Let's be honest, "friendly fraud" is one of the most confusing terms in the e-commerce world. The name itself is a problem. It sounds... well, friendly. Like a harmless mistake. But for any merchant who's been on the receiving end, it's anything but.

Imagine you own a restaurant. A customer comes in, orders the steak, eats every last bite, and then calls their bank the next day claiming they never dined with you. The bank reverses the charge, and you're out the cost of the meal and hit with a fee. That’s friendly fraud in a nutshell.

What Is Friendly Fraud and Why Is It So Misleading?

The "friendly" part has nothing to do with the customer's intent. It simply means the purchase was made by the legitimate, authorized owner of the credit card—not some thief who swiped their details online.

This is what makes it so different from criminal fraud, where a scammer is using stolen card numbers to go on a shopping spree. With friendly fraud, the transaction looks completely normal on the surface.

The Real Meaning Behind the Name

Think of it this way: friendly fraud chargebacks come from someone you thought was a real customer. They used their own card, probably from their own home, and they actually received the product or service they paid for. The trouble starts after the sale is already done.

This is a huge distinction. Why? Because all the standard fraud prevention tools you rely on—like Address Verification Systems (AVS) or checking the CVV code—are completely useless here. Of course the information is correct; it’s the actual cardholder making the purchase!

Why It Happens

A customer might file a friendly fraud chargeback for a couple of reasons, and they range from honest mistakes to outright abuse.

- Accidental Disputes: Sometimes it's a genuine mix-up. The customer doesn't recognize the business name on their bank statement (your "billing descriptor"), they forgot about a recurring subscription payment, or maybe their spouse or kid made the purchase without telling them.

- Intentional Abuse: Then there's the deliberate kind. The customer knows the charge is valid but disputes it anyway. This could be a case of buyer's remorse, or they might be trying to get a product for free. This is often called "cyber-shoplifting," and it's a growing problem.

Because the cardholder is the one kicking off the dispute, friendly fraud is also called "first-party fraud." It’s a totally different beast than fighting off anonymous hackers, and it requires a completely different game plan.

Getting a handle on the difference between friendly fraud and other types of chargebacks is the first step to protecting your revenue. To dig deeper, check out the key distinctions in our guide on friendly fraud vs chargeback fraud and start building a smarter defense.

The True Cost of Friendly Fraud for Your Business

When a friendly fraud chargeback hits, it’s easy to focus on the most obvious loss: the sale itself. The money you earned from that transaction gets yanked right back out of your account. But that refunded revenue is just the tip of the iceberg—the real damage runs much, much deeper.

For every single chargeback, your payment processor also slaps you with a non-refundable chargeback fee. This penalty can range anywhere from $20 to $100, and you have to pay it whether you win the dispute or not. Think of it as an administrative fine for the trouble, and it can add up alarmingly fast.

More Than Just a Lost Sale

Beyond the immediate financial sting, there are hidden costs that slowly bleed your resources. Your team has to drop everything to gather evidence, write responses, and navigate the complicated dispute process. These are valuable hours that could have been spent growing the business, helping other customers, or making your products even better.

Friendly fraud is far from a victimless issue. This type of first-party fraud is a rapidly growing challenge, costing eCommerce businesses over $132 billion annually and accounting for up to 75% of all chargebacks. You can explore more chargeback statistics to see the full picture.

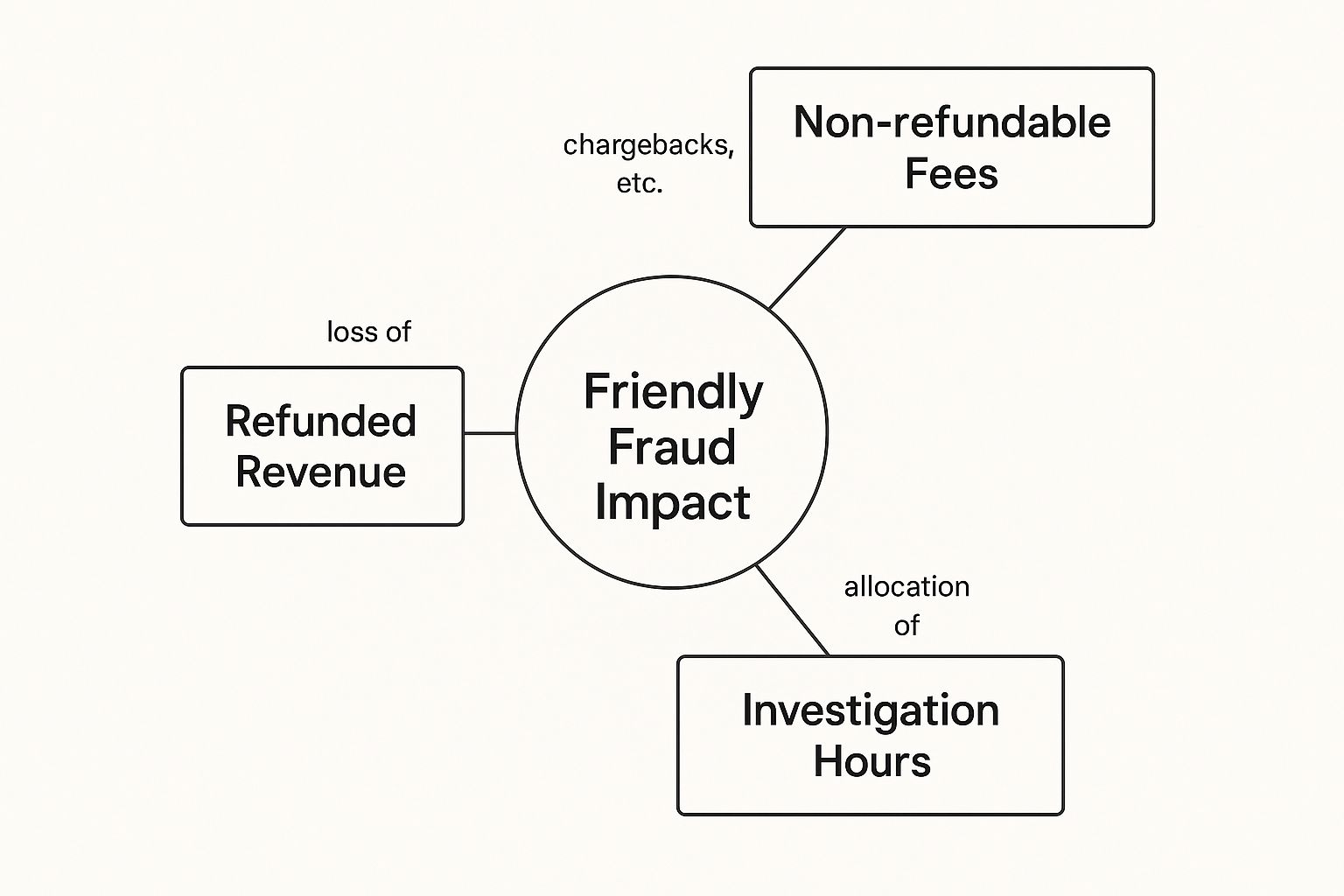

This infographic breaks down the three main ways friendly fraud eats into your bottom line.

As you can see, the total hit from a single chargeback isn't just the sale. It’s a nasty combination of the original transaction, the penalty fee, and the operational hours spent fighting it.

The Biggest Risk You Face

Perhaps the most serious threat from friendly fraud is the danger it poses to your merchant account. Payment processors like Stripe and PayPal keep a close eye on your chargeback ratio—that is, the percentage of your transactions that end up in a dispute.

If this ratio climbs too high, typically above 1%, you’ll be flagged as a high-risk merchant. That’s a label you don’t want. It can lead to some painful consequences:

- Higher processing fees: You'll start paying more for every single transaction you process.

- Account reserves: Your processor might hold back a percentage of your funds just to cover potential future chargebacks.

- Account termination: In the worst-case scenario, you could lose your ability to accept credit card payments altogether.

Losing your merchant account can be a death sentence for an online business. This is why it’s so critical to understand the full cost of friendly fraud. Every dispute chips away at your profits, eats up your team's time, and puts your entire operation at risk.

For a closer look at these penalties, you might be interested in our guide on what a chargeback fee is and how it really affects your business. A proactive approach isn't just a good idea; it's essential for survival.

Why Do Good Customers Initiate Chargebacks?

To really get a handle on friendly fraud, you first have to step into your customer's shoes. Why would someone who happily bought your product suddenly turn around and dispute the charge? The answer isn't as simple as you might think.

Customer motivations fall into two completely different buckets: accidental and intentional. Understanding this split is the absolute key to building a smarter defense. One is an honest mistake, while the other is a calculated abuse of the chargeback system. Let's break down what’s really going on from their perspective.

The Unintentional Mix-Up

Believe it or not, a huge chunk of friendly fraud chargebacks are just honest mistakes. Your customer isn't trying to scam you; they're just confused. They glance at their credit card statement, see a charge they don't recognize, and hit the dispute button because it feels like the fastest way to get answers.

Here are the most common reasons this happens:

- Vague Billing Descriptors: This is a classic. If your legal business name is "Innovatech Solutions LLC," but your customer knows you as "GadgetGo," they'll never recognize that charge. A confusing billing descriptor is one of the biggest, yet most fixable, causes of friendly fraud.

- Forgotten Subscriptions: The "set it and forget it" model is great for recurring revenue, but it has a downside. A customer might have signed up for a service months ago and genuinely forgotten about the recurring payment.

- Family Purchases: We’ve all heard this one. A teenager uses a parent's card for an in-game purchase, or a spouse buys something on a shared account without mentioning it. The primary cardholder sees the charge, assumes the worst, and files a dispute.

The real problem here is a communication breakdown. The customer feels lost and defaults to the only action they know will get a direct response: calling their bank.

Intentional "Cyber-Shoplifting"

Now for the other side of the coin: intentional friendly fraud. This is nothing short of digital shoplifting. The customer knows the charge is legitimate, but they dispute it anyway to get a product or service for free. They are knowingly gaming the consumer protection policies designed to help people with real issues.

This behavior is usually driven by a few specific motives:

- Buyer's Remorse: The customer gets the item, decides they don't want it, and figures it’s easier to file a chargeback than to follow your return process.

- System Abuse: Some people know the chargeback system is heavily weighted in the consumer's favor and simply take advantage of it. They see it as a low-risk, high-reward way to get something for nothing, betting that most merchants won't bother to fight back.

To help you tell the difference, we've broken down the common triggers for both types of friendly fraud. Understanding the why behind a dispute is the first step in figuring out how to respond.

Intentional vs. Unintentional Friendly Fraud Triggers

By seeing these patterns, you can start to identify which chargebacks are simple misunderstandings and which are deliberate attempts to defraud your business. For a deeper dive into what drives these disputes, you can explore the different reasons for a chargeback in our related guide. Knowing what you're up against is half the battle.

Your Proactive Plan to Prevent Friendly Fraud

The absolute best way to handle friendly fraud chargebacks is to stop them before they even start. You can't catch every single one, of course, but a solid, proactive plan is your first and most effective line of defense.

Think of it less like building a fortress and more like paving a smooth, clear road for your customers to travel down. Most of these strategies are simple, cheap, and boil down to one key idea: communication.

When your customers feel like they're in the loop and treated with respect, they're far less likely to run to their bank for a chargeback. You can put these powerful fixes in place today to protect your revenue and build real trust.

Make Your Billing Crystal Clear

One of the quickest wins you can score against friendly fraud is fixing your billing descriptor. That's the little line of text that pops up on a customer's credit card statement. If they don't recognize it, they'll assume it's fraud and dispute the charge. It’s that simple.

Make sure your descriptor is something they'll know instantly. It should use your store's name—the one they actually shop at—not some obscure legal business name they've never seen. A simple format like "BRANDNAME*PRODUCT" or "BRANDNAME.COM" can make all the difference.

Following up with a detailed order confirmation email is just as important. This email is your receipt and your proof. It needs to clearly list:

- What they bought: Include the product names and, if possible, images.

- How much they paid: Give them an itemized breakdown of the cost, taxes, and any shipping fees.

- Your contact information: Make it incredibly easy for them to get in touch if they have a question.

Create a Hassle-Free Customer Experience

A huge part of preventing friendly fraud is having rock-solid and effective complaint handling strategies that solve problems before they escalate. If a customer runs into an issue, you want their first thought to be "I'll contact support," not "I'll call my bank."

Your return policy needs to be transparent and easy to find. Hiding it in the fine print is a recipe for frustration and, you guessed it, chargebacks. A straightforward, fair return process shows customers you stand behind your products and are ready to help if something isn't right.

Around the world, the chargeback process is changing. New research shows that less than half of all chargebacks are directly fraud-related, with a large portion linked to customer confusion or dissatisfaction. This has led many businesses to adopt AI-supported dispute tools and alert systems that can prevent up to 90% of incoming chargebacks by enabling early refunds. Discover more insights about countering first-party fraud on Mastercard.com.

Ultimately, excellent and accessible customer service is your secret weapon. When customers know they can get a quick, helpful response from a real person, they have no reason to file a friendly fraud chargeback. A small investment in great support can save you thousands in lost revenue and fees down the road.

For a deeper dive into defensive measures, check out our complete guide on chargeback prevention.

How to Fight Chargebacks and Win Back Your Revenue

When a friendly fraud chargeback slips past your defenses, it feels like a punch to the gut. But this isn't the end of the road. You absolutely have the right to fight back and reclaim your money through a process called representment.

Think of representment as your opportunity to build a legal case. The bank has already heard the customer's side of the story, and now it’s your turn to present the facts. A well-organized, evidence-backed response not only helps you win back that specific sale but also signals to potential fraudsters that your business doesn’t just roll over.

Gathering Your Compelling Evidence

To win a dispute, you need to prove one simple thing: the charge was legitimate. Your job is to paint a crystal-clear picture for the bank, showing that the real cardholder made the purchase, knew what they were buying, and got the goods or services as promised.

The goal is to collect as much "compelling evidence" as you can. The more data points you have connecting the customer to the transaction, the stronger your case will be.

Here’s a checklist of the most powerful evidence you can gather:

- Order and Shipping Details: This is non-negotiable. Include the order confirmation email, any shipping updates, and—most importantly—the delivery tracking number that shows the item arrived at the customer’s address.

- Customer Communications: Did the customer email your support team? Did they leave a positive product review? Any interaction that proves they engaged with your business after the purchase is incredibly valuable.

- Digital Footprints: For online orders, this is crucial. Provide the customer's IP address from the time of purchase. Even better, show that it matches the IP address from which they downloaded a digital product or logged into their account.

- Transaction Verification: Evidence that you verified the card's CVV number or used an Address Verification System (AVS) match helps establish that the transaction was secure from the start.

Responding quickly is just as important as the evidence you provide. Card networks give you a strict deadline, often just a few weeks, to submit your case. Missing it means an automatic loss, no matter how strong your evidence is.

Building an Unbeatable Case

Once you have your evidence, you need to present it clearly and professionally. Don't just dump a folder of random files on the bank. Write a short, clear rebuttal letter that explains the situation and guides them through your evidence, document by document. A critical component of proving a transaction's legitimacy and winning chargeback disputes lies in understanding expressed consent and showing the bank the customer agreed to your terms.

Fighting friendly fraud chargebacks requires a methodical approach, but it is absolutely winnable. For a more detailed walkthrough of the dispute process, you can learn more about how to win a credit card dispute in our dedicated guide. With the right evidence and a professional approach, you can turn that potential loss into a recovered sale.

Got Questions About Friendly Fraud? We've Got Answers.

Even when you feel you've got a handle on it, friendly fraud can throw some curveballs. It’s a messy topic with a lot of gray areas. Let’s clear up some of the most common questions merchants like you run into.

What Is the Difference Between Friendly Fraud and True Fraud?

This is the big one, and it’s critical to know the difference.

True fraud is what everyone pictures when they hear "credit card fraud." It's a clear-cut crime where a thief steals someone's card details and goes on a shopping spree. In that scenario, the real cardholder is the victim.

Friendly fraud, on the other hand, starts with a perfectly legitimate customer. They use their own card to buy something from you, but later on, they dispute the charge. Whether it was an honest mistake or they're trying to get something for free, you—the merchant—end up as the victim, because the original transaction was completely valid.

Can I Get in Trouble for Fighting a Friendly Fraud Chargeback?

Absolutely not. You won't face any penalties for fighting a friendly fraud chargeback. It’s your right as a merchant.

The official process for challenging a dispute is called representment, and it's built into the system for this exact reason. As long as you play by the card networks' rules and back up your case with solid evidence proving the charge was legitimate, you’re simply protecting your business. Honestly, fighting back is the only way to reclaim the revenue you rightfully earned.

Is There Software That Can Help Manage Friendly Fraud?

Yes, and it can be a total game-changer for your business. There are plenty of services and software platforms out there specifically designed to help merchants tackle friendly fraud chargebacks.

These tools can help you in a few key ways:

- Gather Evidence Automatically: They can instantly pull all the necessary documents, like order details, shipping confirmations, and customer communications.

- Respond Faster: They help you hit those tight deadlines by generating and submitting dispute responses on your behalf.

- Provide Early Warnings: Some systems can even alert you to a potential chargeback before it’s officially filed. This gives you a golden opportunity to issue a refund and dodge the expensive fees and penalties altogether.

Here's why automation matters: Merchants who try to fight disputes manually only win about 8% of their cases. Using an automated solution can seriously boost that success rate, putting money back in your pocket that would otherwise be lost.

Does Improving Customer Service Really Reduce Friendly Fraud?

Yes, and it makes a much bigger difference than you might think. A huge chunk of accidental friendly fraud happens because a customer is confused, frustrated, or just can't figure out how to get help. For them, filing a chargeback feels like the fastest way to solve their problem.

When you offer customer support that's quick, easy to find, and genuinely helpful, you give them a better path. By solving their issue directly—whether it’s a question about their order or a simple return request—you remove their reason for filing a dispute in the first place. A small investment in great service can save you a fortune in chargeback costs.

Tired of losing revenue to friendly fraud chargebacks? ChargePay uses AI to automate the entire dispute process, generating winning responses and recovering your money without you lifting a finger. Stop fighting manually and let automation protect your profits. Learn more at ChargePay.

.svg)

.svg)

.svg)

.svg)