Ever found a charge on your credit card statement that made you scratch your head? That's where a chargeback comes in. Think of it as a financial undo button for consumers, a way for your bank to step in and reverse a transaction.

Your Simple Answer to What Is a Chargeback in Banking

A chargeback is basically a safety net woven into the entire credit card system. It’s not the same as asking a merchant for a refund. Instead, it’s a formal process where the customer’s bank forcibly pulls the money back from your business account to return it to the cardholder.

This whole system was created to build trust in card payments, especially as online shopping took off. It gives people peace of mind, assuring them they won’t be on the hook for fraudulent charges or products that never show up at their door.

The Main Players Involved

When a chargeback gets filed, it’s not just a simple conversation between you and your customer. It’s more like a multi-party negotiation, with a few key players each doing their part.

Let's break down who’s who in this process. The table below outlines each party and their specific role when a dispute is filed.

As you can see, a lot happens behind the scenes. This system, while great for protecting consumers, can create a real headache for businesses like yours.

Not only do you lose the original sale revenue, but you also get slapped with a separate penalty fee. We dig deeper into this in our guide on what a chargeback fee is.

A chargeback isn't just a refund. It's a formal dispute where banks forcibly pull funds from your account. Grasping this is the first real step toward managing them effectively.

And these disputes are becoming more common, not less. With e-commerce booming, chargebacks are following suit. In fact, between the first quarter of 2023 and 2024, e-commerce chargebacks skyrocketed by a massive 222%.

This trend makes it crystal clear: understanding how chargebacks work isn't just helpful, it's essential for survival. The process can feel overwhelming, but knowing who's involved and why it's happening is your best line of defense.

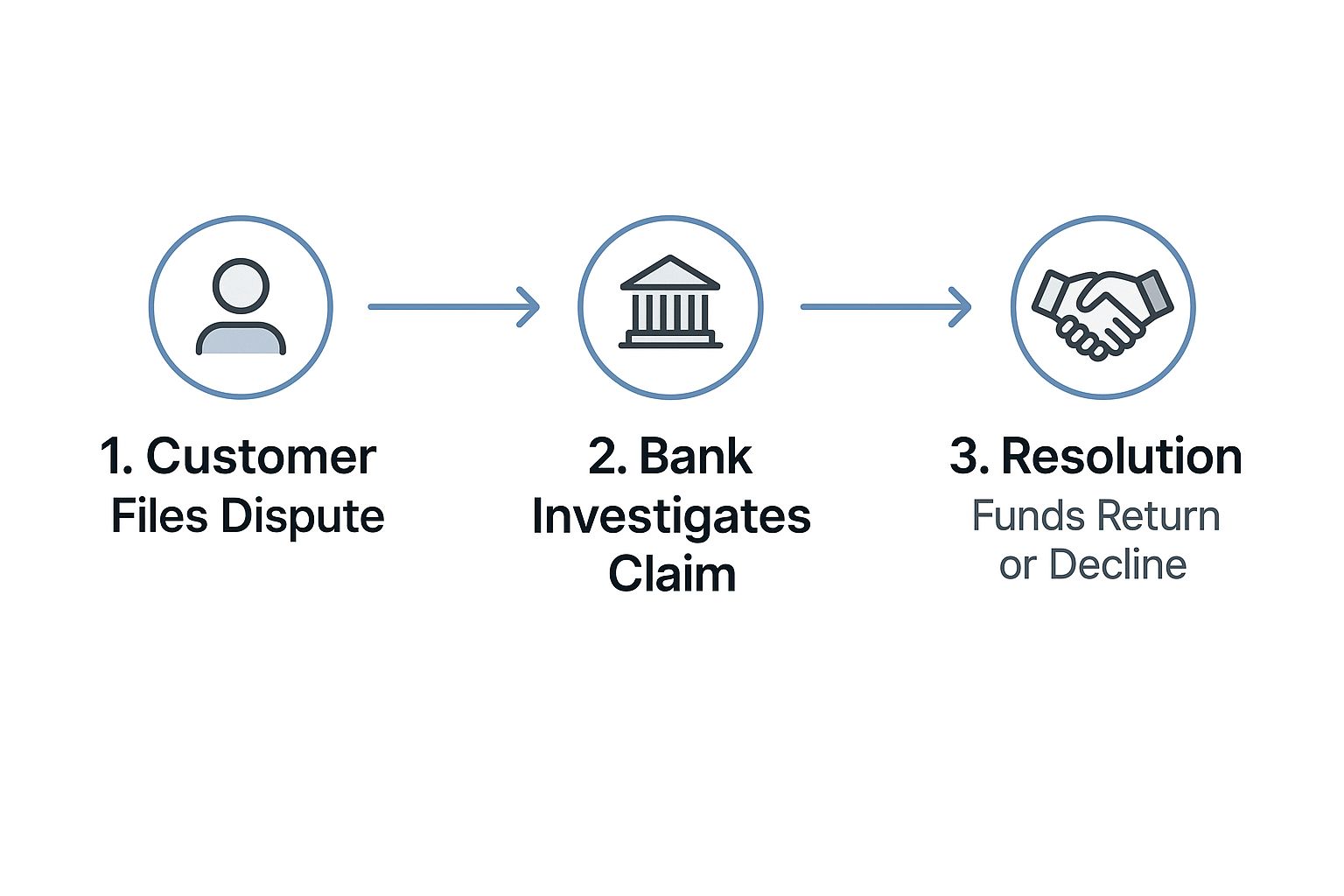

Following the Journey of a Single Chargeback

So, what actually happens when a customer disputes a charge? It isn’t just a quick reversal. It's a formal, multi-step process that can feel like a winding journey with several key stops along the way. For any business owner, understanding this lifecycle is absolutely critical.

Let's trace a single disputed transaction from the moment a customer contacts their bank to the final decision. By breaking this complex banking procedure down into a clear story, you'll see exactly what to expect and where you have the power to influence the outcome.

Step 1: The Customer Initiates the Dispute

It all kicks off when your customer spots a charge on their statement they don't recognize, disagree with, or think is fraud. Instead of reaching out to you for a refund, they call their bank—the issuing bank—and file a dispute.

This is the official start of the chargeback process. The bank looks at the customer's claim to see if it lines up with a valid reason code, which is just a standardized code explaining why the chargeback was filed (e.g., "product not received" or "unauthorized transaction").

If the bank feels the claim is legitimate, they'll often issue a provisional credit to the customer's account. This means the customer gets their money back temporarily while the investigation is underway, usually within a few days to a couple of weeks.

Step 2: The Banks Get Involved and Notify You

Once the issuing bank files the chargeback, it travels through the credit card network (like Visa or Mastercard) to your bank, known as the acquiring bank. Your bank then pulls the disputed amount, plus a non-refundable chargeback fee, directly from your merchant account.

This is often the first time you’ll hear about the problem. You'll receive a formal chargeback notification that includes the transaction details and that all-important reason code. This notice marks the start of a critical countdown.

The infographic below shows the core stages of this journey, from the customer's first move to the final resolution.

As you can see, the process involves a clear handoff from the consumer to the banks, which then puts the ball squarely in your court for the next phase.

Step 3: Investigation and Representment

Now, you're on the clock. You have a very specific, and often tight, timeframe—usually just 20 to 45 days from the dispute date—to respond. You have two choices: accept the chargeback as a loss or fight it through a process called representment.

If you decide to fight back, you need to gather and submit compelling evidence that proves the transaction was legitimate. This evidence has to directly counter the reason code provided in the notice.

So what kind of evidence actually makes a difference?

- Proof of Delivery: Think tracking numbers, delivery confirmations, or signed receipts.

- Order Confirmations: Invoices, order emails, and any communication you had with the customer.

- Usage Logs: For digital goods, this is proof that the customer logged in and used the service.

- Customer Communication: Emails or chat logs where the customer acknowledges the purchase or even expresses satisfaction.

Missing your deadline to respond is an automatic loss. It doesn’t matter how strong your evidence is; if you submit it late, you forfeit the dispute and the funds.

Once you submit your evidence, it's back in the issuing bank's hands. They review your case and will either rule in your favor—reversing the chargeback and returning the funds to your account—or they'll uphold the chargeback, making the customer’s provisional credit permanent. While there are further appeal stages like arbitration, they come with extra fees and are typically reserved for high-value disputes. For most merchants, this initial decision is the final word.

Understanding Why Chargebacks Actually Happen

To stop chargebacks, you first have to understand why they pop up in the first place. A dispute isn't just some random, unlucky event; it's a direct signal that something went wrong somewhere between a customer clicking "buy" and feeling satisfied with their purchase.

Think of it this way: every single chargeback tells a story. When you learn how to read these stories, you can spot the weak points in your business operations and shore them up before they turn into bigger, more expensive problems. Most chargebacks fall neatly into one of three main buckets.

Clear-Cut Criminal Fraud

This is the most straightforward kind of chargeback, and it’s what most people picture when they hear the term "credit card fraud." In these instances, a criminal has gotten their hands on a cardholder's payment details and used them to buy things from your store without permission.

The real cardholder eventually spots the strange charge on their statement, knows they didn't make the purchase, and immediately calls their bank. Because the transaction was genuinely fraudulent, these chargebacks are almost impossible for a merchant to win. It's a clear case of theft.

Some classic examples include:

- Stolen Physical Cards: Someone's wallet gets lifted, and the thief goes on a shopping spree before the owner can cancel the card.

- Phishing Scams: A cardholder gets tricked into typing their credit card details into a fake website, handing the keys to the kingdom over to criminals.

- Data Breaches: Hackers break into a company's database, steal a massive list of credit card numbers, and use them to make illegal purchases across the web.

Unintentional Merchant Errors

The second category is where things get a bit more complicated because the fault actually lies with your business. These chargebacks happen when a customer has a perfectly good reason to be upset because of a mistake on your end.

The good news? These are often the most preventable types of disputes. A simple tweak to your operations or a clearer line of communication can make all the difference, turning a potential chargeback into a resolved customer service ticket.

Merchant errors are frustrating because they're self-inflicted wounds. But they're also your biggest opportunity for improvement. Fixing the root cause can dramatically lower your dispute rate.

Let's look at some common slip-ups:

- Unclear Billing Descriptors: Your business shows up as "SP*WEBSOLUTIONS" on their statement instead of "Awesome Gadget Store," making the customer think it’s a fraudulent charge.

- Shipping or Delivery Problems: A package is seriously delayed, shows up damaged, or gets delivered to the wrong address entirely.

- Technical Glitches: A website bug accidentally bills a customer twice for the same purchase.

The Problem of Friendly Fraud

This is the trickiest and, unfortunately, the fastest-growing category of chargebacks. Friendly fraud happens when a customer disputes a legitimate purchase that they—or someone in their family—actually made and received. It's not criminal in the traditional sense, but it still pulls money right out of your pocket.

Sometimes it's an honest mistake, like a customer forgetting about a recurring subscription they signed up for months ago. Other times, it's a deliberate attempt to get something for free, a practice sometimes called "chargeback abuse" or "cyber-shoplifting."

Understanding the gray area of friendly fraud is absolutely critical for any online business today. For a deeper dive, you can explore our complete guide on how to handle friendly fraud. This murky territory between customer error and outright intent is where many merchants lose revenue they shouldn't have to.

Common Chargeback Triggers and How to Stop Them

To give you a head start, we've put together a quick-reference table. It breaks down some of the most common reasons a chargeback might land on your desk and gives you a practical, preventative action for each one.

Think of this table as your first line of defense. By proactively addressing these common issues, you can cut down on a significant number of preventable disputes and keep more of your hard-earned revenue.

The True Cost of Chargebacks to Your Business

When a chargeback hits, it’s all too easy to just focus on the dollar amount of the original sale. If a customer disputes a $100 order, you might just write that off as the cost of doing business. But that’s a dangerous oversimplification. The real damage runs much, much deeper, creating a ripple effect that can seriously threaten your company's financial health.

Think of a chargeback like an iceberg. The lost $100 sale is just the tip you can see above the water. Beneath the surface, a massive, unseen chunk of costs is waiting to sink your ship. These costs are a nasty mix of direct hits to your bank account and slower, indirect drains on your most valuable resources.

The Immediate Financial Damage

The most obvious hit is the money that gets yanked directly from your account. But it’s not just the sale amount that disappears into thin air. Your payment processor also slaps you with a non-refundable chargeback fee, which can be anywhere from $15 to $100 for a single dispute—and you pay that whether you win or lose.

And don't forget, you’ve probably already sent the product out the door. That means you’ve lost:

- The Original Revenue: The $100 from the sale is gone.

- The Chargeback Fee: Let's call it an average of $25.

- The Cost of Goods Sold: If that product cost you $40 to make or buy, that's gone too.

- Shipping and Handling Costs: Tack on another $10 for postage and packaging.

All of a sudden, that single $100 dispute has actually cost you $175 in cold, hard cash. This immediate financial drain is a huge reason chargebacks hurt businesses, especially for smaller merchants running on tighter margins.

The Hidden Costs That Just Keep Adding Up

Beyond the money you can count, chargebacks bring a whole host of operational headaches. A smart approach to managing operational risk is essential, because these hidden costs can be even more damaging over the long haul.

Think about the hours your team sinks into fighting these disputes. They're digging up evidence, writing rebuttal letters, and trying to navigate the ridiculously complex representment process. That’s precious time and payroll that should have been spent growing the business, not chasing down lost revenue.

The true expense of a chargeback isn't just the money you lose; it's the time and focus you sacrifice. Every hour spent fighting a dispute is an hour not spent building your business.

And this problem is only getting worse. A recent study found that 59% of merchants saw their chargeback volumes jump by over 10% in just one year. The average chargeback in the U.S. is now $110, and with global payment fraud projected to cost a staggering $49.32 billion by 2030, these expenses are on a one-way trip up.

The Long-Term Account Risk

Maybe the most dangerous cost of all is the damage done to your reputation with payment processors. Every single chargeback you get pushes your chargeback ratio higher—that’s the percentage of chargebacks you receive compared to your total number of transactions. If that ratio creeps above the industry threshold (usually around 1%), your acquiring bank will slap a "high-risk" label on your business.

This can trigger a cascade of devastating consequences. You could be hit with higher processing fees, forced to keep a larger sum of cash in reserve, or, in the worst-case scenario, have your merchant account shut down completely. For an e-commerce business, losing the ability to accept credit cards is basically a death sentence, making chargeback management a non-negotiable part of your survival strategy.

Practical Strategies to Prevent Chargebacks

You’ve heard the old saying: the best defense is a good offense. That’s especially true when it comes to chargebacks. Instead of just reacting every time a dispute hits your account, the smartest move is to stop them from happening in the first place. This isn’t just about saving a single sale; it's about protecting your overall revenue, freeing up your time, and keeping your business in good standing with payment processors.

Most of the best preventative measures aren't complicated or expensive. It all comes down to creating a clear, trustworthy, and smooth experience for your customers. You want to leave no room for the kind of confusion or frustration that pushes someone to call their bank. By putting a few key strategies into play, you can build a strong shield against a huge number of preventable disputes.

Make Your Customer Service Accessible and Responsive

When a customer runs into a problem, their first instinct shouldn't be to call their bank. Your goal is to make it faster and easier for them to get in touch with you. A customer who gets a quick, helpful answer directly from your team is far less likely to ever file a formal dispute.

To make this happen, plaster your contact information everywhere. Put your phone number, email address, and a link to a live chat widget front and center on your website—think headers, footers, and order confirmation pages. Make it impossible to miss.

The moment a customer feels they can't reach you, they'll reach out to their bank instead. Excellent, easily accessible customer service is your single best tool for chargeback prevention.

Try to respond to every single inquiry as fast as you can, ideally within 24 hours. A prompt, helpful reply shows customers you’re on their side and builds the trust you need to solve problems without the banks getting involved.

Clarify Your Policies and Billing

Confusion is a massive driver of chargebacks. When customers don't understand your policies or can't recognize a charge on their statement, they immediately assume the worst. That’s why clarity at every single step of the buying journey is non-negotiable.

Start with your billing descriptor—that’s the name that shows up on a customer's credit card statement. It needs to be instantly recognizable as your brand. A generic, cryptic name like "WEB PAYMENTS LLC" is a guaranteed way to trigger a dispute from someone who forgot they bought something from you.

On top of that, make sure all your key policies are clear, simple, and easy to find. This includes:

- Return Policy: State exactly what can be returned, the timeframe for returns, and who pays for shipping. No surprises.

- Shipping Policy: Give accurate estimates for delivery times and be honest about any potential delays.

- Terms of Service: Clearly outline the rules for things like subscriptions or recurring payments, especially how to cancel.

Being upfront builds trust and sets the right expectations from the start, which dramatically cuts down on the chances of a customer feeling like they were misled.

Use Essential Fraud Prevention Tools

While you can’t stop every criminal out there, you can easily put basic security checks in place to weed out the most obvious fraudulent transactions. These tools are standard features with most payment processors and are usually simple to turn on.

Two of the most important are the Card Verification Value (CVV) and the Address Verification System (AVS). The CVV is the three or four-digit code on the back of a credit card, which helps prove the person making the purchase actually has the physical card. AVS checks if the billing address the customer entered matches what the bank has on file.

These simple checks create an extra layer of security that can stop a lot of bad actors in their tracks. For a deeper dive into security measures, check out our guide on effective chargeback fraud prevention. Activating these basic tools is a fundamental first step in protecting your business from clear-cut fraud.

How to Fight and Win Chargeback Disputes

Getting that chargeback notification in your inbox is frustrating, no doubt. But it doesn't have to be the final word. While preventing disputes is always your best bet, you absolutely have the right to challenge any chargeback you believe is unfair. This process is called representment, and it’s your chance to fight back and get your revenue back where it belongs.

Think of representment as building a small-scale legal case. Your one job is to pull together a file of clear, compelling evidence that proves the original transaction was legit and you held up your end of the deal. Just saying "the charge was valid" won't cut it—you need to show undeniable proof.

Gathering Your Compelling Evidence

To build a winning case, you have to directly challenge the reason code that came with the chargeback. The exact evidence you'll need will change from one dispute to the next, but the goal is always the same: leave no doubt in the issuing bank’s mind that the customer’s claim has no merit.

Your evidence file needs to be airtight. Here are some of the most powerful pieces of proof you can collect:

- Order Confirmations and Invoices: These documents show exactly what the customer agreed to buy.

- Proof of Delivery: A tracking number showing a successful delivery or a signed receipt is often your silver bullet, especially for "item not received" claims.

- Customer Communications: Dig up any emails, support tickets, or chat logs where the customer talks about the purchase, asks questions about the product, or even says they're happy with it.

- Terms of Service Agreement: Proof that the customer ticked a box agreeing to your terms—especially your refund and cancellation policies—is a game-changer.

The key is to paint a complete picture of a legitimate transaction, from the moment they clicked "buy" to the moment the product landed on their doorstep. For a deeper dive, our in-depth guide to chargeback representment breaks down how to craft the perfect response.

Meeting Deadlines is Non-Negotiable

In the chargeback world, the clock is your biggest enemy. Every card network has strict, unbendable deadlines for submitting your evidence, often giving you just 20 to 45 days from the dispute date.

If you miss the submission deadline, you automatically lose the dispute. It doesn't matter if you have a mountain of irrefutable evidence; a late response is an immediate forfeit.

This tight window is where so many merchants stumble, especially when they're juggling multiple disputes at once. Staying organized and acting fast is everything. It's also worth noting that merchants facing high chargeback rates might face other issues like account holds; learning about related winning Amazon appeal processes can offer insights into handling similar high-stakes situations.

Automating Your Defense for a Better Win Rate

Manually digging for evidence, writing rebuttal letters, and keeping track of deadlines for every single dispute is a massive drain on your time and resources. As your business scales, trying to do this by hand just isn't sustainable.

This is where modern automation tools completely change the game. Solutions like ChargePay use AI to manage the entire representment process for you. The system can automatically gather all the necessary evidence, generate a perfectly formatted response customized to the specific reason code, and get it submitted long before the deadline hits.

This doesn't just free up your team to focus on growing the business; it also dramatically boosts your win rate. The unfortunate truth is that chargebacks are only becoming more common. Global chargeback volume is projected to jump from 238 million to 324 million by 2028—that's a 36% increase in just a few years. With a hands-free, intelligent system on your side, you can turn a costly headache into a managed, efficient part of your operations.

Frequently Asked Questions About Chargebacks

Even after you get the hang of the chargeback process, a few nagging questions always seem to surface. Getting clear, no-nonsense answers to these common sticking points can make all the difference in how you handle disputes.

Let's clear the air and tackle some of the most common questions we hear from merchants every day.

What Is the Difference Between a Chargeback and a Refund

At a glance, a chargeback and a refund look pretty similar—the customer gets their money back either way. But for your business, they are worlds apart in terms of process, cost, and consequence.

A refund is a simple, direct agreement between you and your customer. You agree to return their money, and it’s handled internally. It's a customer service interaction.

A chargeback, on the other hand, is a forced reversal initiated by the customer's bank. It completely bypasses you, slaps you with non-refundable penalty fees, and dings your record by increasing your chargeback ratio.

Think of it this way: a refund is a conversation, while a chargeback is a verdict handed down by the bank. One is a customer service tool; the other is a formal financial dispute you're forced into.

Can a Merchant Just Refuse a Chargeback

In a word, no. A merchant can't just "refuse" or ignore a chargeback. The moment a customer’s bank kicks off the dispute, the funds are automatically pulled from your account. The process starts whether you participate or not.

But that doesn't mean you're powerless. You absolutely can—and should—fight any chargeback that isn't legitimate. You do this through a process called representment, where you submit compelling evidence to prove the transaction was valid. Ignoring a chargeback is the same as pleading guilty and accepting the loss, so you should always be ready to respond.

How Long Does the Chargeback Process Take

Brace yourself—the chargeback timeline can be frustratingly long. Depending on the card network and how complex the case is, the whole ordeal can stretch from a few weeks to several months.

Here’s a rough idea of how it usually plays out:

- Dispute Kicks Off: The customer calls their bank. It can take a few days for the bank to process the request and officially notify you.

- Your Turn to Respond (Representment): This is where the clock really starts ticking. You typically have between 20 and 45 days from the dispute date to gather your evidence and submit it. This is a hard deadline.

- The Bank Reviews: The issuing bank takes your evidence and reviews it, which can take another 30 to 45 days.

- Things Get Complicated: If the case gets escalated to pre-arbitration or arbitration, the process can drag on for several more weeks or even months.

Because these timelines are so drawn out and the deadlines so strict, having an efficient system in place to manage disputes is critical. You can't afford to let anything slip through the cracks.

Fighting chargebacks manually is a massive drain on your time, energy, and resources. ChargePay uses AI to automate the entire dispute process for you. We handle everything from gathering evidence to submitting winning responses, so you can recover your hard-earned revenue without lifting a finger. See how much you can get back by visiting https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)