When it comes to credit card chargebacks, time isn't on your side. The whole system runs on two different clocks—one for the customer and a much, much shorter one for you, the merchant. A cardholder can typically file a dispute up to 120 days after a transaction, but businesses often get a frantic 20-45 days to fight back.

Why Chargeback Deadlines Feel Like an Uphill Battle

If you accept credit cards, you know the feeling. A chargeback isn't just an annoyance; it's a direct punch to your revenue. At the heart of the problem is a fundamental imbalance in timing.

Picture a relay race where your customer gets a four-month head start, but you have to sprint your leg of the race in just a few weeks. That’s the reality merchants face every single day.

This system was originally designed to build trust in card payments and protect consumers from fraud. It gives people plenty of time to check their statements, spot something fishy, and feel safe making purchases. But for merchants, that long window creates a ton of uncertainty and risk, turning sales you thought were closed months ago into sudden emergencies.

The Merchant's Dilemma

The tough spot you're in boils down to this conflict:

- The Long Customer Window: Cardholders have months to change their minds or file a dispute. A transaction you've long forgotten about can pop back up as a major problem.

- The Short Merchant Window: The moment a chargeback is filed, your clock starts ticking—and it moves fast. You have an incredibly tight window to find all your evidence and build a case to defend the sale.

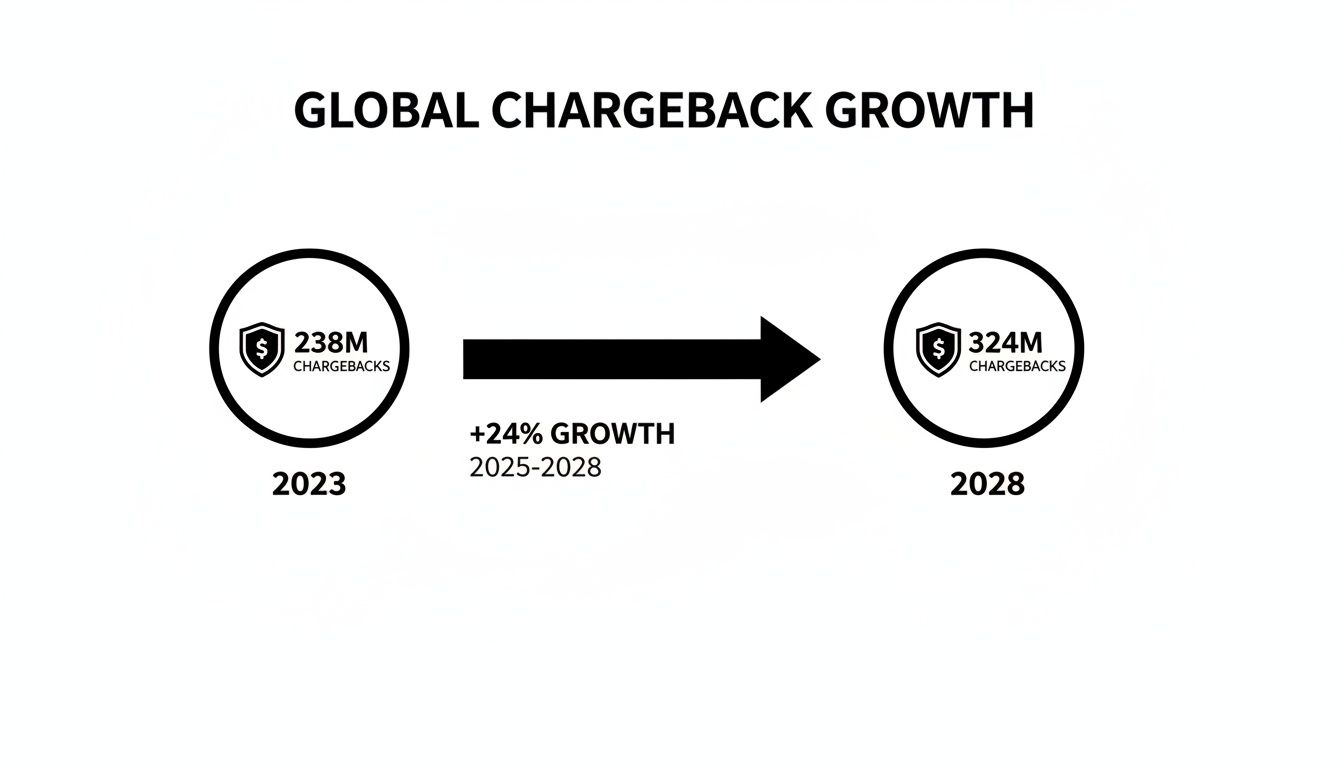

This mismatch puts enormous pressure on your entire operation. And it’s not getting any easier. In 2023 alone, Mastercard reported a staggering 238 million chargebacks filed globally, with projections showing that number will grow by 24% between 2025 and 2028. This isn't just a small-time issue; it's a massive, growing threat.

Miss a response deadline, and it's an automatic loss. The money goes back to the customer, and you're out the product, the shipping costs, and the revenue. There are no do-overs.

Ultimately, you can't afford to ignore the time limit on a credit card chargeback. It demands a crystal-clear understanding of the rules and a rock-solid plan to act fast. Knowing the specifics, like the Visa chargeback time limit, is the first step in turning a frantic, defensive scramble into a proactive strategy that protects your hard-earned revenue.

Comparing Cardholder And Merchant Timelines

When a chargeback hits your account, it’s easy to get tunnel vision and focus on a single deadline. But in reality, you’re dealing with two completely different clocks: one for the cardholder and a much, much faster one for you. Getting this difference is the first step to protecting your revenue.

Think of it as a relay race. Your customer has a long, leisurely jog to decide if they want to dispute a charge—often months after the sale. But the second they file that dispute, the baton is passed, and you’re in an all-out sprint to the finish line.

The stakes for mastering these timelines are only getting higher. Chargebacks are on the rise, and every missed deadline is a gift to friendly fraud.

As this data shows, the problem is growing, turning what might seem like a small issue into a significant threat to your bottom line if you're not prepared.

The Cardholder’s Long Leash

Cardholders are given a very generous window to file a dispute. This is a built-in consumer protection to give them confidence when they swipe, tap, or click. It ensures they have plenty of time to spot a fraudulent charge, follow up on a product that never showed up, or question a service that didn’t live up to its promise.

For most card networks, this window is typically around 120 days.

But here's where it gets a little tricky—the starting line for that 120-day clock isn't always the transaction date.

- Physical Goods: The clock might start ticking from the expected delivery date.

- Services: It could begin on the day the service was supposed to happen.

- Digital Goods: This usually starts from the transaction processing date.

This long window means a sale you thought was closed and done months ago can pop back up as a liability. A customer might not check their statement for weeks, completely forget about a purchase, and still be well within their rights to file a chargeback.

The Merchant’s Mad Dash

The moment a cardholder files that dispute, the pressure is all on you, and your window to respond is brutally short. This is where the time limit on a credit card chargeback becomes your most urgent concern. While the customer gets months to think it over, you often have just a few weeks to pull together your evidence and submit your case.

Fumbling around for order confirmations, shipping receipts, or customer service emails while the clock is ticking is a surefire way to lose money. The entire card dispute process is built for speed on the merchant’s end.

To give you a clearer picture, take a look at how these timelines stack up across the major players.

Chargeback Time Limits For Major Card Networks

These timelines can feel like a tangled mess, as each card network—and even payment processors like PayPal—sets its own rules. Here’s a quick side-by-side to help you keep them straight.

As you can see, the difference is stark. While cardholders generally get around 120 days (and PayPal gives a whopping 180 days), merchants are left with a fraction of that time. Visa gives you 30 days, Mastercard is a bit more generous at 45 days, and Amex expects a response in just 20 days.

The most important thing to remember is this: The customer’s timeline is for starting the fight. Your timeline is for fighting back. If you mix them up, you automatically lose.

Beyond the card networks, having a solid grasp of general payment terms and conditions can provide a wider context for how these disputes work. But at the end of the day, your success comes down to one thing: being ready to act the second that chargeback notice lands in your inbox.

Why Do Chargeback Time Limits Seem So Unfair?

If you’re a merchant, you’ve probably felt the frustration: a customer gets months to file a dispute, but you’re stuck with just a few weeks to fight back. The whole setup can feel lopsided and unfair. But to navigate the system, you first have to understand why it was built this way.

The entire chargeback framework was created with one goal in mind: to make people feel safe using credit cards.

Think back to when credit cards were a new, slightly scary concept. Consumers were hesitant. What if a shady business ripped them off? What if someone stole their card number? To calm these fears, the card networks (like Visa and Mastercard) created the chargeback mechanism as a powerful consumer protection tool. It was a safety net, promising cardholders they wouldn't be on the hook for fraudulent or messed-up transactions.

This original purpose explains the long timelines. A generous window gives cardholders plenty of time to check their statements, spot a problem, and get their thoughts in order before filing a dispute. It was all about building trust in a new way to pay.

A System Built for a Different Era

Here’s the problem: this system was designed for a world of mail-order catalogs and brick-and-mortar stores, not the lightning-fast world of e-commerce. The protections, while well-intentioned, are now easily abused through friendly fraud—when a customer disputes a completely valid charge.

This is where the goals of everyone involved begin to clash:

- The Cardholder: Sees the chargeback as a convenient, no-questions-asked refund button. With months to act, there's zero urgency.

- The Issuing Bank: Their priority is keeping the cardholder happy. Siding with their customer is the easiest way to maintain loyalty.

- The Acquiring Bank: They’re the middleman, processing your payments. They handle the dispute paperwork but ultimately push the financial risk back onto you.

- The Card Network: They set the rules for everyone. Their main concern is keeping their payment network trustworthy so people keep using their cards.

At its core, the logic has never changed: protect the consumer first to keep them spending. As a merchant, you're playing a game where the rules were written to favor your customer from the start.

How This Reality Shapes Your Response

Once you get that, everything else makes more sense. It explains why your response window is so tight—the system is built to get the money back into the consumer’s hands as fast as possible once they raise an alarm. The time limit on a credit card chargeback for merchants isn’t there to punish you; it’s a direct result of the system’s consumer-first design.

Understanding this dynamic is your key to winning. Your evidence can't just prove you were right; it has to prove it within the network's rules, directly countering the customer's claim. You’re not just making a case—you’re making it inside a framework that was never built with you in mind.

Common Exceptions That Change the Deadlines

Just when you think you have the standard 120-day rule down, the chargeback system throws a curveball. The reality is, the time limit on a credit card chargeback isn't always a straight line from the day the purchase was made. A few common exceptions can hit the reset button on that clock, leaving you exposed to disputes you thought were long in the past.

Getting a handle on these special cases is absolutely critical. A transaction that feels ancient can suddenly pop up as a brand-new chargeback, catching you completely off guard if you aren't ready for the system's quirks.

Let's break down the most frequent scenarios where the standard deadlines get bent, so you can see them coming before they impact your revenue.

Recurring Billing and Subscriptions

For any business built on subscriptions—think SaaS platforms, streaming services, or monthly membership boxes—the chargeback clock operates on a different schedule. When a customer disputes a recurring payment, the timeline doesn't start from their initial sign-up date.

Instead, the dispute window is almost always tied to the date of the most recent billing cycle. This means a subscriber who has been a happy, paying customer for over a year could suddenly file a dispute on their latest charge, and the 120-day timer starts from that transaction, not the one from twelve months ago.

The takeaway for subscription merchants is simple but crucial: no customer is ever fully "safe" from a chargeback. Every single renewal payment effectively resets the dispute timer for that specific charge.

Goods or Services Not Received

This is one of the most common—and logical—exceptions to the rule. If a customer pays for a product or a ticket to an event in the future, it wouldn't be fair for their dispute window to slam shut before they even expect to get what they paid for.

In these situations, the chargeback clock usually starts ticking on the expected date of delivery or service.

- Example 1: Physical Goods: A customer orders a custom-built desk on January 1st, but the estimated delivery date is April 15th. If the desk is a no-show, their 120-day dispute window would start from April 15th, not back in January.

- Example 2: Event Tickets: Someone buys concert tickets in March for a show scheduled in August. If the concert gets canceled and they don't get a refund, the clock starts in August, which is when the "service" was supposed to be delivered.

This rule protects consumers from being left empty-handed, but it means merchants must keep meticulous records of shipping dates, delivery confirmations, and service agreements long after the initial payment is processed.

True Fraud and Processing Errors

When a chargeback is filed for true fraud—meaning a criminal stole the cardholder's information and used it without permission—the standard timelines can often be stretched. The card networks recognize that a victim of fraud might not spot the unauthorized transaction right away.

While the 120-day rule is still a solid guideline, some networks, like Visa, can allow timelines up to 540 days in certain fraud scenarios. This gives cardholders plenty of time to review their statements and catch suspicious activity they might otherwise miss.

Similarly, a processing error on the bank's end can also shift the deadlines. These cases have less to do with your actions and more to do with a glitch in the payment system. While they aren't as common, it's another reminder that the standard rules aren't always set in stone. Sometimes, the first sign of trouble isn't a full-blown chargeback but a preliminary inquiry from the bank, which is why it's so important to know the difference between retrieval requests vs chargebacks and respond to both immediately.

How to Beat the Clock and Win More Disputes

Knowing the chargeback time limits is half the battle. The other half is having a rock-solid game plan ready to go the second a dispute hits your inbox. That notification isn't just a customer complaint—it's the starting pistol for a race against time.

Every minute you waste digging through old emails or figuring out your next move is a minute you can’t get back. And let's be honest, the system is already tilted heavily in the customer's favor.

The numbers don't lie. Merchants only manage to successfully defend about 20% of their chargeback cases, while the card-issuing banks win around 75% of the time. This massive gap often comes down to one thing: time. Cardholders can have 120 days or more to file a dispute, but you, the merchant, might have less than 30 days to build your case and respond. For businesses selling internationally, the pressure is even more intense, with experts predicting that losses from chargeback fraud will spike by 40% between 2023 and 2026.

To flip those odds, you need a streamlined, repeatable process that kicks into gear the moment you’re notified.

Your Immediate Action Plan

When that dispute email lands, there’s no time to sit on it. Your only goal is to gather compelling evidence, fast, and package it in a way that directly tears down the customer’s claim. Think of it like building a mini legal case—every document you submit has to serve a purpose.

Your representment package needs to tell a powerful, easy-to-follow story that proves the transaction was legitimate. Here’s your evidence checklist—the stuff you need to grab immediately:

- Transaction and Order Details: The basics, like the order date, amount, and exactly what was purchased.

- Proof of Authorization: This is your proof the card was verified correctly. Look for AVS (Address Verification Service) and CVV (Card Verification Value) match results.

- Customer Communications: Pull up any emails, support tickets, or chat logs you have with the customer. These can be gold for shutting down claims like "product not as described."

- Proof of Delivery: For physical products, this is non-negotiable. A tracking number showing a "delivered" status—especially with signature confirmation—is your best defense against "item not received" claims.

- Terms of Service: A screenshot from checkout showing the customer clicked "I agree" to your terms, refund policy, and shipping details.

Getting these documents is just the first step. The real magic is in how you organize them into a winning narrative. For a deeper look at crafting the perfect defense, check out our guide on how to win a credit card dispute.

A disorganized pile of receipts and emails won't cut it. Your evidence must be presented clearly, with a rebuttal letter that connects each document back to the specific reason code for the chargeback.

Structuring Your Response for Maximum Impact

You're not just dumping data on the bank; you're making their job easy. Remember, the person reviewing your case is probably sifting through hundreds of these a day. A clear, concise, and well-organized response is far more likely to get the attention it deserves.

Here’s a simple structure that works:

- Start with a Strong Rebuttal Letter: Get straight to the point. Briefly introduce the transaction and state exactly why the chargeback is invalid. Directly counter the customer's claim and explain how your evidence proves them wrong.

- Organize Evidence by Relevance: Lead with your knockout punch. If the claim is "item not received," that delivery confirmation should be the very first thing they see.

- Keep It Specific to the Reason Code: Every chargeback has a reason code (like Fraud, Not as Described, etc.). Tailor your evidence to fight that specific reason. Anything else is just noise that weakens your case.

Trying to manage this process manually for every single dispute is a recipe for disaster. It's a huge time-suck and incredibly easy to make a mistake. Miss a single deadline, and you automatically lose.

This is where automation becomes a true game-changer. It transforms a chaotic, reactive scramble into a streamlined strategy for keeping your revenue. By automating evidence gathering and submission, you ensure you never miss a deadline, freeing you up to focus on growing your business instead of constantly putting out fires.

Protecting Your Revenue from Expiring Timelines

Let's cut straight to the point. When you miss a response deadline for a chargeback, you're essentially giving away your product, your shipping costs, and your revenue for free. It’s an automatic loss. No second chances.

Understanding the complex web of timelines is the foundation of a strong defense. The customer has a leisurely 120-day window to file a dispute, but you're left with a frantic 20 to 45-day sprint to respond. But just knowing the rules isn't enough when your revenue is on the line.

Shift from Reaction to Prevention

The only sustainable way to handle the intense pressure of chargeback deadlines is to stop treating every dispute like a new emergency. This constant firefighting drains your time and resources, pulling you away from what you should be doing: growing your business.

What you need is a solid, repeatable system.

That means moving beyond manual processes that are just asking for human error. Trying to track different card network deadlines with calendar reminders and sticky notes is a recipe for missed opportunities and lost money.

Every expired timeline represents a permanent hole in your revenue. It's not just about one lost sale; it's about the cumulative impact on your profitability and the message it sends that your business is an easy target for friendly fraud.

This is where a strategic shift to automation becomes a necessity, not a luxury. An automated system doesn't get distracted, it doesn't forget, and it absolutely does not miss a deadline.

Stop Letting Revenue Slip Away

Implementing an automated chargeback management system is the single most effective action you can take. These tools work around the clock to make sure every dispute is handled correctly and submitted on time, turning a chaotic process into a streamlined workflow.

By providing robust chargeback protection for merchants, these solutions automatically gather evidence, build compelling cases, and manage submissions across all your payment platforms.

It’s time to stop letting tight deadlines dictate your financial success. By embracing automation, you can protect your bottom line, recover revenue you thought was lost, and finally get back to focusing on your customers and your growth. Don't let another dollar slip through the cracks because of an expired timeline.

Frequently Asked Questions

Even when you feel like you've got a handle on the rules, the tricky details of chargeback time limits can still throw you for a loop. Let's tackle some of the most common questions merchants ask so you can act confidently when a dispute hits your dashboard.

What Happens If I Miss the Chargeback Response Deadline?

Put simply: you lose. If you miss the deadline to respond, the case is automatically closed in the customer's favor.

This means you forfeit the disputed funds, and the chargeback gets chalked up against your merchant account. There's no appeal, no second chance. It’s a permanent loss of revenue.

Think of it like a default judgment in court. If you don't show up to defend yourself, you automatically lose. That's why hitting every single deadline is absolutely non-negotiable.

Can a Customer File a Chargeback After 120 Days?

Yes, and it happens more often than you'd think. While 120 days is a common benchmark for many dispute types, several exceptions can stretch this window out much further.

- Recurring Billing: For subscriptions, the clock often resets with each new payment. A long-term customer can still dispute their most recent charge.

- Future Delivery: If a product won't be delivered for months (like a pre-order or event ticket), the dispute window starts from the expected delivery date, not the purchase date.

- True Fraud: In some confirmed fraud cases, card networks like Visa might allow the issuer to file a dispute up to 540 days after the transaction.

Never assume a transaction is "safe" just because 120 days have passed. The exceptions are where the real risk lies.

A common mistake is thinking the timeline is rigid. The reality is that the start date of the dispute clock is flexible and often depends on the specifics of the transaction and the reason for the chargeback.

Does My Product Type Affect the Chargeback Time Limit?

Absolutely. What you sell plays a huge role in when the chargeback clock starts ticking. The rules are designed to be fair to the consumer based on when they should have actually received what they paid for.

Here’s a general breakdown:

- Digital Goods: The timeline usually kicks off from the transaction date since delivery is pretty much instant.

- Physical Goods: The clock often begins on the expected delivery date, giving the customer a reasonable amount of time to receive the item.

- Services or Subscriptions: This can get a little more complex. The window might start from the date the service was supposed to be performed or from the date of the last billing cycle.

How Can I Keep Track of All the Different Deadlines?

Trying to manually track deadlines across Visa, Mastercard, Amex, and Discover—each with its own specific rules and windows—is a recipe for disaster. It's incredibly difficult, and a single human error can cost you the full amount of a sale.

This is exactly where automated chargeback management tools become a lifesaver. These platforms plug directly into your payment systems to manage the entire dispute lifecycle automatically. They flag new chargebacks, help gather the right evidence, and make sure your response is submitted well before the deadline expires, protecting your revenue without all the manual grunt work.

Stop letting missed deadlines drain your profits. ChargePay uses AI to automate the entire dispute process, ensuring you never lose revenue to an expired timeline again. Reclaim your lost revenue with ChargePay today.

.svg)

.svg)

.svg)

.svg)