Thinking about filing a chargeback? At its heart, the process is pretty straightforward: you contact your bank or credit card company, lay out your case, and provide evidence to get a transaction reversed. It's a powerful tool when a purchase goes wrong, but it’s important to know when and why to use it.

Understanding When a Chargeback Makes Sense

Before you jump on the phone with your bank, let's be clear: a chargeback isn't a simple "undo" button for a purchase you regret. Think of it as a consumer protection shield, designed for specific situations where a merchant didn't hold up their end of the bargain. It's your right, but it comes with responsibilities.

And it's a right that consumers are using more and more. Global chargeback volumes are projected to hit 261 million transactions in 2025 and are expected to climb to 324 million by 2028—that’s a 24% jump in just three years. The dollar value is also soaring, from an estimated $33.8 billion in 2025 to $41.7 billion in 2028. These numbers show just how important it is for both shoppers and businesses to understand the process.

Valid Reasons to File a Chargeback

So, when is it the right time to pull the chargeback lever? It really comes down to a few key situations where the merchant failed to deliver on their promise.

Here are the most common and legitimate reasons:

- Unauthorized Charges or Fraud: This is the big one. You check your statement and find a charge you know you didn't make. This is exactly what chargeback protection was designed for.

- Item Not Received: You paid for something that never showed up. If the merchant is unresponsive or can't prove it was delivered, it's time to file.

- Significantly Not as Described: The product you received is completely different from what you ordered. You bought a genuine leather jacket, and a cheap polyester one arrived. If you've received a fake, knowing how to report counterfeit products can add weight to your claim.

- Services Not Rendered: You paid for a service—like a concert ticket or a home repair—that was either canceled or never happened.

- Duplicate Billing: The merchant accidentally charged you twice for the same purchase. It happens, and a chargeback can fix it if they don't.

My rule of thumb is this: if you've made a good-faith effort to resolve the issue directly with the merchant and have hit a wall, a chargeback is your next logical step.

When a Chargeback Is the Wrong Move

Just as important is knowing when not to file a chargeback. Misusing the system can backfire, potentially getting your account flagged or even closed by your bank.

Hold off on filing a dispute in these situations:

- You haven't tried contacting the merchant first. Always give the business a chance to make it right. A direct refund is faster and less of a headache for everyone involved.

- You have buyer's remorse. Simply changing your mind about a purchase isn't a valid reason for a chargeback. That's what the store's return policy is for.

- You forgot about a recurring subscription. If you signed up for a service and just forgot to cancel, the charge is technically valid. Contact the company to cancel all future payments instead.

Should You File a Chargeback or Request a Refund?

Confused about which path to take? This quick guide breaks down the best first move for common situations.

Ultimately, trying to work with the merchant first is almost always the right call. But when that fails, the chargeback process is there to protect you.

Understanding these distinctions is crucial. For a deeper look, check out our guide on the most common https://www.chargepay.ai/blog/reasons-for-a-chargeback. It’ll help you build a stronger, more legitimate case right from the start.

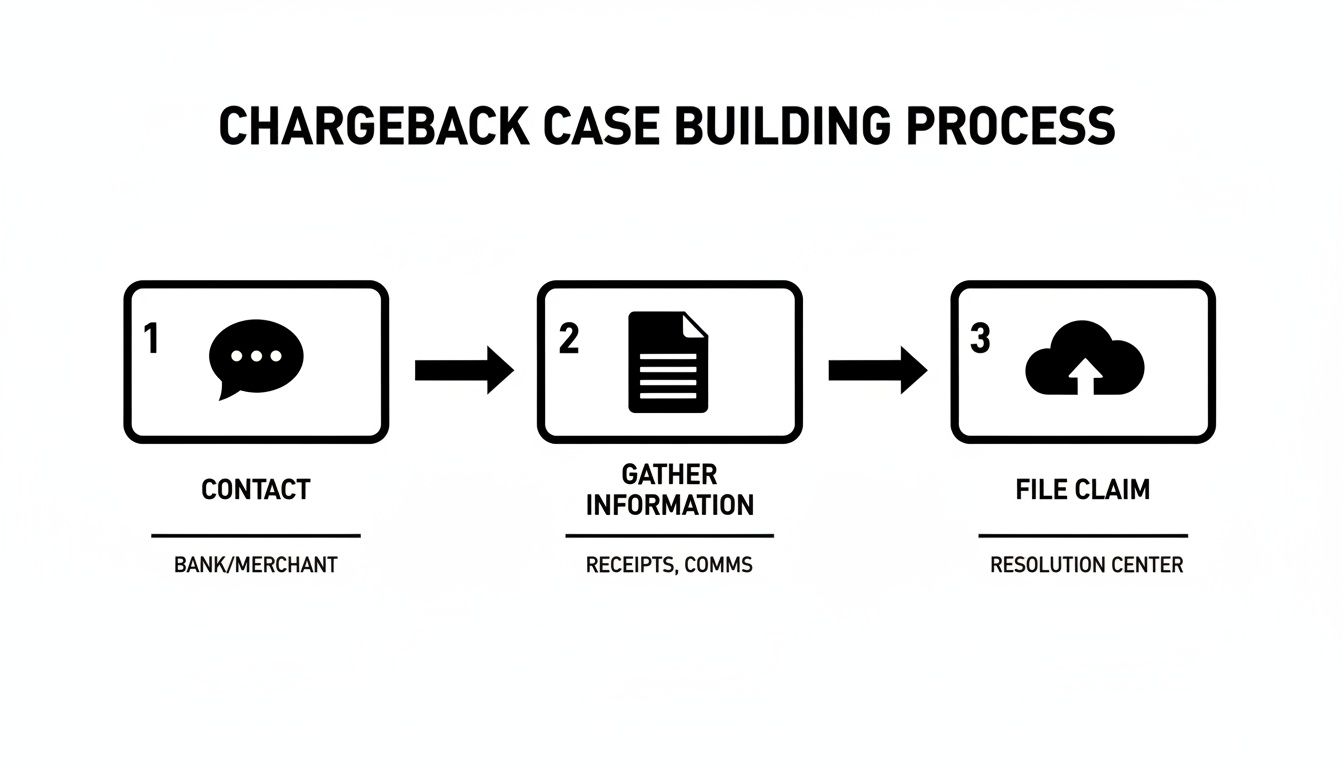

Your Pre-Filing Checklist for a Stronger Case

Before you jump straight to filing a chargeback, a little prep work can make the difference between winning and losing. Just diving in can weaken your claim, but spending a few minutes building your case file first gives you a much better shot.

Think of it like this: you're getting all your ducks in a row before you ever have to present your case to the bank's dispute department.

The first, and honestly most important, step? Contact the merchant directly. This isn't just good manners; many banks actually require you to show you tried solving the problem with the business first. A quick email or phone call can often get the issue sorted out in minutes, saving everyone the headache of a formal dispute.

Start the Conversation with the Merchant

When you get in touch, be calm, clear, and specific. Tell them exactly what went wrong and what you need to make it right. Whether you’re on the phone with a customer service rep or typing out an email, having a clear idea of what you're going to say helps keep the conversation productive.

Here’s a simple email template you can tweak:

Subject: Issue with Order #[Your Order Number]

Hello,

I'm writing about my recent order, #[Your Order Number], which I placed on [Date].

Unfortunately, the [Product Name] I received was [briefly describe the problem - e.g., damaged, not as described, wrong item]. This isn't what I was expecting.

To resolve this, I would like a [state your desired outcome - e.g., full refund, replacement item]. I've attached a few photos showing the issue.

Please let me know the next steps within the next 48 hours.

Thanks,

[Your Name]

Whatever you do, keep records of everything. If you make a call, jot down the date, time, and the name of the person you spoke with. If you use email or a support chat, save a PDF or take screenshots of the entire conversation. This paper trail is gold if the merchant blows you off or refuses to help.

Gather Your Evidence Like a Detective

After you’ve tried to work it out with the merchant, it’s time to pull together your evidence. Your goal is to create a clear, undeniable record of the transaction and the problem you're facing. The more proof you have, the stronger your case.

Here’s what your evidence file should absolutely include:

- Receipts and Order Confirmations: This is non-negotiable. You need the original proof of purchase, whether it's an email confirmation or a digital receipt.

- Photos or Videos: If an item is broken, defective, or just plain wrong, nothing beats visual proof. A short video of a gadget that won't turn on or a photo of a tear in a shirt speaks volumes.

- Product Descriptions: Grab a screenshot of the original product page from the merchant's website. This is how you prove the item you received doesn't match what they advertised.

- Communication Records: Here’s where your record-keeping pays off. Include copies of all emails, chat logs, and your notes from any phone calls. This shows the bank you made a good-faith effort to fix things directly.

- Shipping and Tracking Information: If your issue is an item that never showed up, your tracking number is key. Provide screenshots from the carrier’s website showing it was never delivered or got lost in transit.

By getting all this information organized upfront, you'll be ready for what comes next. A well-documented claim is much tougher for a merchant to fight and way easier for your bank to approve.

For a complete overview of what happens after you file, you can explore the entire card dispute process in our detailed guide. This prep work ensures you're not just asking for a refund—you're proving why you deserve it.

Filing Your Chargeback with Major Banks and PayPal

You've done the prep work, gathered your evidence, and you're sure a chargeback is the right call. Now for the main event: actually filing the claim. The good news is that most financial institutions have made this process pretty painless, whether you're working with a major credit card issuer or a digital wallet like PayPal.

While the exact buttons you click might differ from one bank to the next, the core process is generally the same. You'll need to find their dispute center—usually tucked inside your online account portal or mobile app—and lay out the key details of the transaction you’re fighting.

How to File a Chargeback with Credit Card Companies

When we talk about credit cards, the big networks like Visa, Mastercard, and American Express set the rules of the game. However, you'll never file a dispute with them directly. Your fight is with the bank that issued your card, whether that's Chase, Capital One, or Bank of America. They're your point of contact and the ones who will investigate on your behalf.

Here’s where you'll want to start:

- Online Portal or Mobile App: This is almost always the fastest and easiest route. Just log into your account, find the transaction on your statement, and look for an option like "Dispute a Transaction" or "Report an Issue."

- Phone Call: You can always go old-school and call the customer service number on the back of your card. A representative can kick off the dispute for you, but it’s a smart move to have all your evidence organized and ready to read off.

No matter which path you take, you'll be asked to provide the transaction details and select a reason code. This little code is a big deal. It tells the bank precisely why you're disputing the charge—was it fraud? Did the product never show up? Was it completely different from the description? Nailing the right code is crucial for a smooth process.

Pro Tip: When you're filling out the dispute form, keep it clean and concise. Stick to the facts you’ve already documented. This isn't the time for emotional language. Simply state what happened, what you were promised, and how the merchant dropped the ball.

Thinking about the entire process, from that first contact with the merchant to gathering your proof and finally hitting "submit," can help keep everything straight.

Each step really does build on the last, creating a solid foundation for your claim before you ever have to file it.

Navigating the PayPal Dispute Process

PayPal plays by a slightly different set of rules because it isn't a traditional bank. It has its own internal dispute resolution system, and you have to go through it first before even thinking about a formal chargeback with your linked credit card. Their system is built to push you and the seller to talk it out first.

The process breaks down into two main stages:

- Open a Dispute: Your first move is to open a dispute in PayPal’s Resolution Center. You have 180 days from the transaction date to do this. This essentially opens a direct messaging channel with the seller, giving you both a platform to work things out.

- Escalate to a Claim: If you and the seller are getting nowhere, you have 20 days to escalate the dispute into a formal claim. This is when PayPal steps in, reviews the evidence from both sides, and makes the final call.

This system has its own quirks, so getting it right is key. For a complete walkthrough, you can learn more about how to dispute a PayPal transaction in our detailed guide.

Sample Language for Your Dispute Claim

Whether you're filing with your bank or through PayPal, you'll almost certainly get a text box to plead your case. This is your moment to present the story you’ve built with your evidence.

Here’s a great example for an item that arrived "significantly not as described":

"I ordered a 'Solid Oak Bookshelf' (Order #12345) on May 15, 2024. The item that arrived on May 25th is made of cheap particle board with a thin wood-patterned laminate, not solid oak as promised in the product description. I contacted the merchant, [Merchant Name], via email on May 26th to request a return (see attached email chain), but they refused. I've attached photos of the item I received, a screenshot of the original product listing that clearly states 'solid oak,' and my order confirmation."

This statement works because it’s:

- Factual: It’s packed with dates, order numbers, and specific, objective details.

- Evidence-Based: It directly references the proof you’re attaching.

- To the Point: It gets right to the heart of the problem without any fluff.

Being this organized and clear makes the investigator's job a whole lot easier, which can only help your chances of getting a ruling in your favor. Once you hit submit, the next phase of the process begins.

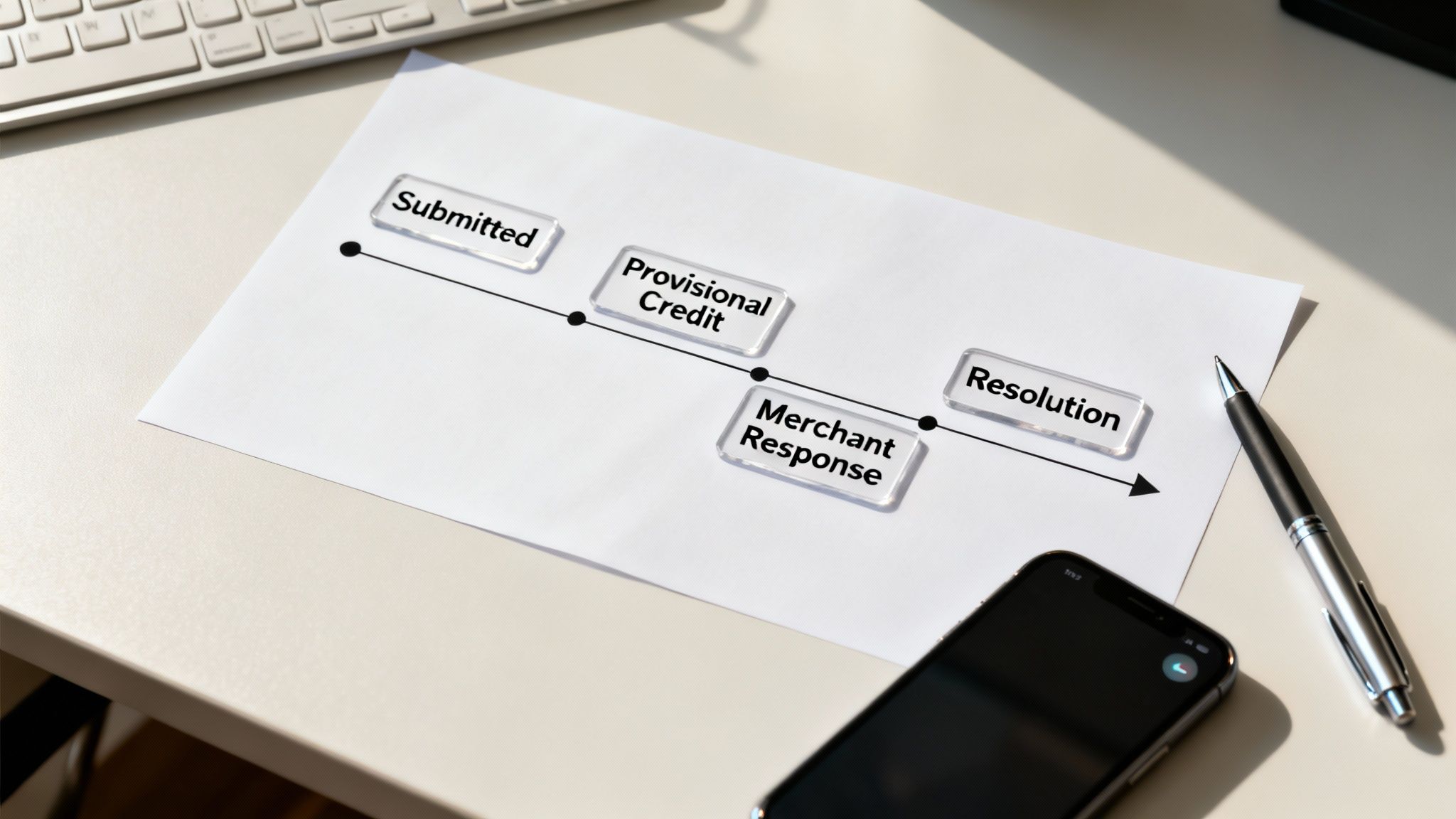

What Happens After You Submit Your Dispute?

Hitting that "submit" button on your chargeback form might feel like the finish line, but it’s really just the start of the next phase. Once you file the dispute, a well-defined process kicks off behind the scenes. Knowing what to expect can make the waiting game a lot less stressful.

The first thing that often happens is your bank may issue a provisional credit to your account. This temporarily returns the disputed amount while the investigation is underway. It’s important to remember this credit isn't permanent—it can be reversed if the final decision doesn't go in your favor.

This waiting period can be a bit nerve-wracking, but it’s a standard part of the process. For a full breakdown of the timeline, check out our guide on how long chargebacks take to resolve.

The Merchant’s Turn to Respond

After your bank reviews your initial claim, they forward it to the merchant's bank. The merchant then has a specific window of time—typically 30 to 45 days—to respond to your dispute. This is their chance to either accept the chargeback or fight it.

If they choose to fight, they’ll submit their own evidence in a process called representment. This is where the evidence you gathered becomes absolutely critical. The merchant will try to prove the charge was legitimate and that you're not entitled to your money back.

So, what kind of proof might they provide?

- Proof of Delivery: Tracking numbers and delivery confirmations showing the item arrived at your address.

- Customer Communication: Emails or chat logs where you seemed happy with the purchase or didn't mention any issues.

- Terms of Service: A copy of their terms and conditions that you agreed to at checkout.

- Usage Logs: For digital goods or services, they might show data proving you logged in and used what you bought.

Key Takeaway: The dispute process is a back-and-forth conversation managed by the banks. The merchant presents their side, and the bank compares it against your evidence. A clear, well-documented case from you makes it much harder for them to win.

This process isn't free for businesses. Each chargeback costs financial institutions between $9.08 and $10.32 just to process. In the travel industry, the average chargeback value is $120 per case. This financial sting is a big reason why merchants are motivated to challenge claims they believe are invalid. For a closer look, you can find more insights about the true cost of a chargeback on Mastercard.com.

What Happens When a Case Escalates

Most disputes are settled after the representment stage. Your bank reviews all the evidence from both sides and makes a final decision. If your evidence is stronger, you keep the money, and the case is closed. If the merchant’s evidence is more compelling, the provisional credit gets reversed, and the charge goes back on your account.

But what if the decision is still unclear? In rare instances, the case can escalate to arbitration.

Think of arbitration as the final appeal. The credit card network itself (like Visa or Mastercard) steps in to act as the ultimate judge. This stage is costly and time-consuming for both banks, so it's usually reserved for high-value or particularly complex disputes. Both sides submit their case files one last time, and the network’s decision is final and binding. While uncommon for most consumer disputes, it’s the last stop on the chargeback journey.

How Merchants View and Respond to Chargebacks

To win a dispute, it helps to understand what’s happening on the other side of the screen. For a merchant, a chargeback isn't just a simple refund. It's an unexpected, often frustrating process that costs them time, money, and can even put their ability to process payments at risk.

When you file a chargeback, the business doesn't just lose the sale amount. They also get slapped with a separate chargeback fee from their payment processor, which can be anywhere from $20 to $100 per dispute, no matter who wins. That financial penalty is exactly why even the smallest disputes get their full attention.

The Merchant's Call to Action

The moment you file a dispute, an alert goes out to the merchant. Their first move is to look at your claim and decide whether to accept the loss or fight back. That decision hinges entirely on the evidence they have on file.

They’ll immediately start digging through their records for anything that can counter your claim. This is what they're looking for:

- Proof of Delivery: A tracking number paired with a confirmation from the shipping carrier showing the package arrived at your address.

- Customer Communications: Any emails, chat logs, or support tickets where you didn't mention a problem or seemed satisfied with your purchase.

- Terms of Service: A digital record showing you checked a box and agreed to their policies (like their return or refund policy) when you bought the item.

- Digital Footprints: For services or digital goods, they might pull server logs showing you logged in, downloaded the file, or used the service you paid for.

All this evidence gets compiled into a response package and sent back to the bank in a formal process called representment. You can learn more about how merchants build these defenses by reading our detailed guide on successful chargeback representment.

The Rise of a Major Headache: Friendly Fraud

One of the biggest pain points for any online business is something called friendly fraud. This is when a customer files a chargeback on a legitimate purchase, either because they forgot about it, someone in their family used their card, or they're intentionally trying to get something for free. The business did everything right, but now they're stuck having to prove it.

And this problem is growing fast. Global chargeback volume is expected to climb by 41%, from 238 million in 2023 to 337 million by 2026. This surge is partly fueled by a sharp rise in friendly fraud, which now ranks as the second most common type of fraud merchants face. For more context, check out the full breakdown of these chargeback statistics on Chargebacks911.com.

Because of friendly fraud, merchants have become much more diligent about fighting disputes. They aren't just defending one sale; they're protecting their business from a costly and damaging trend.

Understanding this perspective is your secret weapon. When you file a chargeback, you’re not just up against a faceless company. You're presenting a case that needs to be stronger and clearer than the merchant's own records. Your organized, compelling evidence is what will cut through the noise and prove your claim is the real deal.

Common Questions About the Chargeback Process

Even when you know the steps, the whole chargeback process can feel a bit murky. Let's clear the air and tackle some of the most common questions people have. Think of this as a quick Q&A to iron out any lingering doubts so you can move forward with confidence.

How Long Do I Have to File a Chargeback?

Timing is everything, and this is where a lot of people get tripped up. While there's no single, universal deadline, a good rule of thumb is that you have about 120 days from the original transaction date to file a dispute with most major credit card networks.

But that's not the whole story. The clock doesn't always start on the day you paid. For instance, say you bought concert tickets for a show six months from now and it gets canceled. Your 120-day window would likely start from the date of the canceled event, not the date you bought the tickets. The same goes for an item you never received—the clock usually starts ticking from the expected delivery date.

Key Takeaway: Don't wait around. These deadlines can be confusing, and what ultimately matters is your specific bank's policy. The sooner you act after a problem pops up, the stronger your case will be.

Can Filing a Chargeback Hurt My Credit Score?

This is a huge fear for many, but you can breathe easy. The short answer is no, filing a legitimate chargeback will not directly ding your credit score.

A chargeback is simply a transaction dispute; it's not a reflection of your ability to pay your bills. Because of this, your bank doesn't report these disputes to credit bureaus like Experian, Equifax, or TransUnion. It won't show up on your credit report or get factored into your score.

That said, you don't want to abuse the system. If a bank spots a pattern of frequent or questionable disputes, they might decide to close your account. While that action itself isn't a negative mark, losing a line of credit reduces your total available credit, which could indirectly cause your score to dip.

What Happens If I Lose the Chargeback Dispute?

Losing a dispute is definitely frustrating, but it's not the end of the road. If the bank sides with the merchant, any provisional credit they gave you during the investigation gets taken back. The original charge goes right back on your account, and you're on the hook for paying it.

Your options get a bit thinner at this point, but you still have a few moves. You could try to appeal the decision, but you'll need some significant new evidence that you didn't include the first time around to have a real shot.

You could also try reaching out to the merchant one last time to see if you can work something else out. For bigger, more valuable items, small claims court is a possibility, but you’ll have to weigh whether the time, cost, and effort are worth the potential payoff.

Can I File a Chargeback for a Debit Card Purchase?

Yes, you absolutely can, but it's a different ballgame. The rules for debit cards generally offer less protection than what you get with credit cards.

Here’s why: debit card disputes fall under the Electronic Fund Transfer Act (EFTA), while credit cards are covered by the much more robust Fair Credit Billing Act (FCBA). This is precisely why using a credit card for online shopping or large purchases is almost always the smarter move.

These are the key differences to keep in mind:

- Tighter Deadlines: The window to report an issue with a debit transaction can be much shorter, sometimes as little as 60 days.

- Access to Your Money: When you dispute a debit card charge, that money comes directly out of your bank account. You might not get a provisional credit as quickly as you would with a credit card, leaving you out of those funds while the bank investigates.

Because of these distinctions, a credit card gives you more leverage and a better safety net when you need to dispute a charge.

If you're a merchant tired of navigating the complexities of chargebacks on your own, ChargePay can help. Our AI-powered solution automates the entire dispute process, helping you recover lost revenue and protect your business from friendly fraud without lifting a finger. Learn more about how ChargePay can boost your win rate and save you time.

.svg)

.svg)

.svg)

.svg)