When a customer disputes a charge, they’re essentially telling their bank, "Hey, I've got a problem with this payment." It's a formal request to reverse a transaction, and it kicks off an official investigation by the bank. If the bank sides with the customer, the money is pulled directly from your business account in a process called a chargeback.

What a Disputed Charge Really Is

Getting a disputed charge notification can feel complicated, but the idea behind it is pretty straightforward. Think of it as a formal complaint filed by your customer—not with you, but directly with their bank. The bank then steps in as a referee between you and the customer to figure out if the charge was legitimate.

This isn’t just a small hiccup; it's a growing headache for businesses everywhere. As online shopping continues to grow, so do disputes. In fact, global chargeback volumes are projected to hit a staggering 337 million by 2025, which is a 27% jump from 2022. It's a trend that's costing merchants real money.

Who Is Involved in a Disputed Charge

When a dispute happens, it helps to know who all the key players are. The process always involves a few core parties, and each one has a specific job to do.

Here’s a quick breakdown of who’s who when a transaction goes sideways.

It's a triangle of communication, and you're one of the key points.

It’s worth noting that many disputes start from simple confusion or issues that could have been sorted out with a quick email. Unfortunately, some customers go straight to their bank first, triggering this whole formal process. Sometimes it's an honest mistake, but other times it can be a deliberate form of chargeback fraud, which is a whole other challenge for merchants.

Why Customers Actually Dispute Charges

To get a handle on disputes, you first need to get inside your customer's head. It’s almost never about some obscure payment code or technical glitch. Instead, it’s usually about a real-world mix-up, an honest mistake, or sometimes, something a little less innocent.

What a disputed charge means really depends on the situation. Generally, though, customer disputes fall into three buckets. Each one calls for a totally different game plan.

Common Reasons for Disputes

Let's break down the three core reasons a customer might hit that "dispute charge" button.

Merchant Error: This one is on you. It could be something as simple as accidentally billing a customer twice, shipping them the wrong t-shirt, or selling a product that just didn't live up to its online description. Mistakes happen.

Criminal Fraud: This is the most clear-cut type of fraud. A thief gets ahold of a stolen credit card number and goes on a shopping spree in your store. The real cardholder spots the charge, has no idea what it is, and immediately reports it.

Friendly Fraud: This is, by far, the trickiest and most frustrating one for business owners. It’s when a legitimate customer disputes a charge they actually made.

This last one, friendly fraud, is a huge headache. It might be accidental—maybe a customer forgot about that monthly subscription they signed up for months ago. Or maybe a teenager used their parent's card without asking.

The real kicker? Some customers dispute charges on purpose just to get something for free. This abuse of the system is shockingly common. In fact, some studies show friendly fraud can account for up to 75% of all chargebacks, often because it's just easier for the customer than asking for a refund.

Getting a grip on these human reasons is the first step to building solid credit card chargeback protection. Once you start seeing the patterns, you can get to work on fixing the problems at their source.

The Hidden Costs of Every Disputed Charge

When a customer disputes a charge, the damage goes way beyond just losing the money from that one sale. The real cost is a painful mix of lost revenue, surprise fees, and wasted time that can quickly start eating into your profits. Getting the full picture is the first step to understanding why you need a solid game plan for handling these disputes.

The first hit is the most obvious one: the original transaction amount gets yanked right out of your account. But the bleeding doesn't stop there. You also have to kiss the non-refundable processing fees goodbye—the ones you already paid just to handle the transaction.

Beyond the Initial Transaction

On top of losing the sale and the processing fees, your payment processor will almost always slap you with an extra penalty. This is a separate chargeback fee that can cost anywhere from $15 to $100. You can learn more about how chargeback fees work in our detailed guide.

But the financial damage isn't just about direct fees. Think about these less obvious, but equally painful, costs:

- Lost Time and Labor: Your team has to drop what they're doing to dig up evidence, write a response, and manage the whole back-and-forth. That's valuable time they could've spent actually growing the business.

- Inventory Loss: If you sell physical products, you don't just lose the revenue. You often lose the item itself, which you can't turn around and sell to someone else.

- Increased Processing Fees: If your dispute rate climbs too high, processors might start charging you more for every transaction. They'll see you as a higher risk and adjust your rates accordingly.

You’re not the only one feeling the pinch. The financial impact is felt across the entire payments system. For instance, Mastercard research shows each dispute costs financial institutions between $9.08 and $10.32 just to process. This highlights why the entire system takes disputes so seriously. You can explore additional insights on the true cost of chargebacks with Mastercard.

Ultimately, a high dispute rate can seriously damage your relationship with your payment processor. If things get bad enough, they might label your business "high-risk" or even shut down your account entirely, leaving you scrambling to find a way to accept payments at all.

Your Action Plan for Handling a Dispute

That sinking feeling when a dispute notification hits your inbox is all too familiar. It’s easy to panic. But instead of reacting on impulse, this is the moment to take a breath and get organized. Having a solid, step-by-step plan can turn a stressful situation into a manageable process you actually control.

Your first move, always, is to immediately pull up the transaction details. Dig into everything: the original order information, any emails or support chats with the customer, and the shipping confirmations. This quick audit gives you the full picture and helps you decide right away if the dispute is even worth fighting.

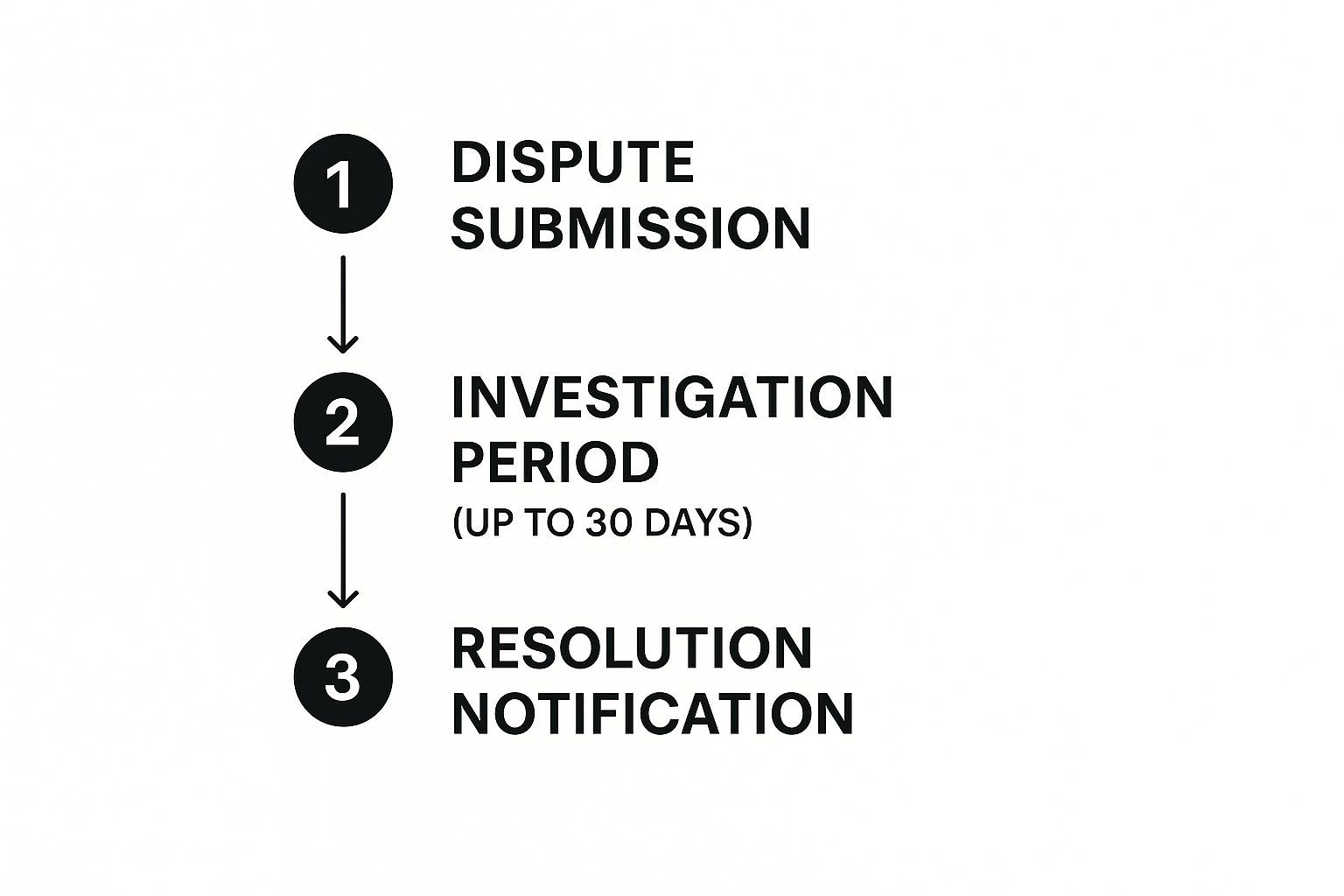

The Lifecycle of a Dispute

From the moment a customer files a claim to the bank's final say, a dispute follows a pretty structured path. Once you understand the stages, the whole process feels a lot less mysterious and you can anticipate what’s coming next.

This graphic lays out the typical flow of a dispute, from start to finish.

As you can see, after the initial dispute is filed, there's an investigation period. This is your window to present your side of the story—and it’s usually your only shot to prove the charge was legitimate.

Gathering Your Evidence and Responding

Okay, this next phase is where you build your case. It’s your opportunity to formally respond to the bank in a process called representment. Your mission is simple: provide compelling evidence that directly shuts down the customer’s claim.

A rock-solid response package almost always includes:

- Proof of Delivery: Shipping confirmations with tracking numbers or, even better, signed delivery receipts. This stuff is gold.

- Customer Communication: Any emails, chat logs, or support tickets showing the customer got help or acknowledged the purchase.

- Order Invoices: Clean, clear receipts that perfectly match the transaction amount and the customer's details.

A crucial thing to remember is that the bank is the judge here, not your customer. Your evidence needs to be clear, concise, and laser-focused on the specific reason for the dispute. A well-organized, professional response dramatically improves your odds of winning.

Putting together a persuasive case definitely takes time, but it’s an essential skill for any merchant who wants to protect their revenue. For a much deeper dive into crafting a winning argument, check out our guide on how to fight a chargeback.

How ChargePay Helps You Fight Back and Win

Trying to fight a disputed charge by hand is a tough, uphill battle. It’s a slow, tedious process filled with tight deadlines and tiny details, and it’s incredibly easy to make a costly mistake. That manual approach is exactly where merchants lose money that should have been theirs.

This is where the right tool completely changes the game. We built ChargePay specifically to automate the entire dispute process, turning what feels like a losing battle into a winnable one. Instead of your team spending hours digging for evidence and filling out forms, ChargePay does the heavy lifting for you.

Automation That Recovers Your Revenue

ChargePay takes over the grunt work of gathering compelling evidence and submitting perfectly crafted responses on time, every single time. This frees up your team to focus on what actually grows your business—not chasing down paperwork.

By automating the dispute process, you’re not just saving time; you’re seriously improving your odds. It's about eliminating human error and using a system built to protect your bottom line from unnecessary losses.

Our platform uses AI-powered evidence gathering and automated submissions to dramatically boost your win rate. That means you can start recovering revenue you previously thought was gone for good. With ChargePay, you’re no longer just reacting to disputes; you’re proactively fighting back and winning.

Answering Your Top Questions About Disputed Charges

Even with a rock-solid business plan, questions about disputed charges are going to pop up. Seeing that notification in your inbox can be jarring, but understanding exactly what you're dealing with makes all the difference. Let's break down some of the most common questions merchants have.

What Is the Difference Between a Disputed Charge and a Chargeback

Think of it like this: a disputed charge is the initial alert, while a chargeback is the final penalty.

When a customer flags a transaction with their bank, that first claim is the disputed charge. It’s the official start of an investigation. If the bank looks into the case and decides the customer is right, they will formally reverse the payment. That reversal is the chargeback.

So, every single chargeback starts its life as a dispute. The good news? Not every dispute has to end in a chargeback if you can resolve it with the customer or win the case with solid evidence.

How Long Do I Have to Respond to a Disputed Charge

Time is not on your side here. The window you have to respond—often called the representment period—is set by the major card networks like Visa and Mastercard. This period usually falls somewhere between 20 and 45 days, but it can vary.

This deadline is strict. If you miss it, you automatically lose the dispute. You'll forfeit the revenue and get hit with any associated fees, no questions asked. Always check the specific deadline in the dispute notification from your payment processor and act fast.

A missed deadline is an automatic loss, regardless of how strong your evidence is. Prioritizing a timely response is one of the most critical parts of managing any disputed charge, meaning you need to have your documentation ready to go.

Can I Prevent Disputed Charges from Happening

You can't eliminate them completely—especially when it comes to outright criminal fraud—but you can absolutely reduce them. Your best defense is a proactive one.

Here are a few practical steps that make a huge difference:

- Use Clear Billing Descriptors: Make sure the name that appears on your customers' bank statements is instantly recognizable as your business. A vague or confusing name is an invitation for a dispute.

- Offer Top-Notch Customer Service: Make it incredibly easy for customers to contact you with problems. A quick refund or an exchange is always cheaper and less damaging than a chargeback.

- Have Transparent Policies: Your return, refund, and cancellation policies should be crystal clear and easy to find on your website. No fine print, no surprises.

Good communication and transparent business practices are your strongest tools. For merchants dealing with specific platforms, understanding the unique rules is key. For instance, our guide on how to handle a PayPal chargeback and win dives into platform-specific strategies that can be a lifesaver.

Managing disputes shouldn't hold your business back. With ChargePay, you can automate the entire process, from evidence gathering to submission, freeing you up to focus on growth. Reclaim your lost revenue by visiting https://www.chargepay.ai today.

.svg)

.svg)

.svg)

.svg)