A chargeback fee is the penalty your payment processor hits you with every single time a customer disputes a transaction. You can think of it as an administrative fee they charge for all the time and resources they spend managing the mess.

This fee is an extra kick in the teeth on top of the original transaction amount you have to refund if you end up losing the dispute.

A Merchant's Guide to Chargeback Fees

When a customer files a chargeback, it kicks off a formal, often lengthy process that ropes in their bank, your bank, and you. Your payment processor is stuck in the middle of this tug-of-war, and the chargeback fee is what they charge for playing referee.

The worst part? It's a non-refundable cost. That means you pay it even if you fight the dispute tooth and nail and actually win the case.

This fee is completely separate from the money being disputed. So, if a customer disputes a $100 purchase, you don't just risk losing that $100. You also get slapped with an additional fee, which usually lands somewhere between $15 to $50 per incident, depending on who your processor is.

Why Do These Fees Even Exist?

It’s easy to feel like you’re being nickel-and-dimed, but payment processors see these fees as a necessary part of doing business for a few key reasons:

- Administrative Costs: Someone has to cover the operational work of investigating the claim, talking to the banks, and shuffling all the necessary paperwork. That someone is you.

- A Nudge for Merchants: The fee acts as a strong incentive for businesses to get their act together and minimize disputes in the first place through things like clearer communication and better customer service.

- Risk Management: For processors, every chargeback is a potential financial risk. This fee helps them offset some of that exposure.

It's really important not to mix this up with a simple return. When a customer asks for their money back, that’s a direct conversation between you and them. A chargeback, on the other hand, is a formal, bank-led battle that always comes with a penalty fee. We dive much deeper into the critical differences between a chargeback vs a refund in our detailed guide.

A chargeback isn't just a reversed sale. It's a costly penalty that piles on the lost revenue, the cost of your goods, and a non-refundable administrative fee that eats directly into your profit margins.

The total cost of a chargeback goes far beyond the initial fee. It’s a snowball effect of direct and indirect costs that can really hurt your bottom line.

Here’s a quick breakdown of what a single chargeback can actually cost you:

Key Components of a Chargeback's Cost to a Merchant

As you can see, a dispute over a $100 item can easily end up costing you almost double that amount when all is said and done.

And unfortunately, these disputes are only becoming more common. Global chargeback volume is projected to jump by 24% between 2025 and 2028, ballooning to 324 million transactions every year. This surge is mostly thanks to the continuous boom in online shopping, making it more critical than ever for merchants to get a handle on preventing chargebacks.

The Hidden Costs of a Single Chargeback

That initial chargeback fee you see on your statement? Think of it as just the tip of the iceberg. The real financial damage from a single dispute cuts much deeper, creating a ripple effect that can seriously hurt your business.

When a customer files a chargeback, you don't just pay a penalty. The first thing that happens is you immediately lose the revenue from that sale—the funds are yanked right out of your account. On top of that, you’ve also lost the product you shipped, and you’re not getting that back.

Then come the operational costs. Your team has to drop what they’re doing to dig up evidence, write responses, and manage the entire dispute process. Every hour they spend fighting the claim is an hour they’re not spending on growing your business, which is a massive hidden expense.

The Long-Term Consequences

The immediate losses are painful enough, but the long-term consequences of a high chargeback rate are far more threatening. Payment processors are always watching your chargeback ratio—that’s the number of chargebacks you get compared to your total transactions.

If this ratio creeps too high (the industry danger zone is often above 0.9%), processors will slap a "high-risk" label on your business. This isn’t just a name; it comes with some serious penalties.

A rising chargeback ratio is a major red flag for payment processors. It signals risk, leading to stricter terms, higher fees, and in a worst-case scenario, the complete termination of your merchant account.

Once you land in that high-risk category, you can pretty much expect:

- Higher Processing Fees: Your standard transaction fees will likely jump across the board to offset the processor's perceived risk.

- Monthly Fines: Card networks like Visa and Mastercard don't mess around. They impose hefty fines and can place your business in monitoring programs that cost thousands each month.

- Frozen Funds: Processors might hold a chunk of your money in a reserve account to cover potential future chargebacks, which can really squeeze your cash flow.

Our guide on the Stripe chargeback fee, for example, breaks down how a major processor handles these situations. Understanding high-risk banking practices can also shine a light on why certain transactions trigger more scrutiny and higher costs.

The Growing Threat of Chargebacks

And this whole problem is only getting bigger as e-commerce continues to boom. Projections show that global chargeback volumes are expected to swell to 337 million by 2025, a huge leap from 265 million back in 2022. This surge points to growing friction in online shopping, putting more and more merchants at risk of costly disputes.

Ultimately, a high number of chargebacks can lead to account termination. Losing your merchant account means you can no longer accept credit card payments, which for many online businesses, is a death sentence. This makes managing and preventing chargebacks not just a good idea, but an essential part of your business's survival.

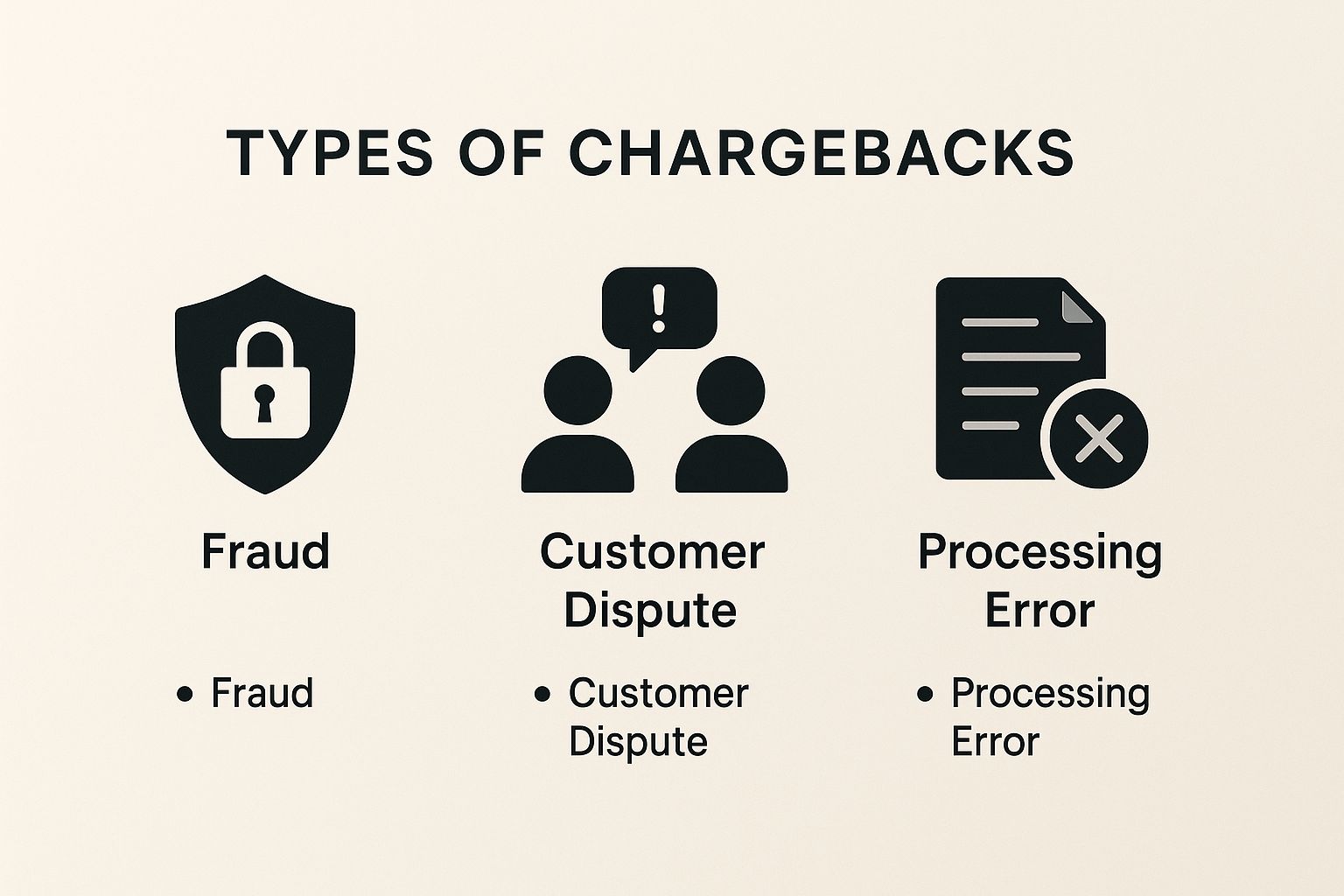

Understanding Why Customers File Chargebacks

To really get a handle on chargeback fees, you first have to get inside your customer's head and figure out why they’re filing a dispute in the first place. It’s not always as simple as it looks; the reasons are often layered and complex. Nailing down these motivations is the crucial first step to building a prevention strategy that actually works.

When you boil it all down, every chargeback falls into one of three buckets. Understanding each one helps you spot the weak points in your own business, whether it's a gap in your checkout security or a breakdown in your customer service follow-up.

This image lays out the main triggers for chargebacks, from outright criminal activity to a simple misunderstanding.

As you can see, disputes are a mix of legitimate fraud, merchant slip-ups, and customer-driven issues. Each one needs a totally different game plan to solve.

Criminal Fraud

This is the most straightforward—and scary—type of chargeback. It’s exactly what it sounds like: a criminal gets their hands on stolen credit card details and uses them to buy something from your store. When the real cardholder spots the bogus charge, they report it to their bank, and a chargeback is triggered.

Because you have zero relationship with the actual cardholder, these disputes are nearly impossible to win. The best defense here is a good offense. You need to stop these transactions before they ever get processed by using solid fraud detection tools.

Merchant Error

Let’s be honest, sometimes the fault is on our end. These chargebacks pop up because of mistakes or poor communication from the business itself. It happens to the best of us.

Common slip-ups include:

- Shipping the wrong item or a product that shows up broken.

- Using confusing billing descriptors that customers don't recognize on their bank statements. A charge from "SP*PRODUCTS" is a mystery, while "Your Awesome Brand" is instantly recognizable.

- Missing a delivery deadline or failing to send tracking info, making the customer think their order is lost in the void.

- Making it a nightmare to get a refund or having a customer service team that's impossible to reach. When they can't get help from you, they'll go straight to their bank.

The most preventable chargebacks are often the result of simple merchant errors. Clear communication, accurate order fulfillment, and accessible customer support can eliminate a huge number of these costly disputes.

Friendly Fraud

And now for the most frustrating category of them all. Friendly fraud is when a legitimate customer disputes a perfectly valid charge they actually made. This can happen for a few reasons, ranging from genuine confusion to straight-up deception.

Maybe a customer forgot about a subscription renewal, or their teenager used their card without asking. In the worst cases, a buyer just wants to get something for free and knows how to game the system. This type of chargeback has turned into a massive headache for online businesses. You can learn more about how to spot and fight these disputes in our complete guide to handling friendly fraud.

Practical Ways to Reduce Chargeback Fees

Knowing what causes a chargeback fee is one thing, but actively stopping them from happening is a whole different ballgame. The best defense is a good offense, and that means putting smart systems in place to head off disputes before they even start. Taking a proactive stance doesn't just save you money on fees; it also protects your merchant account and your relationship with your payment processor.

Think of it as your playbook for protecting revenue. The goal is to make the chargeback process completely unnecessary for your customers by giving them stellar service and crystal-clear communication from the moment they land on your site.

Strengthen Your Customer Service Fundamentals

Honestly, the easiest way to dodge a dispute is to solve a customer's problem directly. When shoppers feel like you're actually listening and have their back, they are far less likely to run to their bank for a refund.

- Make Support Easy to Find: Your contact info—phone number, email, maybe even a live chat—should be right there on every page. Don't make people dig through your site to find a way to talk to you.

- Respond Quickly and Empathetically: Set a goal to answer every single inquiry within 24 hours. A quick, helpful response can be all it takes to turn a frustrated customer into a happy one, stopping a dispute in its tracks.

- Have a Clear and Fair Return Policy: Your refund and return rules need to be simple and easy to find. Hidden fees or a complicated return process are just asking for chargebacks.

Nailing these basics builds a foundation of trust. It gives customers a better, easier path to a solution than filing a chargeback. For a deeper dive, our guide on effective chargeback prevention lays out even more advanced strategies.

Optimize Your Technical and Checkout Processes

A surprising number of chargebacks come from simple confusion or a technical hiccup during checkout. By tightening up these little details, you can wipe out a huge chunk of disputes, especially the ones tied to "friendly fraud."

A classic example? An unrecognizable name on a credit card statement. When a customer sees a charge from "XYZ*WEBSERVICES_CA," their first instinct is often to assume it’s fraud and call their bank.

Use a Clear Billing Descriptor: Make sure your billing descriptor clearly shows your business name. Something like "YourBrandName.com" is way more effective than some generic processor code and instantly tells the customer who charged them.

Beyond that, you absolutely need to have basic and advanced security measures in place to protect both your business and your customers. These technical safeguards are your first line of defense against fraud.

Here are a few non-negotiable steps to take:

- Require the CVV: Always, always ask for that three or four-digit security code on the back of the card. It’s a simple step that helps prove the customer actually has the physical card.

- Use Fraud Detection Tools: Put systems in place that can sniff out red flags, like when the billing and shipping addresses don't match or when someone tries to make too many purchases in a short time.

- Always Get Delivery Confirmation: For every physical item you ship, use a service that provides tracking and confirms delivery. This piece of paper (or digital record) is your best friend if a customer claims they never got their order.

By combining top-notch service with smart technical checks, you create a secure and transparent shopping experience. That alone will dramatically reduce the risk of getting hit with those painful chargeback fees.

How to Fight a Chargeback and Win

Even with the best fraud prevention in place, some chargebacks are going to slip through. It's just part of doing business. But when you know a dispute is illegitimate, you don’t have to just eat the loss. It’s time to fight back and defend your revenue.

This process is officially called representment, and it’s your chance to tell your side of the story to the bank.

The secret to winning is acting fast and building a rock-solid case backed by compelling evidence. As soon as that chargeback notice hits your inbox, the clock starts ticking. You usually have a very tight window to respond, so putting it off isn't an option. Your one and only goal is to prove the original transaction was legit and you held up your end of the deal.

Building Your Case with Evidence

Think about it: the bank reviewing the case has no idea who you are or who your customer is. They're an impartial third party, so they rely completely on the proof you provide. Vague claims like "the customer received the item" won't get you anywhere. You need to deliver clear, undeniable evidence that directly shuts down the customer's reason for the chargeback.

The best evidence to submit really depends on what you're selling:

- For Physical Goods: Always include delivery confirmation with a tracking number. Show proof of shipping to the customer’s verified address, and include any emails or chat logs where the customer talks about their order.

- For Digital Products or Services: Submit IP logs that show the customer accessed or downloaded the product. Server records proving usage and any emails confirming their account creation or login activity are golden here.

A well-organized representment case tells a clear story. It should walk the bank through the entire transaction, from the moment the order was placed to the final delivery, leaving no room for doubt.

Pulling all this information together can feel like a scramble, which is why getting organized from the start is so important. A well-written response, often called a rebuttal letter, is your best tool for this. For some pointers on how to structure your argument for the best results, our rebuttal letter template can help you build a winning case.

By consistently fighting back against bogus disputes, you’re not just getting your money back. You're also sending a strong signal to payment processors that you're a serious merchant who won't be taken advantage of.

Got Questions About Chargeback Fees? We've Got Answers.

When you're trying to protect your business's bottom line, the world of chargeback fees can feel a bit confusing. Let's clear up some of the most common questions merchants have about these frustrating costs.

Can I Get a Chargeback Fee Refunded if I Win the Dispute?

Unfortunately, the answer is almost always a hard no. Think of the chargeback fee as a non-refundable administrative cost your payment processor charges just for handling the dispute.

Even when you fight back and win—proving the transaction was legitimate and getting the disputed funds returned—the processor keeps that fee. It covers their time and effort. This is a huge reason why preventing chargebacks in the first place is so much better than fighting them after the fact.

What Is a Chargeback Ratio and Why Does It Matter?

Your chargeback ratio is one of the most important health metrics for your merchant account. It’s a simple calculation: your total monthly chargebacks divided by your total monthly transactions.

If this number starts creeping up past the threshold set by the major card networks (usually around 1%), alarm bells start ringing. Your business can get flagged as "high-risk," which can lead to some serious consequences like hefty fines, higher processing fees, or even losing your ability to accept card payments entirely.

Is There a Difference Between a Refund and a Chargeback?

Yes, and this is a critical distinction every merchant needs to understand. A refund is a cooperative agreement between you and your customer. You agree to return their money, and it's often a sign of good customer service. No penalties, no drama.

A chargeback, on the other hand, is a forced reversal initiated by the customer's bank. It completely bypasses you and triggers a formal dispute process involving the banks. It’s an adversarial process that always comes with a penalty fee and a black mark on your record.

A chargeback is a forced payment reversal initiated by a customer’s bank, which comes with penalty fees and hurts your merchant standing. A refund is a direct, penalty-free agreement between you and your customer.

Stop losing revenue to tedious manual disputes. ChargePay uses AI to automatically fight and win chargebacks for you, recovering up to 80% of lost funds without you lifting a finger. See how it works at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)