When you hear the term "credit card pre-authorization," it might sound like a bit of technical jargon, but it's something you've probably run into dozens of times without even realizing it.

Simply put, a pre-authorization is a temporary hold placed on a customer's credit card funds. It’s not an actual charge. Instead, think of it as a way to "earmark" a certain amount of money to make sure the customer's card is valid and has enough funds to cover a purchase. This is a crucial safety net for businesses, especially when the final bill isn't set in stone.

What Is a Credit Card Pre-Authorization?

The best way to understand a pre-authorization is to think about checking into a hotel. When you hand over your card at the front desk, the hotel doesn't charge you for the full stay right then and there. Instead, they place a hold on your card for the estimated total, plus a little extra for incidentals like the minibar or room service.

They aren't taking your money yet—they're just making sure it's available when you check out and the final bill is tallied. That temporary hold is the pre-authorization.

This is standard practice for any business where costs can change. Car rentals do it, gas stations do it, and even restaurants do it to account for a potential tip. It’s a temporary freeze on a portion of a customer’s credit limit before the transaction is finalized. For a deeper dive, BlueSnap offers a great overview of the mechanics behind card authorizations.

Pre-Authorization vs. Final Charge at a Glance

It’s easy for customers (and even new merchants) to get confused between a pending hold and a final charge on a statement. This table breaks down the key differences in a simple way.

Ultimately, a hold is just a placeholder, while a capture is the real deal—the final step where you get paid.

The Hold Versus the Charge

It’s so important to get this distinction right: a pre-authorization is not a final charge. The money hasn't left the customer's account. It's just unavailable for them to spend elsewhere until the hold is either completed or released. This is a common point of confusion for customers who see a "pending" transaction and assume they've already been billed.

From a merchant's perspective, a pre-authorization accomplishes two critical goals:

- It Validates the Card: First and foremost, it confirms the card is active and the details are correct. No more guessing games.

- It Verifies Funds: It checks that the customer has enough available credit to cover the expected cost of the service or product.

This simple step is a powerful safety net for your business. It protects you from the headache of declined payments and the frustration of no-shows by confirming the customer's ability to pay before you deliver a service or ship a product.

Every pre-authorization has one of two fates: it either turns into a final charge (a process called a "capture") or it's released back to the customer if the sale doesn't go through. To get the full picture, you can learn more about how all credit card transactions work in our detailed guide.

How the Pre-Authorization Process Works Step by Step

Think of a pre-authorize credit card transaction as a simple handshake agreement between your business and the customer's bank. Once you see the moves, the whole thing clicks into place. It’s a pretty simple process involving just a few key players: you, your customer’s bank (the issuer), and your payment processor.

Let's walk through the life of a typical pre-authorization, from the initial "hello" to the final settlement.

Step 1: The Authorization Request

It all kicks off the moment a customer hands over their credit card details. Whether they’re booking a hotel room online or starting a tab at your bar, you send an authorization request through your payment processor straight to their bank.

This isn't a request for money just yet. All you're doing is asking the bank, "Hey, does this person have at least $X available on their card?"

Step 2: The Bank's Response and the Hold

The customer's bank gets the ping and immediately checks the account. It confirms the card details are legit, checks the available credit, and scans for any fraud red flags. For extra safety, many online transactions now use an additional verification step. You can dig deeper into how these checks work in our guide on what 3-D Secure authentication is.

If everything checks out, the bank gives a thumbs-up by sending back an approval code. It then puts a temporary hold on the customer's funds for the amount you requested, which reduces their available credit. This is what shows up as a "pending" charge on their statement.

Key Takeaway: The money hasn't moved to your account. The bank has simply fenced it off, guaranteeing it'll be there for you to collect later. This hold usually lasts for 5 to 7 days, but it can stick around longer for businesses like hotels or car rentals.

Step 3: Capturing or Voiding the Transaction

From here, the pre-authorization can go one of two ways. Once you've provided the service or shipped the product and you know the final bill, it's time to settle up.

- Capture: You "capture" the funds. This is your signal to the bank to finalize the deal and transfer the money from the customer's account into yours. You can capture the full amount of the hold or just a partial amount if needed.

- Void/Release: If the customer cancels their order or you no longer need the hold, you can "void" the authorization. This tells the bank to release the funds, and the pending transaction vanishes from their statement, freeing up their credit. If you don't do anything, the hold will just expire on its own after its set time is up.

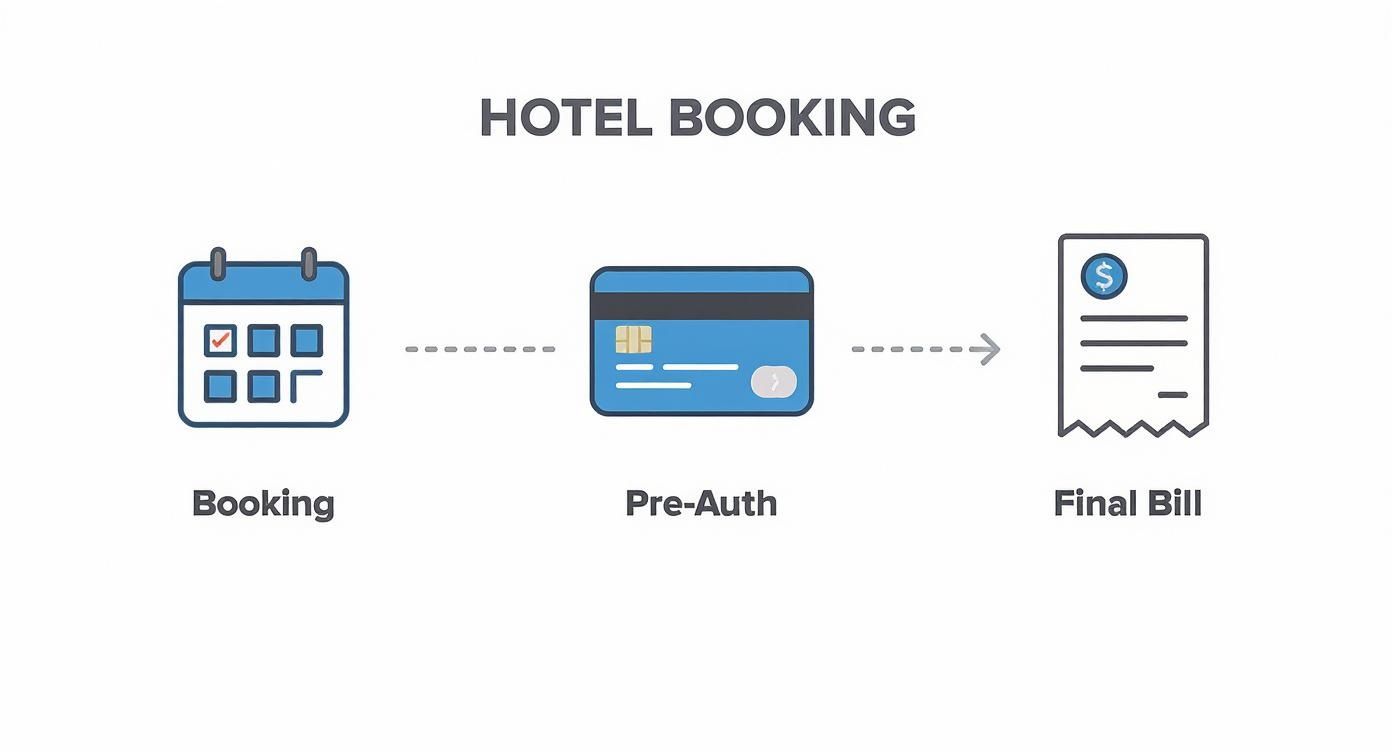

This flowchart breaks down the simple three-stage process for a common scenario like a hotel booking.

As you can see, the pre-auth acts as a critical middle step, locking in the funds after a booking is confirmed but before the final bill is actually paid.

The Big Wins: Why Your Business Needs Pre-Authorization

Alright, we've walked through how a pre-authorization works. Now for the million-dollar question: why should you bother using it? It turns out this simple step offers some serious perks, protecting your bottom line and making your entire operation run a whole lot smoother.

Think of pre-authorization as your first line of defense. It’s a quick, instant check to confirm a customer's card is real and has enough money on it before you tie up your inventory, book a time slot, or start any work. Just by doing this, you massively cut down the risk of dealing with failed payments later.

Slash Chargebacks and Shut Down Fraud

For any merchant, the word "chargeback" is enough to cause a headache. Pre-authorizing a card is a great first step in verifying its legitimacy, acting as a screen for potentially stolen card details. By simply confirming the card is active and has funds, you can filter out a chunk of fraudulent attempts right from the get-go.

This upfront check is a key part of a solid chargeback prevention strategy. While it won't stop every single dispute, it absolutely creates a more secure environment for every transaction you process.

The global credit card market is exploding, with transaction volume expected to hit a staggering $3.843 trillion by 2025. With that much money flying around, secure payments are non-negotiable. It’s no surprise that 78% of card issuers now use AI to detect fraud, which has helped slash fraud rates by 44%—especially in e-commerce, where pre-auth is king.

Guarantee Your Payment and Lock In Cash Flow

If you run a business that depends on appointments or custom orders, you know how much no-shows and last-minute cancellations can hurt your wallet. A pre-authorization gives you a reliable way to capture a cancellation fee or cover the cost of materials you've already bought.

It's a powerful way to secure your revenue. Think of it as a digital handshake that guarantees the customer has the funds set aside, protecting your cash flow from unexpected losses.

This is a game-changer for businesses like:

- Service Providers: Salons, consultants, and clinics can lock in a deposit or cancellation fee.

- Custom Shops: Anyone creating personalized products can make sure they get paid before starting the work.

- Rental Companies: Car rental agencies and equipment hire businesses can hold a security deposit for any potential damages.

If you're looking to weave pre-authorization into your online store, a good general e-commerce guide can offer a solid foundation on payment processing and other key strategies. At the end of the day, this simple financial tool doesn't just protect you—it makes your entire payment process cleaner and more predictable.

Implementing Pre-Authorization on Popular Platforms

Alright, so you see the value in pre-authorizations. The next logical question is, "How do I actually turn this on?"

The great news is you don't need to be a developer or a payments guru to pre-authorize a credit card. Most modern payment platforms have this feature built right in. It's often as simple as flipping a switch in your settings.

Instead of your system capturing the payment the second a customer clicks "buy," you can tell it to first authorize the card and then wait for you to manually capture the funds. Let's look at how this works on some of the biggest platforms merchants use every day.

Shopify Payments

If you're one of the millions of merchants on Shopify, setting this up is incredibly easy. By default, Shopify is set to automatically grab the payment. To change this, you just need to adjust one simple setting.

- Go to your Shopify admin dashboard and click on Settings.

- Navigate to the Payments section.

- Under "Shopify Payments," click Manage.

- Scroll down to the "Payment capture" section and select Manually capture payment for orders.

That’s it. Now, when an order comes in, the payment is only authorized. You'll then go into the order details and click "Capture payment" once you're ready to ship or finalize the sale.

Stripe

Stripe is the powerful engine behind countless payment systems, and it offers fantastic flexibility. To use pre-authorization, you essentially create a two-step payment process. Instead of creating a direct charge, you first create a "payment intent" and then capture it later.

While this can be done via their API for custom setups, many platforms that integrate with Stripe (like WooCommerce) have simple plugins or settings that let you enable "Authorization and Capture" without touching a single line of code. You just need to look for the payment action setting and switch it from "Charge" to "Authorize."

Pro Tip: Stripe authorizations typically expire after seven days. It's crucial to have a clear workflow to ensure you capture payments before the hold is released, or you'll lose the payment guarantee.

PayPal

PayPal also makes it easy to separate authorization from capture, which is essential for managing orders effectively. Much like the other platforms, you can configure your PayPal account to only authorize payments at checkout, giving you time to review the order before finalizing the charge.

For businesses looking for a robust solution, you can find a lot of information in our comprehensive guide on how PayPal Checkout works.

This is particularly useful for sellers who need to verify inventory or deal with custom products. Enabling this feature usually involves adjusting your payment settings within your PayPal business account or through the e-commerce platform you've connected it to.

Braintree

Owned by PayPal, Braintree is another popular choice, especially for businesses that need more advanced customization. It works a lot like Stripe. When processing a transaction, you have the option to submit it for settlement immediately or to just authorize it.

If you choose to only authorize, the transaction is verified and the hold is placed, but the funds aren't captured until you explicitly tell Braintree to do so. This is perfect for subscription models or businesses that need to confirm service delivery before billing.

Platform Pre-Authorization Feature Comparison

Choosing the right platform often comes down to the specifics. The table below breaks down how each of these major players handles pre-authorization, including how long the holds typically last.

As you can see, while the concept is the same across the board, the details like hold duration and setup can vary. Always double-check your platform's specific documentation to make sure your workflow aligns with their rules.

Best Practices for a Smooth Pre-Authorization Workflow

Just knowing how to pre authorize a credit card is only half the battle. Using this feature the right way is what really protects your business and keeps your customers happy. If you're sloppy with it, you'll end up with expired holds, confused customers, and lost sales.

The good news is, a few simple best practices can turn pre-authorization from just another tool into a powerhouse for your operation. It all comes down to being clear, timing things right, and getting your team on the same page.

Communicate Clearly with Your Customers

Transparency is your best friend here. Most shoppers have no idea what a "pending hold" is—they just see their available balance drop and assume the worst. A little bit of panic often follows.

You need to get ahead of this. A simple, clear message on your checkout page, in a confirmation email, or even on an FAQ page can save you from a mountain of support tickets.

Example Wording: "Please note: We will place a temporary hold on your card for the total amount. This is not a final charge, and your card will only be billed once your order ships. The hold will be released within 5-7 business days."

That one sentence builds trust and sets the right expectations from the get-go.

Keep a Close Eye on Hold Durations

Every pre-authorization has a ticking clock. For most platforms like Stripe and Shopify, that clock runs out in about seven days. If you don't capture the payment before that hold expires, the funds are released back to the customer, and your guarantee disappears with them.

To avoid this nightmare, you need a process for tracking your authorized orders. Set up reminders or use your platform’s order management system to flag any orders getting dangerously close to their deadline. This is an absolute must if you sell custom products or have longer shipping lead times. A missed capture forces you to go back to the customer and ask to run their card again, which is an easy way to lose a sale.

Develop a Solid Internal Policy

Your entire team needs to know exactly how and when to use pre-authorizations. Documenting a clear policy makes sure everyone is following the same playbook, creating a consistent experience for both your staff and your customers.

Your policy should nail down a few key things:

- When to Capture: Define the specific trigger for capturing the payment. Is it when the shipping label is printed? When the package leaves the warehouse? Be specific.

- Handling Partial Captures: Lay out the rules for split shipments. If you only ship one item from a larger order, you should only capture the cost of that specific item, leaving the rest of the hold active.

- Managing Cancellations: Make it a rule to immediately void authorizations for any cancelled orders. This frees up the customer's funds right away and prevents unnecessary frustration.

Creating these ground rules streamlines your whole operation and cuts down on human error. As an extra layer of protection, it’s also smart to understand how technologies like tokenization keep card data safe during this whole process. You can dive deeper into that with our guide on what tokenization in payments is.

Getting these practices right has never been more important. In the U.S. alone, the number of active credit card accounts shot up to 631.39 million in early 2025. With credit cards making up 35% of all payments and networks like Visa and Mastercard having over 2.4 billion cards out there globally, a bulletproof pre-authorization workflow is essential for keeping your risk low. You can find more details in these credit card trends and statistics.

FAQ

Even after you get the hang of how to pre-authorize a credit card, a few questions always seem to come up. Getting these common sticking points sorted out will help you handle every transaction with confidence. Let's dig into some of the most frequent questions we hear from merchants.

How Long Does a Pre-Authorization Hold Last on a Credit Card?

The lifespan of a pre-auth hold isn't set in stone. It usually hangs around for 5 to 7 days, but this can change depending on the customer's bank and your type of business.

For example, a hotel might place a hold that lasts for the guest's entire stay, plus a few extra days just in case. The most important thing for you is to capture the funds before that hold expires. If you wait too long, the authorization disappears, and the money is no longer guaranteed.

Miss that window, and you'll have to run the card all over again. That creates a brand new charge, which could easily get declined if the customer’s available credit has changed.

Does a Pre-Authorization Look Like a Real Charge on a Customer's Statement?

Yes, and this is probably the single biggest source of confusion for customers. When someone checks their online banking app, a pre-authorization almost always shows up as a "pending" transaction. To them, it looks exactly like a real charge.

This is why crystal-clear communication is so important. You have to let customers know it's just a temporary hold, not the final charge, and that the money hasn't actually left their account. Once you capture the final amount or let the hold expire, that pending item will vanish from their statement.

A simple heads-up can prevent a lot of customer service headaches. Explaining the process upfront shows transparency and helps your customers understand what’s happening with their account.

What Happens If a Pre-Authorized Payment Is Declined?

If your request to pre-authorize a card gets declined, that's an immediate red flag. The customer's bank is essentially telling you, "Nope, those funds aren't available." This usually happens for a few common reasons:

- Insufficient Funds: The customer doesn't have enough available credit to cover the hold amount.

- Incorrect Information: A simple typo in the card number, expiration date, or CVC.

- Fraud Alert: The bank's security system flagged the transaction as suspicious.

- Card Restrictions: The card might be expired, reported lost, or have other blocks on it.

When an authorization fails, the transaction stops right there. Your best move is to discreetly let the customer know their card was declined and ask for another way to pay.

Can I Pre-Authorize an Amount Different from the Final Charge?

Absolutely. In fact, this flexibility is one of the main reasons pre-authorization is so handy. It's the perfect tool for any situation where you don't know the final total at the time of purchase.

Think about a restaurant adding a tip, a hotel billing for room service, or a gas station charging for the exact amount of fuel pumped. In every case, you can pre-authorize an estimated amount and then capture the final, correct amount later.

There's just one key rule to remember: you generally cannot capture more than the amount you originally pre-authorized. If the final bill ends up being higher, you’ll probably need to run a second, separate transaction for the difference.

Navigating the world of payments and chargebacks can be tricky, but you don't have to do it alone. ChargePay uses AI to automate the entire chargeback dispute process, helping you recover lost revenue without lifting a finger. See how our hands-free solution can boost your win rates and protect your bottom line by visiting https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)