When you hear "disputes with banks," it’s easy to think of a simple chargeback. But for any business owner, especially in e-commerce, the real story is much deeper—and it comes with a much higher price tag than just the lost sale.

Understanding the Real Cost of Bank Disputes

Dealing with bank disputes often feels like you're fighting a battle on multiple fronts. It all starts with the immediate hit of losing the revenue from that transaction, but honestly, that's just the tip of the iceberg. The costs quickly start to pile up, becoming a major financial and operational drag on your business.

Think of it this way: every single dispute kicks off a chain reaction of hidden expenses.

For starters, your bank or payment processor is going to hit you with a non-refundable fee for every chargeback, no matter who ends up winning. These fees can stack up fast, turning what seems like a small problem into a serious financial headache. Our guide on what is chargeback fee breaks down just how damaging these penalties can be.

Beyond the Transaction Amount

The financial sting doesn't stop with fees. You also have to account for the operational costs, which are often overlooked but can be just as damaging. Your team has to drop what they’re doing to handle the dispute.

This means they have to:

- Investigate the claim: This involves digging through order histories, customer communication logs, and shipping records.

- Gather evidence: Compiling screenshots, receipts, and proof of delivery takes valuable time away from activities that actually make you money.

- Write a response: Crafting a compelling rebuttal that meets the bank's strict, and often confusing, requirements is a skill in itself.

All of this eats up hours of your team's time—time that could be spent on customer service, marketing, or developing new products. It’s a resource drain that directly hits your bottom line.

To give you a clearer picture, let's look at the common disputes businesses run into and how they really affect operations.

Common Bank Disputes and Their Business Impact

Here’s a quick overview of the most frequent disputes businesses face, what causes them, and their typical financial impact.

These examples show that the financial fallout extends far beyond just refunding the original sale.

The Rise of Sophisticated Scams

Today’s bank disputes aren't always about a customer claiming their package never showed up. They’ve evolved into much more complex forms of fraud.

In fact, a global survey of banking scams found that sophisticated threats like push payment fraud are now one of the most frequent issues financial institutions are dealing with worldwide. This means businesses aren't just handling simple misunderstandings anymore; they're up against organized fraud attempts. You can learn more about these evolving threats in the KPMG report.

The true cost of a bank dispute isn't just the money you lose in the transaction; it's the fees you pay, the time your team wastes, and the potential long-term damage to your business's reputation and ability to process payments.

Ultimately, ignoring the full scope of these disputes is a costly mistake. Each one chips away at your profits and distracts your team from what really matters. Recognizing the real stakes involved is the first step toward building a solid defense that protects your revenue and helps your business grow.

How to Respond to a Bank Dispute Effectively

That notification about a new dispute? It can feel like a punch to the gut. But don't panic. The best way to handle disputes with banks is to have a clear, repeatable process ready to go. Acting fast and being methodical is everything here.

The moment that notification hits your inbox, the clock starts ticking. Most payment networks give you a pretty tight window to respond—sometimes just a few weeks. If you miss that deadline, it's an automatic loss. So, the first thing you need to do is pull up every piece of information you have on that specific transaction.

Gather Your Evidence Immediately

Your job is to build a case so solid and straightforward that the bank has no other option but to side with you. This means digging up undeniable proof that the transaction was legit and you held up your end of the bargain. Put on your detective hat and start collecting everything related to the order.

Here’s a quick checklist of what you should be looking for:

- Transaction and Order Details: The receipt, the order confirmation email you sent, and any notes you have in your system.

- Customer Communication: Save every single email, chat log, or social media message you exchanged with the customer. These can be gold, especially if they show satisfaction or prove you offered support.

- Proof of Delivery: This one is non-negotiable. A tracking number with a "delivered" status to the correct address is probably the strongest piece of evidence you can have.

- Product Descriptions and Policies: Grab screenshots of the product page the customer bought from. Don't forget to include your return and refund policies to prove you were upfront about everything.

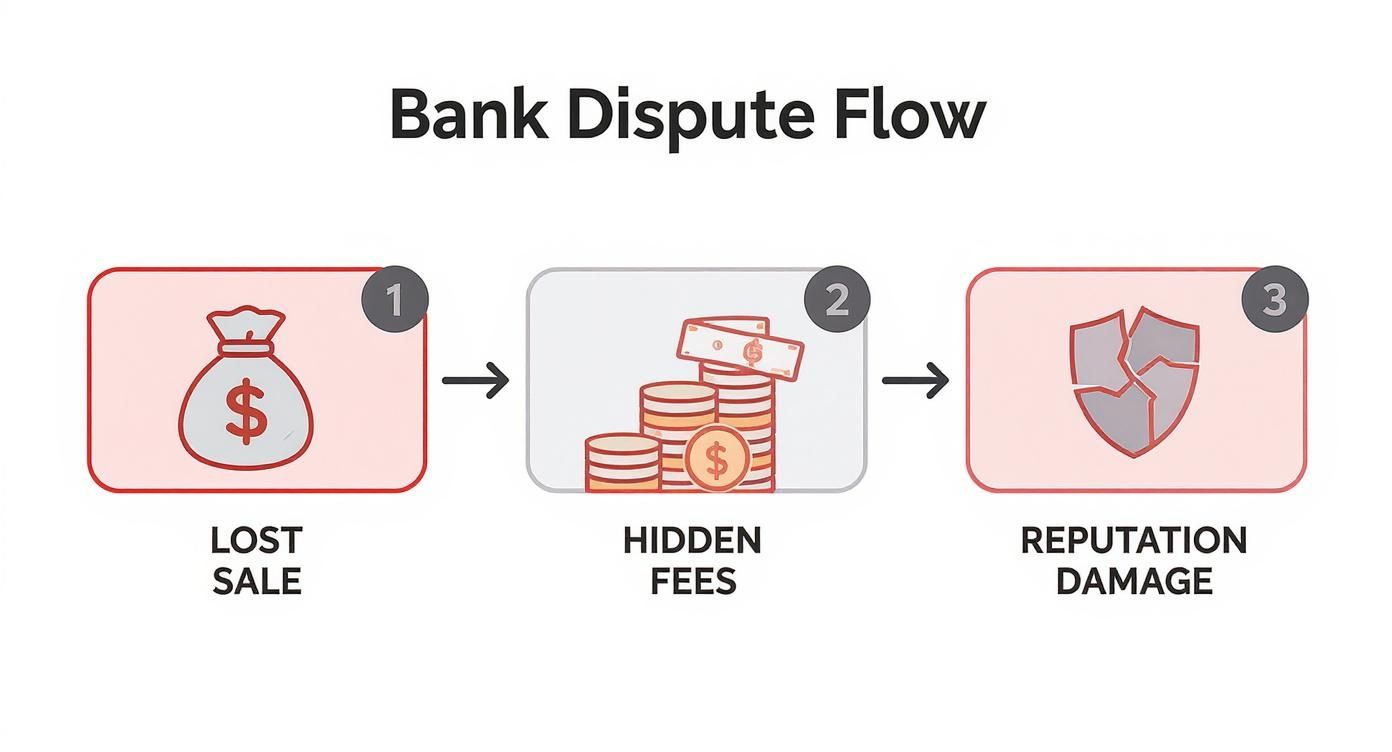

This infographic really puts into perspective how the costs of a dispute can spiral out of control, from the initial lost sale to hidden fees and damage to your reputation.

As you can see, failing to respond effectively means you're not just losing that one sale. You're also paying penalties and putting your business's good standing on the line.

Craft a Winning Rebuttal Letter

Once you've got all your evidence lined up, it's time to write your response, which is often called a rebuttal letter. The name of the game here is clarity and precision. Bank reviewers look at thousands of these, so make yours incredibly easy to digest. Keep it professional, stick to the facts, and leave emotion out of it.

You'll want to structure your letter to directly counter the customer's claim. For example, if they're claiming "product not received," your delivery confirmation should be front and center. If the claim is "product not as described," use your product page screenshots and communication logs to prove otherwise.

A strong rebuttal is objective and evidence-based. It should tell a clear story of a valid transaction, supported by documentation that leaves no room for doubt.

Finally, package everything up and submit your response through your payment processor’s portal, making sure you're well ahead of the deadline. For a deeper look at the specific tactics that can give you an edge, check out our guide on how to win a credit card dispute. Following these steps gives you the best possible shot at protecting your hard-earned revenue.

Proactive Strategies to Prevent Bank Disputes

The best way to handle disputes with banks? Stop them before they even start. While having a solid response strategy is crucial, preventing the problem in the first place saves you a world of time, money, and stress. It’s all about building trust from the very first click.

This proactive approach doesn't mean you have to overhaul your entire business. More often than not, it's the small, thoughtful changes that make the biggest difference in cutting down chargebacks and keeping both your customers and the banks happy.

Crystal Clear Communication Is Key

Most disputes aren't born from bad intentions; they come from simple confusion. A customer glances at their statement and doesn't recognize a charge, or a product arrives and doesn't quite match what they pictured. Your first and best line of defense is absolute clarity.

Think about your billing descriptor for a second—that little line of text that pops up on a customer's bank statement. If it’s your obscure legal company name instead of your well-known brand, you’re practically inviting a dispute. Make it instantly recognizable.

The same idea applies to your product pages. Are your descriptions accurate and detailed? Do your photos show the product from every angle, maybe even next to a common object for scale? Being brutally honest about what you're selling is the best way to prevent the dreaded "not as described" claim.

Simple Steps to Reduce Disputes

You can put several powerful tactics in place right now to safeguard your business. These small adjustments can dramatically lower your dispute rate.

- Offer Top-Notch Customer Service: Make it ridiculously easy for customers to contact you. A prominent phone number, a clear email address, or a live chat widget can turn a potential dispute into a simple refund or exchange.

- Set Clear Policies: Your shipping, return, and refund policies should be easy to find and even easier to understand. No legalese. A customer who knows exactly what to expect is far less likely to file a chargeback out of frustration.

- Always Use Tracking: Ship every single order with delivery confirmation. This is your number one piece of evidence against "product not received" claims. It’s non-negotiable.

Preventing a dispute is always cheaper and more effective than fighting one. By focusing on transparency and customer experience, you're not just avoiding chargebacks—you're building a stronger, more trustworthy brand.

A robust defense against potential bank disputes and financial fraud starts with mastering bank statement verification to ensure every transaction is solid. Verifying that the details match up at every stage is a fundamental step in protecting your revenue.

Stay Ahead of Growing Threats

Preventing disputes isn't just good business practice; it's a financial necessity, especially as these issues become more common. Global chargeback volume is a serious challenge for merchants everywhere.

In fact, from 2025 to 2028, the global chargeback volume is projected to grow by 24%, hitting an estimated 324 million transactions each year. That trend alone should tell you how critical proactive measures are.

Ultimately, by zeroing in on clear communication and transparent operations, you create an environment where disputes are far less likely to crop up. These strategies are your best defense, protecting your bottom line and letting you focus on growing your business instead of constantly putting out fires.

Using Automation for Smarter Dispute Management

Let's be honest, managing disputes by hand is a grind. It’s slow, tedious, and as your business scales, it’s frighteningly easy for things to slip through the cracks. What might start as one or two chargebacks a month can quickly snowball into a full-time headache. This is where automation isn't just helpful—it's a game-changer for handling disputes with banks.

Modern tools can step in and handle the entire messy process. We're talking about automatically gathering the right evidence, crafting compelling responses, and submitting everything on your behalf. It’s not just about saving a few hours; it’s about using technology to make smarter, data-driven decisions that directly protect your revenue.

How Automation Outperforms Manual Efforts

Picture the usual fire drill: a dispute notice comes in, and you're left scrambling. You have to dig through old emails, hunt down shipping confirmations, and try to piece together a coherent rebuttal letter, all with a ticking clock in the background. It's stressful.

An automated system does all of that in seconds. It plugs directly into your sales and shipping platforms, pulling every piece of necessary proof instantly.

This speed and precision give you a massive upper hand. Banks and card networks operate on strict rules and even stricter deadlines. Automation ensures you hit every requirement, every single time. It takes the guesswork out of the equation and eliminates the risk of a missed deadline costing you the dispute.

By automating the dispute response process, you’re not just speeding it up—you're making it more consistent and reliable. This frees up your team to focus on growing the business, not on tedious administrative tasks.

Relying on manual processes alone is a huge financial gamble. For every dollar lost to fraud, it’s estimated that US merchants will actually pay $4.61 in related costs. The numbers get even scarier when you look at the big picture: total annual losses from chargeback fraud are projected to hit $28.1 billion by 2026. That’s a staggering 40% jump from 2023. These aren’t just abstract figures; they represent real money walking out the door. You can dig into more of these eye-opening chargeback fraud statistics to see the full scope of the problem.

Let's break down how automation truly transforms the day-to-day work of managing disputes.

Manual vs Automated Dispute Management

The difference is night and day. Automation removes the friction and potential for error at every single step, turning a chaotic manual workflow into a streamlined, efficient machine.

AI-Powered Insights and Smarter Decisions

The best automation platforms don't just stop at filling out forms. They use artificial intelligence to spot trends and patterns that a human eye would almost certainly miss. For example, an AI system might flag a cluster of chargebacks coming from a specific zip code or linked to a particular product, hinting at a potential friendly fraud scheme.

This gives you powerful, actionable insights to beef up your defenses. You can start making informed decisions, like adding extra verification steps for certain types of orders or tweaking product descriptions to head off future misunderstandings. It’s all about shifting from a reactive "put out the fire" mode to a proactive, preventative one.

If you’re ready to see what this looks like in practice, you can explore our complete guide to automated chargeback and dispute management using AI.

Ultimately, bringing automation into your dispute management is one of the smartest investments you can make for your business. It directly boosts your win rates, recovers revenue you’d otherwise lose, and transforms a major operational headache into a smooth process that works for you 24/7.

When and How to Escalate a Difficult Dispute

You’ve done everything by the book. You gathered compelling evidence, wrote a crystal-clear rebuttal, and followed every single rule, but the bank still sided with the cardholder. It’s incredibly frustrating, but a lost dispute isn't always the end of the road.

When the standard process lets you down, it’s time to think about escalating.

Escalating a dispute simply means taking your case up the chain of command, either to a higher authority within the bank or to an outside regulatory body. This is your shot to get a fresh pair of eyes on the evidence and make the argument that the first decision was flat-out wrong.

This move isn't for every lost dispute, of course. It's reserved for those cases where your proof is undeniable and you genuinely believe the outcome was unfair.

Before you even think about escalating, you need to be 100% certain your documentation is airtight. If you have a feeling the case might head into more formal territory, it’s smart to get familiar with what happens during pre-arbitration so you know exactly what to expect.

Knowing Your Escalation Paths

Once you’re ready to move forward, you have a few clear options to push your dispute up the ladder. The best path really depends on the specifics of your case and the bank you’re dealing with.

Most businesses will have these primary options available:

- The Bank's Internal Ombudsman: Many of the bigger banks have an internal, independent office whose whole job is to resolve complaints that couldn't be settled through the usual channels. This should always be your first stop. It's often the fastest way to get a formal review without looping in outsiders.

- Regulatory Bodies: If the internal route is a dead end, you can file a formal complaint with a government agency. In the United States, the Consumer Financial Protection Bureau (CFPB) is a serious player. They investigate consumer complaints against financial companies and have the power to make things happen.

- Legal Counsel: For those really high-value disputes or situations involving complex fraud, it might be time to call in a lawyer. Someone who specializes in financial or commercial law can help you understand your legal standing and navigate the often-confusing system.

When you escalate, your mission is to tell a clear, chronological story backed by evidence that leaves no room for doubt. You want to make it incredibly easy for the reviewer to see exactly why the original decision was a mistake.

Presenting Your Case for a Formal Review

Think of an escalation as rebuilding your case from scratch for a brand-new audience. Don’t just forward the same old documents and hope for the best.

Instead, put together a formal package. It should include a cover letter that neatly summarizes the dispute, a timeline of events, all your original evidence, and a direct explanation of why you believe the decision needs to be overturned.

Be precise. Be professional. And be persistent.

Keep a detailed record of every email, phone call, and letter. Follow up systematically so your case doesn't get lost in a pile. Escalating a dispute definitely requires patience, but knowing your rights—and actually using them—is critical to protecting your business from unfair losses.

Common Questions About Bank Disputes

Even with the best game plan, navigating disputes with banks can feel like you're trying to solve a puzzle in the dark. Let's shed some light on the questions we hear from merchants all the time.

What Is the Difference Between a Chargeback and a Refund?

Think of it this way: a refund is a friendly handshake. It’s a direct agreement between you and your customer to return their money. You're in control, and it's a normal part of customer service.

A chargeback, however, is a whole different beast. This is a forced reversal kicked off by the customer's bank. The money is immediately yanked from your account while they investigate. This process always comes with extra fees and can ding your reputation with payment processors.

How Long Do I Have to Respond to a Bank Dispute?

The clock starts ticking the second you're notified, and the deadlines are non-negotiable. Card networks like Visa and Mastercard set the rules, and you typically have somewhere between 20 to 45 days to get your evidence together and submit it.

Miss that window? It’s an expensive mistake. You’ll almost certainly lose the dispute—and the revenue—by default. Moving fast is absolutely critical.

The biggest difference between a refund and a chargeback is who’s in the driver's seat. One is a customer service solution you manage. The other is a formal, bank-led process that costs you time, money, and fees, no matter how it turns out.

Can I Stop Friendly Fraud Chargebacks?

Friendly fraud is tricky—it’s when a customer disputes a charge they actually made. While you can't eliminate it entirely, you can absolutely put up a strong defense to reduce it. Prevention is your best weapon here.

A few tactics I've seen work wonders:

- Use Clear Billing Descriptors: Make sure your business name is instantly recognizable on their bank statement. "XYZ_SHOP" is much better than a generic processor code.

- Offer Great Customer Service: Be easy to find and quick to respond. You want customers to email you, not call their bank.

- Maintain Simple Return Policies: A confusing or difficult return process is a fast track to a frustrated customer filing a dispute. Keep it simple.

- Always Use Delivery Confirmation: This is your golden ticket. It's the best proof you have against claims that a product never showed up.

The goal is to make talking to you easier and more appealing than filing a dispute. For a deeper dive, check out our detailed guide on disputes and chargebacks.

What Happens If I Get Too Many Chargebacks?

Payment processors watch your chargeback ratio like a hawk. This is simply the number of chargebacks you get compared to your total transactions. If that number creeps above 1%, alarms start going off, and you'll be labeled a "high-risk" merchant.

That's a label you don't want. It can trigger some serious consequences, like steeper processing fees, having your funds held in a reserve account, or even getting your merchant account shut down completely. That would make it nearly impossible to accept credit card payments at all.

Protecting your revenue means getting a handle on bank disputes. ChargePay uses AI to automate the entire fight, from finding the right evidence to submitting responses that win, helping you get your money back without the headache. Learn more at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)