That weird, unfamiliar charge on your credit card statement? It’s an unsettling feeling, but thankfully, there’s a clear path forward. Most of the time, a reason to dispute a charge boils down to a few common situations: outright fraudulent transactions, simple billing mistakes, or cases where you just didn't get what you paid for.

What It Means to Dispute a Charge

Think of a charge dispute as calling in a referee to review a questionable play on the field. You're not accusing anyone of anything just yet; you're just hitting the pause button and asking your bank or credit card company to take a closer look at a transaction you believe is wrong.

This process is one of the most powerful tools you have as a consumer. It’s designed to protect you from everything from clerical errors to outright theft. When you file a dispute, you’re formally asking a neutral third party to step in and verify if the charge is legitimate.

It happens more often than you'd think. Maybe it’s a subscription you know you canceled popping back up, or a charge from a restaurant in a city you've never even visited. Sometimes, the merchant's name on the statement is so cryptic you can't even tell what the charge is for. For a deeper look at the basics, check out our guide on the meaning of disputed charges.

Quick Guide to Common Charge Dispute Reasons

To make things a bit clearer, here’s a quick rundown of the most common reasons you might find yourself needing to dispute a charge. Think of this as your cheat sheet for identifying what went wrong.

This table covers the usual suspects, but remember that any transaction you believe is incorrect is worth investigating. Always trust your gut if something feels off.

Why Disputes Are on the Rise

That last point—not recognizing a transaction—is a huge reason why disputes are becoming more common. In fact, the total number of chargebacks across the globe is expected to reach a staggering 337 million cases. That's a massive 27% jump in just three years.

This statistic, highlighted by industry experts at Chargeblast, shows just how often people are left scratching their heads over confusing statement entries.

A charge dispute isn’t about being difficult; it's about ensuring your financial records are accurate. It’s your right as a consumer to question any transaction that doesn’t seem right and have it properly investigated.

Ultimately, this system gives you the power to protect your money when things go wrong. Whether it’s a simple duplicate charge or something more serious like receiving a counterfeit product, filing a dispute gets the ball rolling on a formal review to make things right. It’s a crucial process that keeps things fair for both you and the businesses you buy from.

Common Reasons You Can Dispute a Charge

Spotting a weird charge on your statement can be unsettling, but here’s the good news: most legitimate reasons for a dispute fall into just a few buckets. Figuring out which category your problem fits into is the first step to getting your money back.

Most of these issues aren't about kicking off a huge legal fight. They’re usually just about something going wrong between the moment you clicked "buy" and when the product (or service) was supposed to arrive. Let's break down the most common situations.

Unauthorized Transactions and Outright Fraud

This one is the most straightforward. If you see a charge you know for a fact you didn't make or approve, that’s a massive red flag for fraud. Simple as that.

It often happens when a physical card is lost or stolen, but it's just as likely your card details were swiped in a data breach. The charge could be from a store you’ve never heard of or an online shop you've never visited.

Think of this as someone dipping into your bank account without permission. The second you confirm you didn’t authorize that payment, you have a rock-solid reason to dispute a charge. You need to act fast to lock down your account.

Billing Errors and Clerical Mistakes

Sometimes, it’s not fraud—it’s just a simple mistake. Businesses are run by people and computer systems, and both can mess up. These mix-ups can lead to all sorts of incorrect charges on your statement.

If the merchant won't or can't fix the error themselves, a billing error is a totally valid reason to file a chargeback.

Here are a few classic examples you might run into:

- Duplicate Charges: You bought one coffee, but your statement shows you paid for two.

- Incorrect Amount: The price tag said $50, but you were charged $500. A simple typo at the register can cause a major headache.

- Recurring Billing Issues: You canceled that gym membership weeks ago, following their rules, but the monthly charge just popped up again.

And it's not always the merchant. Sometimes your own bank can be the source of confusing charges. It's always a good idea to keep an eye out for unexpected or incorrect bank fees, which might also be worth questioning.

Problems with Goods or Services

This category is huge, especially in the age of online shopping. It covers any situation where you paid for something but didn't actually get what was promised. At its core, it’s about a merchant failing to hold up their end of the deal.

This is where a ton of disputes come from, because you can't inspect an item in person before you buy it online. The chargeback process exists to hold businesses accountable.

Common Scenarios You Might Encounter

- Item Not Received: You ordered something, the tracking number says "delivered," but there's no package on your porch. It's vanished into thin air.

- Significantly Not as Described: This is the classic online shopping nightmare. You ordered a premium "genuine leather" jacket, and what showed up is a cheap, flimsy piece of plastic. The item is so different from the advertisement that it’s basically useless.

- Damaged or Defective Goods: The gadget you ordered arrives with a cracked screen, or it just won’t turn on. If the seller refuses to offer a replacement or a refund, a dispute is your logical next move.

- Service Not Provided: You paid a landscaper to fix your yard, but they never showed up. Or you bought concert tickets for a show that was canceled, and the venue never issued refunds.

Seeing your own situation in these examples is the key. Whether it’s a fraudulent charge, a simple typo in billing, or a product that was a complete letdown, knowing you have a valid reason to dispute a charge is the first step toward taking action and reclaiming your money.

What Is Friendly Fraud and Why It Matters

Not every charge that looks wrong is a clear case of criminal fraud or a simple billing mistake. Sometimes, the situation is a bit murkier, leading to something the industry calls friendly fraud.

Despite its harmless-sounding name, friendly fraud is a massive headache for businesses. It happens when a legitimate cardholder—that's you—disputes a charge they actually made. This usually isn’t done out of malice; it’s almost always an honest mistake.

Picture this: you're scrolling through your credit card statement and see a charge from "NVP*Software Inc." You have no clue what that is, so you assume your card was stolen and file a dispute. A week later, you realize that was the billing name for that cool photo-editing app you bought last month. That’s friendly fraud in a nutshell.

Common Causes of Accidental Disputes

This kind of dispute often stems from simple confusion or a lapse in memory. It's an easy mistake for anyone to make, but knowing the common triggers can help you avoid filing a dispute by accident.

Here are a few classic scenarios that lead to friendly fraud:

- Unrecognized Merchant Name: The business name on your statement is different from the storefront name you remember.

- Forgotten Purchases: That small, impulsive online purchase you made weeks ago completely slips your mind by the time the bill arrives.

- A Family Member's Purchase: Your teenager uses your saved card for an in-app game purchase, or your spouse buys something without mentioning it.

- Unexpected Subscription Renewals: You signed up for a free trial, forgot to cancel, and it automatically rolled into a paid subscription.

While it might seem like a small oversight, friendly fraud is a huge problem. It's estimated that up to 75% of all chargebacks are actually instances of friendly fraud, costing U.S. merchants over $170 billion each year.

Why It's Better to Contact the Merchant First

Before you hit that "dispute charge" button, it’s always a good idea to pause and double-check your own records. A quick phone call or email to the merchant can often clear things up in minutes, which is far faster than the weeks a formal chargeback process can take.

This simple step saves everyone involved time and hassle. More importantly, it helps keep the dispute system working as it should—protecting you from genuine fraud or uncooperative merchants, not from charges that are just hard to place.

For a deeper look at this topic, you can learn more about the complexities of friendly fraud in our article. By being mindful, you ensure consumer protections are there when you truly need them.

How to File a Charge Dispute Step by Step

So, you've realized you have a solid reason to dispute a charge. That's the first hurdle. The next part—actually filing the dispute—can feel a little intimidating, but it doesn't have to be. The good news is that it’s a pretty straightforward path if you just take it one step at a time.

Before you even think about calling your bank, your first move should almost always be to reach out directly to the merchant. Honestly, a quick phone call or a friendly email can often resolve the whole thing in minutes. Many issues, like accidental duplicate charges or simple shipping mistakes, are just honest errors that a business is more than happy to fix to keep you as a customer.

Gather Your Evidence

If a friendly chat with the merchant doesn’t solve the problem, it’s time to start building your case. Your bank isn’t just going to take your word for it; they need proof to back up your claim, so getting organized is key. Think of yourself as a detective putting together the clues.

Your main goal here is to create a crystal-clear timeline of what happened and prove that your claim is legitimate. This is probably the single most important part of the process. Strong evidence is what will convince your bank to rule in your favor.

Here’s a quick checklist of what you should start gathering:

- Transaction Details: Get the exact date, the amount of the charge, and the merchant's name as it shows up on your statement.

- Receipts and Invoices: Your original proof of purchase is a must-have.

- Communications: Collect copies of every email, chat log, or even just notes from your phone calls with the merchant. Dates and times are your friends here.

- Photos or Videos: If an item showed up damaged or was completely different from the description, visual proof is incredibly powerful.

- Proof of Return: If you already sent the item back, have that shipping receipt and tracking number ready to go.

Contact Your Credit Card Issuer

With all your evidence neatly organized, you're ready to make it official and file the dispute. Most banks give you a few ways to do this, but hopping onto their online portal is usually the quickest and easiest route.

You can typically find a "dispute a charge" option right in your online account or mobile app. The system will guide you through picking the transaction and selecting a reason for the dispute. This is where you’ll upload all those documents you just gathered.

If you'd rather talk to a person, you can always call the number on the back of your credit card. A representative will walk you through the process over the phone and tell you how to send in your evidence.

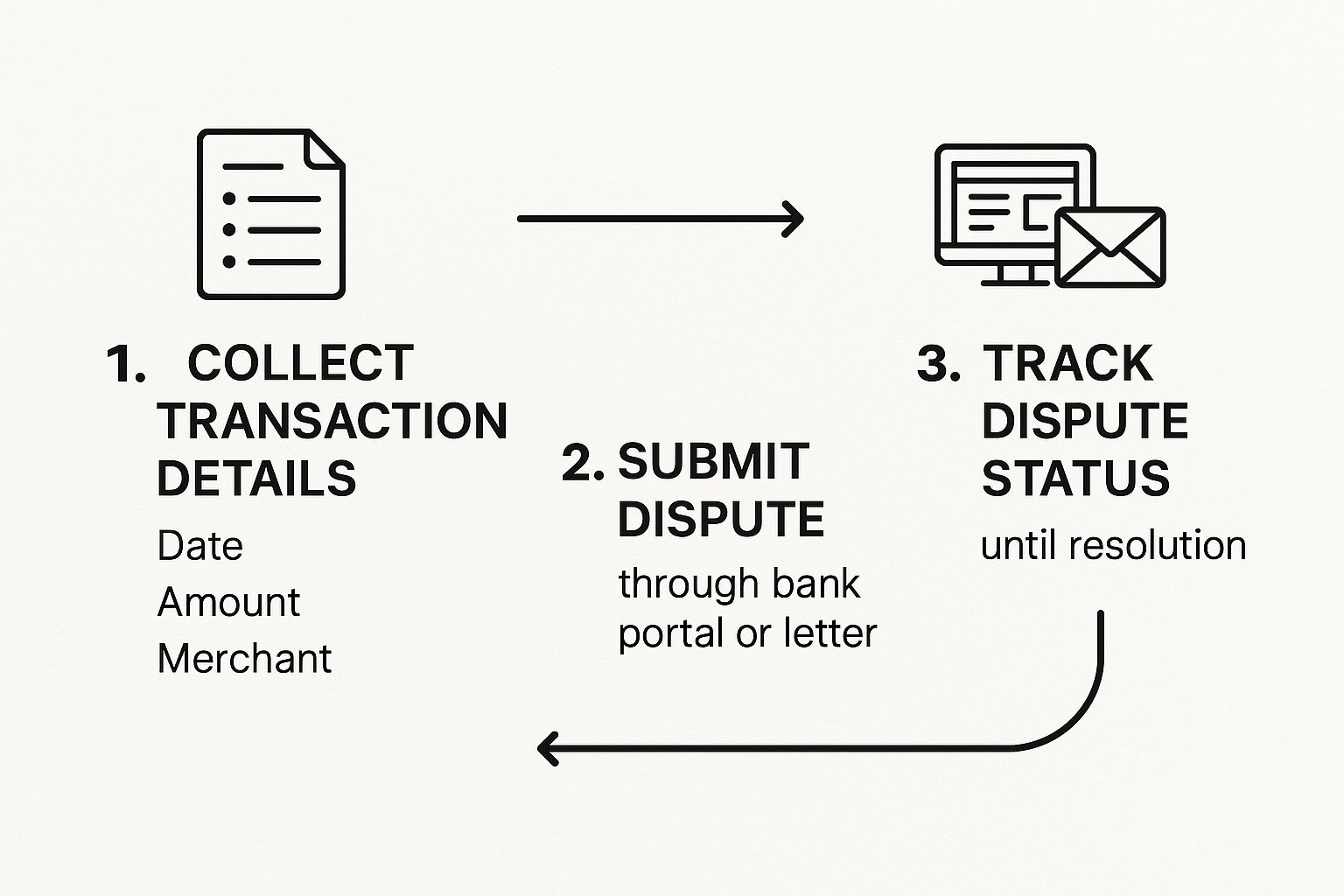

This infographic breaks down the core steps for getting your dispute submitted and tracked.

As the visual shows, it’s a logical flow from gathering your info to getting a final resolution. The key is to stay engaged with the process until a decision is made.

The most critical part of your submission is clarity. Briefly and factually explain what went wrong. Stick to the point: "I ordered a blue widget and received a broken red one. I contacted the merchant on [Date], but they did not respond."

Follow Up on Your Case

Once you've filed, the bank kicks off its investigation, which can take anywhere from 30-90 days. Don't be surprised if you get a provisional credit for the disputed amount while they work—this is pretty standard.

But don't just assume the case is closed. Keep an eye on your email and your account for any updates or requests for more information. Winning often comes down to persistence and great documentation. For a deeper dive into making sure you come out on top, check out our guide on how to win a credit card dispute.

What Happens After You File a Dispute

So, you’ve gathered your evidence and hit "submit." While it might feel like you've crossed the finish line, you've actually just kicked off the chargeback process. This isn't an instant fix; think of it as the beginning of a formal, behind-the-scenes investigation that requires a bit of patience.

The first thing you'll probably notice is a provisional credit showing up in your account for the disputed amount. This is a temporary refund your bank floats you while they look into the claim. It’s their way of making sure you’re not out of cash while things get sorted, but keep in mind—it can be taken back if your dispute doesn't pan out.

The Investigation Timeline

Once you file, your bank officially takes up your case and sends it over to the merchant's bank. This is where your evidence really starts to matter, because the merchant now gets a chance to respond. They can either accept the dispute or fight back with their own proof that the charge was perfectly valid.

This back-and-forth can take some time. On average, the whole investigation process wraps up within 30 to 90 days. The exact timeline can shift depending on how complex the case is and the specific rules of the card network (like Visa or Mastercard). If you're curious about the nitty-gritty of those deadlines, you can learn more about the chargeback time limit and how it might affect your situation.

The best thing you can do during this waiting period is stay organized. Keep a file with copies of everything you submitted and be ready to jump back in if your bank reaches out for more information.

Possible Outcomes of Your Dispute

When the dust settles, the investigation can end in a few different ways. Knowing what to expect will help you figure out your next move.

Here are the most common results:

- Dispute Approved: This is the best-case scenario. The bank sides with you, the provisional credit becomes permanent, and the case is closed. You win.

- Dispute Denied: If the merchant comes back with compelling evidence proving the charge was legitimate, your bank may rule in their favor. In this case, that temporary credit will be reversed, and the money will be taken back out of your account.

- Merchant Issues a Refund: Sometimes, a merchant will look at the situation and decide it’s less hassle to just issue a refund directly instead of going through the whole formal dispute process. This also closes the case in your favor.

If your dispute gets denied, don't throw in the towel just yet. You often have the right to appeal the decision, especially if you can bring new evidence to the table.

Common Questions About Disputing Charges

Even after you get the hang of the process, a few specific questions always seem to pop up right when you're about to pull the trigger on a dispute. Getting these last few details straight can be the difference between feeling hesitant and feeling confident.

Let's walk through some of the most common questions that might be on your mind. Remember, each reason to dispute a charge has its own rules and timelines, so knowing these little details is a big deal. It’s not just about spotting a problem; it’s about handling it the right way.

How Long Do I Have to Dispute a Charge?

Timing is everything. Seriously, it's one of the most critical parts of a successful dispute. In the United States, the Fair Credit Billing Act (FCBA) gives you a firm 60 days from the date your statement was mailed to officially let your credit card issuer know about a billing error.

That said, the major card networks like Visa and Mastercard are often a bit more generous. They might give you a window of up to 120 days from the actual transaction date. The best advice? Act the second you spot something wrong. Don't put it off, because waiting can make your case way more complicated than it needs to be.

Will Disputing a Charge Hurt My Credit Score?

This is a big one, but I’ve got good news: you can relax. As a general rule, filing a charge dispute will not hurt your credit score. Think of it as a fundamental consumer right you're entitled to use, and credit bureaus don't ding you for exercising it.

While the charge is under investigation, you aren't on the hook for paying that specific amount. But here's the catch: if the bank denies your dispute and you still refuse to pay up, that delinquency could get reported and ding your score. Just follow the process, and your credit will be fine.

Can I Dispute a Debit Card Charge?

Yep, you absolutely can, but the rules of the game are a little different. Debit card disputes fall under the Electronic Fund Transfer Act (EFTA). The protections against someone using your card without permission are strong, but they get weaker the longer you wait to report a lost or stolen card.

When it comes to issues like poor product quality or an item that never showed up, the protections aren't quite as ironclad as they are for credit cards. You can still file the dispute, but you might find the process takes longer, and getting a provisional credit while they investigate isn't always a sure thing.

What Should I Do if My Dispute Is Denied?

Getting a denial notice is a real gut punch, but it doesn't have to be the end of the line. Your first move should be to read the bank's explanation carefully. You need to understand exactly why they sided with the merchant.

If you have new evidence that you didn't include the first time around, you can often appeal the decision. Get in touch with your card issuer, ask about their appeal process, and lay out your new information clearly.

If an appeal doesn't pan out, you still have options, like filing a complaint with the Consumer Financial Protection Bureau (CFPB). For even more in-depth answers, you can check out our extensive FAQ page about chargebacks.

At ChargePay, we believe merchants shouldn't lose revenue to complicated disputes. Our AI-driven platform automates the entire chargeback process, helping you win more disputes and recover funds without lifting a finger. See how we can protect your bottom line by visiting https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)