Ever signed up for a free trial online, only to find yourself jumping through hoops to cancel it? That kind of frustrating experience is exactly what the FTC Negative Option Rule is designed to stop. Think of it as a consumer protection rule aimed at businesses that trap customers in subscriptions they no longer want.

What Is the FTC Negative Option Rule

At its heart, the FTC Negative Option Rule is all about fairness. It targets any business setup where a customer’s silence—or their failure to take action—is treated as consent to keep charging them. This covers a whole range of common sales tactics you see every day.

The best way to think about it is like a "two-way door" policy for your business. If a customer can walk in and sign up with a simple click, they must be able to walk out just as easily. The rule demands that canceling a service has to be as straightforward as it was to sign up in the first place.

The Evolution from Niche Rule to Broad Mandate

This rule isn't brand new. The original version dates all the way back to 1973, and it was mainly for old-school "book-of-the-month" clubs where you'd keep getting products unless you specifically opted out. But today's subscriptions economy, powered by platforms like Shopify and PayPal, needed something stronger.

That's why the FTC rolled out major updates, making the rule much broader. It now covers nearly all types of recurring payment models, including:

- Automatic Renewals: Think software, streaming services, or any subscription that renews on its own.

- Continuity Plans: Regular shipments of physical goods like coffee, vitamins, or grooming products.

- Free-to-Pay Trials: Those promotional periods that automatically convert to a paid plan if you don't cancel in time.

The big idea is simple: A customer's silence should not be treated as a blank check. The rule makes sure that any recurring charge is based on a clear, upfront agreement and an equally clear path to get out of it.

Why This Matters for Your Business

This isn’t just a friendly suggestion from the government; it's a federal requirement with real teeth. The expanded rule is designed to shut down shady practices that make it a nightmare for people to end their financial commitments.

For merchants, this means you need to take a hard look at your entire customer journey, from the initial sales page to the final cancellation screen. If you're handling any kind of recurring payments, you absolutely have to understand these regulations.

Making your cancellation process simple and transparent isn't just about following the law. It’s also about building trust. When customers know they can leave easily, they're more likely to sign up in the first place, stick around longer, and are far less likely to file frustrating chargebacks.

Does This Rule Apply to Your Business?

When you hear about the FTC Negative Option Rule, it’s easy to picture massive companies with millions of subscribers. The truth is, this rule has a much wider net, catching businesses of all sizes—from solo entrepreneurs to growing e-commerce stores.

The main takeaway is this: if your business charges customers again and again after they sign up once, you’re almost certainly covered. It doesn't matter if you're using Shopify, Stripe, PayPal, or any other payment platform.

Bottom line, the FTC is looking at any transaction where a customer’s silence leads to another charge. That simple idea covers a lot of ground.

The Three Main Business Models Under Scrutiny

So, does your business model fall under the rule? Let's break down the main categories the FTC is watching. Most subscription-style businesses fit neatly into one of these buckets.

Automatic Renewals: This is the big one. It covers any service that automatically renews at the end of a billing cycle. Think monthly software access, weekly meal kits, or annual memberships.

Continuity Plans: Very similar to auto-renewals, but this usually involves shipping physical products on a regular schedule. A monthly coffee subscription, a quarterly vitamin delivery, or a "product-of-the-month" club are all perfect examples.

Free-to-Pay Conversions: This model is a hugely popular way to get new customers. You offer a free or cheap trial that automatically flips to a full-price paid plan if the customer doesn’t cancel before the trial is up.

If your checkout process involves any of these, the FTC expects you to play by its rules for clear disclosures, getting proper consent, and making cancellation a breeze.

Real-World Examples of Affected Businesses

Still not sure if this is you? Let’s look at some real-world examples. The rule's reach often surprises merchants who think they’re too small to be on the FTC's radar.

A small business running a niche subscription box on Shopify, for instance, is just as responsible as a major streaming service. A SaaS company offering a 14-day free trial has to follow the same rules as a national gym chain signing up new members.

Anyone looking to set up their own fan subscription platform needs to pay close attention, as this rule directly governs how you have to disclose and handle those recurring payments.

The rule isn't about what you sell; it's about how you sell it. If the transaction involves an automatic recurring payment, the FTC Negative Option Rule is designed to govern that relationship.

Why Every Merchant Needs to Pay Attention

Simply ignoring these regulations isn’t a strategy. The rule applies to all sellers using these business models, no matter their size or industry. Even if you think your current setup is fair, it might not hit the specific legal standards for transparency and easy cancellation.

This broad reach means everyone from digital course creators to e-commerce stores selling physical goods needs to take a hard look at their checkout and cancellation flows.

Being proactive isn't just about dodging potential fines. It’s about building a healthy, sustainable business on a foundation of customer trust. A straightforward checkout and a no-hassle cancellation process lead to happier customers, fewer complaints, and a big reduction in costly chargebacks.

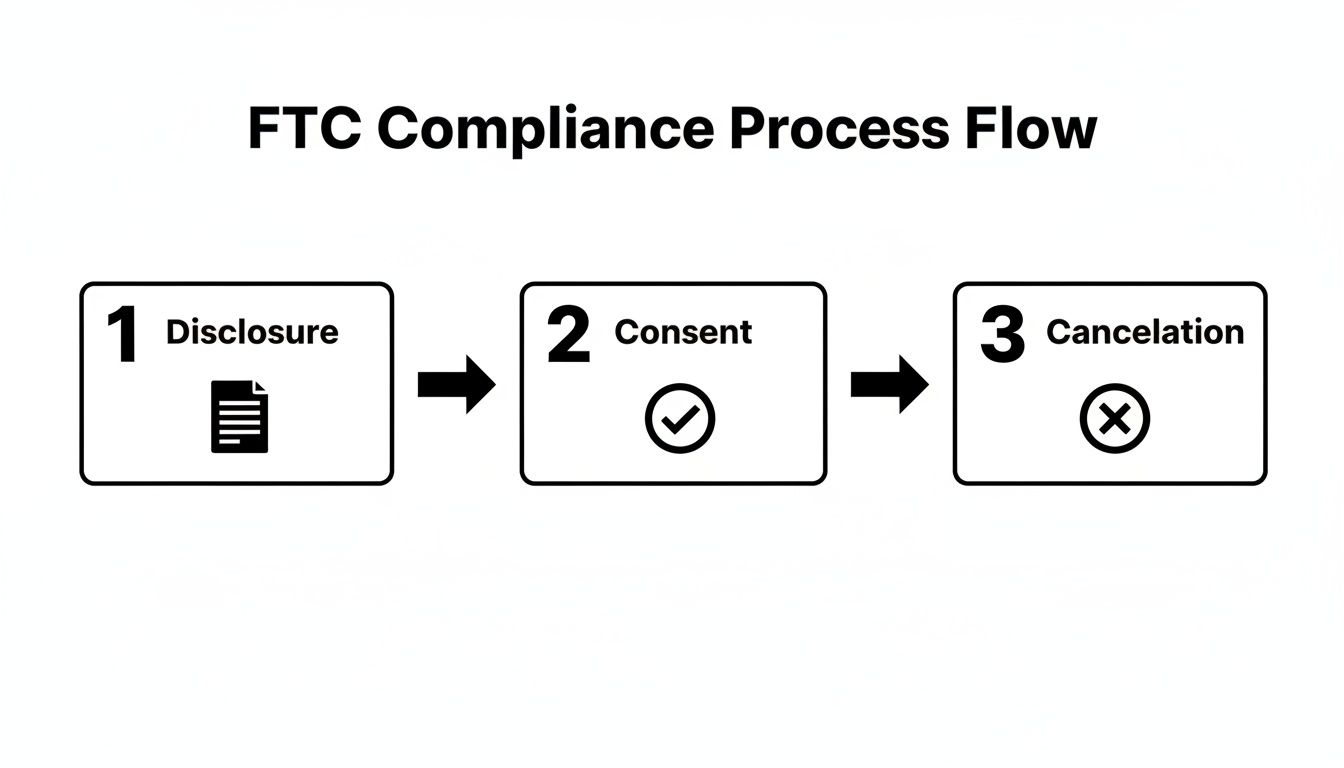

Your Three-Step Compliance Checklist

Getting compliant with the FTC Negative Option Rule can feel like a huge project, but it really just boils down to three core ideas. Think of it as a simple journey to build trust: be upfront, get clear permission, and make leaving easy.

Nailing these three things isn't just about dodging trouble with the FTC. It's about creating a better, more transparent experience for your customers. That means less frustration, fewer chargebacks, and a more loyal customer base in the long run.

Let’s break down exactly what you need to do.

Step 1: Clearly Disclose Your Terms

First things first: transparency. Before a customer even thinks about pulling out their credit card, they need to see all the key terms of your offer laid out plain and simple. Hiding details in the fine print or behind vague links is a fast track to a violation.

Think of it like the instructions for a piece of IKEA furniture. You need to see all the parts and steps right away, not find a crucial booklet hidden inside the box after you've already started.

Your disclosures have to include these key pieces of information, right where people will see them:

- What they’re being charged for: State clearly that they'll be charged on a recurring basis unless they take action to cancel.

- The total cost: Specify the exact amount they'll be charged after any trial period is over. No surprises.

- Renewal dates and frequency: Explain precisely when the charges will hit—for example, "monthly on the 15th" or "annually on your signup date."

- Cancellation deadline: If there’s a cutoff date to cancel before the next payment, it has to be clearly stated.

- How to cancel: Give them simple, easy-to-follow instructions for the cancellation process itself.

Step 2: Get Informed and Unambiguous Consent

Once you’ve laid out your terms clearly, the next job is to get the customer's explicit consent for the recurring charges. This isn't something you can just imply or bury in a general "I agree to the terms and conditions" checkbox. The FTC wants to see a specific, deliberate "yes" to the negative option feature.

This consent has to be completely separate from any other agreements you have. For instance, you can't lump in consent for recurring billing with your privacy policy. The customer has to actively agree to the automatic payments.

The rule's logic is pretty straightforward: A customer should never be surprised by a recurring charge. Gaining separate, informed consent ensures they understand and accept the ongoing financial commitment before it begins.

This means you must use something like an unchecked checkbox that the customer has to physically click to agree. Pre-checked boxes are a massive red flag for non-compliance and are explicitly banned. By making customers take this deliberate action, you create a solid record of their consent and dramatically cut down on future disputes. For more tips on building a smooth and compliant payment experience, check out our insights on optimizing your checkout process.

Step 3: Provide a Simple Cancellation Method

The last piece of the compliance puzzle is making it just as easy to cancel as it was to sign up. If a customer can join with a few clicks online, they must be able to leave the exact same way. Forcing them to call a support line, fill out a long form, or navigate a confusing maze of website menus is a non-starter.

This is often called the "click-to-cancel" provision. Your cancellation method has to be easy to find, simple to use, and take effect right away. Forcing customers to sit through retention pitches or answer a long survey before they can finally cancel is no longer acceptable.

A simple, user-friendly cancellation process does more than keep you compliant. It shows you respect your customers' decisions, which leaves a positive impression. A customer who leaves on good terms is way more likely to come back later or recommend your business to others.

Common Checkout Mistakes and How to Fix Them

Knowing the theory behind the FTC Negative Option Rule is a good start, but seeing it in action is where things really click. Plenty of well-meaning merchants make small mistakes in their checkout and cancellation flows that can spiral into big problems.

Let's walk through some of the most common missteps and, more importantly, how to fix them. Think of it as turning potential compliance headaches into opportunities to build trust with your customers.

These issues often pop up from older design habits that focused more on getting the sale than being upfront. But under the new rule, transparency isn't optional. Getting your e-commerce website designing right is crucial to make sure any recurring offer you have is fully compliant and avoids hefty penalties.

The good news? These fixes are usually pretty simple. It's all about shifting your mindset from "hiding the details" to "highlighting the commitment."

The Vague Hyperlink Mistake

This one is a classic. You've seen it a thousand times: a checkout page with a tiny line of text that says, "By clicking 'Pay Now,' you agree to our Terms and Conditions." All the important stuff—the renewal cost, the billing date, how to cancel—is buried inside that linked document.

The Fix: Don't make your customers go digging. Pull that essential information out of the hyperlink and put it right on the checkout page. The full price they'll pay after a trial, how often they'll be billed, and the cancellation deadline should be crystal clear, right next to the payment button. Clarity is your best friend here.

This simple flowchart breaks down the three core pillars of FTC compliance: clear disclosure, explicit consent, and easy cancellation.

As you can see, each step needs to be a distinct, unambiguous part of the customer's journey, leaving zero room for confusion.

The Pre-Checked Consent Box Trap

Another huge red flag for the FTC is the pre-checked consent box. This is where the box to agree to recurring charges is already ticked for the customer before they even get there. The rule is absolutely firm on this: consent must be affirmative and unambiguous. A pre-checked box assumes consent; it doesn't earn it.

The Fix: This one's easy. Always use an unchecked checkbox for agreeing to recurring payments. The customer has to physically perform the action of clicking that box themselves.

This deliberate action serves as clear evidence that the customer understood and agreed to the negative option feature. It's a small change that makes a huge difference in proving informed consent.

Compliant vs. Non-Compliant Practices

To make it even clearer, let's look at a side-by-side comparison of common practices. This table should help you spot any gaps in your own checkout flow and see exactly how to fix them.

Getting these details right isn't just about avoiding fines—it's about building a better, more transparent relationship with your customers from the very first interaction.

The Confusing Cancellation Maze

Finally, a lot of businesses stumble on the "simple cancellation" test. If a customer has to click through five different screens, watch a mandatory "we're sad to see you go" video, or call a support line that's only open on weekdays to cancel an online subscription, you're not compliant. The rule is simple: cancelling must be at least as easy as signing up.

The Fix: Put a clear "click-to-cancel" feature right inside the customer's account dashboard. It should be easy to find and take just a few clicks to complete. If you want a better sense of what a clear post-purchase experience looks like, check out our guide on creating the perfect https://www.chargepay.ai/order-confirmation page.

Remember, the FTC gets thousands of complaints about negative options every year, and these complaints fuel enforcement actions. In one famous case, FTC v. FTN Promotions, the defendants racked up $171 million in unauthorized charges by making cancellation a nightmare. These widespread issues are exactly why the rule exists—to push merchants toward a more honest, "easy exit" design.

The Real Costs of Non-Compliance

Ignoring the FTC Negative Option Rule isn't just a regulatory gamble; it's a direct threat to your bottom line. The consequences go way beyond a simple slap on the wrist, creating a ripple effect of financial and reputational damage that can be incredibly tough to bounce back from.

The most obvious hit comes directly from government enforcement. We're not talking about minor fines here—these penalties are designed to be a serious deterrent. When the FTC catches a business breaking the rules, the financial penalties can be crippling, especially for a small or medium-sized company.

But the official penalties are just the tip of the iceberg. It's the hidden costs that often do the most long-term damage to an e-commerce business.

The Surge in Customer Disputes and Chargebacks

When customers feel like they've been tricked or trapped into a subscription, they don't just shrug and accept the charge. More often than not, their first move is to call their bank and file a dispute, which immediately triggers a chargeback. Poor compliance with the Negative Option Rule is a direct pipeline to higher chargeback rates.

Put yourself in their shoes for a second. If canceling your service is a confusing nightmare, a chargeback feels like the easiest way out. This knee-jerk reaction creates a cascade of problems for you:

- Immediate Revenue Loss: The sale amount from the disputed transaction is gone.

- Added Fees: On top of that, you get hit with a separate fee for every single chargeback filed against you.

- Wasted Resources: Your team ends up spending valuable time and energy fighting disputes instead of focusing on growing the business.

This vicious cycle of unhappy customers and forced refunds can chew through your profits in no time. If you want a deeper dive into how much each dispute really costs, check out our guide on what a chargeback fee is.

Risking Your Relationship with Payment Processors

Every chargeback filed against you gets tracked. Payment processors like Stripe and PayPal keep a close eye on your chargeback ratio—the percentage of your transactions that end up in a dispute. If that number creeps too high, you get flagged as a high-risk merchant.

This is a huge problem. Being labeled "high-risk" can lead to:

- Higher processing fees, which cuts into your margins on every sale.

- A rolling reserve, where the processor holds back a chunk of your revenue to cover potential future disputes.

- Account termination, which is the absolute worst-case scenario. Losing your merchant account can shut down your ability to accept online payments overnight.

Proactive compliance isn't just about following the law; it's a core business strategy. By making your terms crystal clear and your cancellation process dead simple, you protect your revenue, your reputation, and your crucial relationships with payment partners.

The FTC isn't slowing down, either. The 2024 rule amendments specifically target misrepresentations tied to negative options, giving the agency the power to levy penalties up to $51,744 per violation. You can get more insight into these enforcement updates straight from the FTC's policy statement.

At the end of the day, the costs of cutting corners far outweigh the effort it takes to build a transparent, customer-friendly subscription model from the get-go.

Your Top Questions About the Rule Answered

Wading through the fine print of any new regulation can feel a bit overwhelming. When it comes to the FTC Negative Option Rule, we see the same questions pop up time and time again from merchants trying to figure out how it all affects their day-to-day business.

Let’s clear the air and tackle some of the most common questions we hear. Think of this as the final piece of the compliance puzzle, making sure your subscription model is built on a solid, trustworthy foundation.

Do I Need to Send Annual Reminders for Subscriptions?

This is a big one, and it’s a source of a lot of confusion. In earlier drafts of the rule, the FTC was seriously considering a mandate for businesses to send out annual reminders to every subscriber, especially for plans that didn't involve physical products.

But here’s the bottom line: the final version of the rule dropped that requirement. While it’s no longer a federal mandate under this specific rule, it’s still an incredibly smart business practice. A simple yearly heads-up can prevent customer sticker shock, build a ton of goodwill, and slash the number of chargebacks from people who simply forgot they were still subscribed.

Even though the final rule ditched the mandatory annual reminder, the FTC has hinted it might bring the idea back in the future. Staying ahead of the curve by sending reminders is a great way to protect your business and keep your customers happy.

What About 'Save' Offers During Cancellation?

Another hot topic is what you're allowed to do when a customer hits that "cancel" button. Can you offer them a sweet deal or a different plan to convince them to stick around? The short answer is yes, but you have to play it by the book.

You can absolutely present a "save" offer, but it cannot, under any circumstances, get in the way of the cancellation itself. The customer has to be able to easily say "no thanks" and immediately proceed with cancelling their subscription without jumping through any extra hoops. Forcing them to sit through a lengthy pitch or click through a maze of pages just to leave is a definite no-go and a clear violation.

Does This Rule Apply to B2B Transactions?

For the most part, the FTC's consumer protection rules, like this one, are aimed squarely at business-to-consumer (B2C) transactions. The primary goal is to shield individual consumers from shady or confusing subscription tactics.

That said, it isn't always black and white. If your B2B deals involve very small businesses or sole proprietors—who often act a lot like regular consumers—it’s smart to play it safe. Erring on the side of caution and following the rule’s principles is your best bet. For a deeper dive into common business questions, feel free to check out our full FAQ page.

When Does This All Go Into Effect?

Timing is everything. After the rule was published in the Federal Register, its key provisions were set to roll out in stages. The rules targeting misrepresentations took effect around January 14, 2025.

The rest of the provisions, including the big one—the click-to-cancel requirement—become fully enforceable on May 14, 2025. You can get more details on the official implementation timeline to make sure you’re on track.

At ChargePay, we know that building trust through transparency is the best way to reduce chargebacks. Our AI-powered platform automates the entire dispute process, helping you recover lost revenue so you can focus on what you do best: creating amazing customer experiences. Learn how ChargePay can protect your business.

.svg)

.svg)

.svg)

.svg)