When you spot a weird charge on your statement, it's easy to feel frustrated. So, what's the right way to dispute a transaction? You've got two main paths: contact the merchant directly, or go straight to your bank or credit card company. While calling the merchant can sometimes clear up simple mix-ups, I've found that going to your financial institution is usually the faster and more effective route.

Your First Moves After Spotting a Bad Charge

We've all been there—that sinking feeling when you see a charge you don't recognize. Before you start to panic, take a deep breath. Acting quickly and methodically is key, and your first few actions can make all the difference in getting your money back.

The numbers back up the gut instinct to call your bank. A huge 76% of consumers skip the merchant and take their disputes directly to their bank. Why? It comes down to trust. A solid 89% of people trust their financial institutions to handle it, and success breeds confidence. In fact, 88% of people who win a dispute are more likely to file another one if needed. FF News has some great insights on these consumer trends if you want to dig deeper.

This preference just makes sense. Banks have established procedures and legal protections in place for you, which is a far cry from trying to negotiate with a merchant who might not be willing to help.

To help you get started, here's a quick rundown of what you should do immediately.

Your First Steps in a Transaction Dispute

Taking these initial steps sets you up for a much smoother process.

Knowing the Rules of the Game

Before you start the dispute process, you need to be clear on two things: whether your claim is valid and how much time you have to act. A valid dispute isn't just about a charge you don't recognize; it covers a whole range of issues.

You've got solid ground to stand on in these common scenarios:

- Unauthorized Charges: This is the big one—you didn't make the purchase, and it’s likely fraud.

- Product Not as Described: You ordered a blue widget, but a broken red one showed up.

- Services Not Rendered: You paid for a service that was never provided.

- Incorrect Amount Billed: You were charged the wrong price for something.

Acting fast is also non-negotiable. Most credit card companies give you a window of 60 to 120 days from the transaction date to file. If you wait too long, you could lose your chance to get your money back entirely. You can learn more about the specifics in our detailed guide on the meaning of disputed charges.

Building a Case Your Bank Cannot Ignore

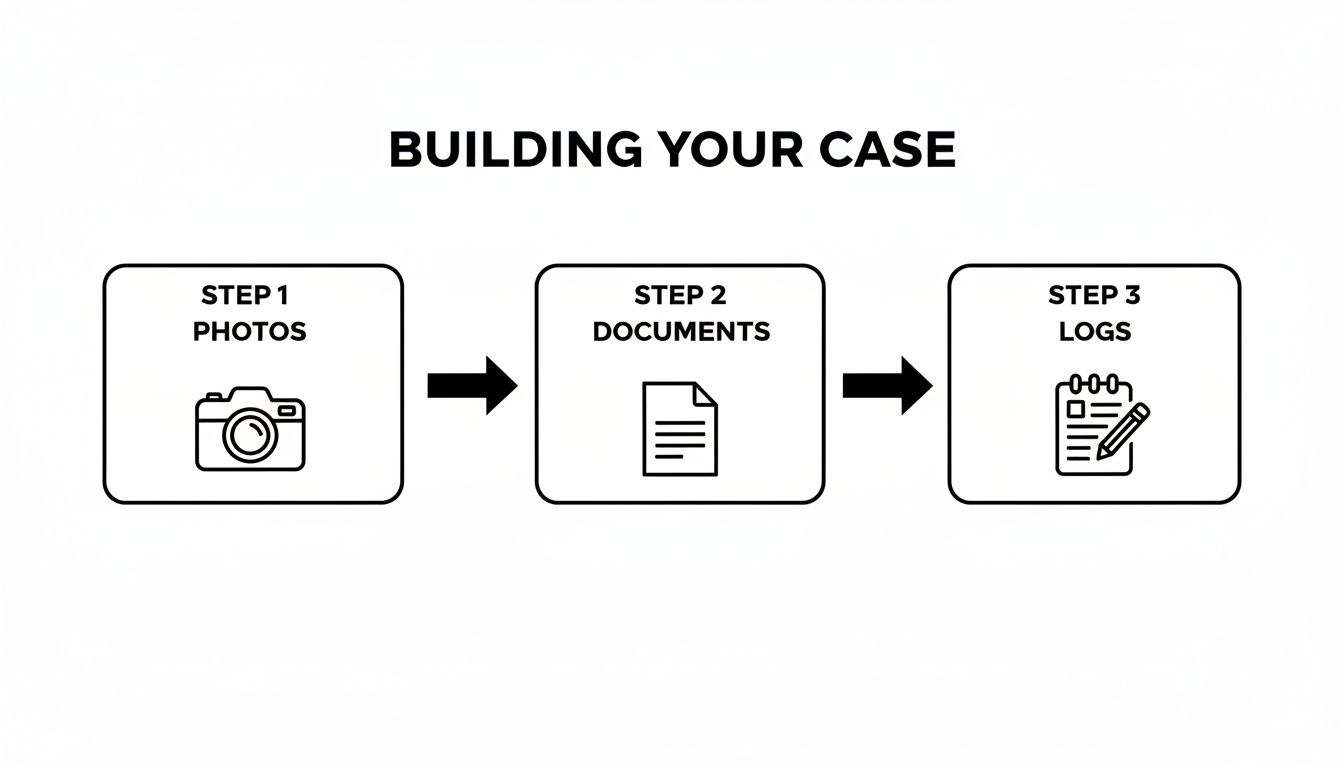

Winning a dispute isn't about just telling your bank a charge is wrong; it's about proving it. Bank investigators are looking for a clear, logical story backed up by solid proof. Your job is to hand them a case file that leaves absolutely no room for doubt. Think of yourself as a detective building an airtight argument.

The specific evidence you'll need really depends on the kind of dispute you're filing. Every situation calls for a different set of documents to tell your side of the story effectively.

When a Product Isn't as Described

Did you order a high-end leather jacket only to receive a cheap, plastic knock-off? Or maybe you bought a phone that was listed as "like new" but showed up with a massive crack across the screen. When this happens, your best evidence is visual.

You need to clearly show the gap between what was promised and what you actually got. Start by grabbing screenshots of the original product listing—pay close attention to the description, the seller's photos, and any specific claims they made.

Next, take your own crystal-clear photos or a short video of the item that arrived. Make sure you highlight all the defects, damage, or differences. A simple side-by-side comparison of their photo and yours can be incredibly powerful for an investigator.

For Services Never Delivered or Canceled

This is a classic problem with contractors, online courses, or even event tickets. If you paid for a service that never materialized, your evidence is all about communication and agreements.

Pull together the following:

- Contracts or Agreements: Any document that outlines the scope of work and delivery dates is absolutely essential.

- Email Correspondence: Dig up and save every email discussing the service. This includes any attempts you made to follow up or ask about delays.

- Cancellation Confirmations: If you canceled a subscription according to the merchant's own terms but were still charged, that confirmation email is your golden ticket.

For instance, if you paid a deposit for a catering service that was a no-show at your event, your signed contract and the unanswered emails you sent the week before are your primary pieces of evidence.

A well-documented timeline of your communication is often the deciding factor. Log every call, save every email, and screenshot every chat message. This creates a powerful narrative showing you acted in good faith while the merchant simply failed to deliver.

Tackling Unauthorized Charges and Fraud

When a fraudulent charge pops up on your statement, the game changes. Now, the focus is on proving you couldn't possibly have made the transaction.

Document the exact moment you discovered the charge. Make a note of where you were when the transaction supposedly happened—if you were at work in Chicago and the charge was made at a store in Miami, that’s compelling proof.

Report the fraud to your bank immediately. They'll likely ask you to confirm other recent, legitimate transactions to help them spot the fraudulent pattern. While the bank does the heavy lifting on the technical side, your quick reporting and a clear account of events are vital.

Building a strong case is the first step, and you can find more strategies on how to win a credit card dispute in our other guides.

How to Navigate the Bank's Dispute Process

Alright, you've got your evidence lined up and you're ready to make it official. The next step is filing the dispute with your bank or credit card company. This is where you formally present your case, and knowing how their system works can make the whole thing a lot less stressful.

Each bank gives you a few different ways to submit a claim. You can usually choose between their online portal, mobile app, a phone call, or even sending a formal letter. Honestly, for most situations, the digital options are your best bet. They’re fast, you get an instant paper trail, and they often walk you through exactly what’s needed.

Choosing Your Method and Reason Code

Submitting your dispute through your bank's app or online portal is almost always the most efficient route. With global chargebacks on the rise—expected to jump 24% between 2025 and 2028—banks are swamped. Each dispute costs them somewhere between $9.08 and $10.32 to process, so they have a real incentive to resolve clear-cut cases quickly through these automated systems. You can dig into these trends in the latest Mastercard chargeback report.

When you start the filing process, you’ll be asked to pick a reason code. This is a super important step because it tells the bank why you're disputing the charge. Getting this right from the get-go can speed everything up.

Common reason codes you'll likely see are:

- Fraudulent Transaction: Use this when you didn't authorize the charge at all—your card was stolen or cloned.

- Product Not Received: The item you paid for simply never showed up.

- Product Not as Described: What you got is wildly different from what was advertised.

- Canceled Recurring Transaction: You canceled a subscription but got dinged with another charge anyway.

Be precise here. Choosing "Fraudulent Transaction" for a package that never arrived will just send your case down the wrong path and slow things down.

What to Expect After You File

Once you hit submit, the bank kicks off its investigation. One of the first things they usually do is issue a provisional credit to your account for the disputed amount. Don't get too excited—this is a temporary credit. It’s not your money for good just yet.

This is where all that evidence you gathered comes into play.

Having photos, documents, and communication logs ready makes your submission to the bank that much stronger.

The investigation itself can take a while, anywhere from a few weeks to a couple of months. During this time, your bank reaches out to the merchant's bank to get their side of the story. The merchant then gets a chance to provide their own evidence to argue against your claim.

Pro Tip: Keep a close eye on your account and any emails or letters from your bank. They might need more information from you, and if you're slow to respond, it could put your whole case at risk. Set up alerts on your banking app so you don't miss any updates.

While you're waiting, keep all your original evidence saved somewhere safe. It's a good idea to check your dispute status online every week or so. If you feel like too much time has passed without an update, don't hesitate to call the bank's dispute department and politely ask for a status check. You can get a better sense of the entire timeline by exploring our guide to the credit card dispute process.

Understanding How the Merchant Fights Back

When you file a dispute, it's not a one-way street. The merchant gets a chance to tell their side of the story, and understanding their playbook is the key to building a case that actually wins. Think of it like a debate—if you know your opponent's arguments ahead of time, you can prepare a much stronger rebuttal from the get-go.

Once you dispute a charge, your bank shoots a notice over to the merchant's bank. This kicks off a process where the business can either accept the chargeback or decide to fight it. If they choose to fight, they enter what’s called the chargeback representment phase, where they submit their own evidence to prove you were wrong.

The Merchant's Arsenal of Evidence

Trust me, merchants don't just roll over and accept the loss. They have a whole range of evidence they use to counter claims. This "compelling evidence" is specifically designed to prove to the bank that the transaction was legit and they held up their end of the bargain.

Here's what they'll almost certainly use against you:

- Proof of Delivery: This is the go-to for physical goods. A shipping confirmation with a tracking number showing the package landed on your doorstep is incredibly powerful evidence for them.

- IP Logs and Geolocation Data: Bought a digital product? They'll pull the IP address you used to make the purchase to show it came from your general location, maybe even one of your known devices.

- Customer Communication: This one trips a lot of people up. Any emails, chat logs, or support tickets where you talked about the product—or even just acknowledged receiving it—can be used against your claim.

- Terms of Service Agreement: Remember that little box you checked? They do. A record proving you agreed to their terms, especially their refund policy, is a cornerstone of their defense.

A big part of anticipating their move is knowing about the ecommerce fraud prevention strategies they have in place. These systems are built to flag suspicious orders and automatically gather the data they need to fight a dispute later on.

Pro Tip: Knowing what evidence the merchant has gives you a massive advantage. If you know they have a delivery confirmation, your argument can't be "it never arrived." It needs to be "the box was empty" or "the product was broken on arrival," and you need proof to back that up.

Why Merchants Are Wary of "Friendly Fraud"

From the merchant's perspective, they're constantly on guard against something called friendly fraud. This is when a legitimate customer disputes a perfectly valid charge—maybe they forgot about the purchase, didn't recognize the name on their statement, or are deliberately trying to get something for free. It’s a massive, costly headache for businesses.

This is why they’re so motivated to challenge disputes they believe are bogus. Globally, merchant win rates in chargeback disputes are pretty low at around 45%, meaning they lose money and get hit with fees on most cases. To fight back, a staggering 90% of merchants now actively submit compelling evidence to challenge claims. Your initial dispute needs to be rock-solid to overcome their inevitable response.

This isn't about feeling sorry for the merchant. It's about being smart. Arm yourself with this knowledge so you can build a dispute that anticipates and dismantles their arguments before they even make them.

You can get a deeper look at how merchants build their cases in our complete guide to chargeback representment.

What to Do After the Bank's Decision

The waiting game is finally over. You’ve been on pins and needles, and now the bank has made a decision. This is the moment of truth, but it’s critical to remember that their initial ruling isn’t always the final word.

What you do next depends entirely on the outcome: did you win or lose?

If the bank sided with you, congratulations! That provisional credit you received is now officially yours to keep, and you’ll get a notification confirming it. For most people, this is the end of the road. The case is closed, and the money is safely back in your account.

Still, it’s always a smart move to double-check your statement one last time to make sure everything lines up. I’d also recommend holding onto your evidence for a few more months, just in case. But for the most part, you can breathe a sigh of relief.

When the Bank Denies Your Claim

Getting that denial notice can feel like a punch to the gut, especially when you’re absolutely certain you were in the right. But don't throw in the towel just yet. An initial loss doesn't mean you're out of options—it just means it’s time to prepare for the next round.

Your very first move should be to carefully read the bank’s explanation. They are legally required to tell you exactly why they denied your claim. Did the merchant come back with compelling evidence, like a delivery confirmation you couldn't refute? Or was your own evidence just not strong enough to make your case? Understanding their reasoning is the key to planning your appeal.

A denial is not a dead end. It’s an opportunity to strengthen your case. Often, a dispute is lost because of a single missing piece of evidence or a misinterpretation of the facts. Finding and fixing that weak spot is your key to winning an appeal.

If you’re convinced the bank made a mistake or you've uncovered some new, game-changing evidence, you can absolutely escalate the issue.

Appealing the Decision Through Pre-Arbitration

The official appeal process is often called pre-arbitration (or a second presentment). Think of it as your formal request for the bank to take a second look at your case. But here’s the catch: you can't just resubmit the same old information and hope for a different result. You need to bring something new to the table.

To launch a successful appeal, you need to focus on a few key things:

- Provide New Evidence: Did you find an email you overlooked before? Maybe you now have a signed document from an expert confirming the product was a counterfeit. This is the kind of fresh proof that can completely turn a case around.

- Write a Rebuttal Letter: This is your chance to address the bank’s reasons for denial point-by-point. Clearly and calmly explain why their conclusion was wrong and how your evidence—both old and new—paints a different picture.

- Act Quickly: Just like the initial dispute, appeals have strict deadlines. You need to contact your bank immediately to understand their specific timeline and procedures for filing an appeal.

Winning an appeal is definitely tougher, but it happens all the time. Your success really hinges on your ability to present a stronger, more complete case the second time around, directly countering the merchant's arguments and leaving no doubt about the validity of your dispute.

Proactive Ways to Prevent Future Disputes

While knowing how to navigate a dispute is a must, the real win is stopping them from ever happening. Think of it as prevention being the best medicine. A few simple, proactive habits can shield your finances from the headaches of fraud and billing errors, saving you a ton of time and stress down the road.

Making a few smart moves now can dramatically cut your risk. These aren't complicated, life-altering changes—just some mindful practices to keep you in the driver's seat of your accounts.

Simple Habits for Financial Safety

- Turn On Instant Alerts: The first thing you should do is set up your banking app to ping you for every single transaction. This is your personal fraud detector, letting you spot a bogus charge in seconds, not weeks.

- Use Virtual Card Numbers: When shopping online, see if your bank offers single-use or merchant-locked virtual cards. This is a game-changer. It means your real card number never gets exposed if a retailer suffers a data breach.

- Keep Digital Receipts: Ditch the overflowing shoebox of paper receipts. Instead, save digital copies to a dedicated folder in the cloud. When you need proof for a dispute months later, you'll find it in seconds.

For business owners, the stakes are different. You're not just preventing personal hassles; you're actively protecting your revenue from chargebacks. This is where automation becomes your best friend.

Merchants can use specialized tools for automated chargeback prevention that identify and stop potential disputes before they even have a chance to escalate.

Common Questions About Disputing Transactions

Even after you know the steps, a few questions always seem to pop up when you're staring down a transaction dispute. Getting clear answers can make the whole process feel much less intimidating, so let's tackle the ones we hear most often.

How Long Do I Have to Dispute a Transaction?

This is a big one, and the answer isn't always as simple as you'd hope.

In the U.S., the Fair Credit Billing Act (FCBA) gives you a solid 60 days to dispute a charge. That clock starts ticking from the date the statement with the error was mailed to you, not the transaction date itself.

But here’s a pro tip: the card networks themselves, like Visa and Mastercard, are often more generous. They can give merchants and consumers a window of up to 120 days from the original transaction date. The best advice? Cut through the noise and check directly with your bank or card issuer. Their specific policy is the one that ultimately matters. Whatever you do, don't wait.

Will Disputing a Transaction Hurt My Credit Score?

Let’s clear this up right away. The short answer is no.

Filing a legitimate transaction dispute is a protected consumer right. It isn’t reported to the major credit bureaus—Equifax, Experian, or TransUnion—so it won’t directly ding your credit score.

The only way it could cause an issue is indirect. Let's say the disputed charge is reversed, but you then forget to pay the rest of your legitimate credit card balance. That late payment would be reported and could hurt your score. So, as long as you keep your account in good standing, you have nothing to worry about.

Can I Dispute a Debit Card Transaction?

Yes, you absolutely can, but the rules are a bit different, and time is even more critical.

Debit card disputes fall under the Electronic Fund Transfer Act (EFTA). Since the money comes directly from your checking account, the stakes are higher and speed is essential. You want to get that cash back in your account ASAP.

When dealing with a lost or stolen debit card, your liability is capped at just $50 if you report it within two business days. The longer you wait, the more of the fraudulent charges you could be on the hook for. The dispute process itself is similar to a credit card, but the urgency is cranked way up.

Ready to stop losing revenue to chargebacks? ChargePay uses AI to automatically fight and win disputes for you, recovering up to 80% of lost funds without you lifting a finger. See how ChargePay works.

.svg)

.svg)

.svg)

.svg)