A credit card preauthorization is a temporary hold a business places on your card to make sure it's valid and has enough funds for an upcoming purchase. Think of it less like an actual charge and more like a temporary reservation for your money.

This hold doesn't take any funds from your account. It just reduces your available credit for a short time.

What Is a Credit Card Preauthorization?

Ever checked into a hotel or rented a car and spotted a "pending" transaction on your credit card statement for an amount you hadn't actually spent yet? That’s a credit card preauthorization in action. It's a normal, super important part of how modern payments work, acting as a financial safety net for both you and the merchant.

The main purpose is simple: verification. Before a business provides a service or product, they need to know you can pay for it. A preauthorization confirms that your account is active and the necessary funds are available, all without finalizing the sale. This is especially helpful for businesses where the final cost isn't known right away.

The Restaurant Reservation Analogy

Think of it like booking a table at a popular restaurant. You give them your name to hold your spot, ensuring you have a table when you show up. You haven't paid for the meal yet, but the restaurant has reserved that place just for you.

A preauthorization works the same way with your money. A merchant "reserves" a specific amount of your available credit to cover the expected cost. No money leaves your account during this hold, but you can't spend that reserved portion elsewhere until the hold is lifted. It's just a placeholder, confirming your ability to pay later. You can learn more about the complete journey of credit card transactions in our detailed guide.

This temporary hold is not a final charge; it’s a standard security measure that disappears once the actual transaction is completed or canceled. It protects merchants from non-payment and assures you that your service will be delivered smoothly.

Why This Is So Common

This method has become standard practice, especially in industries like travel and hospitality. In fact, over 40% of global merchants use preauthorizations to lower the risk of failed payments and disputes.

As fraudulent claims continue to climb—with chargeback volumes projected to hit 337 million by 2026—preauthorizations provide a vital first line of defense. They help create a more secure way to do business for everyone involved.

How the Preauthorization Process Works Step by Step

To really get your head around credit card preauthorization, it helps to follow the money—or in this case, the hold on the money. The whole thing is a carefully choreographed dance between you, the business, and the banks, and it all happens in a matter of seconds. Let's pull back the curtain and see what happens from the moment a card is used.

The journey kicks off with a simple request. When a merchant starts a transaction, they aren't actually asking for the full payment right away. Instead, their payment system sends a quick signal to the cardholder's bank, essentially asking, "Hey, does this person have enough credit available to cover this amount?"

This first step is the preauthorization request. Think of it like a bouncer checking an ID at the door; it's a quick verification before anyone gets let in.

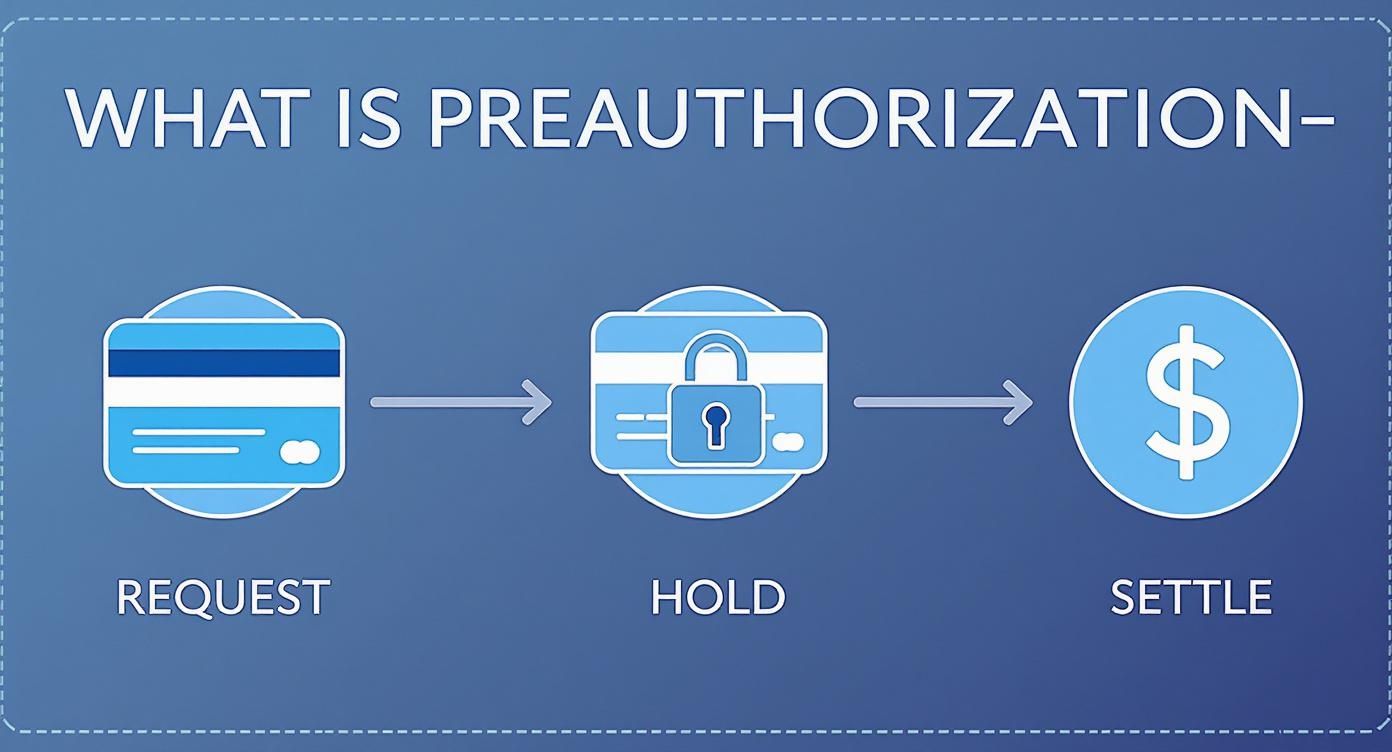

The Three Key Stages of a Preauthorization

Once that request is fired off, a few things happen very quickly. The entire flow is built for speed and security, making sure the merchant is protected while the customer's funds aren't actually touched until the final purchase is locked in.

This infographic breaks down the simple three-step flow of a credit card preauthorization.

As you can see, the process moves from a simple request to a temporary hold, and finally, to either settlement or release.

Here's how it unfolds in a clear sequence:

The Merchant's Request: The business (let's say, a hotel) uses its point-of-sale (POS) terminal or online payment gateway to send a preauthorization request to the customer's credit card issuer (their bank). This request includes a specific amount to hold.

The Bank's Approval and Hold: The bank gets the request and takes a quick look at the account. It confirms two things: that the card is valid and that there's enough available credit. If it's all good, the bank approves the request and places a temporary preauthorization hold on the funds. This reduces the customer's available credit by that amount.

The Final Transaction Phase: This is where the road forks. The next step is either capturing the funds or releasing the hold.

A preauthorization is not a charge. It is a temporary freeze on a portion of your available credit. Your account balance does not change, but the amount you are able to spend is temporarily lowered.

Capturing the Payment or Releasing the Hold

After the service has been provided or the final purchase amount is clear, the merchant has to close the loop. They can't just leave that hold on the account forever.

If a purchase goes through, the merchant will capture the funds. This action turns the temporary hold into a final, permanent charge. The final amount is often different from what was preauthorized—for instance, a hotel might preauthorize $100 for incidentals but only capture $35 for the items actually used from the mini-bar.

On the other hand, if no purchase is made or the transaction is canceled, the preauthorization hold is voided or released. The merchant tells the bank to remove the hold, and the available credit is restored. This happens all the time in "card-not-present" situations where a card is used to secure a reservation but not for the final bill. You can learn more about how merchants can securely handle card-not-present transactions in our guide.

This system is pretty fundamental to how modern commerce works. The global push for real-time payments, which has jumped by 37.2%, leans heavily on tools like preauthorization to keep things running smoothly. In North America, where digital wallet use has hit 76%, and in Europe, where 88% of card payments are contactless, preauthorizations are just a standard part of the process that keeps transactions secure.

Preauthorization Hold vs a Final Charge

Ever seen a "pending" transaction on your credit card statement and assumed the money was already gone? It’s a common mix-up, but a credit card preauthorization hold and a final charge are two completely different animals. Getting them straight is key for both happy customers and smooth operations on the merchant side.

At its heart, the distinction is pretty simple. Think of a preauthorization as a temporary reservation of funds, while a final charge is the actual transfer of that money. One is a placeholder; the other is the real deal.

The Key Differences in Purpose and Appearance

The first big split is their purpose. A preauthorization is all about verification and security. It’s a quick check to confirm a credit card is valid and has enough available credit to cover a potential purchase, which cuts down the risk for the merchant.

A final charge, on the other hand, is the final act—the settlement of a completed transaction. This is the merchant officially collecting payment for the goods or services they’ve provided.

You can see this difference reflected in how they show up on a card statement.

- Preauthorization Holds: These pop up as "pending" or "processing." They don’t actually change your account balance, but they do temporarily reduce your available credit.

- Final Charges: These appear as "posted" transactions. They’re permanent entries that increase your balance, reflecting money that has officially been transferred from your credit line.

For businesses using modern payment systems, having solid tools for managing pending transactions is a must. It keeps everything clear and running smoothly, from the initial hold to the final capture.

Duration and Common Scenarios

Another crucial difference is how long they stick around. A preauthorization hold is, by nature, temporary. The exact duration can vary, but it typically lasts anywhere from a few hours to several days, depending on the merchant’s industry and the bank’s policies. If the merchant doesn't capture or cancel it, the hold simply expires and vanishes.

In contrast, a final charge is permanent. It stays on your account until it's paid off and doesn't just disappear on its own. While it can be disputed—which kicks off a whole other process—it’s considered a settled debt. If you want to dive deeper into that, you can check out the differences between a chargeback vs a refund in our detailed article.

A preauthorization is like reserving a rental car—the company holds your card details to ensure you're good for the cost. A final charge is like buying a coffee—you pay the exact amount, and the transaction is immediately complete.

To make this crystal clear, let's break it down in a side-by-side comparison.

Preauthorization Hold vs Final Charge at a Glance

This table lays out the core differences between a temporary hold and a final, posted charge.

Understanding these distinctions helps everyone involved—from the customer wondering about a pending charge to the merchant managing their cash flow.

Why Businesses Use Preauthorization Holds

If you're a business owner, you know that a credit card preauthorization is much more than just a technical step. It’s a vital tool for managing financial risk and, frankly, for keeping the lights on. Think of it as a safety net that protects your business from potential losses before they can even happen.

At its core, a preauthorization hold is all about being proactive. It lets you confirm that a customer has a valid payment method with enough funds before you hand over a product or provide a service. This one simple check dramatically cuts down on the headaches of declined payments, insufficient funds, or fraudulent cards after you've already committed your resources.

This isn't just about stopping fraud—it's about creating a predictable and stable cash flow. For any business, but especially for small and medium-sized ones, a series of failed transactions can be incredibly damaging. A preauthorization is your first line of defense against that kind of instability.

Reducing Costly Chargebacks and Disputes

One of the biggest migraines for any merchant is the dreaded chargeback. When a customer disputes a charge, it kicks off a time-consuming and expensive process that often leads to lost revenue and extra fees. Preauthorization helps nip this problem in the bud.

By verifying the card and the customer's ability to pay right from the start, you can weed out many of the issues that snowball into disputes later. For example, a customer can’t really claim they didn't have the money for a purchase if a preauthorization hold was successfully placed. That initial check provides a layer of proof that the account was legitimate and funded when the agreement was made.

A preauthorization is like an initial "handshake" between you and the customer's bank. It establishes that the transaction is legitimate from the get-go, which can be invaluable if a dispute ever pops up.

This proactive measure is a key part of a strong defense. Preventing a dispute is always, always better than fighting one, and that's where solid merchant chargeback protection strategies are so important for your long-term financial health. Using holds significantly lowers the odds of you facing these costly battles.

Securing Payment for Variable Costs

Lots of businesses operate in a way where the final bill isn't set in stone from the beginning. Think about a hotel stay with potential mini-bar charges, or a car rental that might come back with an empty gas tank. Preauthorization is the perfect solution for these scenarios.

A hotel, for instance, might place a hold for the room cost plus a little extra for potential incidentals. This guarantees they can cover the final bill, whatever it ends up being, without having to chase down the customer for payment later. The hold makes sure the funds are reserved and ready to be captured once the final total is calculated.

Here are a few common examples from different industries:

- Car Rentals: A hold is placed to cover the rental fee plus a security deposit for potential damages, tolls, or fuel charges.

- Gas Stations: When you pay at the pump, a hold is placed to ensure you can cover a full tank, even if you only end up pumping a few gallons.

- Restaurants and Bars: It's standard practice to preauthorize a card to open a tab, ensuring the customer can cover their bill at the end of the night.

The global credit card system is designed to handle exactly this. With over 1.3 billion Visa and 1.1 billion Mastercard cards out there, preauthorization is a standard feature. For businesses, using this tool helps manage the risks that come with the 3.9 credit cards the average American holds, reducing the chance of failed transactions and disputes. You can find more insights on global credit card usage on sellerscommerce.com.

Ultimately, this process lets businesses with uncertain final costs operate with confidence, knowing that payment is secured from the moment the service begins. It turns a potential financial headache into a secure, manageable part of daily operations.

Where You Will See Preauthorizations in Real Life

You’ve probably run into credit card preauthorization way more often than you think. It's not some obscure financial trick; it’s a standard practice you encounter in completely normal, everyday situations.

Once you see how it works in the real world, you'll understand why this temporary hold is such a practical tool for so many businesses. Preauthorizations are most common in industries where the final bill isn't known upfront. It’s a simple, effective way for a merchant to make sure they’ll get paid for the full amount, whatever it turns out to be.

At the Hotel Front Desk

This is the classic example of preauthorization. When you check into a hotel, the front desk staff will almost always swipe your card, even if you’ve already paid for the room itself.

They aren't double-charging you. What they're actually doing is placing a preauthorization hold for a set amount—usually the cost of one night plus a little extra for "incidentals."

So, why do they do this? The hold is basically a security deposit to cover any extra costs you might rack up during your stay.

- Mini-bar snacks or drinks: That late-night candy bar is covered.

- Room service orders: Your breakfast in bed is secured by the preauthorization.

- Pay-per-view movies: The hold ensures the hotel gets paid for any movies you decide to watch.

- Potential damages: In rare cases, it provides a buffer for any accidental damage to the room.

When you check out, the hotel calculates your final bill. They "capture" the exact amount you owe from the preauthorized hold and release whatever is left over. If you didn't have any extra charges, the whole hold is released, and it vanishes from your pending transactions. This is a core part of payment processing in hospitality and a key concept for effective chargeback management in travel.

By preauthorizing a card, a hotel secures payment for variable costs without needing a separate cash deposit, creating a smoother and more secure check-in experience for everyone.

Renting a Car

Renting a vehicle is another prime example. When you pick up your rental, the company will place a hold on your card that's often much higher than the daily rental fee you were quoted.

This hold typically covers the estimated total cost of the rental, plus a hefty security deposit. That deposit protects the company from all sorts of potential issues.

The preauthorization gives the rental agency a financial safety net for things like:

- Late Returns: If you bring the car back a day late, the extra fees are already covered.

- Fuel Charges: Didn't return the car with a full tank like you were supposed to? They can charge you for the refuel.

- Tolls and Fines: Any unpaid tolls or traffic tickets you racked up can be settled from the hold.

- Damages: It acts as a deductible in case the car comes back with new dings or scratches.

After you return the car and they’ve given it a final look-over, the company captures the actual amount you owe and releases the rest of the hold.

At the Gas Pump

Have you ever paid at the pump and later noticed a pending charge for $100 or more, even though you only bought $40 worth of gas? That’s a preauthorization in action.

Because the pump has no idea how much fuel you’re going to take, the system puts a temporary hold on your card for a fixed, high amount. This is just to make sure you have enough available credit to cover a full tank, preventing drive-offs.

The moment you hang up the nozzle, the pump sends the final, correct amount to your bank. The initial hold is then replaced by the actual charge, usually within a few hours.

Other Common Scenarios

Beyond these big three, you’ll find preauthorizations popping up in other places. Restaurants and bars often use them to open a tab, guaranteeing the final bill can be covered. Automated booking systems also lean on this method to secure reservations without charging customers upfront.

For example, when businesses choose a tennis and padel court reservation software, systems that use preauthorization are a game-changer for managing bookings and cutting down on no-shows.

In every case, the goal is the same: verify a card is valid and secure a future payment for a service with a variable cost, all while protecting the business from taking a loss.

Making Preauthorization Work for Everyone

Whether you’re the customer watching a pending charge hit your account or the merchant placing one, making the credit card preauthorization process go smoothly really boils down to two things: clear communication and knowing what to expect. A little bit of proactive management on both sides can head off confusion, build trust, and make sure the whole transaction wraps up without a hitch.

Knowing your role in the process makes the whole experience better. For customers, it’s all about keeping an eye on your available credit. For merchants, it’s about being transparent and efficient with your customer’s money.

Advice for Customers

As a cardholder, the single best thing you can do is stay on top of any holds on your account. They’re a completely normal part of using a credit card, but knowing how they work is key to managing your money.

Here are a few simple tips to keep in mind:

- Check Your Pending Transactions: Pop open your online banking app every now and then. Seeing which holds are active helps you track your real-time available credit so you don't accidentally spend more than you have available.

- Remember the Impact on Your Credit Limit: A preauthorization hold isn't just a placeholder; it actively reduces your spending limit. This is a big deal when you're traveling or making several large purchases, as a few holds can quickly tie up a huge chunk of your credit line.

- Don’t Panic If a Hold Lingers: Holds usually disappear in a few business days, but sometimes they can stick around. If you notice a hold is still there long after you've completed a transaction, or if it seems like it's been forgotten, your first step should be to contact the merchant. If that doesn't work, a quick call to your bank will almost always get it sorted out.

The bottom line here is to just be aware. A preauthorization isn't an error on your account; it's a standard part of the process. Keeping tabs on your account helps you spot any real issues right away.

Best Practices for Merchants

If you run a business, transparency is your best friend. Customers are far more understanding and patient when they know what’s happening from the get-go. Setting clear policies and acting quickly are the cornerstones of building great customer relationships and avoiding needless chargebacks.

Here’s how you can make the whole process feel seamless for your customers:

- Communicate Your Hold Policy Loud and Clear: Be upfront about preauthorizations. A simple heads-up on your website, at the checkout counter, or in your booking confirmations can prevent a lot of headaches. A simple line like, "Just so you know, we place a temporary hold of $50 for any incidentals," is all it takes.

- Keep Hold Amounts Reasonable: Only preauthorize what you actually need. Slapping an excessively large hold on a customer's card is a surefire way to cause frustration and tie up their funds unfairly. Base the amount on realistic potential costs, not a worst-case scenario.

- Capture or Release Funds Promptly: The moment the final bill is settled, capture the payment. If the customer cancels their order or booking, release that hold immediately. Taking swift action shows you respect your customer's finances and helps you build a reputation as a business that’s easy and fair to deal with.

Got Questions? We've Got Answers

Still have a few things you're wondering about credit card preauthorization? Totally normal. It's one of those behind-the-scenes processes that isn't always crystal clear. Here are some quick, straightforward answers to the questions we hear most often.

How Long Does a Preauthorization Hold Last?

A preauthorization hold isn’t forever. Typically, it sticks around for about 5 to 7 business days, but this can change depending on the business you're dealing with and your bank's own rules. For example, a hotel might keep the hold for your entire stay, while the hold from a gas pump usually vanishes within 24 hours.

If the merchant doesn't finalize the payment or cancel the hold, it just expires on its own, and the funds are released back to your available credit.

Does a Preauthorization Actually Take Money from My Account?

Nope, a preauthorization doesn't pull any money out of your account. It's just a temporary hold that lowers your available credit. Think of it less like a charge and more like a reservation for the funds.

Your account balance stays exactly the same until the business captures the final payment. Only then does the hold turn into an actual charge.

A preauthorization is like putting a "reserved" sign on a portion of your credit line. The money is still yours, but it's earmarked for a specific payment, so you can't spend it somewhere else.

What Should I Do If a Hold Isn’t Released?

If you see a pending charge that's overstayed its welcome, the first move is to contact the merchant. They’re the ones who started the hold, so they’re the ones who need to release it. A quick phone call or email is usually all it takes to get it sorted out.

If you can't get ahold of them or they aren't helping, your next call should be to your credit card company. They can give you more details on the hold's status and sometimes help speed up the process of getting it removed.

Can I Cancel a Preauthorization Myself?

As a customer, you can't just cancel a preauthorization hold on your own. That power lies with the merchant who placed it in the first place. If you cancel a reservation or a service, it's on them to tell their payment processor to release the hold on your card.

Once they give the command, the funds should free up again. Just keep in mind it might take a few business days for your bank to process the release and for your available balance to update.

Managing payments and stopping disputes in their tracks is a must for any online business. With ChargePay, you can put your chargeback management on autopilot, protect your revenue, and get back to what you do best—growing your business. Stop losing money to bogus claims and let our AI-powered system get your funds back effortlessly. Learn how ChargePay can secure your profits today.

.svg)

.svg)

.svg)

.svg)