Think of chargeback protection as a security system for your online store. It's a mix of strategies and tools designed to help you prevent disputes before they happen and fight them effectively when they do. Essentially, it stops money from being unfairly yanked back out of your account by a customer's bank.

Why Chargeback Protection Is Now Essential

Let's be honest—chargebacks feel like a leak in your revenue bucket. For a long time, many merchants treated them as a minor cost of doing business. Just a few drips here and there, right? But with the explosion of online shopping, those small drips have become a steady stream, draining cash and damaging your relationship with payment processors.

Ignoring them just isn't an option anymore. A single chargeback isn't just a lost sale. It's a triple hit: you lose the product, the shipping costs, and you're slapped with a non-refundable bank fee. When those start piling up, they can do real damage. We break down the full impact in our guide on how chargebacks hurt businesses.

The Growing Urgency for Merchants

This problem is only getting bigger. The more people shop online, the more card-not-present (CNP) transactions happen, which has fueled a massive spike in disputes. Global chargeback volumes are climbing fast, projected to hit 337 million cases by 2025—a staggering 27% increase from 2022.

This chart paints a clear picture of the upward trend.

The data confirms it: what used to be a manageable annoyance has ballooned into a serious financial threat that demands a dedicated game plan.

A solid chargeback protection strategy isn't just about winning back lost sales—it's about protecting your business's financial health and making sure you can keep processing payments without getting shut down.

Beyond the Financial Drain

Chargebacks aren't just about the money you lose directly. They create a huge operational headache. Your team has to drop everything to dig up evidence, write compelling dispute responses, and meet tight deadlines. All that time could have been spent growing the business.

This hidden cost can be just as damaging as the lost revenue itself. The best defense is a good offense, and that means putting a proactive plan in place. For a deep dive into practical tips, check out this great resource on preventing chargebacks. It's the first step to keeping your business safe and successful.

The Hidden Costs of a Single Chargeback

A chargeback feels like a simple refund to a customer, but for a merchant, it's a financial gut punch that sends ripples through the entire business. It's so much more than just a reversed sale. When a customer disputes a transaction, you're not just out the original purchase price. You've also lost the product you sent, the money spent on shipping, and the non-refundable processing fees you already paid.

Then comes the extra sting: your bank tacks on a separate chargeback fee, which can be anywhere from $20 to $100 per incident. It’s essentially a penalty for the dispute itself, and you have to pay it whether you win or lose the case. All of a sudden, that $50 sale you thought you made has actually cost you well over $100.

This cascade of costs is exactly why effective chargeback protection for merchants is a must-have, not a nice-to-have. To get a better handle on these penalties, you can dig deeper into what is a chargeback fee.

The Domino Effect on Your Business

The bleeding doesn't stop with direct costs. Think about the operational side. Your team has to drop everything to go on a paper chase—digging through transaction logs, pulling shipping receipts, and crafting a detailed response to fight the dispute. Every hour they spend on that is an hour they aren't spending on growing the business, helping other customers, or improving your products.

And then there's the really big one: your chargeback-to-sales ratio. This is the key number payment processors watch to gauge how risky your business is. It’s a simple calculation—the number of chargebacks you get in a month divided by your total number of sales.

If your ratio creeps over a certain line—often as low as 0.9%—processors might flag you as a "high-risk" merchant. That label can lead to much higher processing fees, frozen funds, or worst of all, losing your merchant account entirely. That means you can't accept card payments at all.

Costs Felt Across the System

It isn't just merchants feeling the pain, either. The entire payments world absorbs these costs. For example, banks and financial institutions spend between $9.08 and $10.32 on average just to handle the administrative side of a single dispute. In industries with big-ticket items, like travel, the average chargeback can hit $120 per case. These disputes are a massive financial drain for everyone involved.

A single chargeback kicks off a chain reaction of expenses, both obvious and hidden, that can seriously threaten your profitability and your business's stability. Once you see the full picture, it’s clear that a solid chargeback protection strategy isn't just another business expense—it's an essential investment in your survival.

Decoding the Different Types of Chargebacks

To win the fight against chargebacks, you have to know what you’re up against. It's like a doctor diagnosing an illness before prescribing a treatment—you can't apply a one-size-fits-all solution. Chargebacks aren't all the same; they fall into three main buckets, and each requires a unique game plan.

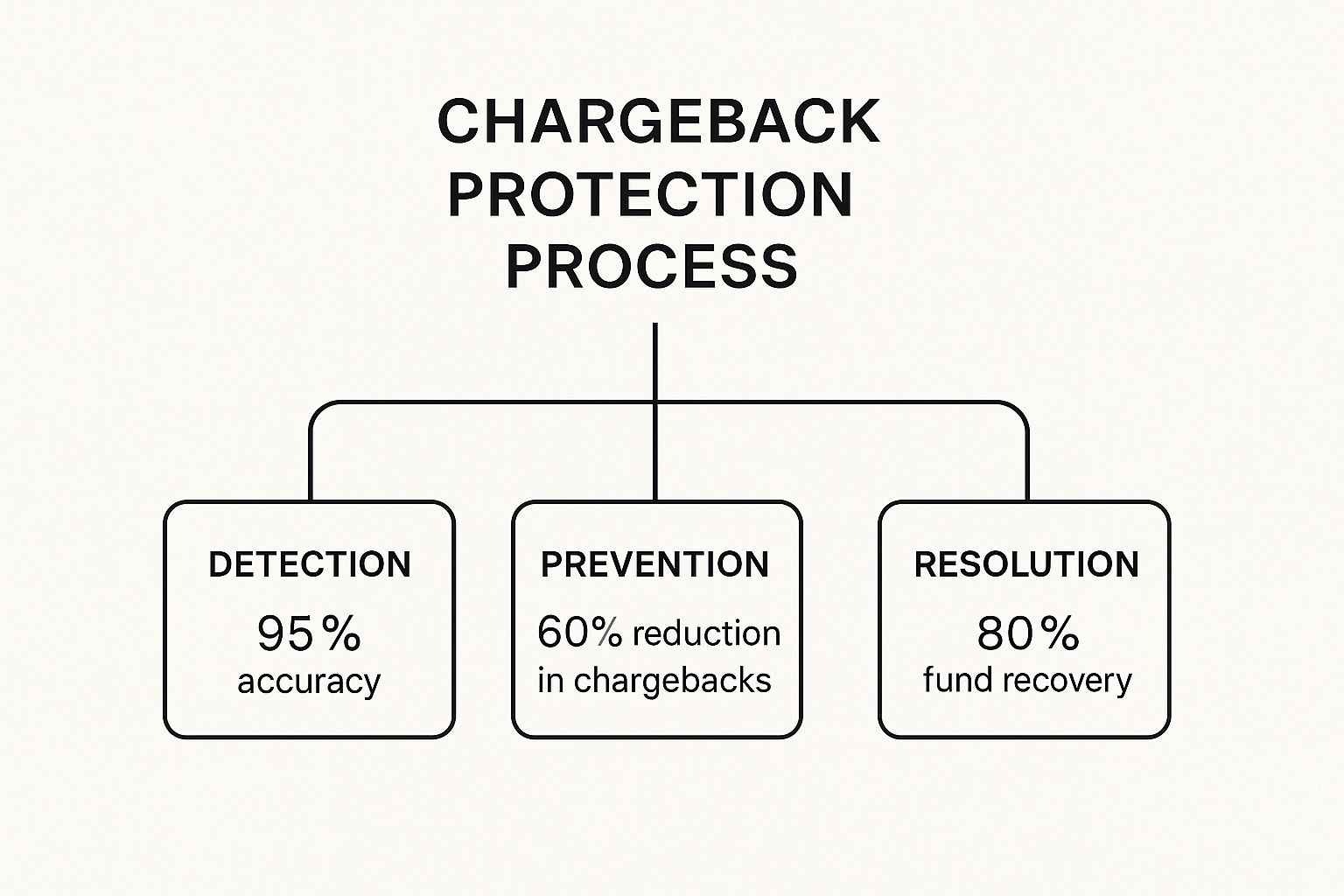

A solid protection strategy is built on layers, focusing on detecting fraud, preventing disputes before they happen, and resolving the ones that slip through.

As you can see, the goal is to stop problems early and recover revenue efficiently when a dispute does occur. This multi-layered approach is the core of any good chargeback protection for merchants plan.

Criminal Fraud: The Obvious Threat

This is what most people picture when they hear "credit card fraud." It's straight-up theft. A criminal gets their hands on stolen card details and uses them to buy something from your store. Since the actual cardholder never authorized the payment, the chargeback that follows is almost always legitimate.

Here, your best defense is a strong offense. Think of tools like Address Verification Service (AVS), CVV checks, and 3D Secure as your front-line security. They make it significantly harder for a fraudster to successfully use stolen information.

Merchant Error: The Accidental Dispute

Sometimes, the problem starts at home. A merchant error chargeback is exactly what it sounds like—a dispute that happens because of a mistake on your end. Maybe the wrong item was shipped, a customer was billed twice, or your subscription renewal policy was buried in the fine print. Even a customer who receives a damaged product and can’t get a quick reply from support is likely to go straight to their bank.

The good news? These are often the easiest chargebacks to prevent. Clear communication, transparent policies, and a responsive customer service team can resolve these issues long before they turn into a formal dispute.

Friendly Fraud: The Sneaky Saboteur

This one is the most frustrating type of chargeback by far. Friendly fraud happens when a real customer makes a legitimate purchase but disputes it later. The reason could be anything from not recognizing the charge on their statement to forgetting about a recurring payment or simply having a case of "buyer's remorse." In more malicious cases, a customer might even lie, claiming an order never arrived just to get their money back.

This is what makes friendly fraud so tough to fight. The transaction looks completely normal at first. Recent data highlights the challenge, showing that about 45% of all chargebacks are fraud-related, with friendly fraud and criminal fraud making up nearly equal shares of that number. Other common culprits are confusing billing descriptors and delivery problems. You can read the full report to understand these trends better.

Because the purchase was made by the actual cardholder, proving your side of the story requires rock-solid evidence like delivery confirmations, customer service emails, and website usage logs.

To help you get a clearer picture, let's break down how to tackle each chargeback type. The table below matches the cause with the most effective prevention tactic for each category.

Comparing Chargeback Types and Prevention Tactics

Ultimately, understanding why a chargeback happened is the first and most critical step. Once you can categorize the dispute, you can apply the right strategy and start protecting your revenue more effectively.

Building Your First Line of Defense

The best way to win a chargeback dispute is to prevent it from ever happening in the first place. Think of your business as a fortress—you need strong walls and a sharp lookout to spot threats before they get close. This is your game plan for building a defense that protects your revenue from the ground up.

Your first line of defense has nothing to do with fancy software. It’s all about clear, honest communication. So many disputes start from a simple misunderstanding. When a customer doesn't recognize a charge on their statement or can't get a quick answer from your support team, their next move is often to call their bank.

Layer One: Proactive Communication

The cornerstone of good chargeback protection for merchants is simply making your business easy to work with. That means being transparent and accessible at every step. Before you start building these defenses, it helps to understand the thinking behind them. For a great primer on the core principles, check out a complete guide to risk management.

Here are a few simple tweaks that can make a massive difference:

- Crystal-Clear Billing Descriptors: Does the name on your customer’s credit card statement actually match your brand name? A generic, confusing descriptor like "SP *WEBSERVICES123" is a known trigger for friendly fraud. Make sure it's something they'll recognize immediately.

- Accessible Customer Service: Your contact information—phone, email, live chat—should be impossible to miss. If a customer has to go on a scavenger hunt to find out how to contact you, they’ll just give up and file a dispute instead.

- An Easy-to-Find Return Policy: Don't bury your return policy in the fine print. Make it clear, fair, and easy to find on product pages and during checkout. A straightforward policy builds trust and gives customers a reason to solve problems with you directly.

Layer Two: Smart Technology

Once your communication is airtight, it’s time to bring in the tech. These tools are your digital gatekeepers, helping you spot and stop shady-looking transactions before they can turn into problems. They are absolutely critical for filtering out obvious criminal fraud.

The goal isn't to block every single transaction. It's to add just enough friction for fraudsters that they give up and move on to an easier target, all while keeping the checkout process seamless for your real customers.

These tools are your second layer of defense, working behind the scenes to confirm that the person making the purchase is who they say they are. For a deeper dive into these strategies, our article on chargeback prevention provides a detailed breakdown.

Your Essential Tech Checklist:

- Address Verification Service (AVS): This tool checks that the billing address entered at checkout matches the address the credit card company has on file. A mismatch is a classic red flag for fraud.

- CVV Checks: That little three or four-digit code on the back of a credit card is a simple but powerful security check. Requiring it proves the customer most likely has the physical card in their hand.

- 3D Secure (e.g., Verified by Visa, Mastercard SecureCode): For higher-risk transactions, this adds an extra authentication step. The customer has to enter a password or a one-time code sent to their phone to prove their identity to their bank, which adds a serious layer of security.

How Automation Strengthens Your Strategy

Trying to fight chargebacks manually is like trying to bail out a sinking ship with a thimble. It's a frantic, exhausting process of digging up evidence, filling out forms, and praying you beat the deadline. As your business grows, this manual approach just doesn't scale, and your win rate eventually takes a hit.

This is where automation comes in to do the heavy lifting. It shifts your chargeback strategy from a reactive scramble to a proactive, well-oiled machine. It’s the difference between having a single employee drowning in paperwork and having a whole team of experts working for you 24/7.

Think of it as the ultimate assistant. Instead of you manually hunting through order histories, an automated system instantly gathers all the proof needed for a dispute—transaction details, shipping confirmations, customer emails, you name it. It then packages all that information into a perfectly formatted response, customized for that specific bank's requirements.

The Power of AI in Dispute Management

The best chargeback protection for merchants today goes a step further than basic automation by adding artificial intelligence (AI) into the mix. AI-powered platforms don't just gather data; they analyze thousands of past disputes to figure out what wins and what loses. This insight allows the system to build the strongest possible case for you every single time.

This isn't just about saving time. By consistently submitting professional, evidence-backed responses, these systems can seriously boost your win rate. One study found that AI-powered automation can increase a merchant’s win rate by as much as 3.5 times compared to handling disputes the old-fashioned way.

The real game-changer with AI is its ability to learn and adapt. It spots patterns in chargeback reasons and bank decisions, constantly tweaking its strategy to improve your odds of getting your money back.

If you're looking to really get into the weeds, our complete guide to automated chargeback and dispute management provides a much deeper look at how this technology works.

Focusing Your Efforts Where They Count

Let's be honest: not all disputes are created equal. Some are clear cases of fraud that you have a great shot at winning. Others might be legitimate service issues where it’s smarter to just accept the loss. Wasting time and money fighting an unwinnable case is just as costly as ignoring a winnable one.

This is another area where AI-driven systems shine. They can actually predict the odds of winning a specific dispute based on the evidence on hand and the reason code given. This predictive insight lets you focus your energy where it matters most.

- High-Probability Cases: The system automatically compiles all the evidence and fights the disputes you are very likely to win. No more revenue left on the table.

- Low-Probability Cases: For disputes with a low chance of success, the system can flag them for you. This saves you from throwing good money after bad.

This intelligent filtering means your team can stop getting bogged down in endless paperwork and start focusing on improving the customer experience to prevent future disputes. By letting automation handle the fight, you're not just saving time—you're clawing back lost revenue and building a stronger business.

Choosing the Right Protection Service

With so many chargeback services out there, picking the right one can feel overwhelming. The trick is to find a partner that actually understands your business, not just some generic, one-size-fits-all solution.

Before you even start looking, take a look inward. How many transactions are you running each month? Are you getting a few disputes here and there, or are you drowning in them? The type of chargeback you're facing is also a huge clue. If you're constantly fighting friendly fraud, for example, you'll need a service that's a master at gathering compelling evidence, which is a different skill set than what's needed for fixing simple shipping mix-ups.

Full vs. Partial Automation

One of the first big decisions you'll make is how much you want the service to handle. Do you go for full or partial automation?

Partially automated services give you a leg up. They might send you alerts or provide templates for your responses, but your team still has to do the heavy lifting of putting it all together and submitting it. It’s better than doing everything from scratch, but it still eats up valuable time.

On the other hand, fully automated solutions take the entire process off your plate. They automatically collect the evidence, write the dispute response, and submit it for you. You don't have to do a thing. This is a game-changer for businesses that want to stop wasting time on disputes and get back to actually running their company.

The right level of automation really comes down to your team's bandwidth. If you have someone who can dedicate time to managing disputes, partial automation might be enough. But if you're a small team already stretched thin, full automation is almost always the smarter move.

Integration and Pricing Models

Next up: how easily does this service plug into what you're already using? Smooth integration with your payment gateway—whether that’s Stripe, Shopify, or PayPal—is a must. A clunky, difficult integration will create more headaches than it solves. If you're on Stripe, you can get some specific advice from our guide on Stripe chargeback protection.

Then, you need to get real about the pricing. Some companies charge a flat monthly fee, no matter how many disputes you fight or win. Others work on a success-based model, where they only get paid if they win your case and recover your money. This pay-for-performance model is really appealing because their success is tied directly to yours. If they don't win, you don't pay.

Ultimately, finding the right service boils down to asking a few simple questions:

- How much work are we willing to do? (Partial vs. Full Automation)

- Does it play nicely with our current tech? (Gateway Integration)

- How do we want to pay for the results? (Pricing Model)

Answering these honestly will quickly help you cut through the noise and find a partner that truly adds value to your business.

Still Have Questions? Let's Clear a Few Things Up

Even after seeing how chargeback protection works, it's natural to have a few questions. Let's walk through some of the most common things merchants ask when they’re weighing their options.

Is This Really Worth the Money for a Small Business?

For most small businesses, the answer is a resounding yes. Think of it this way: the cost of losing just one chargeback—when you factor in the lost product, shipping, and bank fees—can easily be more than a month’s subscription for a protection service.

When you're running on tight margins, preventing a handful of disputes each month isn't just a small win; it's a direct boost to your bottom line. It also keeps your relationship with your payment processor healthy, which is crucial.

Can’t I Just Handle Chargebacks on My Own?

You certainly can try, but it's a huge time sink. Managing chargebacks yourself means dropping everything to dig up evidence, craft a convincing rebuttal, and submit everything before the bank's strict deadline passes.

As your business scales, that time becomes your most valuable asset. Spending it on disputes means you're not spending it on growth. An automated service not only boosts your win rate but gives you that time back, making it one of the best investments you can make.

What's the Difference Between Fraud Prevention and Chargeback Protection?

This is a really important distinction, because while both protect your revenue, they do it at completely different stages of a transaction.

The core difference is this: fraud prevention tries to stop bad actors at the door, while chargeback protection helps you recover money when someone (even a real customer) disputes a charge after the fact.

Let's break it down:

Fraud Prevention is all about being proactive. Tools like Address Verification System (AVS) and CVV checks work in real-time to block obvious fraudsters before they can even complete a purchase.

Chargeback Protection is reactive. It kicks in after a customer has already filed a dispute with their bank. This is your defense against things like "friendly fraud," where a legitimate customer disputes a charge they actually made—something a fraud filter can't catch.

A solid strategy really needs both working together. You need strong prevention to minimize the number of fraudulent chargebacks coming in, and an effective protection plan to fight and win the disputes that inevitably slip through.

Ready to stop losing revenue to chargebacks? ChargePay uses AI to automate the entire dispute process, recovering up to 80% of your lost funds without you lifting a finger. See how it works at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)