Let's cut through the jargon. A debit card chargeback is essentially a forced refund, but with a serious twist. When a customer disputes a transaction, their bank doesn't put a hold on a credit line—it pulls the money directly from your business's cash account.

Think of it as an electronic clawback. The money was settled, in your bank, and then suddenly it’s gone. This immediate hit to your cash flow is what makes debit card chargebacks particularly painful for merchants.

What Are Debit Card Chargebacks Anyway?

You’ve probably heard the term "chargeback" thrown around, most likely in relation to credit cards. But when it comes to chargebacks on debit cards, the game changes. While the end result—a reversed payment—is the same, the impact on your business's finances is much more direct.

This whole process kicks off when a customer contacts their bank about a problem with a purchase they made from you. The bank then steps in to investigate and, in the meantime, reverses the charge, yanking those funds right out of your merchant account.

The People Involved in a Chargeback

To really get a handle on the process, you need to know who the key players are. A chargeback isn't just a squabble between you and the customer; it’s a formal process involving a cast of financial institutions, each with a specific part to play. Knowing who does what makes the whole system a lot less intimidating.

For instance, the customer's bank (known as the issuer) is the one that gets the ball rolling. But it’s your bank (the acquirer) that has to pull the funds from your account and help you fight back if you decide to dispute the chargeback.

A common misconception is that chargebacks are just a fancy word for a refund. In reality, they are a formal dispute mechanism that comes with extra fees and can damage your relationship with payment processors if they happen too often.

The Key Players in a Debit Card Chargeback

Here’s a quick look at who's involved when a debit card chargeback happens and what they do. Getting familiar with these roles is the first step toward successfully managing any disputes that come your way.

Understanding this lineup is crucial because you'll be interacting with several of these players—directly or indirectly—anytime a chargeback lands on your plate.

How Debit and Credit Card Chargebacks Really Differ

It’s easy to think a chargeback is just a chargeback, no matter what kind of plastic your customer uses. But treating debit and credit card disputes the same is a huge mistake—one that can put your business's cash flow at serious risk. While the two processes might look similar on the surface, they operate under completely different rules and have vastly different impacts on your accounts.

The biggest difference boils down to one simple question: where is the money coming from? When a customer disputes a credit card purchase, their bank is essentially putting a hold on a line of credit. The immediate financial hit isn't to you or the customer; it's a temporary adjustment on a loan.

With chargebacks on debit cards, however, the funds are yanked directly from your business's bank account. This isn't a credit hold. It's a real-time withdrawal of your hard-earned cash. The money you thought was settled and secure is suddenly gone, creating an immediate hole in your operating budget.

The Rules of the Game Are Different

Another key difference is the legal framework that governs these disputes. Understanding these rules helps explain why the processes and timelines feel so different for merchants.

- Credit Cards: These are protected under the Fair Credit Billing Act (FCBA). This law gives customers broad protections, including a liability limit of just $50 for unauthorized charges and a pretty generous window to file a dispute.

- Debit Cards: These fall under Regulation E, also known as the Electronic Fund Transfer Act. While it also offers protection, the rules are much stricter. A customer's liability depends entirely on how quickly they report a lost or stolen card.

This distinction is crucial. The FCBA is designed to protect consumers using a line of credit, while Regulation E is built to protect actual cash in a bank account. For you as a merchant, this means the urgency and risk tied to debit card chargebacks are significantly higher.

Key Takeaway: The money for a debit chargeback comes from your cash account, not a credit line. The impact on your business's cash flow is instant and direct, making these disputes particularly dangerous to your financial health.

Why This Difference Puts Your Business at Risk

Because debit card disputes involve real cash transfers, the whole process moves with a lot more urgency. Banks are on the hook with strict deadlines to resolve these issues, which puts immense pressure on you to respond.

For example, say a customer disputes a charge for a subscription they forgot about. If they used a debit card, their bank will likely issue a provisional credit to their account almost immediately—while simultaneously pulling the funds from yours. You’re then left scrambling to prove the charge was legitimate, often within a very tight timeframe.

This rapid movement of funds creates financial blind spots. If you aren't tracking debit chargebacks separately from credit card disputes, you might not realize just how much actual cash is being siphoned from your account until it’s too late. The rising costs only make it worse. The average chargeback amount for debit card transactions has climbed to about $169.13, and dispute rates have surged by 78% year-over-year in some periods.

In certain sectors like online travel, that increase has been as high as 816%, showing just how volatile this issue can be. You can explore more about these chargeback statistics to see the full picture.

Ultimately, a one-size-fits-all approach to chargebacks just doesn't cut it. To protect your bottom line, you need a smart response strategy that recognizes the unique and immediate threat that chargebacks on debit cards pose to your business.

The Debit Card Chargeback Process Step by Step

When a chargeback notice lands in your inbox, it can feel like a sudden, confusing storm. But getting a grip on the process is the first step toward navigating it successfully. It's best to think of the debit card chargeback journey as a series of predictable stages, each with its own set of rules and deadlines.

It all kicks off when a customer decides to dispute a transaction. They don't call you; they call their bank. That single action starts a formal chain reaction that pulls you, your bank, and the card networks into the mix. From that moment on, the clock is ticking.

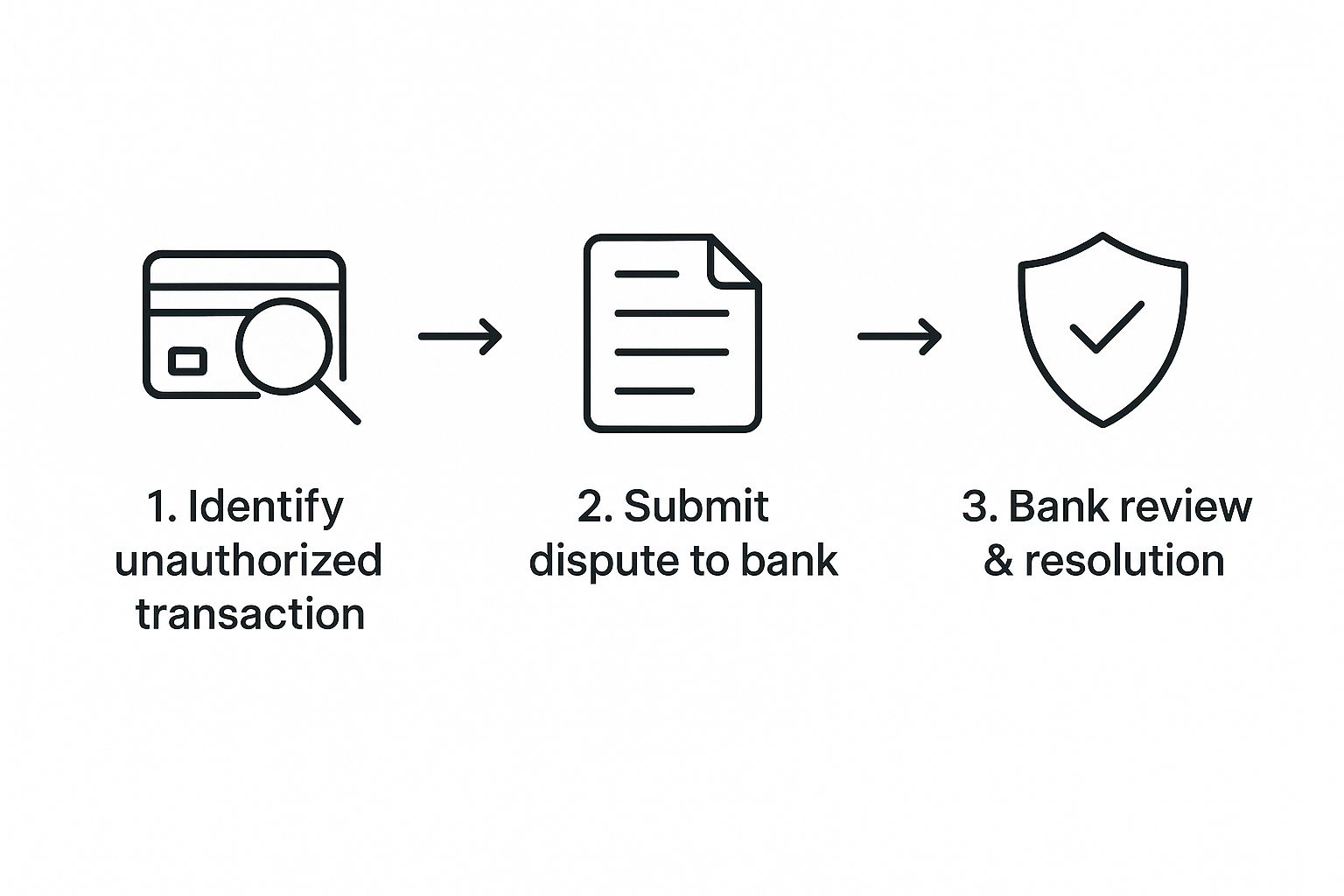

The following infographic shows the first moves a customer makes to start the chargeback process.

As you can see, the process begins when the customer spots a problem, formally files a dispute with their bank, and then waits for the bank's review. Let's break down exactly what happens next from your perspective as the merchant.

Step 1: The Customer Initiates the Dispute

The whole thing starts when your customer contacts their bank—the issuing bank—to report a problem with a debit card transaction. This could be for any number of reasons, from a charge they don't recognize to a product that never showed up.

Once the customer files the dispute, the bank reviews the claim to see if it qualifies for a chargeback. For chargebacks on debit cards, the bank often moves quickly due to consumer protection laws like Regulation E.

Step 2: The Provisional Credit and Debit

This is where you first feel the financial sting. Almost immediately after the customer files a dispute, their bank will often issue a provisional credit. This means the customer gets their money back temporarily while the bank investigates.

To fund this credit, the bank pulls the money directly from your merchant account. This is a crucial detail for debit card chargebacks—the cash is gone from your account before you even get a chance to tell your side of the story.

A provisional credit isn’t the final word. It’s just a temporary hold on the funds while the investigation plays out. If you win the dispute, this transaction gets reversed, but that initial hit to your cash flow is unavoidable.

Step 3: You Receive a Formal Notification

Next, your acquiring bank (your business bank) or payment processor will send you a formal notification about the chargeback. This document is packed with vital information, including:

- The transaction details (amount, date)

- The customer's specific claim

- A reason code explaining why the chargeback was filed

That reason code is your starting point. It tells you if the customer is claiming fraud, a processing mistake, or an issue with the product or service itself. You can get a much deeper look into the entire journey by checking out our detailed guide on what to do when you get a chargeback on a debit card.

Step 4: The Critical Response Window Opens

The chargeback notification officially starts a countdown. You now have a very limited time—usually between 10 and 30 days—to respond. This is your one and only shot to fight the chargeback and get your money back.

If you miss this deadline, you automatically lose the dispute. The provisional credit given to the customer becomes permanent, and there are no do-overs.

To fight back, you need to submit a rebuttal through a process called representment. This means gathering compelling evidence that proves the original transaction was legitimate and sending it back to your acquiring bank.

Step 5: The Bank Makes a Final Decision

Once you submit your evidence, your acquiring bank reviews it and passes it along to the customer's issuing bank. The issuing bank then makes the final call.

- If you win: The chargeback is reversed. The funds that were taken from your account are returned.

- If you lose: The chargeback stands. The customer keeps the money, and you're out both the revenue and the product.

This whole process, from the initial dispute to the final verdict, can take several weeks or even a few months. Understanding each step is key to preparing a timely, evidence-backed response, which gives you the best possible chance to protect your revenue.

Why Customers File Debit Card Chargebacks

To get a handle on debit card chargebacks, you first have to understand why they happen. These disputes don't just materialize out of thin air. They're usually a symptom of a much deeper problem, anything from clear-cut criminal fraud to a simple, honest-to-goodness mix-up.

When you start to peel back the layers, you’ll see that chargebacks aren't one single issue. They're a collection of separate problems, and each one needs its own game plan. Getting to the root of these causes is the first real step toward building a defense that actually protects your revenue.

True Fraud: The Most Obvious Culprit

This is the one everyone thinks of first: criminal fraud. It’s the classic scenario where a thief gets their hands on a customer's debit card information and goes on a shopping spree. The actual cardholder eventually spots the unfamiliar charges on their statement and, quite rightly, disputes them.

This kind of fraud is pretty black and white. Your customer is the victim, and you, the merchant, are unfortunately stuck in the middle.

- Stolen Physical Cards: A lost or stolen wallet leads to a string of fraudulent purchases before the card can be canceled.

- Phishing and Skimming: Crooks use tricky emails or hidden devices on ATMs and payment terminals to swipe card details.

- Data Breaches: A security failure at another company can leak thousands of debit card numbers, which then get used for illegal online purchases.

When these transactions hit, a chargeback is the right and necessary tool for the customer to get their stolen money back. For your business, the goal isn't really to fight this type of chargeback but to beef up your fraud detection to stop these transactions from ever getting approved.

Merchant Error: An Unfortunate but Fixable Cause

Sometimes, the problem starts right in your own backyard. Mistakes in your systems or daily processes can directly lead to chargebacks. These are often the easiest to prevent because the solution is entirely in your hands. A customer might file a dispute simply because they see no other way to fix a mistake you made.

Common merchant errors include:

- Processing Glitches: A system hiccup accidentally charges a customer twice for the same product.

- Unclear Billing Descriptors: The charge on their bank statement is a cryptic jumble like "TRXN-ECOMM45*CA" instead of your store's name. Not recognizing it, the customer assumes it's fraud.

- Shipping and Fulfillment Issues: The wrong item gets sent, a product shows up damaged, or it never arrives at all. If your customer service is slow to help, a chargeback becomes the path of least resistance.

Fixing these issues boils down to better operational habits and clearer communication. Something as simple as a clean billing descriptor or a responsive support team can head these disputes off at the pass.

The Rise of Friendly Fraud

This is easily the most maddening and difficult category to deal with. Friendly fraud is when a real customer disputes a purchase they genuinely made. It isn't born from the same malicious intent as criminal fraud, but it costs merchants billions. In fact, some studies show friendly fraud accounts for nearly 80% of all chargebacks.

Friendly fraud, sometimes called "I didn't do it" fraud, isn't always a deliberate lie. It can come from simple forgetfulness or confusion, but the financial hit to your business feels just as real as any criminal attack.

Here are a few classic friendly fraud scenarios:

- Forgotten Purchases: Someone signs up for a free trial that rolls into a paid subscription. A few months later, they see the charge, don't remember agreeing to it, and file a chargeback.

- Family Member Purchases: A teenager uses their parent's debit card for in-game currency. The parent sees the charge, doesn't recognize it, and immediately disputes it.

- Buyer’s Remorse: A customer makes an impulse buy, regrets it the next day, and files a chargeback to get their money back instead of going through your return process.

Because the legitimate cardholder is making the purchase, your standard fraud filters won't catch this. The best defense is crystal-clear communication, simple cancellation processes for subscriptions, and keeping meticulous transaction records.

To dig deeper into how you can spot and fight these claims, check out our complete guide to chargeback fraud.

Common Reasons for Debit Card Chargebacks

To help you connect the dots, let's break down the most frequent reasons for chargebacks, what they look like in the real world, and what they're telling you about your business.

By understanding these distinct reasons, you can shift from just reacting to chargebacks to proactively fixing the core issues driving them. This is how you stop revenue leaks for good.

How to Effectively Fight Debit Card Chargebacks

Getting hit with a chargeback notice can feel like a punch to the gut, but it doesn't have to be a knockout blow. That notification isn't a final verdict; it's really just an invitation to tell your side of the story. This process of fighting back is formally known as representment, and it's your single best opportunity to reclaim that lost revenue.

Think of it like you're building a case file for a small claims court. The bank is the judge, and your job is to present clear, undeniable evidence that proves the original transaction was totally legitimate. A strong case isn't about arguing your point—it's about documenting everything.

Start with the Reason Code

Your very first move is to look at the reason code that came with the chargeback notification. This little two-to-four-digit code is the bank's shorthand for why the customer disputed the charge in the first place. It's your roadmap, telling you exactly what kind of evidence you need to start gathering.

A code for "Fraudulent Transaction," for instance, demands a completely different set of proof than one for "Product Not Received." Don't just start grabbing random files and receipts. Let that reason code guide your evidence collection from the very start.

Gather Your Compelling Evidence

Once you know why the chargeback was filed, you can get to work building your defense. The key here is compelling evidence. You need rock-solid documents that directly contradict the customer's claim, leaving zero room for doubt.

Here’s a look at what you’ll need for a couple of common dispute types:

For a "Product Not Delivered" Claim:

- Shipping Confirmation: Get the dated receipt from your shipping carrier, like UPS, FedEx, or USPS.

- Tracking Number: This needs to show the full journey of the package, from your warehouse all the way to the customer's address.

- Proof of Delivery: This is the most crucial piece of the puzzle. It's the final confirmation showing the package was successfully delivered, including the date, time, and sometimes even a photo of it sitting on the customer's doorstep.

- Matching Addresses: Show that the shipping address on the original order perfectly matches the delivery address in the tracking information.

For a "Product Not as Described" Claim:

- Product Descriptions and Photos: Pull up the exact product page the customer ordered from. High-quality images and detailed, accurate descriptions prove what you advertised.

- Order Confirmation: Include the email or receipt that shows exactly what the customer ordered, down to the size, color, and model number.

- Customer Communications: Any emails, chat logs, or call transcripts where the customer discussed the product can be incredibly powerful, especially if they seemed happy with it at first.

Winning a chargeback is less about writing a persuasive essay and more about presenting an airtight case file. The more factual, verifiable evidence you provide, the higher your odds of getting the funds reversed.

Write a Clear and Concise Rebuttal Letter

All that evidence needs a cover letter, and this is your rebuttal. This is no place for a long, emotional story. You need to keep it professional, stick to the facts, and get straight to the point.

Your rebuttal letter should be a simple, logical summary of your evidence. Structure it like this:

- Start with the basics: State the transaction date, the exact amount, and the customer's name.

- Address the claim directly: Clearly state the reason code and explain why the customer's claim is incorrect. For example, "The customer filed this chargeback under Reason Code 13.1, claiming the product was not delivered. However, our evidence proves otherwise."

- Summarize your proof: Briefly list the evidence you've attached. "As you'll see in the attached documents, we have provided a shipping confirmation from FedEx (Exhibit A), a tracking number showing delivery on [Date] (Exhibit B), and a delivery photo at the customer's address (Exhibit C)."

- End with a clear request: Politely ask for the chargeback to be reversed based on the mountain of evidence you've just provided.

For merchants looking to really master this part of the process, digging into the details of chargeback representment can offer deeper insights and proven strategies.

Submit Before the Deadline

This might be the most critical rule of all. Debit card chargeback timelines are notoriously short, often giving you just 10 to 20 days to get your response in. If you miss that window, you lose automatically—no matter how strong your evidence is.

Always, always prioritize chargeback responses. Set up alerts, use a calendar, or find automation tools to make sure you never miss a deadline. Responding promptly doesn't just keep you in the game; it shows the bank you're on top of your business and serious about defending the transaction.

Proven Strategies to Stop Chargebacks Before They Happen

While knowing how to fight chargebacks is an essential skill for any merchant, the real win is preventing them from ever happening. Being proactive is always going to be less of a headache—and less expensive—than dealing with disputes after the fact. A few smart tweaks to your customer service and security can make a massive difference.

It all boils down to one simple idea: make it easier for a customer to contact you than to contact their bank. When someone has a problem, their first thought should be to reach out to your support team, not to file a dispute. Getting this right can dramatically lower your chargeback numbers.

Make Your Customer Service Impossible to Miss

The second a customer has to hunt for your contact info, you're pushing them one step closer to a chargeback. Your support channels can't be an afterthought buried in the footer of some forgotten page. They need to be front and center.

- Be Accessible: Plaster your phone number, email address, and a live chat link in your website's header and footer. Make it obvious.

- Be Responsive: Aim to answer every inquiry quickly and professionally. A customer who gets a fast, helpful reply feels heard and is far less likely to escalate the issue to their bank.

- Be Clear: Write your return and refund policies in plain English. Complicated rules or surprise fees just breed frustration and send customers straight to the chargeback process.

Think of your customer service team as your first line of defense. A small investment here can save you thousands in lost sales and painful chargeback fees down the road.

The goal is to make getting a refund from you the path of least resistance. When it's easier to resolve an issue directly with your business than to file a chargeback, you stay in control.

Sharpen Your Security and Communication

Great service is a huge piece of the puzzle, but your technical and communication practices are just as important for stopping disputes—especially those tied to fraud or simple confusion.

One of the most common triggers for "friendly fraud" is a billing descriptor that a customer doesn't recognize on their bank statement. If they see a charge from "SP *WEBSERVICES_483" instead of "Your Awesome Store," they’re going to assume it’s fraud and dispute it.

Talk to your payment processor about setting a clear, static billing descriptor that actually includes your business name. It’s a tiny change that can wipe out a massive source of confusion. On top of that, you need to use basic security tools to screen every transaction.

Essential Security Checks:

- Address Verification Service (AVS): This tool simply checks if the billing address the customer entered matches the one their bank has on file.

- Card Verification Value (CVV): Requiring that three or four-digit code from the back of the card is a great way to prove the customer physically possesses the card, filtering out a good chunk of fraud.

A layered strategy that combines top-notch service, crystal-clear communication, and solid security is your best shield against chargebacks on debit cards. You can find a whole lot more proven tactics in our complete guide on chargeback prevention strategies.

And the need for these strategies is only getting more critical. Projections show that global chargeback volume is set to rocket to 324 million transactions by 2028—that's a 24% jump from 2025 alone. This surge, driven by the explosion of e-commerce, is expected to push the total value of disputes from $33.8 billion to $41.7 billion. You can learn more about these chargeback statistics and trends and see why getting ahead of disputes is more important than ever.

Answering Your Top Debit Card Chargeback Questions

When it comes to debit card chargebacks, a few key questions always seem to pop up. Let's tackle them head-on, so you can feel more confident and prepared when a dispute lands on your desk.

How Long Do I Have to Fight a Debit Card Chargeback?

You’re on the clock! Typically, you have between 30 and 45 days to respond to a debit card chargeback. This isn't set in stone, as the exact window can vary by bank and card network.

The most important thing is to act fast. If you miss that deadline, you automatically lose the dispute. The funds are gone for good.

Can a Customer File a Chargeback Months Later?

Yes, they absolutely can. Most card networks give customers a generous window—up to 120 days from the transaction date—to file a dispute.

In some cases, this timeline can be even longer. Think about services that haven't been rendered yet or products with a future delivery date. For these, the clock might not start ticking until that expected date passes.

Winning a Chargeback Reverses the Transaction

When you successfully fight a chargeback, it's called a reversal. This is just a formal way of saying the funds that were taken from your account are put back. A win almost always comes down to one thing: providing clear, compelling evidence that proves the customer's claim is invalid.

Does Winning a Dispute Remove It From My Record?

Unfortunately, no. Even when you win a reversal and get your money back, the initial chargeback still dings your record. It counts toward your overall chargeback ratio.

Payment processors watch this ratio like a hawk. This is exactly why having a solid grasp of what is chargeback management and focusing on prevention is the best long-term strategy for your business.

Tired of manually fighting chargebacks? ChargePay uses AI to automate the entire dispute process, recovering lost revenue for you. See how much you can recover.

.svg)

.svg)

.svg)

.svg)