needs to be instantly recognizable. No cryptic LLC names.

- Send Detailed Confirmations: Your order and shipping confirmation emails aren't just for the customer; they're your receipts. They prove a legitimate purchase happened.

- Require Delivery Signatures: For anything high-value, a signature is your golden ticket. It's undeniable proof that the package made it into the right hands.

- Get Ahead with Dispute Alerts: Services from Ethoca and Verifi can be game-changers. They give you a heads-up when a customer is unhappy, letting you issue a refund before things escalate into a damaging chargeback.

Each of these steps helps discourage dishonest claims and gives you the ammo you need to fight back when someone tries to pull a fast one.

How Many Chargebacks Is Too Many?

There's a very clear line in the sand drawn by the major card networks. Generally, if your chargeback ratio climbs above 1%, you're in the danger zone. This isn't just a friendly suggestion; it's a critical threshold that processors like Visa and Mastercard monitor closely.

The math is simple: it's the number of chargebacks you get in a month divided by your total transactions for that same month. Creeping over that 1% mark consistently can lead to some serious headaches, like higher processing fees, held funds, or even having your merchant account shut down for good.

What Evidence Do I Need to Fight a Chargeback?

When you decide to dispute a chargeback, the quality of your evidence is everything. You're not just telling your side of the story; you have to prove it with undeniable facts.

Your representment package needs to be airtight. Here’s what you should always include:

- Proof of Delivery: A tracking number showing the item was delivered to the customer’s address is non-negotiable. Signature confirmation? Even better.

- Customer Communications: Pull up every email, live chat log, or support ticket. Show that you were responsive and professional.

- Transaction Details: Include the AVS (Address Verification System) and CVV match results from the initial transaction. This helps prove the legitimate cardholder made the purchase.

- Policy Agreement: A screenshot showing the customer had to check a box to agree to your return policy before checkout is incredibly powerful evidence.

The more detailed and organized your documentation is, the better your chances are of winning the dispute and recovering your money.

Ready to stop reacting to chargebacks and start preventing them automatically? ChargePay uses AI to manage disputes, recover lost revenue, and protect your business without the manual work. See how much you can save with ChargePay.

.svg)

.svg)

.svg)

.svg)