When a customer files a chargeback, the clock starts ticking. Fast.

Generally, a cardholder has a pretty generous window to dispute a charge—anywhere from 90 to 120 days. But for you, the merchant, that window shrinks dramatically. You'll typically only get 20 to 45 days to pull together your evidence and fight back. If you miss that deadline, it's game over. You automatically lose the dispute and the money.

Why Chargeback Time Limits Matter for Your Business

Think of that merchant response window as a shot clock in basketball. The moment a dispute is filed, you’re on the clock. You have a very specific amount of time to make your play. Let that buzzer sound without taking a shot, and you forfeit possession—or in this case, the revenue from that sale.

These deadlines aren’t just arbitrary rules; they’re set by the big card networks like Visa and Mastercard. Ignoring them is one of the fastest ways to lose money. This isn't just about following rules—it's about protecting your bottom line from totally avoidable losses.

The Financial Risks of Inaction

The second a customer disputes a charge, the bank yanks those funds right out of your merchant account. That’s when your timer starts. You have to prove the transaction was legitimate, and if you're late to the party, you kiss that money goodbye for good.

This isn’t just a minor annoyance; it’s a direct hit to your cash flow. And as more business moves online, the problem is only getting bigger. The global volume of chargebacks is expected to climb from 261 million in 2025 to a staggering 324 million by 2028. That’s a 24% jump in just three years. You can dig into more of these chargeback stats to see just how serious this is.

For a merchant, every single chargeback is a potential double-whammy. You’re already out the product or service you provided, and now the revenue has been clawed back, too. Being proactive isn't just a good idea; it's your only real defense.

Beyond a Single Lost Sale

The fallout from missing a chargeback deadline goes way beyond losing one sale. Each dispute you lose dings your chargeback ratio, which is a critical health metric that payment processors watch like a hawk.

Let that ratio creep too high, and you’re in for a world of hurt. You could be looking at:

- Higher Processing Fees: Your acquirer might hike up your transaction fees to cover what they now see as a higher risk.

- Account Scrutiny: Your merchant account could get flagged for review, which often means holds on your funds.

- Account Termination: In the worst-case scenario, you could lose your ability to accept credit cards entirely.

At the end of the day, respecting these deadlines is about keeping your business financially healthy and stable. You have to be on top of it.

Decoding the Deadlines for Major Card Networks

When it comes to the time limit on chargebacks, there's no single, universal rule. It's not a one-size-fits-all situation. Each major card network—like Visa, Mastercard, and American Express—plays by its own set of deadlines.

While you'll often hear the number 120 days thrown around, the real trick is knowing when that clock actually starts ticking. Think of it this way: a customer buys something in January but doesn't spot a problem with it until March. Depending on the network's rules and the specific reason for the dispute, their window to file a claim could stretch much further than you'd think. This is why knowing the specifics for each card type is so crucial; it dictates the timeline you have to work with.

Visa and Mastercard Timelines

For the two biggest players, Visa and Mastercard, the timelines look similar on the surface but have important differences under the hood. Both generally give cardholders up to 120 days to initiate a chargeback. That clock usually starts from the transaction date, but not always. For issues like an item that never showed up, it might start from the expected delivery date instead.

But here's the critical part for you as a merchant: once that chargeback is filed, your window to respond is dramatically shorter. For a Visa dispute, you typically have just 30 days to get your compelling evidence submitted. Mastercard is a little more generous, giving you 45 days, but don't get too comfortable—this can change. For digital goods or other card-not-present transactions, that window can shrink. You can dive deeper into the specific rules by checking out this guide on the Visa chargeback time limit.

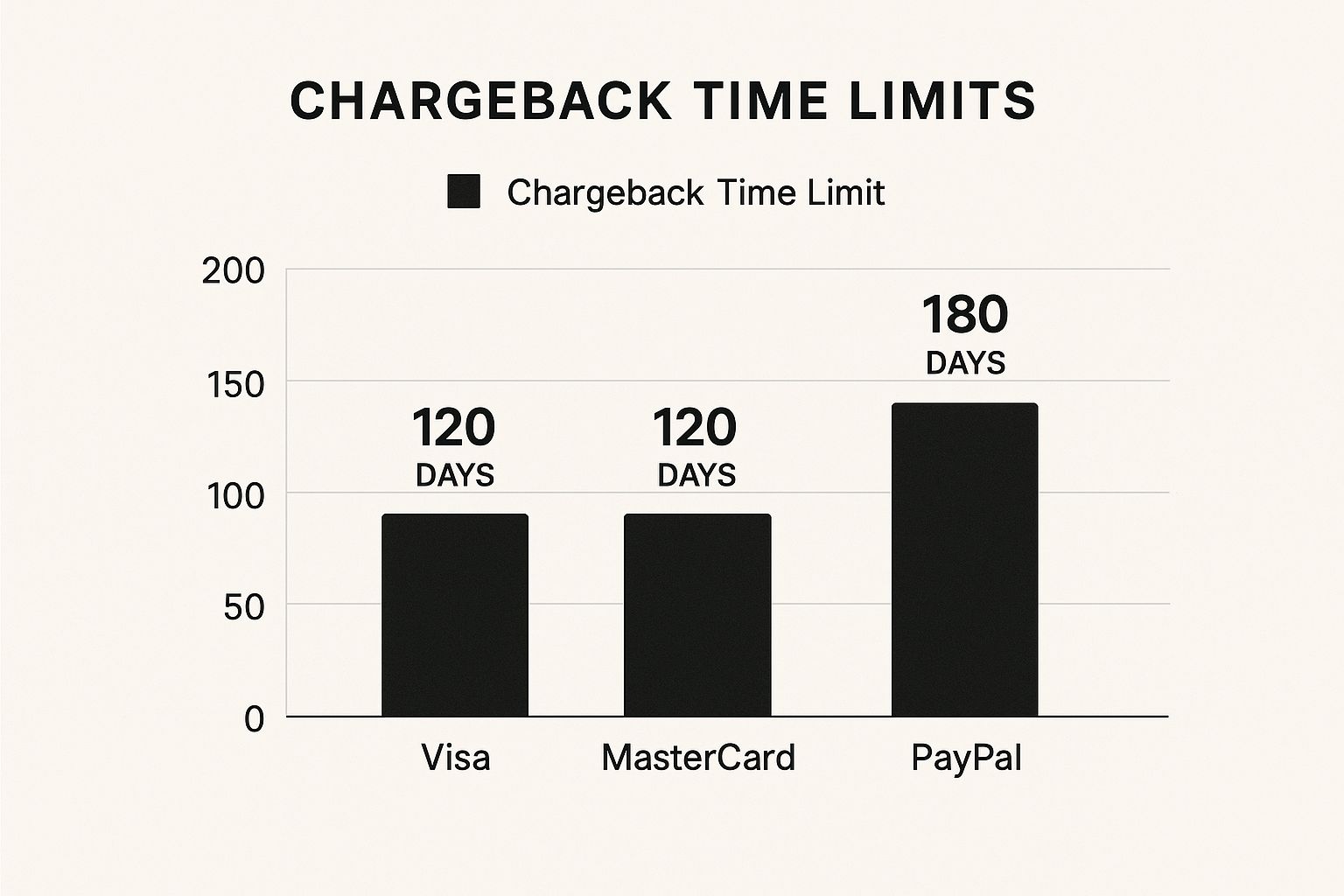

This visual breaks down the typical timeframes for cardholders across a few major payment platforms.

As you can see, while Visa and Mastercard often move in lockstep, other platforms like PayPal can give cardholders an even longer dispute window, sometimes up to 180 days.

To make it easier to see how these stack up, here’s a quick-glance table comparing the standard cardholder time limits.

Chargeback Time Limits by Card Network

Just remember, these are the cardholder's deadlines. Your response clock is much, much shorter.

American Express and Other Networks

American Express operates a little differently from the others. Since it acts as both the card network and the issuing bank, it runs a "closed-loop" system that often speeds things up. While cardholders still generally get up to 120 days to file, merchants are hit with a much tighter deadline—often just 20 days to respond to a dispute.

One crucial takeaway is that the cardholder’s deadline is not your deadline. The moment a dispute is filed, your much shorter response clock begins, and it is unforgiving. Missing it means an automatic loss.

At the end of the day, successfully managing these deadlines comes down to knowing three key things the second a dispute lands on your desk:

- Which card network is involved?

- What is the specific reason code for the chargeback?

- When did your response clock officially start?

Getting the answers to these questions is the absolute first step in building a defense that actually stands a chance.

The True Cost of Missing a Chargeback Deadline

So, what’s the big deal if the clock runs out on a chargeback dispute? It’s easy to write it off as just losing the money from a single sale, but the financial hit goes way deeper than that. When you miss a time limit on chargebacks, you’re not just losing a fight; you might be sending a signal that you’re an easy target, which can unintentionally invite more disputes your way.

If you don’t respond in time, you automatically lose. Period. And the consequences start piling up immediately. It's not just the original sale amount that vanishes from your account. Payment processors often tack on additional penalties and fees for every lost dispute. Suddenly, the total loss is way more than the value of whatever you sold. You can get the full story on these penalties by learning exactly what is a chargeback fee.

The Ripple Effect on Your Business Health

Think of each missed deadline as a small crack in your business’s foundation. One or two might not seem like much, but they add up fast, pushing your chargeback ratio higher and higher. This ratio is a key metric payment processors use to decide how risky your business is.

A rising chargeback ratio sets off a domino effect that can seriously hurt your business down the road. The fallout often looks like this:

- Higher Processing Fees: Your payment processor might hike up your transaction rates to cover their perceived risk.

- Frozen Funds: Acquirers could place a reserve on your merchant account, locking up your cash flow when you need it most.

- Account Termination: In a worst-case scenario, you could lose your merchant account entirely, making it impossible to accept card payments.

This is how one missed deadline connects directly to your ability to stay in business. Being proactive isn't just about winning disputes; it's about protecting the very core of your operations.

The Financial Weight of Each Dispute

The cost of handling chargebacks is climbing for everyone. By 2025, it's projected to cost financial institutions between $9.08 and $10.32 just to process a single dispute. For merchants, especially in places like the U.S. where the average chargeback is $110, doing nothing is a risk you can’t afford to take.

When a merchant misses a deadline, they aren't just losing a sale. They are absorbing additional fees, damaging their reputation with processors, and potentially inviting more fraudulent claims down the road.

Understanding these financial blows really drives home the importance of every single deadline. When you factor in concepts like the psychology of loss aversion, it’s clear why these hits feel so significant. Each loss isn't just a number on a spreadsheet; it’s a direct threat to your stability and hard-earned revenue.

Common Triggers That Start the Chargeback Clock

To really get a handle on the time limit on chargebacks, you first need to know what starts the clock. It's not just about the length of the window—it's about the specific event that flings it open. Different triggers can totally change when that 120-day countdown begins for your customer, which in turn affects your own (much shorter) deadline to respond.

Think of it like a smoke detector. It doesn’t go off the moment you buy it; it goes off when it actually senses smoke. In the same way, the chargeback clock doesn't always start on the transaction date. More often than not, it begins on the "discovery date"—the day the customer first realizes something is wrong.

These triggers typically fall into three main buckets, and each one has its own quirks when it comes to timing. Getting familiar with them helps you see potential disputes coming long before they ever land on your desk.

Product and Service Issues

This is probably the most common category of them all. It covers any situation where the customer feels they didn't get what they paid for. The clock here is almost always tied to delivery or when the service was supposed to be finished.

Here are a few classic examples:

- Item Not as Described: A customer orders a blue sweater but gets a red one instead. The clock starts the moment they open that package and see the wrong item.

- Product Never Arrived: If a shipment gets lost or stuck in transit, the clock usually starts from the expected delivery date, not the day they bought it. This can push the dispute window out significantly.

- Defective Goods: The item shows up broken or just stops working a few weeks later. The day they discover the defect is what kicks off the timeline for the customer to file a dispute.

The key takeaway here is that for physical goods and services, the timeline is often linked to fulfillment. A shipping delay of two months means the chargeback window effectively starts two months later than the transaction date.

Processing and Billing Errors

Sometimes, the problem has nothing to do with the product but with the transaction itself. These kinds of errors can be sneaky because a customer might not spot them for weeks or even months, giving them a much longer period to file a dispute.

A perfect example is a recurring subscription. A customer might not be combing through their bank statements every month and only notice they’ve been charged for a service they canceled months ago. In this case, the time limit on chargebacks begins when they spot the error, not when the first incorrect charge happened. This "discovery rule" is a huge deal for merchants with subscription models. If you want a deeper dive, you can explore the various reasons to dispute a charge in our complete guide.

Unauthorized Transactions or Fraud

This category is pretty straightforward but incredibly important. When a cardholder sees a charge on their statement they don’t recognize, their first thought is usually fraud. For an unauthorized transaction, the clock starts ticking the moment they see that suspicious charge.

Since many people only review their statements once a month, the discovery could be weeks after the transaction actually happened. This is exactly why having a clear billing descriptor is so critical—a confusing one can easily be mistaken for fraud, triggering a chargeback that you could have avoided altogether.

Your Game Plan for Beating the Deadline Every Time

Knowing the rules of the chargeback game is one thing, but having a winning strategy is something else entirely. To consistently beat the time limit on chargebacks, you need a solid plan that kicks into gear the moment a transaction happens—not just when a dispute notice lands in your inbox. This isn't about reacting; it's about being prepared.

Think of yourself as a detective. The goal is to have all the evidence for a case neatly organized in a file before you’re ever called to court. For merchants, this means meticulous record-keeping isn't just a good idea; it's non-negotiable. Every customer interaction, delivery confirmation, and transaction detail needs to be at your fingertips.

The golden rule here is simple: the more compelling and organized your proof, the better your odds of winning. Don't wait until the clock is ticking to start digging through old emails or shipping manifests.

Set Up Your Defense System Immediately

Your first line of defense is pure speed. You can't afford to lose precious days just because a chargeback notification got buried in an overflowing inbox. Setting up instant alerts is a critical first step.

Most payment processors offer real-time notifications for new disputes. Turning these on ensures you and your team know about a chargeback the moment it’s filed. This simple action can give you a head start of several days, which is a massive advantage when you only have a 20 or 30-day window to work with.

The difference between winning and losing a dispute often comes down to the first 48 hours. A fast, organized response shows the bank you're on top of things and prevents a last-minute scramble for evidence.

Once you get that alert, your internal process should take over immediately. This is where having a clear, repeatable system becomes your greatest asset. The goal is to move from notification to evidence submission smoothly, without any guesswork.

Create a Repeatable Response Playbook

A huge part of your game plan is establishing clear internal procedures that everyone on your team understands. If you need some help structuring your process, you can learn how to write effective internal policies that leave no room for error.

Your playbook should have a few key components:

- Designated Point Person: Assign one person or a small, dedicated team to be fully responsible for managing disputes. This eliminates confusion and ensures someone always owns the process.

- Response Templates: You're going to see the same dispute reasons pop up again and again. Create pre-written templates for these common scenarios to save time and ensure your responses are always consistent, professional, and contain all the required information.

- Deadline Calendar: Use a shared calendar to mark the response deadline for every single chargeback. Treat these dates as if they're set in stone—because they are.

This structured approach transforms what can be a chaotic fire drill into a calm, manageable workflow. A comprehensive strategy for https://www.chargepay.ai/blog/chargeback-dispute-management isn't just about fighting individual claims; it's about building a system that protects your revenue automatically.

To make sure nothing slips through the cracks, use a checklist for every dispute. This ensures every step is followed and no deadline is ever forgotten.

Your Chargeback Response Checklist

When a dispute notification arrives, the clock starts ticking. This simple checklist helps ensure your team gathers all the necessary evidence and responds effectively before time runs out.

By following a systematic approach like this, you ensure you never lose a winnable case simply because you ran out of time. It's about turning chaos into a predictable—and profitable—process.

Answering Your Questions About Chargeback Time Limits

Even with a solid game plan, you're bound to have questions about the finer points of the time limit on chargebacks. This area is filled with "what if" scenarios that can leave even the most seasoned merchants feeling a little uncertain. Let's clear up some of the most common questions business owners face.

We'll tackle the real-world concerns you might run into, from what happens if you miss a deadline to whether you can ever get an extension. The goal here is to give you straightforward answers so you can handle these situations with confidence, not confusion.

What Happens if I Miss a Deadline?

This is the big one, and the answer is brutally simple: if you miss the deadline, you automatically lose the dispute. There are no second chances, no do-overs, and no appeals. The funds are gone for good, awarded to the cardholder, and the case is officially closed.

Think of it like missing a flight. Once that gate closes, it doesn't matter why you were late; the plane is taking off without you. This is exactly why acting fast and tracking every case meticulously is non-negotiable. Missing a deadline doesn't just cost you the sale—it also dings your chargeback ratio.

The moment a deadline passes, your opportunity to present evidence disappears. Card networks and banks are incredibly strict on this, as these timelines are what keep the entire dispute process moving efficiently for everyone involved.

Can a Chargeback Time Limit Be Extended?

In almost every scenario, the answer is no. The deadlines set by card networks for merchants to respond are firm. You should never, ever operate under the assumption that you can get an extension. It's extremely rare and usually only happens under extraordinary circumstances, like a widespread natural disaster that shuts down business operations.

For cardholders, the "discovery rule" can sometimes feel like an extension. For example, if a customer doesn't spot a billing error for a few months, their 120-day clock might start from the day they discovered the issue, not the transaction date. But for your response as the merchant, that clock is unforgiving.

Do All Transactions Follow the Same Time Rules?

Not always. The type of transaction can definitely influence the timeline, especially with recent rule changes from networks like Mastercard. Deadlines can shift based on several factors:

- Physical vs. Digital Goods: Under new Mastercard rules, for instance, the merchant response time for digital goods can be shorter (30 days) than for physical goods where you have proof of delivery (45 days).

- Recurring Payments: As we've touched on, subscription billing errors are a classic reason for disputes where the discovery date can be long after the initial transaction.

- Reason for the Dispute: The specific reason code tied to the chargeback can also affect the timeline, as some codes come with their own unique rules.

This is exactly why you have to analyze each dispute individually. Don't just assume the deadline for one chargeback will be the same as the last one. For more detailed answers to specific scenarios, you can always check out our extensive chargeback FAQ page for further guidance. The key is to treat every dispute with fresh eyes and confirm the deadline every single time.

.svg)

.svg)

.svg)

.svg)