Think of disputes and chargebacks as two stages of the same headache. A dispute is the initial flare-up—a customer flagging an issue with their bank. A chargeback is the full-blown migraine that follows, where the bank yanks the money right out of your account.

Clearing Up the Confusion Behind Disputes and Chargebacks

Every sale you celebrate carries the small but real risk of a payment problem. Getting the difference between a simple dispute and a painful chargeback isn't just about knowing the lingo; it's about protecting your bottom line.

Let's walk through a common scenario. A customer sees a charge on their statement they don't recognize or has an issue with a purchase. Their first move is to call their bank. That phone call kicks off the dispute.

At this point, it’s basically a warning shot. The bank pings you about the inquiry, giving you a short window to clear things up directly. Maybe you can provide a refund, offer a replacement, or just explain the charge.

If you can't resolve it in time, or if the customer's bank decides to push it forward, the situation escalates into a chargeback. This is no longer a simple question. The bank forcibly reverses the transaction, taking the funds from your merchant account and handing them back to the cardholder while the investigation unfolds.

Why This Distinction Matters

Understanding this sequence is everything because how you respond depends entirely on where you are in the process. Catching it at the dispute stage—sometimes called a retrieval request—is your golden opportunity to stop a chargeback before it ever happens.

A formal chargeback is so much more than a refund. It hits you with penalty fees, dings your reputation with payment processors, and can even put your entire merchant account at risk.

A Quick Look at Disputes vs. Chargebacks

To make it even clearer, let's break down the core differences in a simple table. Think of this as your cheat sheet for telling these two stages apart.

In short, a dispute is a question, while a chargeback is a forceful action. Both demand your immediate attention, but the stakes get much higher once a dispute becomes a chargeback.

Who Is Most at Risk?

While any business can get hit with chargebacks, some industries are just more prone to them. If you’re in a sector known for higher fraud or customer dissatisfaction rates, connecting with specialized high-risk merchant account providers is a smart move for managing your financial stability.

To sum it all up:

- A Dispute Is an Inquiry: This is the customer raising their hand with a question for their bank. It’s your chance to provide answers and shut the process down before it costs you real money.

- A Chargeback Is a Reversal: This is the bank taking action. The money is gone from your account, and now the burden is on you to prove the transaction was legitimate to get it back.

Now, let's dive into the entire lifecycle to see how you can manage both effectively and keep your hard-earned revenue safe.

The True Cost of Chargebacks to Your Business

When you get hit with a chargeback, the first thing you probably see is the lost sale. But that refunded amount? It's just the tip of the iceberg. The real financial damage from disputes and chargebacks runs much deeper, chipping away at your profitability in ways you might not even realize.

Think of it like an unexpected car repair. The bill for the new part is bad enough, but then you’ve got the towing fees, labor costs, and the time you lose without your car. A single chargeback works the same way, kicking off a chain reaction of hidden costs that add up fast.

For every single chargeback filed, your payment processor will slap you with a non-refundable chargeback fee. This is a penalty you have to pay whether you win or lose the dispute, and it can range from $15 to over $100. It's basically their fee for the administrative hassle. To see a full breakdown, check out our guide on what a chargeback fee includes.

The Financial Drain Beyond the Lost Sale

The financial sting doesn't stop with fees. The whole process eats up your team's valuable time and energy. Someone has to drop what they’re doing to dig into the claim, hunt down evidence like receipts and shipping confirmations, and then write a convincing response.

These operational costs are a big deal. Every hour spent on administrative busywork is an hour not spent growing the business, helping other customers, or making your products better. For a small team, this can be a massive productivity killer.

The financial impact of chargebacks extends far beyond your business. On average, it costs banks between $9.08 and $10.32 just to process a single chargeback. When you consider that merchants only win about 18% of the cases they fight, it's clear how difficult it is to recover these mounting losses. To learn more, read the full analysis on the true cost of chargebacks from Mastercard.

The Long-Term Damage to Your Business Health

Beyond the immediate cash drain, chargebacks inflict serious, long-term harm on your business. Payment processors keep a close eye on your chargeback ratio—that is, the number of chargebacks you get compared to your total number of transactions.

Each card network, like Visa and Mastercard, sets a threshold, usually around 1%. If your ratio starts creeping over that line, you get flagged as a high-risk merchant. That new label comes with a whole new set of headaches:

- Higher Processing Fees: Processors will start charging you more for every single transaction to cover their perceived risk.

- Monthly Monitoring Programs: You could be forced into a program that hits you with steep monthly fines until your ratio drops.

- Frozen Funds: The processor might hold back a percentage of your revenue in a reserve account, just in case there are more chargebacks.

The worst-case scenario? If you can't get your chargeback ratio under control, you risk getting your merchant account shut down. Losing your ability to accept credit card payments is a death sentence for most online businesses, and it becomes incredibly difficult to find another processor willing to take you on once you've been blacklisted.

This is why treating chargebacks as just another "cost of doing business" is so dangerous. Each one is a direct threat to your financial stability and your ability to operate. Once you understand all these hidden costs, it becomes crystal clear that a proactive strategy for managing disputes and chargebacks isn't just a good idea—it's essential for survival.

Understanding Why Chargebacks Happen

To get a handle on disputes and chargebacks, you have to know why they happen in the first place. It’s rarely as simple as a customer just wanting their money back. Think of a chargeback as a symptom of a deeper problem—figuring out that problem is your first step to building a solid defense.

You almost have to put on a detective hat. When a dispute lands on your desk, you need to look for clues to understand what really went wrong. When you boil it down, almost every single chargeback can be traced back to one of three main culprits.

These root causes cover everything from simple, honest mistakes on your end to straight-up criminal activity. Getting familiar with each one helps you see where the weak spots in your process might be.

Merchant Error and Service Issues

Let's be honest: sometimes, the fault is genuinely with the business. These are often the most straightforward chargebacks to understand and, thankfully, the easiest to prevent down the road. Merchant error simply means your operations didn't live up to what the customer was expecting.

Simple slip-ups can easily lead to a frustrated customer calling their bank. For example, if you ship the wrong product, the item shows up damaged, or a website glitch causes a double charge, a dispute is pretty much guaranteed.

Other common service-related issues include:

- Unclear Return Policies: If a customer can't figure out how to send something back, they might just file a chargeback as a shortcut.

- Delayed Shipping: When an order takes way longer to arrive than you promised, customers lose patience. Fast.

- Poor Customer Support: A slow or unhelpful response can turn a simple question into a formal dispute.

Fixing these internal processes is one of the most powerful ways to cut down on disputes and chargebacks right at the source.

Criminal Fraud

This is what most people picture when they hear the word "fraud." Criminal fraud is when a thief gets their hands on stolen credit card information and uses it to buy something from your store. The real cardholder eventually spots the unauthorized charge and, of course, reports it to their bank.

Because the purchase was made without the cardholder's consent, the bank will almost always side with them. That leaves you with a chargeback, the loss of whatever you shipped, and a hit to your bottom line.

Visa reports that a staggering 75% of all chargebacks are not related to true criminal fraud but fall into other categories. This means that while protecting against stolen cards is important, it's only one piece of a much larger puzzle.

This kind of chargeback is a direct attack on your business. It requires good fraud detection tools that can flag suspicious activity, like mismatched billing and shipping addresses or a strange number of rapid-fire orders from the same place.

The Rise of Friendly Fraud

The last and, frankly, most complicated category is friendly fraud. This is when a legitimate customer makes a purchase with their own card but disputes the charge later on. Unlike criminal fraud, there's no stolen card involved here.

The reasons for friendly fraud can be accidental or totally intentional. A customer might genuinely forget about a recurring subscription payment or not recognize your business name on their credit card statement. In other cases, a family member might have used their card without asking first.

But friendly fraud can also be deliberate. Some people know how to game the system, using chargebacks as a way to get products or services for free. Because these disputes look like legitimate transactions on the surface, they can be incredibly tough to fight. It's a growing headache for merchants, and you can learn more about the nuances and how to fight back in our detailed guide on what is friendly fraud.

Pinpointing the exact cause of a chargeback is crucial. Was it a simple shipping mistake, a stolen credit card, or a customer who forgot they signed up for your service? Each scenario requires a different response and a different long-term prevention strategy. By understanding these three core drivers, you can start building a smarter, more targeted approach to protecting your revenue.

How the Chargeback Process Actually Works

When a customer kicks off a dispute, it sets in motion a formal, multi-step process that can feel like a maze. Knowing the map is the first step to getting through it successfully. This isn't just a single event—it's a journey with very specific stages, strict deadlines, and several key players.

It all begins when a cardholder calls their issuing bank (the bank that gave them their credit card) about a problem. It could be an unrecognized charge on their statement, an item that never showed up, or a product that was nothing like the description. This single complaint is the spark that lights the chargeback fire.

Once the customer files the complaint, their bank looks it over. If the claim seems valid under the card network's rules, the bank officially starts a chargeback. At this point, the funds are provisionally pulled from your merchant account and handed back to the customer while everything gets sorted out.

The Key Stages of a Chargeback Lifecycle

From here, the process is highly structured. You, the customer, the issuing bank, and your bank (the acquiring bank) all have a part to play. If you miss a deadline at any point, it often means an automatic loss, so staying on top of the timeline is absolutely critical.

This whole sequence is governed by strict rules set by card networks like Visa and Mastercard. For a deeper dive into one network's specific rulebook, check out our guide on the Visa chargeback process.

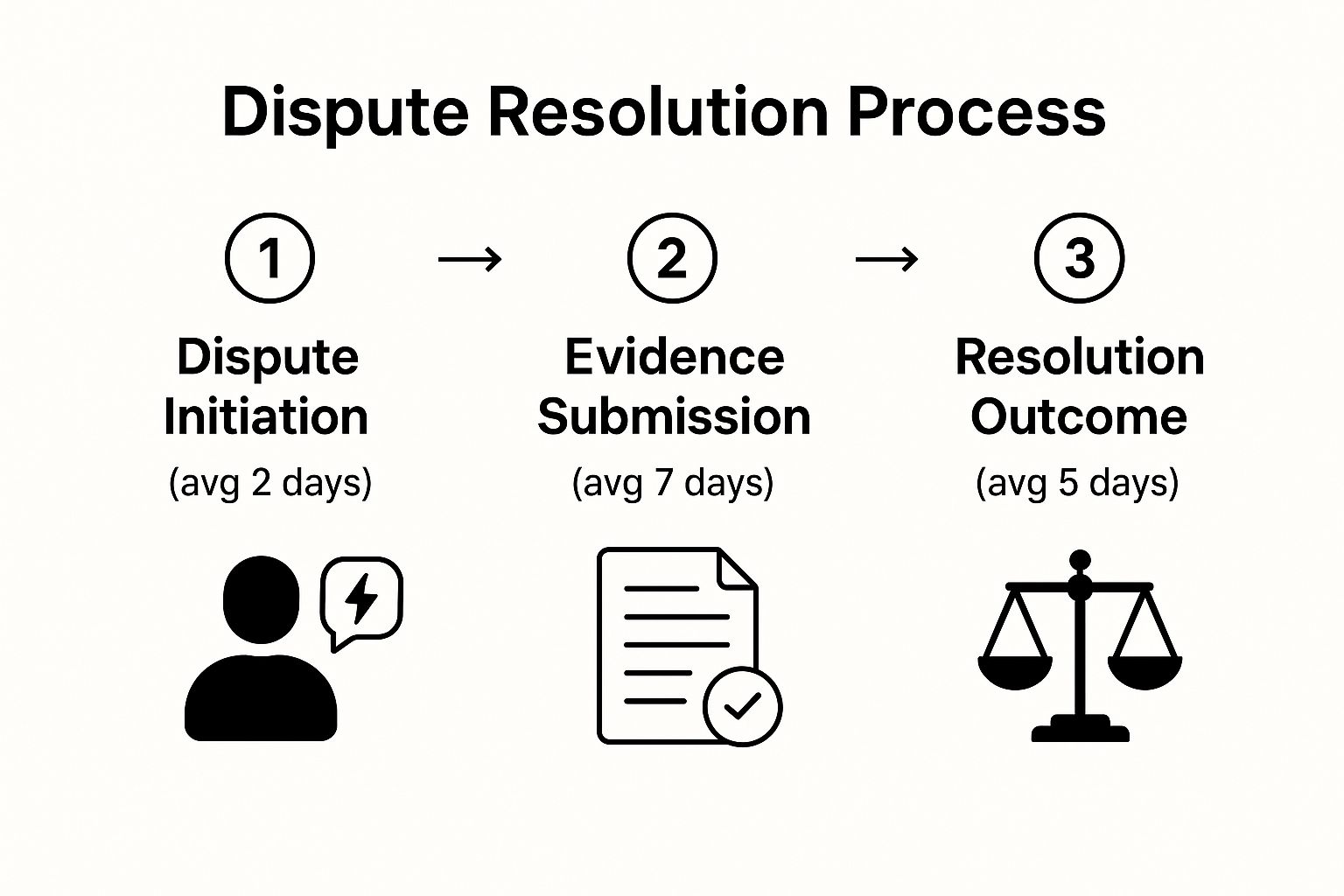

The entire dispute resolution process can be broken down into three main phases, each with its own average timeline.

As you can see, the full cycle can take weeks or even months, which really drives home why quick, organized action from merchants is so important.

Representment: Your Chance to Fight Back

After the funds are reversed, you'll get a chargeback notification. This is your cue to step in and present your side of the story in a process called representment. You have a limited window—usually 7 to 45 days, depending on the reason code and card network—to submit compelling evidence proving the charge was legitimate.

Think of this evidence package as your case file. It has to be solid enough to convince the issuing bank to overturn its initial decision.

Your evidence might include things like:

- Proof of Delivery: A shipping confirmation with a tracking number showing the item was delivered to the customer's address.

- Customer Communication: Emails, chat logs, or support tickets showing you communicated with the customer about their order.

- Terms of Service: A screenshot proving the customer agreed to your terms and conditions, especially your refund policy.

Once you submit your evidence, the issuing bank reviews both sides of the story. They act as the judge and jury, making a final decision based on the evidence provided and the specific rules for that chargeback reason.

And these disputes are becoming more common every year. Global chargeback volumes are projected to hit 324 million within three years, a huge jump from $33.8 billion to an expected $41.7 billion. This trend is largely fueled by the explosion of e-commerce and how easy it is for customers to initiate disputes and chargebacks right from their online banking app.

The Final Decision and Arbitration

If the bank rules in your favor, the funds are put back into your account, and the case is closed. But if they side with the customer, the chargeback stands. You're out the revenue and the product.

In some rare cases, if you still feel the decision was wrong, you can escalate the issue to arbitration. This is a final, binding process where the card network itself (like Visa or Mastercard) makes the ultimate call. Be warned, though—arbitration is expensive and risky. If you lose, you’ll be on the hook for hefty fees, so it's a step that should only be considered as a last resort.

Proven Strategies to Prevent Chargebacks

The best way to win the fight against disputes and chargebacks is to stop them before they even start. You can't prevent every single one, but a solid, proactive defense will dramatically lower your risk and protect your hard-earned revenue.

It's all about creating a clear, trustworthy experience for your customers, from the second they land on your site to long after their package arrives. Think of it like building a fortress. Each strategy you put in place is another layer of defense, making it tougher for issues to slip through the cracks and morph into costly chargebacks. The good news? Many of these are simple, common-sense tweaks to your daily operations.

Build a Foundation of Clarity and Trust

The root of so many chargebacks isn't malicious—it's just plain confusion. When customers are surprised or confused, their first instinct is often to call their bank. Your main goal is to stamp out that confusion by being as transparent as humanly possible.

This starts with crystal-clear communication across the board. Your product descriptions need to be detailed and accurate, backed up by high-quality photos from multiple angles. Misrepresenting a product, even by accident, is a one-way ticket to a "Product Not as Described" chargeback.

Next, get your policies in order:

- Easy-to-Find Return Policy: Don't bury your return policy in the footer where no one can find it. Make it obvious and easy to understand. A customer who knows how to get a refund directly from you is far less likely to file a chargeback.

- Clear Shipping Timelines: Give realistic delivery estimates and keep customers in the loop if there are delays. A quick email heads-off an "Item Not Received" dispute before it happens.

- Recognizable Billing Descriptor: Check what name shows up on your customer's credit card statement. A vague or unfamiliar descriptor is a top cause of friendly fraud simply because people don’t recognize the purchase.

Sharpen Your Technical Defenses

Beyond clear communication, you need strong technical tools working behind the scenes to filter out sketchy transactions. These automated systems are your first line of defense against criminals using stolen card info. For merchants, implementing robust fraud prevention measures is non-negotiable. You can explore effective strategies to prevent ecommerce fraud, which is a primary cause of chargebacks.

Key technical tools include:

- Address Verification Service (AVS): This tool checks if the billing address entered by the customer matches the address on file with their bank. It's a simple but effective check.

- Card Verification Value (CVV): Always require the three- or four-digit security code on the card. This simple step helps prove the customer has the physical card in their hands.

- 3D Secure Authentication: Technologies like Verified by Visa and Mastercard SecureCode add an extra security step, requiring the customer to enter a password or a one-time code sent to their phone to finish the purchase.

By putting these security checks in place, you create friction for fraudsters while providing a safer checkout experience for legitimate customers. This is your digital gatekeeper, stopping bad actors before they can even get through the door.

Provide Outstanding Customer Service

Never, ever underestimate the power of great customer service. A responsive and helpful support team can de-escalate potential problems long before they become formal disputes and chargebacks. Make it ridiculously easy for customers to contact you with questions or concerns.

When a customer does reach out, respond quickly and with empathy. Even if you can't give them exactly what they want, a fast, respectful reply shows you're taking them seriously. This builds goodwill and makes them more willing to work with you for a solution. A complete strategy also means using smart tools to handle these issues. You can check out a complete guide to automated chargeback and dispute management using AI to see how technology can lighten the load.

Common Questions About Disputes and Chargebacks

Even with the best prevention plan in place, you're going to have questions about disputes and chargebacks. It just comes with the territory. When those situations pop up, it’s easy to feel a little lost, but having the right answers helps you act with confidence instead of just reacting.

This section tackles the most common questions we hear from merchants. Think of it as your go-to FAQ for those tricky "what-if" scenarios that can put a dent in your revenue and your day.

Getting a handle on these answers will help you make smarter decisions, whether you're staring down a confusing customer claim or just trying to get a better grip on your business's risk.

Can I Get a Chargeback After Issuing a Refund?

Yes, you absolutely can. It’s a frustrating scenario often called a "double refund," and unfortunately, it’s more common than you’d think.

Usually, it happens for one of two reasons. A customer gets antsy waiting for the refund to hit their account and decides to call their bank anyway. Or, they simply don’t recognize the credit on their statement when it finally does show up.

This is where crystal-clear communication becomes your best defense. Always tell customers your refund timeline upfront (e.g., "You can expect to see the refund on your statement in 5-10 business days"). Even better, send a confirmation email the second you process it. That simple step creates a paper trail, sets the right expectations, and dramatically lowers the odds of a premature chargeback.

What Is a Chargeback Ratio and Why Does It Matter?

Your chargeback ratio is one of the single most important health metrics for your business, especially in the eyes of payment processors like Visa and Mastercard. It’s the simple formula they use to decide how risky you are to work with.

It's calculated by taking the number of chargebacks you get in a month and dividing it by your total transactions for that same month.

Each card network has a threshold they expect merchants to stay under, which is typically around 1%. The moment your ratio starts creeping above that magic number, you get flagged. This can trigger some serious consequences, like higher processing fees, being forced into costly monitoring programs, or even having your merchant account shut down completely. Keeping this number low isn’t just good practice—it’s critical for survival.

Is It Always Worth It to Fight a Chargeback?

Fighting every single chargeback that comes your way isn't always the smartest play. It really needs to be a strategic decision, weighing what you stand to gain against the time and resources you'll have to put in.

Think of it as a quick cost-benefit analysis. For a low-value order where your evidence is just so-so, the time your team spends building a case might be worth more than the sale itself. In those situations, it can be better to just accept the loss and move on.

On the other hand, for a high-value sale where you have rock-solid proof—like a delivery confirmation, customer emails, or a signed contract—it's almost always worth fighting. It's also crucial to fight obvious cases of friendly fraud to show processors you're actively defending your business against illegitimate disputes and chargebacks.

Should I Block a Customer Who Filed a Chargeback?

Blocking a customer after a chargeback is tempting, but it’s a nuanced decision. A blanket "one strike and you're out" policy might save you from repeat offenders, but it could also mean losing out on future sales from a good customer who just had a single, legitimate issue.

A much better approach is to look at the reason behind the chargeback.

- Stolen Card Fraud: If the chargeback was due to a stolen credit card, then yes, you should absolutely block that card and any associated user info from making future purchases.

- Service Issues: If the customer filed a chargeback because of a genuine mistake on your end, blocking them would just make a bad situation worse.

- Friendly Fraud: For customers who are clearly gaming the system, blocking them is a smart move. Research shows that nearly 15% of consumers who file one chargeback will file five or more annually, so you’re just protecting yourself from future headaches.

How Can AI Tools Help With Disputes?

Trying to manage disputes and chargebacks by hand is a recipe for frustration. It's slow, mind-numbingly tedious, and full of opportunities for human error. This is where AI-powered tools are a total game-changer.

Instead of your team wasting hours digging through order histories and shipping logs, an AI system automates the whole process. It can instantly read the chargeback reason code, pull together all the necessary evidence from your different platforms (sales, shipping, CRM), and build a professional, compliant response for you.

This kind of automation does way more than just save a ton of time. It significantly boosts your win rate by making sure every response is accurate, complete, and submitted long before the deadline hits. AI basically acts as your 24/7 chargeback specialist, working in the background to protect your revenue so you can get back to growing your business.

Stop letting chargebacks eat into your profits. ChargePay uses AI to automate the entire dispute process, recovering up to 80% of your lost revenue without you lifting a finger. See how much you can reclaim by visiting https://www.chargepay.ai today.

.svg)

.svg)

.svg)

.svg)