Ever wondered how a hotel or gas station seems to know your card is good before you've even checked out or finished pumping gas? The magic behind that is a credit card pre-authorization hold.

This isn't a charge. Think of it more like a temporary "hold" or a reservation placed on a customer's funds. The money doesn't actually leave their account, but it's set aside to make sure they have enough available credit or cash to cover the eventual purchase.

What a Pre-Authorization Hold Means for Your Business

Let’s stick with the hotel example. A guest checks in, you swipe their card, and you place a hold for the cost of their room plus a little extra for potential incidentals. That money isn't transferred to you yet. All that's happened is that the guest's available credit has been temporarily reduced, guaranteeing those funds will be there when they check out and you're ready to settle the final bill.

Why This Matters for Merchants

This simple process is a game-changer for any business that deals with variable final costs. By confirming the customer has the funds upfront, you dramatically cut down on the risk of painful declined payments and the headaches of dealing with chargebacks later. It’s your way of making sure the customer can cover the tab before you provide the service or hand over the product.

A pre-authorization is essentially a merchant’s way of asking the bank, "Is this customer good for the money?" before committing to the sale. It’s a vital step in secure payment processing.

In short, a pre-auth is a standard industry practice where you temporarily reserve a piece of a cardholder's credit limit. While this hold reduces their available credit, it doesn't immediately pull the funds, which protects both you and your customer.

This two-step system—authorize first, capture later—is a key part of the entire lifecycle of credit card transactions. It verifies funds without immediately charging the customer.

For businesses like car rentals, restaurants with tabs, or hotels, this is just standard operating procedure. It provides a financial safety net, making sure that when it's time to capture the final amount, the payment will go through without a hitch.

How a Transaction Hold Actually Works

To really get a handle on credit card pre-authorization holds, you have to follow the money through its entire lifecycle. It’s less of a single event and more like a four-part story: Authorization, Capture, Void, and Refund. Each stage plays a big part in making sure transactions are both secure and accurate.

Let's walk through a super common scenario: opening a bar tab at a restaurant. The moment you hand over your card, the process kicks off.

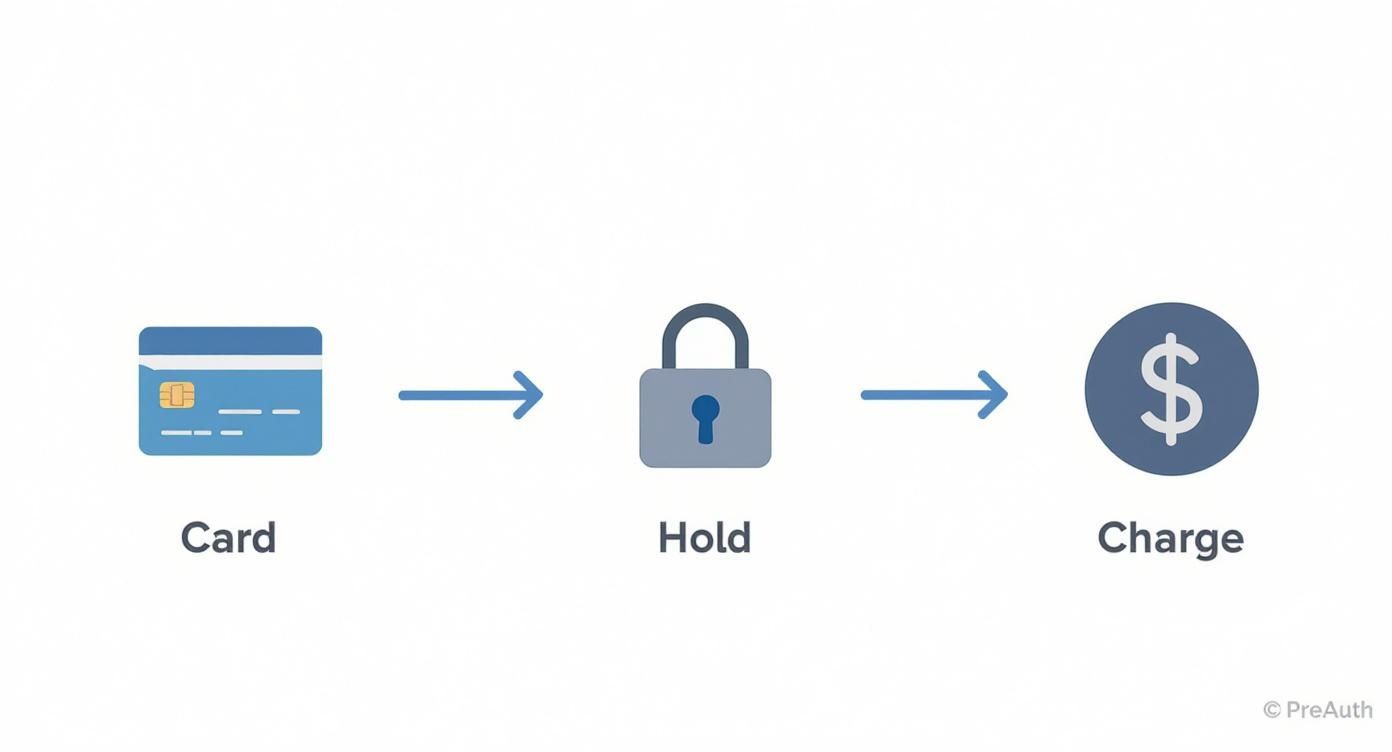

This visual breaks down the simple flow from placing the initial hold to finalizing the charge.

As you can see, the hold is that crucial middle step. It locks in the funds before they’re officially pulled from the customer’s account and sent to yours.

Authorization: The Initial Handshake

The second the bartender swipes your card, an authorization request zips off. This message travels from the payment terminal, through the card network (like Visa or Mastercard), and lands at the customer’s issuing bank. The bank quickly checks if the card is legit and has enough available credit.

If everything looks good, the bank approves the request and places a temporary hold—the pre-authorization—on a set amount, say $50. This money hasn't actually moved anywhere; it's just been earmarked for your business.

This first step is really a quick conversation between your bank (the acquirer) and the customer's bank (the issuer). Grasping the difference between an acquirer vs issuer is pretty key to understanding how this whole communication chain works.

Capture: Finalizing the Payment

At the end of the night, after a few drinks and a generous tip, the final bill comes to $65. When the bartender closes out the tab, they don't start a brand new transaction. Instead, they capture the funds from that original authorization.

This "capture" message tells the customer's bank to turn the temporary hold into a final, settled charge for the real amount. The initial $50 hold vanishes, and the final $65 charge is officially posted, starting its journey to your bank account.

Void and Refund: Fixing Mistakes

But what happens when things don't go as planned?

Void: Let's say a customer opens a tab but has to leave before ordering anything. Since no money has actually been captured, you can simply void the authorization. This cancels the hold on their card, freeing up their funds almost right away. No formal charge ever appears on their statement.

Refund: Now, imagine you accidentally charged them $75 instead of the correct $65. Because the funds have already been captured, you can't just void it. You have to issue a refund, which is a totally separate transaction that sends the money back to the customer's account.

To make these differences crystal clear, here’s a quick breakdown of how these stages stack up against each other.

Comparing Authorization, Capture, and Void

This table gives a side-by-side look at the key stages in a pre-authorization lifecycle, showing the purpose and impact of each step.

Each of these actions serves a distinct purpose, either moving a sale forward or correcting it when needed. Knowing which one to use and when is fundamental to smooth payment operations and good customer service.

How Pre-Authorization Holds Affect Your Business

A pre-authorization hold isn't just a behind-the-scenes step in a transaction; it has real, tangible effects on both your customers and your back-office operations. On one hand, it’s a vital tool for locking in a payment and keeping fraud at bay. On the other, it introduces a delicate balancing act you have to get just right.

For your customer, a pre-auth hold instantly ties up a portion of their available credit or debit card balance. Even though you haven't actually taken any money, those funds are temporarily frozen. This can easily lead to confusion and frustration, especially if the hold amount is higher than they expected or, worse, causes another purchase to be declined.

This is a daily reality in industries where the final total isn’t known upfront. Think about restaurants that need to account for a tip or hotels that hold a deposit for potential incidentals. While it protects the business from taking a loss, it can create friction when the final charge is much lower than the hold, leaving a customer's funds locked up longer than necessary.

Merchant-Side Impacts on Cash Flow and Operations

While holds are great for securing revenue, they also directly influence the financial rhythm of your business. The funds from an authorized transaction don't actually hit your account until you formally "capture" them. This final step can take a few days to fully settle, creating a temporary but noticeable gap in your cash flow.

On top of that, managing these holds adds another task to your team's plate. You have to keep a close eye on all your open authorizations to make sure they're captured before they expire, which usually happens within 3-7 days.

An uncaptured hold is a missed sale. If you forget to finalize the transaction within the authorization window, the hold expires, and you lose the guaranteed funds.

This creates a few key operational challenges:

- Reconciliation: Your team needs a rock-solid process for matching every authorization to its final capture. Without it, you're leaving money on the table.

- Customer Service: Your staff needs to be ready to explain why a customer sees a "pending" charge on their statement or why a hold is still there after they've paid.

- Dispute Risk: Mismanaged holds—like accidental double authorizations or trying to capture an expired hold—are a fast track to customer disputes and costly chargebacks.

Handling pre-authorizations correctly is a crucial piece of your overall chargeback risk management strategy. When you get it right, you protect your business and keep your customers happy. But when it goes wrong, it can create financial headaches and chip away at the trust you've worked so hard to build.

Solving Common Problems with Authorization Holds

While a credit card pre-authorization is a fantastic tool for securing payments, it’s not a perfect system. Glitches and simple human errors can create frustrating situations for both you and your customers. Knowing how to troubleshoot these common hiccups is key to keeping your operations smooth and your customers happy.

Most issues fall into a few common buckets: holds that stick around too long, accidental duplicates, or captures that just won't go through. Let’s break down how to handle each one.

The Problem of Stale or Expired Holds

One of the most frequent complaints comes from a "stale hold"—an authorization that lingers on a customer's account long after a transaction is complete or canceled. This usually happens when a hold isn't properly voided or when the final capture amount is different from the initial authorization, leaving the original hold in limbo.

Similarly, an expired hold occurs when you fail to capture the funds within the 3-7 day window provided by the card networks. Once it expires, the hold is released, and your guarantee of payment vanishes with it.

To fix these issues, your first step is always to check your payment terminal or gateway.

- For Stale Holds: Immediately find the original authorization and execute a void. This sends a direct message to the customer’s bank to release the funds. If you can't, contact your payment processor for help.

- For Expired Holds: You've lost the guarantee. You will need to run a new transaction, which means you’ll need the customer's card details again. Proactive communication is essential here to explain the situation.

Handling Accidental Duplicate Holds

It happens more often than you'd think. A terminal glitch or a simple mistake can result in two or more holds for a single transaction, unnecessarily tying up a large chunk of a customer’s available credit. This is a bad experience that can quickly lead to a declined card and an unhappy customer.

The moment you spot a duplicate hold, act fast. The longer it sits there, the more likely it is to cause a problem for your customer, potentially leading to a formal dispute.

The solution is straightforward: identify the extra authorization and void it immediately. Reassure the customer that you've corrected the error and that their funds should be released shortly, usually within 24 hours.

When a Valid Authorization Fails to Capture

This is perhaps the most puzzling issue. You have a valid authorization code, the hold is active, but when you try to capture the funds, the transaction fails. This can be caused by a few different things, from a system timeout to a communication breakdown between your processor and the issuing bank.

Here’s a step-by-step plan:

- Wait and Retry: Sometimes, it's a temporary network issue. Wait a few minutes and try to capture the payment again.

- Contact Your Processor: If it fails a second time, don't keep trying. Contact your payment processor’s support team with the transaction details and authorization code. They can investigate the root cause.

- Communicate with the Customer: Let them know there’s a technical delay. Transparency prevents them from thinking something is wrong with their card.

Mistakes with holds can sometimes escalate into formal disputes. To better understand the different stages of a payment dispute, you can learn more about the differences between retrieval requests vs chargebacks in our detailed guide.

Best Practices for Managing Pre Authorization Holds

When it comes to handling a credit card pre authorization hold, the best defense is a good offense. Being proactive instead of reactive can sidestep most of the common headaches before they even begin, making life easier for both you and your customers.

It all starts with clear communication. Let's be honest, customers get nervous when they see a pending charge they don't fully understand. You can get ahead of that anxiety by simply being upfront about your hold policy from the get-go.

Communicate Clearly and Proactively

A quick heads-up at the point of sale can work wonders. Just letting a customer know you’re placing a temporary hold—and explaining that it’s not the final charge—makes a world of difference.

A few tips to get this right:

- Train Your Staff: Make sure every team member can explain what a pre-authorization is in plain English. No jargon.

- Use Simple Signage: A small notice at the checkout counter or on your website's payment page can do the heavy lifting for you.

- Be Specific When You Can: Tell them the exact amount if possible and why. For example, "We'll be holding the room rate plus $50 for any incidentals."

This kind of transparency builds trust and cuts down on those panicked phone calls and potential disputes down the line.

Act Within the Authorization Window

That pre-authorization hold isn't going to stick around forever; it has a shelf life. Most holds last somewhere between 3 to 7 days, though this can vary by card network. If you don’t capture the funds within that window, the hold drops off, and your payment guarantee vanishes with it.

Always aim to capture funds well before the authorization expires. Waiting until the last minute is just asking for trouble—a technical glitch or simple delay could cause you to miss the window and lose the sale.

Making it a daily habit to capture all open authorizations is a smart operational move. It secures your revenue quickly and keeps your cash flow healthy and predictable.

Embrace Modern Payment Technology

Trying to track every single hold manually is a recipe for disaster. It's tedious, time-consuming, and just plain easy to mess up. This is where modern payment tech really shines.

Picking the best payment processing solutions isn't just a good idea; it's a vital best practice for handling pre-auths efficiently. These systems can automate a huge chunk of the reconciliation process, freeing you from the manual grind.

Good tech helps both sides. For you, it means better security. For your customer, it means a smoother experience. The right systems reduce manual errors, speed up reconciliation, and ultimately, strengthen your bottom line. To take it a step further, you might even consider a payment orchestration platform to tie all your payment processes together seamlessly.

Frequently Asked Questions About Pre Auth Holds

Even after you get the hang of pre-auths, a few specific questions always seem to pop up. We get it. We've put together some quick, clear answers to the most common things we hear from merchants, clearing up any lingering confusion about how these holds actually work in the wild.

Let's dive in and get you the details you need to handle any situation with confidence.

How Long Does a Pre Authorization Hold Last?

A typical credit card pre-auth hold sticks around for 3 to 7 days. The exact timing, though, really depends on the card network (like Visa or Mastercard) and the customer's own bank. For some businesses, like hotels or car rentals, holds can last much longer—sometimes for the entire rental period, which could be up to 30 days.

It's absolutely critical that you capture the payment while that authorization is still active. If you wait too long, the hold expires, the funds get released back to the customer, and you've lost your guaranteed payment.

What's the Difference Between a Pre-Auth and a Pending Charge?

For the customer staring at their banking app, a pre-auth and a pending charge look almost identical. Both show up as temporary transactions that tie up part of their available balance. But behind the scenes, they serve very different purposes.

- A pre-authorization hold is just a temporary freeze on funds. Its only job is to check if the card is valid and if the customer can cover a potential future payment. It's step one.

- A pending charge is a real transaction that's already in the pipeline. It’s been submitted for settlement and is on its way to becoming a permanent, posted charge.

Think of it this way: the pre-auth is the "reservation" you make on the funds, while the pending charge is the actual bill waiting to be processed.

Can a Pre Authorization Hold Be for the Wrong Amount?

Yes, and this is a huge source of customer confusion. A pre-auth hold is often just an estimate, which can be higher or lower than the final bill. For example, a bar might authorize $1 just to open a tab, while a hotel might hold the cost of a three-night stay plus an extra 20% to cover any minibar raids or other incidentals.

When you finally capture the real amount, the original hold should disappear and be replaced by the final charge. But if your initial hold was much higher than the final bill, it can take a few business days for the bank to release those leftover funds. This can really frustrate customers, so being upfront about why the hold amount might be different is key.

What Happens if a Pre-Authorization Is Never Captured?

If you never capture the funds, the hold simply expires. The temporary freeze on the customer's account is automatically lifted by their bank, and their available balance goes back to normal. No money ever actually moves.

For a merchant, an uncaptured pre-authorization is a lost sale. You delivered a product or service but dropped the ball on collecting the payment while it was guaranteed.

This is exactly why diligent reconciliation is a non-negotiable part of running your business. Regularly checking for open authorizations and capturing them ensures you get paid for your work and keeps your cash flow healthy. It's the only way to prevent revenue from slipping through the cracks due to a simple oversight.

Managing payment holds and the disputes they can spark is a critical part of running a successful business. If chargebacks are cutting into your profits, ChargePay offers a hands-free solution. Our AI-powered system automates the entire dispute process, helping you recover lost revenue without lifting a finger. See how much you could reclaim by visiting https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)