A debit card chargeback is a powerful way to get your money back when a purchase goes wrong. It essentially reverses a transaction, pulling funds from a merchant’s account and returning them to yours.

Think of it as an “undo” button for your bank account, but with a formal process attached. It's managed by your bank to protect you from things like fraud or unresolved problems with sellers.

What Is a Debit Card Chargeback

A debit card chargeback is basically a safety net for money you’ve already spent. Unlike a credit card dispute, where you're technically arguing over the bank's money until you pay the bill, a debit card chargeback deals with funds that have already left your checking account. That difference often makes the whole situation feel a lot more urgent.

When you file a chargeback, you're doing more than just asking for a refund. You’re officially telling your bank that a transaction was illegitimate for a specific, valid reason. Maybe the charge was fraudulent, the product you ordered never showed up, or what you received wasn't what was advertised.

This action kicks off a formal investigation that involves a few key players:

- You (The Cardholder): You get the ball rolling by filing the dispute.

- Your Bank (The Issuing Bank): They review your claim and act as your representative.

- The Business (The Merchant): They get a chance to prove the charge was legitimate.

- The Merchant's Bank (The Acquiring Bank): They handle communication with the merchant.

The Basic Chargeback Journey

The whole thing is really a structured conversation between everyone involved, with the banks acting as mediators. Your bank will usually give you a temporary credit while they investigate, which can feel like an instant win.

But hold on—it's not over yet. The merchant has every right to challenge your claim with their own evidence. If they can provide compelling proof—like a shipping confirmation with your signature—that temporary credit can be taken right back.

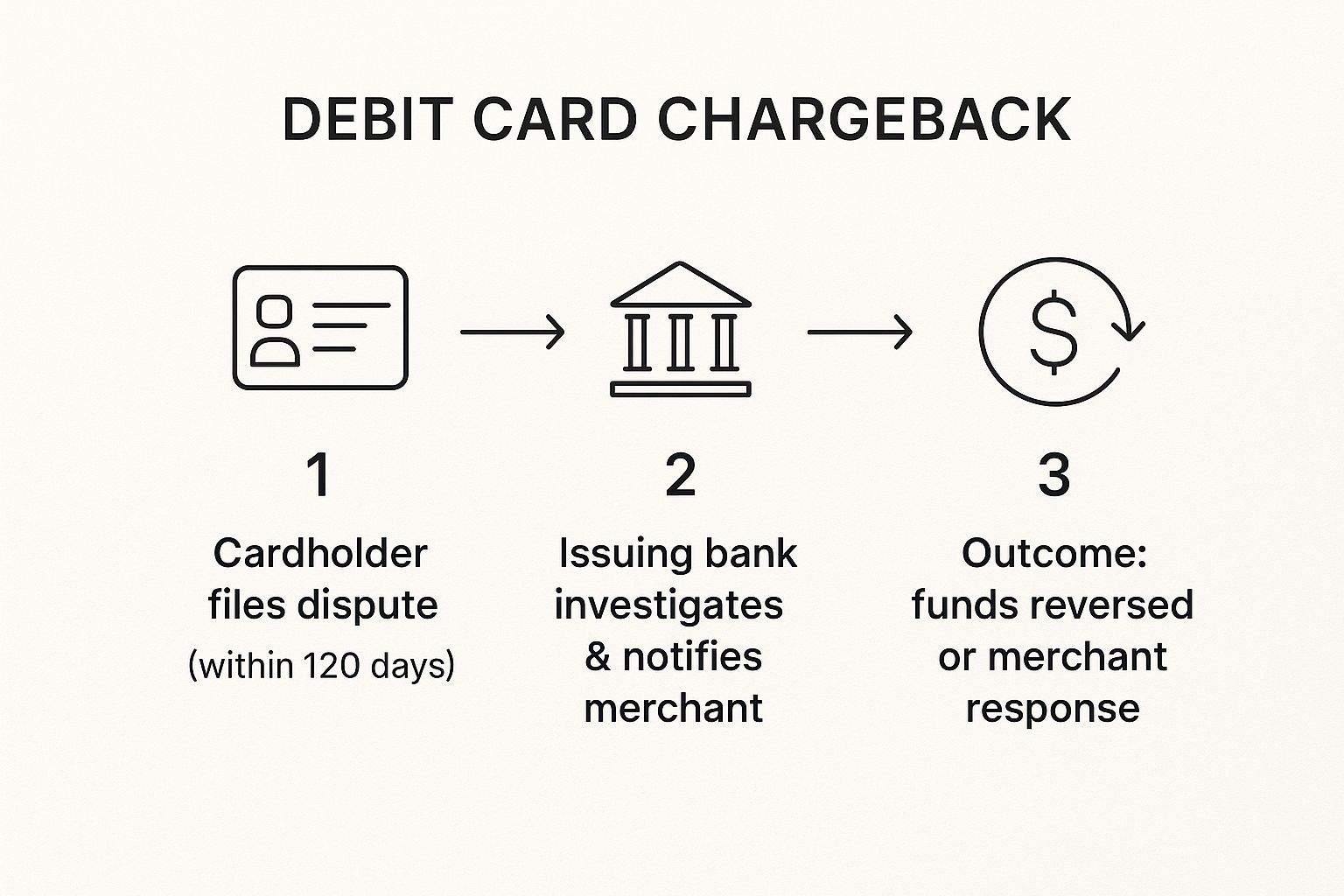

This infographic breaks down the essential steps in a typical debit card chargeback.

As you can see, the process starts with you and really hinges on the bank's investigation before a final decision is made. To dive deeper, you can learn more about how a chargeback for a debit card works in our detailed guide. Getting a handle on this flow is the first step to successfully navigating any dispute.

Valid Reasons to File a Chargeback

Let's get one thing straight: a debit card chargeback isn't for every purchase that leaves you feeling a bit disappointed. It’s not a tool for buyer's remorse, and you can’t use it just because you changed your mind.

Think of it less like a super-powered refund button and more like a formal dispute process. It’s designed to protect you when a transaction has gone seriously wrong and you’ve hit a dead end trying to solve it with the business directly. Your bank needs a legitimate, recognized reason to step in and claw back your money. Let's dig into what those reasons actually are.

Fraudulent or Unauthorized Transactions

This is the big one—the most common and clear-cut reason for a chargeback. You're scrolling through your bank statement and spot a charge from a company you’ve never heard of, for a purchase you know you didn’t make. That’s a massive red flag for fraud.

Maybe your card details got swiped in a data breach, or a skimmer at an ATM copied your information. These kinds of unauthorized transactions are exactly what the chargeback system was built to combat.

Key Takeaway: When you claim fraud, your bank needs to be sure the charge was truly unauthorized. You’ll have to confirm you didn't just lend your card to a family member and that the transaction is a complete mystery to you.

Products or Services Not Received

You paid for something, but it simply never showed up. This is another classic scenario where a debit card chargeback comes into play. You ordered a new couch online, the delivery date came and went, and now the company is giving you the silent treatment.

Before you file, you have to prove you tried to sort it out with the merchant first. Banks want to see that you made a genuine effort to get the product you paid for or get your money back.

- What you’ll need: Keep everything. Your order confirmation, any shipping info (or the lack of it), and a record of all your attempts to contact the seller—emails, chat logs, you name it. This paper trail proves you paid up and tried to fix the problem yourself.

Item Not as Described or Defective

Sometimes the package arrives, but what’s inside is a far cry from what you ordered. You paid for a high-end leather jacket and got a cheap plastic knockoff. Or maybe that brand-new laptop you ordered arrived with a cracked screen and refuses to power on.

This covers situations where the item is significantly different from its description or is just plain broken out of the box. Just like with non-delivery, you have to contact the merchant first to try and arrange a return or replacement. If they won’t play ball, a chargeback is your next move.

- What you’ll need: Evidence is king here. Snap clear photos or take a video of the wrong or damaged item. It’s also smart to grab screenshots of the original product page to show exactly what you were supposed to receive.

How to Navigate the Chargeback Process

When you’re absolutely sure a charge on your account is wrong, it’s time to take action. Diving into the debit card chargeback process might feel a bit intimidating, but it's really just a structured path designed to protect you.

Think of it like building a case. The more organized and proactive you are from the start, the better your odds are of getting your money back.

Interestingly, the journey doesn't start with your bank. The very first step—one that many banks require before they’ll even look at your dispute—is to talk to the merchant directly.

Step 1: Contact the Merchant First

Before you escalate things, always give the business a fair shot at making it right. A quick phone call or a simple email can often clear up a simple misunderstanding, like a shipment that’s just running late or an accidental billing error.

Make sure you document every single interaction. Jot down who you spoke with, the date, and what was said. This isn’t just busywork.

This step is powerful for two reasons. First, it's the fastest way to get a refund or fix the problem without the formal hassle of a dispute. Second, if the merchant is unhelpful, that communication log becomes your star evidence, proving to your bank that you tried to resolve it in good faith.

Step 2: File the Dispute with Your Bank

If talking to the merchant leads to a dead end, now it’s time to bring in your bank. You can usually kick off the official dispute process over the phone, through your bank's online portal, or by walking into a branch. Be ready to give them all the details.

Your bank will need some key info to get the ball rolling:

- Transaction Details: Have the exact date, the precise amount, and the merchant’s name ready.

- Reason for the Dispute: Be crystal clear about why you're filing. Is it fraud? Did the item never show up? Was it damaged?

- Supporting Evidence: This is where your documentation shines. Hand over order confirmations, photos of the broken item, and the notes from your conversations with the merchant.

Timing is everything here. Under the Electronic Fund Transfer Act (EFTA), you generally have 60 days from the statement date to report any unauthorized transactions. For other problems, card network rules might give you up to 120 days, but don't wait. Acting fast is always the best strategy.

It's a common myth that a chargeback is a get-out-of-jail-free card for a purchase you just regret. Banks investigate these claims seriously. Using the system for reasons that aren't valid is often called "friendly fraud" and can have real consequences. To keep the system fair for everyone, it’s vital to understand and use good strategies for chargeback fraud prevention.

Step 3: The Investigation and Outcome

Once your dispute is filed, the bank takes the reins. The first thing they'll likely do is issue a provisional credit to your account for the disputed amount. Hold on—this isn't a final win. It’s a temporary refund while they dig into the details.

Behind the scenes, your bank reaches out to the merchant's bank, which then gets in touch with the merchant. The business gets a chance to tell its side of the story and provide its own evidence, like a delivery confirmation or a signed receipt. This back-and-forth can take anywhere from a few weeks to a couple of months.

Eventually, you'll get the final verdict. If the bank sides with you, that provisional credit becomes permanent. If they rule in favor of the merchant, the credit gets reversed, and the money is pulled back out of your account.

Your Consumer Rights and Protections

When you kick off a debit card chargeback, you’re not just asking for a favor—you're exercising a legal right. Thankfully, specific consumer protection laws are in place to give you a fair shot when a transaction goes sideways, making sure you don't get left in the lurch.

The big one here is the Electronic Fund Transfer Act (EFTA). Think of it as the official rulebook that dictates how your bank must handle disputes for electronic payments, and yes, that includes every time you swipe your debit card.

Understanding Your Legal Backing

The EFTA is what puts real power behind your claim. It sets clear deadlines and, crucially, limits how much you can lose, especially with unauthorized charges. For instance, if you report a lost card or a bogus transaction within two business days, your maximum liability is capped at just $50. This is a massive safety net, but it only works if you act fast.

This legal framework is what gives the whole chargeback process its teeth. It’s not just a suggestion; it legally requires your bank to investigate your claim on time. To get into the nitty-gritty, you can explore the full extent of your chargeback rights in our detailed guide.

A Quick Word of Caution: Just because you have this power doesn't mean it should be used lightly. The chargeback system is there for genuine disputes, not as a tool for buyer's remorse or to score a free product. Abusing it can backfire.

The Problem with Friendly Fraud

Filing a chargeback without a legitimate reason has a name: "friendly fraud." This is what happens when a customer disputes a valid charge, maybe because they're confused, frustrated with a merchant's return policy, or in some cases, doing it on purpose.

It might not sound like a big deal, but friendly fraud is a huge headache for businesses. It costs merchants the sale, plus they get hit with hefty chargeback fees and lose time dealing with the paperwork. Over time, those costs get passed on to everyone in the form of higher prices.

Your Responsibilities as a Cardholder

To make sure the chargeback process works as intended, you have a few responsibilities. Following these guidelines not only makes your own case stronger but also helps keep the system fair for everyone.

- Communicate First: Before you even think about a chargeback, reach out to the merchant directly. Banks almost always want to see that you’ve made a good-faith effort to resolve the problem first.

- Keep Meticulous Records: Save everything. Emails, receipts, tracking numbers, photos of the item—all of it. This evidence is the bedrock of a successful claim.

- Act Honestly: Only file a chargeback for a valid reason, like actual fraud, an item that never showed up, or a product that arrived broken. The process is a shield, not a sword.

As online shopping continues to boom, these protections are more important than ever. In fact, global debit card chargebacks are projected to climb from 261 million transactions in 2025 to 324 million by 2028—that’s a 24% jump. This surge is fueled by digital commerce, which now accounts for about 63% of all merchant transactions worldwide and naturally leads to more disputes over online orders. You can find more insights about these chargeback statistics on chargeflow.io.

What to Do If Your Chargeback Is Denied

It’s a frustrating moment: you’ve waited weeks for a decision, only to see your debit card chargeback denied. It can feel like you’ve hit a brick wall, but a denial isn't always the end of the road.

Your bank isn't necessarily saying you're wrong. What they're saying is that the evidence you submitted wasn't strong enough to overcome the merchant's case.

Usually, a denial boils down to one of two things. Either your evidence wasn't quite compelling enough, or the merchant came back with a powerful rebuttal—think delivery confirmations, signed receipts, or screenshots of their terms of service. The first step is figuring out why your claim fell short.

Rebuilding Your Case for an Appeal

If you’re confident the decision was wrong, you can usually appeal. In the industry, this is sometimes called a "second chargeback" or "pre-arbitration." Think of it as your second shot to present a much stronger, more detailed case.

This is your chance to patch up any holes from your first attempt. Your goal is to either find new information or reframe your existing evidence to make your argument airtight.

Here’s how you can beef up your claim:

- Dig for New Evidence: Did you uncover an old email from the merchant promising a feature that wasn't delivered? Do you have a better photo clearly showing the product's defect? Any fresh proof can tip the scales.

- Write a Clearer Story: Draft a new, more detailed letter explaining what happened. Pinpoint exactly where the merchant's evidence is misleading or incorrect and directly counter their claims.

- Use Their Own Policies Against Them: If the merchant broke their own return policy or terms of service, grab screenshots of those rules. Clearly explain how they failed to follow them.

An appeal is basically asking for a fresh set of eyes on your dispute. You aren't just sending in the same old paperwork. You're actively reinforcing your position and fixing the weaknesses that caused the first denial.

Knowing When to Push for an Appeal

Before you jump back into the ring, take a second to weigh the effort against the potential reward. An appeal takes time and energy, so you need to be realistic. If the amount you're fighting for is small and you don't have any new evidence, it might not be worth the headache.

But if you’ve got solid new proof and the amount is significant, an appeal is the logical next step. Just remember that timing is everything. It’s a good idea to get familiar with the typical debit card chargeback time limit and how it applies to each stage of the dispute. A well-timed, well-documented appeal gives you the best possible chance to turn that denial into a win.

Why Merchants Often Fight Chargebacks

To really get what's happening during a dispute, it helps to step into the merchant's shoes for a moment. When you file a debit card chargeback, a business owner doesn't just see a refund request. For them, it's the start of a costly, time-consuming battle they often feel they have no choice but to fight.

For any business, a chargeback is way more than just losing the money from a sale. They also get slapped with a separate, non-refundable chargeback fee by their payment processor. These fees can run anywhere from $20 to $100 per dispute, which means a single returned sale quickly turns into a much bigger financial hit.

The Bigger Picture for Businesses

Beyond the instant sting of fees, merchants have an even bigger reason to push back: their relationship with their bank. Every single chargeback gets tallied up and contributes to their chargeback ratio—that's the number of disputes they get compared to their total sales.

If that ratio creeps too high, their bank starts to see them as a risky partner. This isn't just a slap on the wrist; it can lead to some pretty dire consequences that put their entire ability to operate at risk.

- Higher Processing Fees: The bank might hike up the fees they charge the merchant for every single transaction they process.

- Account Termination: If things get bad enough, the bank could just shut down their merchant account completely, leaving them with no way to accept card payments.

A merchant fighting a chargeback isn't just trying to claw back one sale. They are actively protecting their bottom line and their crucial relationship with their bank to prevent serious, long-term damage.

This is exactly why learning how to fight a chargeback effectively is such a vital skill for any business. The stakes are much, much higher than a single transaction.

The problem is hitting certain industries particularly hard. For example, online travel and lodging have seen a huge spike in chargebacks, mostly from booking cancellations and service disagreements. E-commerce is also feeling the heat, with a surge in disputes tied to shipping delays and a troubling rise in friendly fraud. You can dig deeper into the latest chargeback statistics on chargeback.io.

Of course. Here is the rewritten section, crafted to sound like an experienced human expert.

Common Questions About Chargebacks

Even with a good handle on the process, a few nagging questions always seem to surface. Let's clear up some of the most common points of confusion when it comes to a debit card chargeback.

Is a Debit Chargeback Harder to Win?

Honestly, yes, it can sometimes feel like an uphill battle compared to a credit card dispute. The big reason comes down to the laws that protect you.

Debit card protections fall under the Electronic Fund Transfer Act (EFTA), which is laser-focused on unauthorized transactions and has some pretty strict reporting deadlines. Credit cards, on the other hand, are covered by the Fair Credit Billing Act (FCBA), which casts a much wider net, covering things like billing errors or if you're unhappy with the quality of goods you received. While you can absolutely win a debit chargeback for those same reasons, the legal framework isn't as cut-and-dry, which puts a lot more weight on the quality of the evidence you bring to the table.

How Long Do I Have to File a Dispute?

This is a huge one, and the clock starts ticking sooner than you might think. The answer really depends on why you're filing.

For straight-up fraud or unauthorized charges, the EFTA gives you 60 days from the day your bank statement was sent to report it. Jump on it within the first two business days, and your liability is capped at just $50.

For other problems, like a package that never showed up or a product that was a total dud, the card network rules (think Visa or Mastercard) are usually more generous. They often give you up to 120 days from the transaction date. But my advice is always the same: act immediately.

Key Takeaway: Don't put it off. The clock starts ticking the moment you spot a problem, and waiting too long is one of the fastest ways for a bank to shut down your claim from the get-go.

Could Filing a Chargeback Hurt My Bank Account?

Filing a legitimate chargeback is what the system is for. It won't harm your relationship with your bank or mess with your account standing. It’s there to protect you from fraud and merchants who don't hold up their end of the bargain.

Where you can run into trouble is by misusing the process. If your bank spots a pattern of filing disputes that don't seem to have a valid reason—a practice often called "friendly fraud"—they’ll see it as a major red flag. In rare, extreme cases, they might even decide to close your account.

Stop losing revenue to confusing chargeback processes. ChargePay uses intelligent automation to manage disputes for you, recovering up to 80% of lost funds without any manual work. Learn how ChargePay can protect your business.

.svg)

.svg)

.svg)

.svg)